Exam 3: The Basics of Record Keeping and Financial Statement Preparation: Income Statement

Exam 1: Introduction to Business Activities and Overview of Financial Statements and the Reporting Process139 Questions

Exam 2: The Basics of Record Keeping and Financial Statement Preparation: Balance Sheet115 Questions

Exam 3: The Basics of Record Keeping and Financial Statement Preparation: Income Statement129 Questions

Exam 4: Balance Sheet: Presenting and Analyzing Resources and Financing120 Questions

Exam 5: Income Statement: Reporting Results of Operating Activities109 Questions

Exam 6: Statement of Cash Flows140 Questions

Exam 7: Introduction to Financial Statement Analysis166 Questions

Exam 8: Revenue Recognition, Receivables, and Advances From Customers138 Questions

Exam 9: Working Capital167 Questions

Exam 10: Long-Lived Tangible and Intangible Assets182 Questions

Exam 11: Notes, Bonds, and Leases139 Questions

Exam 12: Liabilities: Off-Balance Sheet Financing, Retirement Benefits, and Income Taxes117 Questions

Exam 13: Marketable Securities and Derivatives144 Questions

Exam 14: Intercorporate Investments in Common Stock103 Questions

Exam 15: Shareholders Equity: Capital Contributions and Distributions199 Questions

Exam 16: Statement of Cash Flows: Another Look146 Questions

Exam 17: Synthesis and Extensions246 Questions

Select questions type

Current accounting practice takes the viewpoint of shareholders by reporting the amount of net income available to shareholders after subtracting from revenues all expenses incurred in generating the revenue by claimants (for example, employees, lenders, governments) other than shareholders.

(True/False)

4.8/5  (33)

(33)

The result of closing entries is that balances in all temporary accounts

(Multiple Choice)

4.9/5 (37)

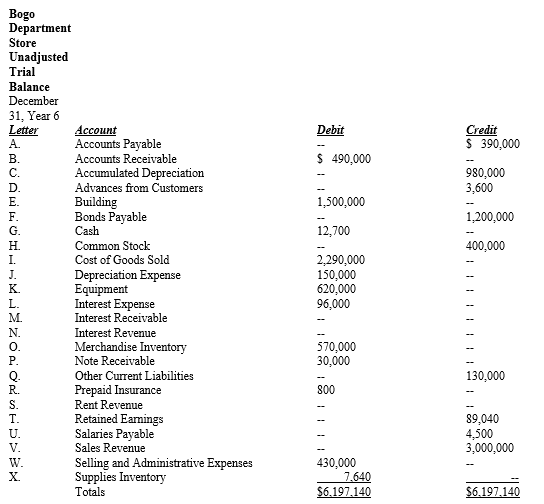

On the next page is the unadjusted trial balance of Bogo Department Store on December 31, Year 6.The company closes its books annually.You are asked to indicate the adjusting entries required on December 31, Year 6 to conform the books to accrual accounting principles.

1. Bogo neglected to record unpaid charges for telephone services for December in the amount of $13,700.

2. The balance in the Advances from Customers account represents the amount received from a lessee on November 1, Year 6 for the rental of excess warehouse space owned by Bogo. The rental period is for the six months ended April 30, Year 7.

3. Bogo acquired a warehouse on July 1, Year 6 and correctly recorded the acquisition cost of $600,000 in its accounts. The warehouse has a 30-year estimated life and zero salvage value. Bogo neglected to record depreciation on the warehouse, although it has correctly recorded depreciation on all other depreciable assets for Year 6.

4. Bogo debited Selling and Administrative Expenses for salaries paid during Year 6. Salaries remaining unpaid as of December 31, Year 6 total $3,700.

5. Sales made on account during the last two days of December, Year 6 totaled $12,000. Bogo incorrectly recorded these sales by debiting accounts payable. These accounts had not been collected by year end.

6. Bogo sold a piece of equipment during Year 6 for $1,800 that had originally cost $6,000 and had accumulated depreciation of $4,200. Bogo recorded this sale by debiting Cash for $1,800 and crediting Equipment for $1,800.

7. The balance in the Prepaid Insurance account represents the balance as of January 1, Year 6. Bogo renewed its only insurance policy on March 1, Year 6 and charged the one-year premium of $5,100 to Selling and Administrative Expenses.

