Exam 15: Cost Allocation: Joint Products and Byproducts

Exam 1: The Accountants Vital Role in Decision Making171 Questions

Exam 2: An Introduction to Cost Terms and Purposes202 Questions

Exam 3: Cost-Volume-Profit Analysis165 Questions

Exam 4: Job Costing161 Questions

Exam 5: Activity-Based Costing and Management160 Questions

Exam 6: Master Budget and Responsibility Accounting179 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I190 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II156 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation178 Questions

Exam 10: Analysis of Cost Behaviour251 Questions

Exam 11: Decision Making and Relevant Information194 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management160 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis152 Questions

Exam 14: Period Cost Allocation180 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts192 Questions

Exam 16: Revenue and Customer Profitability Analysis165 Questions

Exam 17: Process Costing155 Questions

Exam 18: Spoilage, Rework, and Scrap155 Questions

Exam 19: Inventory Cost Management Strategies161 Questions

Exam 20: Capital Budgeting: Methods of Investment Analysis196 Questions

Exam 21: Transfer Pricing and Multinational Management Control Systems183 Questions

Exam 22: Multinational Performance Measurement and Compensation166 Questions

Select questions type

The net realizable value method is generally used for products or services that are processed and after splitoff additional value is added to the product and a selling price can be determined.

(True/False)

4.8/5  (40)

(40)

One problem with the physical measure method of allocation is that the physical weights used for allocating joint costs may have no relation to the product's ability to produce revenue.

(True/False)

4.7/5 (39)

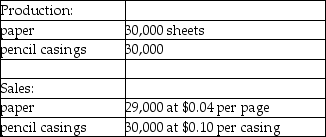

Use the information below to answer the following question(s).Raynor Manufacturing purchases trees from Tree Nursery and processes them up to the splitoff point, where two products (paper and pencil casings)are obtained.The products are then sold to an independent company that markets and distributes them to retail outlets.The following information was collected for the month of October.Trees processed:

50 trees (yield is 30,000 sheets of paper and 30,000 pencil casings and no scrap)

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-Which method allocates joint costs on the basis of each product's relative sales value at the splitoff point?

Cost of purchasing 50 trees and processing them up to the splitoff point to yield 30,000 sheets of paper and 30,000 pencil casings is $1,500.Raynor Manufacturing's accounting department reported no beginning inventories; however, ending inventory amounts reflected 1,000 sheets of paper in stock.

-Which method allocates joint costs on the basis of each product's relative sales value at the splitoff point?

(Multiple Choice)

4.9/5 (38)

When a single manufacturing process yields two products, one of which has a relatively high sales value compared to the other, the two products are respectively known as

(Multiple Choice)

4.8/5 (31)

All of the following methods may be used to allocate joint costs EXCEPT the

(Multiple Choice)

4.9/5 (38)

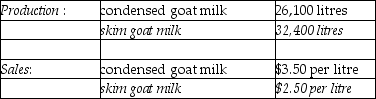

Answer the following question(s)using the information below:

The Morton Company processes unprocessed goat milk up to the splitoff point where two products, condensed goat milk and skim goat milk result.The following information was collected for the month of October:

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240.There were no inventory balances of either product.Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage)of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre.Xyla can be sold for $18 per litre.Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50.The product can be sold for $9 per litre.There are no beginning and ending inventory balances.

-Which method of allocating costs would be used if the selling prices of all products at the splitoff point are unavailable?

The costs of purchasing the 65,000 litres of unprocessed goat milk and processing it up to the splitoff point to yield a total of 58,500 litres of salable product was $72,240.There were no inventory balances of either product.Condensed goat milk may be processed further to yield 19,500 litres (the remainder is shrinkage)of a medicinal milk product, Xyla, for an additional processing cost of $3 per usable litre.Xyla can be sold for $18 per litre.Skim goat milk can be processed further to yield 28,100 litres of skim goat ice cream, for an additional processing cost per usable litre of $2.50.The product can be sold for $9 per litre.There are no beginning and ending inventory balances.

-Which method of allocating costs would be used if the selling prices of all products at the splitoff point are unavailable?

(Multiple Choice)

4.8/5 (44)

Match each of the following costs with the appropriate joint production process cost classification.

A)separable cost

B)joint cost

-Cost of processing crude oil in a gasoline refinery.

(Short Answer)

4.8/5 (40)

Use the information below to answer the following question(s).Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y)are obtained and sold.The following information was collected for the month of November.Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.The beginning inventories totalled 50 litres for X and 25 litres for Y.Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y.October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.The beginning inventories totalled 50 litres for X and 25 litres for Y.Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y.October costs were per unit were the same as November.

-What are the respective physical volume proportions for products X and Y?

(Multiple Choice)

4.9/5 (41)

If managers make processing or selling decisions using incremental revenue/incremental cost approach, which of the following statements is TRUE?

(Multiple Choice)

4.8/5 (43)

Use the information below to answer the following question(s):

Orange Paper Company processes wood pulp into two products.During February the joint costs of processing were $156,000.Production and sales value information for the month were as follows:

Paper sells for $2.85 a kilogram and cardboard sells for $3.90 a kilogram.There were no beginning inventories for April but ending inventories totalled 15,000 kilograms for paper and 18,000 kilograms for cardboard.

-How much of the Orange Paper Company joint costs should be allocated to the cardboard using the net realizable value method based on total production?

Paper sells for $2.85 a kilogram and cardboard sells for $3.90 a kilogram.There were no beginning inventories for April but ending inventories totalled 15,000 kilograms for paper and 18,000 kilograms for cardboard.

