Exam 5: Inventory

Exam 1: Business, Accounting, and You148 Questions

Exam 2: Analyzing and Recording Business Transactions146 Questions

Exam 3: Adjusting and Closing Entries149 Questions

Exam 4: Accounting for a Merchandising Business149 Questions

Exam 5: Inventory152 Questions

Exam 6: The Challenges of Accounting: Standards, internal Control, audits, fraud, and Ethics139 Questions

Exam 7: Cash and Receivables166 Questions

Exam 8: Long-Term and Other Assets169 Questions

Exam 9: Current Liabilities and Long-Term Debt167 Questions

Exam 10: Corporations: Paid-In Capital and Retained Earnings160 Questions

Exam 11: The Statement of Cash Flows133 Questions

Exam 12: Financial Statement Analysis159 Questions

Select questions type

Inventory turnover equals average ending inventory divided by cost of goods sold.

(True/False)

4.7/5  (44)

(44)

The second step in using the gross profit method to estimate ending inventory is to:

(Multiple Choice)

4.9/5 (42)

Beginning inventory plus net purchases equals cost of goods sold.

(True/False)

4.9/5 (40)

Inventory is probably the retailer's smallest (by value)current asset.

(True/False)

4.8/5 (40)

The Vintage Showroom,an antique shop,would most likely use the FIFO method of accounting for inventory.

(True/False)

5.0/5 (30)

A method of valuing inventory based on the assumption that the newest goods will be sold first is called the:

(Multiple Choice)

4.7/5 (33)

An ending inventory error in one year does not have any effect on the inventory at the start of the next year.

(True/False)

4.8/5 (44)

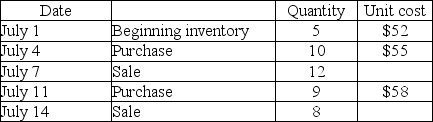

Lionworks Enterprises had the following inventory data:

Assuming average cost,what is the cost of goods sold for the July 14 sale?

Assuming average cost,what is the cost of goods sold for the July 14 sale?

(Multiple Choice)

4.9/5 (46)

The historical gross profit percentage can be used to estimate the current period's gross profit.

(True/False)

5.0/5 (50)

Making notes in the financial statements to explain the justification of valuation changes and other financial decisions would be an example of:

(Multiple Choice)

4.7/5 (39)

The sum of ending inventory and cost of goods available for sale equals cost of goods sold.

(True/False)

4.7/5 (39)

Companies that want a "middle ground" solution to net income and the amount of income taxes that the company will pay will value their inventory at:

(Multiple Choice)

4.8/5 (39)

When using the LIFO inventory method,the ending inventory has the newer,higher costs.

(True/False)

4.9/5 (36)

In order to pay the least income tax possible in periods of constant costs,the company should use which of the following inventory costing methods?

(Multiple Choice)

4.9/5 (37)

If gross profit is overstated in Period 1,then the ending inventory and net income in Period 1 were respectively:

(Multiple Choice)

4.9/5 (37)

When purchasing inventory on account in a perpetual inventory system,which of the following is TRUE?

(Multiple Choice)

4.8/5 (47)

When using LIFO,an accounting department only needs to know:

(Multiple Choice)

4.9/5 (35)

Cost of goods available for sale minus estimated Cost of Goods Sold yields the estimated:

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)