8. A physical inventory of store supplies on December 31, Year 6 revealed that supplies costing $1,850 were on hand.

9. The note receivable was received from a corporate officer on December 1, Year 6. The note bears interest at 6 percent. The interest is payable with the principal amount borrowed at maturity on June 1, Year 7.

Required:

Indicate the letters in the unadjusted trial balance corresponding to the accounts debited and credited and the amount in each debit and credit entry.Use only the accounts listed in the unadjusted trial balance.More than one account may be debited or credited in a particular adjusting entry.If no adjusting entry is needed, indicate "No Entry" by the number of the entry.Remember that asset increases and liability and shareholders' equity decreases are recorded with debits and asset decreases and liability and shareholders' equity increases are recorded with credits.

Required:

Indicate the letters in the unadjusted trial balance corresponding to the accounts debited and credited and the amount in each debit and credit entry.Use only the accounts listed in the unadjusted trial balance.More than one account may be debited or credited in a particular adjusting entry.If no adjusting entry is needed, indicate "No Entry" by the number of the entry.Remember that asset increases and liability and shareholders' equity decreases are recorded with debits and asset decreases and liability and shareholders' equity increases are recorded with credits.

(Essay)

4.8/5 (37)

The following balances have been excerpted from Bain balance sheets: December 31, 2014 December 31,2013 Prepaid Insurance 66,000 \ 7,500 Interest Receivable 3,700 14,500 Salaries Payable 61,500 53,000 Bain Company paid or collected during 2014 the following items: Insurance premiums paid. \4 1,500 Interest collected 123,500 Salaries paid 481,000 The salary expense on the income statement for 2014 was

(Multiple Choice)

4.9/5 (31)

Expenses provide future benefits, and assets measure the consumption of those benefits.

(True/False)

4.9/5 (38)

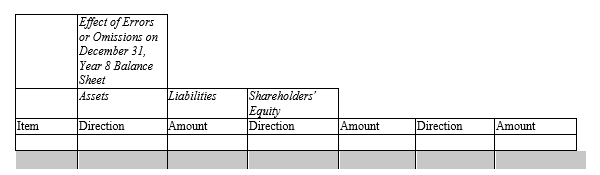

Humana Corporation neglected to make various adjusting entries on December 31, Year 8.Indicate the effects on assets, liabilities, and shareholders' equity on December 31, Year 8 of failing to adjust for the following independent items as appropriate, using the notation O/S (overstated), U/S (understated), and No (no effect).Also, give the amount of the effect.Ignore income tax implications.Use the following format:

a. On December 15, Year 8, Humana Corporation received a $1,400 advance from a customer for products to be manufactured and delivered in January, Year 9. The firm recorded the advance by debiting Cash and crediting Sales Revenue and has made no adjusting entry as of December 31, Year 8.

b. On July 1, Year 8, Humana Corporation acquired a machine for $5,000 and recorded the acquisition by debiting Cost of Goods Sold and crediting Cash. The machine has a five-year useful life and zero estimated salvage value.

c. On November 1, Year 8, Humana Corporation received a $2,000 note receivable from a customer in settlement of an accounts receivable. It debited Notes Receivable and credited Accounts Receivable upon receipt of the note. The note is a six-month note due April 30, Year 9 and bears interest at an annual rate of 12 percent. Humana Corporation made no other entries related to this note during Year 8.

d. Humana Corporation paid its annual insurance premium of $1,200 on October 1, Year 8, the first day of the year of coverage. It debited Prepaid Insurance $900, debited Insurance Expense $300, and credited Cash for $1,200. It made no other entries related to this insurance during Year 8.

e. The Board of Directors of Humana Corporation declared a dividend of $1,500 on December 31, Year 8. The dividend will be paid on January 15, Year 9. Humana Corporation neglected to record the dividend declaration.

f. On December 1, Year 8, Humana Corporation purchased a machine on account for $50,000, debiting Machinery and crediting Accounts Payable for $50,000. Ten days later, the account was paid and the company took the allowed 2 percent discount. Cash was credited $49,000, Miscellaneous Revenue was credited $1,000, and Accounts Payable was debited $50,000. It is the policy of Humana Corporation to record cash discounts taken as a reduction in the cost of assets. On December 28, Year 8, the machine was installed for $4,000 in cash; Maintenance Expense was debited and Cash was credited for $4,000. The machine started operation on January 1, Year 9. As the machine was not placed into operation until January 1, Year 9, as appropriate, no depreciation expense was recorded for Year 8.