-How much of the Orange Paper Company joint costs should be allocated to the cardboard using the net realizable value method based on total production?

(Multiple Choice)

4.8/5 (37)

Use the information below to answer the following question(s).Beverage Drink Company processes direct materials up to the splitoff point, where two products, A and B, are obtained.The following information was collected for the month of July:

Direct materials processed: 2,500 litres (with 20 percent shrinkage)

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500.There were no inventory balances of A and B.Product A may be processed further to yield 1,375 litres of Product Z5 for an additional processing cost of $150.Product Z5 is sold for $25.00 per litre.There was no beginning inventory and ending inventory was 125 litres.Product B may be processed further to yield 375 litres of Product W3 for an additional processing cost of $275.Product W3 is sold for $30.00 per litre.There was no beginning inventory and ending inventory was 25 litres.

-What is Product Z5's estimated net realizable value?

Cost of purchasing 2,500 litres of direct materials and processing it up to the splitoff point to yield a total of 2,000 litres of good products was $4,500.There were no inventory balances of A and B.Product A may be processed further to yield 1,375 litres of Product Z5 for an additional processing cost of $150.Product Z5 is sold for $25.00 per litre.There was no beginning inventory and ending inventory was 125 litres.Product B may be processed further to yield 375 litres of Product W3 for an additional processing cost of $275.Product W3 is sold for $30.00 per litre.There was no beginning inventory and ending inventory was 25 litres.

-What is Product Z5's estimated net realizable value?

(Multiple Choice)

4.8/5 (37)

The estimated net realizable value method allocates joint costs on the basis of the expected final sales value in the ordinary course of business, less the expected separable costs of production and marketing of the total production for the period.

(True/False)

5.0/5 (33)

Use the information below to answer the following question(s).Cranbrook Chemical Ltd.manufactures two industrial compounds.In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000.The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton.The respective selling prices of Jarlon and Kharton are $38 and $58.Both products may be processed further.Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product.The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively.The selling price of Jaxton is $48 per jar.The selling price of Kraxton is $102 per jar.

-Assuming Cranbrook uses the sales value at splitoff method and 2,000 containers of Jarlon and 75 containers of Kharton are unsold at the end of the period, Cranbrook would report ending inventory of

(Multiple Choice)

4.7/5 (38)

Byproducts are recognized in the general ledger either at the time of production or at the time of sale.

(True/False)

4.9/5 (41)

Use the information below to answer the following question(s).Cranbrook Chemical Ltd.manufactures two industrial compounds.In the month of May, 15,000 litres of direct material costing $160,000 were processed at a cost of $400,000.The joint process yielded 16,000 containers of a compound known as Jarlon and 4,000 containers of a compound known as Kharton.The respective selling prices of Jarlon and Kharton are $38 and $58.Both products may be processed further.Jarlon may be processed into Jaxton at an incremental cost of $8 per jar of the final product while Kharton may be processed into Kraxton at an additional cost of $32 per jar of the final product.The volume of jars of the final product are: 12,000 and 3,000 for Jaxton and Kraxton respectively.The selling price of Jaxton is $48 per jar.The selling price of Kraxton is $102 per jar.

-Using the physical measures method, the joint costs allocated to Kharton would be

(Multiple Choice)

4.7/5 (36)

Use the information below to answer the following question(s).Chem Manufacturing Company processes direct materials up to the splitoff point, where two products (X and Y)are obtained and sold.The following information was collected for the month of November.Direct materials processed:

10,000 litres (10,000 litres yield 9,500 litres of good product and 500 litres of shrinkage)

The cost of purchasing 10,000 litres of direct materials and processing it up to the splitoff point to yield a total of 9,500 litres of good products was $975,000.The beginning inventories totalled 50 litres for X and 25 litres for Y.Ending inventory amounts reflected 300 litres of product X and 525 litres of product Y.October costs were per unit were the same as November.

-An advantage of the sales value at splitoff method is

(Multiple Choice)

4.9/5 (27)

The Organic Milk Company produces three products from a joint processes using whole milk: butter, cheese, and cream.The joint costs amount to $24,000 per batch of output.Each batch totals 50,000 litres: 25% butter, 25% cheese, 50% cream.All products are processed further without gain or loss in volume.Separable costs are butter, $0.50 per litre; cheese, $2.00 per litre; cream, $0.25 per litre.The selling prices per litre are respectively: $3.50, $6.00, $4.00.Required:

1.How much joint cost per batch should be allocated to cream, assuming that joint costs are allocated on a physical measure basis?

2.If joint costs are assigned on a net realizable value basis, how much joint cost should be allocated to cheese?

3.An organic grocer has offered to buy all of the cheese produced at $5.50 per litre.Traditionally 90% of the cheese production is sold.How much better or worse off financially is the company from accepting this offer?

(Essay)

4.7/5 (32)

Match each of the following costs with the appropriate joint production process cost classification.

A)separable cost

B)joint cost

-Cost of canning soup in a soup plant.

(Short Answer)

4.8/5 (38)

Use the information below to answer the following question(s).Troy Company processes 15,000 litres of direct materials to produce two products, Product X and Product Y.Product X, a byproduct, sells for $4 per litre, and Product Y, the main product, sells for $50 per litre.The following information is for August:

The manufacturing costs totalled $95,000.

-How much is the ending inventory for the byproduct if byproducts are recognized in the general ledger when production is completed?

The manufacturing costs totalled $95,000.

-How much is the ending inventory for the byproduct if byproducts are recognized in the general ledger when production is completed?

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)