Exam 3: Principles of Option Pricing

Exam 1: Introduction40 Questions

Exam 2: Structure of Options Markets65 Questions

Exam 3: Principles of Option Pricing60 Questions

Exam 4: Option Pricing Models: The Binomial Model60 Questions

Exam 5: Option Pricing Models: The Black-Scholes-Merton Model60 Questions

Exam 6: Basic Option Strategies60 Questions

Exam 7: Advanced Option Strategies60 Questions

Exam 8: Structure of Forward and Futures Markets61 Questions

Exam 9: Principles of Pricing Forwards, Futures and Options on Futures60 Questions

Exam 10: Futures Arbitrage Strategies59 Questions

Exam 11: Forward and Futures Hedging, Spread, and Target Strategies60 Questions

Exam 12: Swaps60 Questions

Exam 13: Interest Rate Forwards and Options60 Questions

Exam 14: Advanced Derivatives and Strategies60 Questions

Exam 15: Financial Risk Management Techniques and Appplications60 Questions

Exam 16: Managing Risk in an Organization60 Questions

Select questions type

The put-call parity rule for American options is stated as equalities.

(True/False)

4.9/5  (24)

(24)

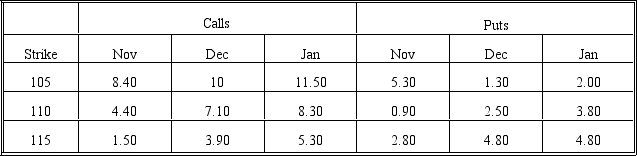

The following quotes were observed for options on a given stock on November 1 of a given year. These are American calls except where indicated. Use the information to answer questions 7 through 20.

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-What is the intrinsic value of the December 115 put?

The stock price was 113.25. The risk-free rates were 7.30 percent (November), 7.50 percent (December) and 7.62 percent (January). The times to expiration were 0.0384 (November), 0.1342 (December), and 0.211 (January). Assume no dividends unless indicated.

-What is the intrinsic value of the December 115 put?

(Multiple Choice)

4.9/5 (35)

The difference between a Treasury bill's face value and its price is called the

(Multiple Choice)

4.7/5 (42)

The price of a call option is directly related to interest rates.

(True/False)

4.7/5 (44)

The lower the exercise price, the more valuable the call option.

(True/False)

4.9/5 (31)

Which of the following inequalities correctly states the relationship between the difference in the prices of two European calls that differ only by exercise price

(Multiple Choice)

4.9/5 (30)

Suppose you use put-call parity to compute a European call price from the European put price, the stock price, and the risk-free rate. You find the market price of the call to be less than the price given by put-call parity. Ignoring transaction costs, what trades should you do?

(Multiple Choice)

4.7/5 (43)

An option can be priced at less than zero because it can potentially generate a large profit for its owner.

(True/False)

4.7/5 (34)

The difference between two American put options with different strike prices is less than or equal to the dollar difference between the strike prices, the higher strike price minus the lower strike price.

(True/False)

4.8/5 (40)

A stock is equivalent to a long call, short put and long risk-free bond.

(True/False)

4.8/5 (38)

The difference between an American call's price and its intrinsic value is called the time value because the call can be exercised at any time.

(True/False)

4.8/5 (38)

A situation in which early exercise of an American put can be justified is

(Multiple Choice)

4.8/5 (44)

Even if there are no dividends on the stock, American put-call parity will not be the same as European put-call parity.

(True/False)

4.9/5 (43)

The lower bound of a European put on a non-dividend paying stock is lower than the intrinsic value of an American put.

(True/False)

4.8/5 (35)

Given a longer-lived American call and a shorter-lived American call with the same terms, the longer-lived call must always be worth

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)