a. On December 15, Year 8, Humana Corporation received a $1,400 advance from a customer for products to be manufactured and delivered in January, Year 9. The firm recorded the advance by debiting Cash and crediting Sales Revenue and has made no adjusting entry as of December 31, Year 8.

b. On July 1, Year 8, Humana Corporation acquired a machine for $5,000 and recorded the acquisition by debiting Cost of Goods Sold and crediting Cash. The machine has a five-year useful life and zero estimated salvage value.

c. On November 1, Year 8, Humana Corporation received a $2,000 note receivable from a customer in settlement of an accounts receivable. It debited Notes Receivable and credited Accounts Receivable upon receipt of the note. The note is a six-month note due April 30, Year 9 and bears interest at an annual rate of 12 percent. Humana Corporation made no other entries related to this note during Year 8.

d. Humana Corporation paid its annual insurance premium of $1,200 on October 1, Year 8, the first day of the year of coverage. It debited Prepaid Insurance $900, debited Insurance Expense $300, and credited Cash for $1,200. It made no other entries related to this insurance during Year 8.

e. The Board of Directors of Humana Corporation declared a dividend of $1,500 on December 31, Year 8. The dividend will be paid on January 15, Year 9. Humana Corporation neglected to record the dividend declaration.

f. On December 1, Year 8, Humana Corporation purchased a machine on account for $50,000, debiting Machinery and crediting Accounts Payable for $50,000. Ten days later, the account was paid and the company took the allowed 2 percent discount. Cash was credited $49,000, Miscellaneous Revenue was credited $1,000, and Accounts Payable was debited $50,000. It is the policy of Humana Corporation to record cash discounts taken as a reduction in the cost of assets. On December 28, Year 8, the machine was installed for $4,000 in cash; Maintenance Expense was debited and Cash was credited for $4,000. The machine started operation on January 1, Year 9. As the machine was not placed into operation until January 1, Year 9, as appropriate, no depreciation expense was recorded for Year 8.

(Essay)

5.0/5 (38)

Entries for the following items were either omitted or recorded incorrectly in preparing the financial statements for Year 3.Indicate the amount and nature [understatement (U), overstatement (O), no effect (N)] of the effect of the omission on total assets, total liabilities, and net income for Year 3.Ignore income tax effects.Use the following format:

a. On December 1, Year 3, a firm debits Prepaid Rent (Advances to Car Rental Agency) for $600 for 6 months' rent on an automobile. The firm has neglected to make the adjusting entry on December 31.

b. A firm debits Administrative Expenses for $6,000 for a microcomputer acquired on July 1, Year 3. The microcomputer has an expected useful life of 3 years and zero estimated salvage value.

c. A firm rents out excess office space for the 6-month period beginning January 1, Year 3. It received the rental check for this period of $600 on December 26, Year 2, and correctly credited Advances from Tenants. It made no further journal entries during Year 3.

d. Interest on Notes Receivable of $500 had accrued by December 31, Year 3, but the firm overlooked making an entry to record this interest.

e. A firm receives a check for $250 from a customer on December 31, Year 3, in settlement of an account receivable. The firm recorded this entry with a credit to Sales.

f. A firm records as $470 an expenditure of $740 for travel during December, Year 3.

(Essay)

4.9/5 (41)

Certain merchandise that a firm may acquire may be inventory or supplies.Accounting treats them differently as to the matching criteria used.

Required:

a.Describe the situation where merchandise would be considered inventory. How would the firm account for the costs of the merchandise?

b.Describe the situation where merchandise would be considered supplies. How would the firm account for the costs of the merchandise?

(Essay)

4.8/5 (31)

Adjusting entries are part of the measurement of net income for the period and financial position at the end of the period.

(True/False)

4.9/5 (42)

The _____ convention, links the timing of some expenses with revenue recognition.

(Multiple Choice)

4.9/5 (47)

Which financial statement reports operating performance for a specific period of time?

(Multiple Choice)

4.7/5 (40)

If an expense has been incurred but not yet recorded, then the end-of-period adjusting entry would involve

(Multiple Choice)

4.8/5 (37)

Failure to record the expired amount of prepaid rent expense would not

(Multiple Choice)

4.8/5 (45)

The Supplies account balance at the beginning of the period was $6,600.Supplies totaling $12,825 were purchased during the period and debited to Supplies .A physical count shows $3,825 of Supplies at the end of the period.The proper journal entry at the end of the period

(Multiple Choice)

4.7/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)