Exam 27: Cost Management for Just-In-Time Environments

Exam 1: Introduction to Accounting and Business188 Questions

Exam 2: Analyzing Transactions216 Questions

Exam 3: The Adjusting Process179 Questions

Exam 4: Completing the Accounting Cycle198 Questions

Exam 5: Accounting for Merchandising Businesses220 Questions

Exam 6: Inventories170 Questions

Exam 7: Sarbanes-Oxley, Internal Control, and Cash178 Questions

Exam 8: Receivables148 Questions

Exam 9: Fixed Assets and Intangible Assets177 Questions

Exam 10: Current Liabilities and Payroll174 Questions

Exam 11: Corporations: Organization, Stock Transactions, and Dividends172 Questions

Exam 12: Long-Term Liabilities: Bonds and Notes186 Questions

Exam 13: Investments and Fair Value Accounting133 Questions

Exam 14: Statement of Cash Flows161 Questions

Exam 15: Financial Statement Analysis184 Questions

Exam 16: Managerial Accounting Concepts and Principles175 Questions

Exam 17: Job Order Costing176 Questions

Exam 18: Process Cost Systems177 Questions

Exam 19: Cost Behavior and Cost-Volume-Profit Analysis215 Questions

Exam 20: Variable Costing for Management Analysis154 Questions

Exam 21: Budgeting185 Questions

Exam 22: Performance Evaluation Using Variances From Standard Costs160 Questions

Exam 23: Performance Evaluation for Decentralized Operations198 Questions

Exam 24: Differential Analysis and Product Pricing161 Questions

Exam 25: Capital Investment Analysis179 Questions

Exam 26: Cost Allocation and Activity-Based Costing111 Questions

Exam 27: Cost Management for Just-In-Time Environments122 Questions

Select questions type

Connally Company's payroll department required that every time card be checked twice to ensure pay accuracy. The company has 1,000 employees and has determined that the checks cost the company $8,000 per year. They have decided to change this policy and only check those names which appear on the exceptions report and a random check on the entire payroll. Currently only 15% of the payroll is evaluated each payroll. Determine the inspection activity cost per employee on the 1,000 employees both before and after the improvement.

(Essay)

4.9/5  (34)

(34)

Examples of transforming a traditional manufacturing environment to a just-in-time environment is to do all of the following except

(Multiple Choice)

4.9/5 (32)

In a just-in-time (JIT) environment, the journal entry to record conversion costs would include a debit to the raw and in process inventory account.

(True/False)

4.9/5 (45)

In a just-in-time (JIT) environment, raw materials are delivered less frequently than in a traditional environment.

(True/False)

4.7/5 (41)

Push manufacturing is also referred to as make-to-order processing.

(True/False)

4.9/5 (47)

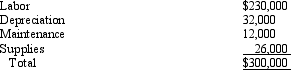

Cariboo Pattern Company makes dressmakers' patterns using a machine that stamps the pattern outline onto tissue paper. The stamping center produced 40,000 patterns in August, with a machine time per pattern of 20 seconds. Annual budgeted cell conversion costs were as follows:

Cariboo planned 2,500 total machine hours for the year.

Calculate Cariboo's budgeted cell conversion cost rate for the year.

Cariboo planned 2,500 total machine hours for the year.

Calculate Cariboo's budgeted cell conversion cost rate for the year.

(Essay)

4.9/5 (30)

Axelgold Company produces parts for the auto industry. Part X2 is machined in Department #1, which has the following budgeted conversion costs:

All costs are driven by machine hours. Total possible hours for the year are 2,800. It takes .03 hours to machine one unit of Part X2.

All costs are driven by machine hours. Total possible hours for the year are 2,800. It takes .03 hours to machine one unit of Part X2.

(Essay)

4.7/5 (33)

Logan Electronics Corporation manufactures and assembles electronic motor drives for video cameras. The company assembles the motor drives for several accounts. The process consists of a just-in-time cell for each customer. The following information relates only to one customer's just-in-time cell. For the year planned labor and overhead was $76,800,000; materials costs, $25 per unit. Planned production included 9,600 hours to produce 76,800 motor drives. Actual production for the month of August was 5,200 units, and motor drives shipped amounted to 5,040 units. From the foregoing information, determine the budgeted cell conversion cost per hour.

(Multiple Choice)

4.8/5 (28)

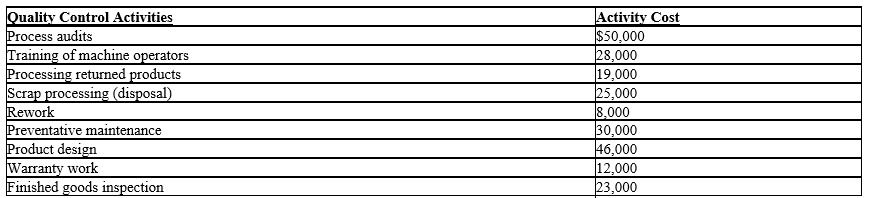

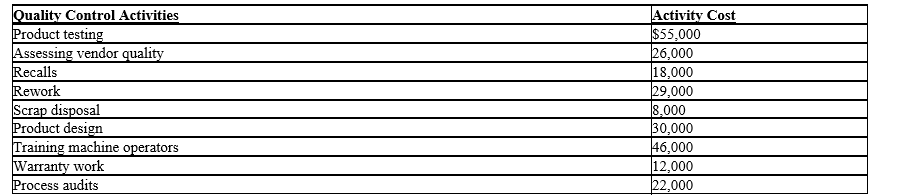

Schedule of Activity Costs  From the above schedule of activity costs, determine the internal failure costs.

From the above schedule of activity costs, determine the internal failure costs.

(Multiple Choice)

4.9/5 (34)

Just-in-time manufacturing philosophy reduces all of the following except

(Multiple Choice)

4.8/5 (34)

Sifton Electronics Corporation manufactures and assembles electronic motor drives for video cameras. The company assembles the motor drives for several accounts. The process consists of a just-in-time cell for each customer. The following information relates only to one customer's just-in-time cell for the coming year. Projected labor and overhead, $7,370,000; materials costs, $28 per unit. Planned production included 4,000 hours to produce 27,500 motor drives. Actual production for August was 1,600 units, and motor drives shipped amounted to 1,380 units. From the foregoing information, determine the manufacturing cost per unit.

(Multiple Choice)

4.8/5 (35)

A backflush accounting system uses work in process inventories as control points between each process step.

(True/False)

4.9/5 (43)

Schedule of Activity Costs From the above schedule of activity costs, determine the prevention costs.

(Multiple Choice)

4.7/5 (34)

Schedule of Activity Costs

From the above schedule, compute the percentage of non-value-added activities.

From the above schedule, compute the percentage of non-value-added activities.

(Essay)

4.8/5 (40)

A process-oriented layout segments production facilities into functional departments.

(True/False)

4.9/5 (41)

Prevention costs and appraisal costs are considered costs of controlling quality.

(True/False)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)