Exam 8: Cost-Based Inventories and Cost of Sales

Exam 1: The Framework for Financial Reporting84 Questions

Exam 2: Accounting Judgements142 Questions

Exam 3: Statements of Income and Comprehensive Income133 Questions

Exam 4: Statements of Financial Position and Changes in Equity; Disclosure Notes144 Questions

Exam 5: The Statement of Cash Flows178 Questions

Exam 6: Revenue Recognition156 Questions

Exam 7: Financial Assets: Cash and Receivables126 Questions

Exam 8: Cost-Based Inventories and Cost of Sales177 Questions

Exam 9: Long-Lived Assets208 Questions

Exam 10: Depreciation, Amortization, and Impairment174 Questions

Exam 11: Financial Instruments: Investments in Bonds and Equity Securities128 Questions

Select questions type

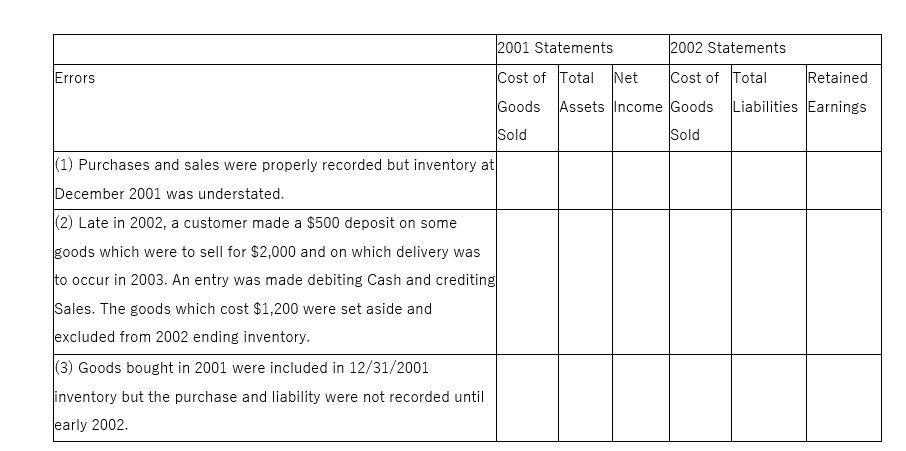

Use a "+" to denote an item is too high as a result of an error, a "-" to denote too low, and a 0 to indicate no effect. What is the effect of each of the following errors on the financial statements of a company, which uses a periodic inventory system?

(Essay)

4.9/5  (27)

(27)

Once biological assets are ready for sale, they have effectively become inventory and are then measured at the lower of their cost and net realizable value (NRV).

(True/False)

4.8/5 (32)

ABC Inc. had net sales of $120,000 during 2013. Its finished goods inventories were valued at $20,000 on January 1st, 2013. During the year, $60,000 of goods was purchased for resale. The company has a gross profit percentage of 40%. What was the company's cost of goods sold for 2013?

(Multiple Choice)

4.7/5 (33)

If purchases made in one year are mistakenly recorded the following year, this error will counterbalance, that is, there will be no effect on income over a 2-year period.

(True/False)

4.8/5 (44)

A company purchase merchandise for $9,000 on credit terms 2/10, n/30, on May 8, 2001 before payment of the invoice, the company returned one-third of the goods for credit because they were damaged in shipment. Give the preferable entry for the return, assuming a periodic inventory system is used by the company.

(Essay)

4.7/5 (42)

Which of the following would cause an increase in the cost ratio as used in the retail inventory method?

(Multiple Choice)

4.8/5 (44)

On December 15, 2013, a corporation accepted delivery of goods for resale which it purchased on credit. As of December 31, the company had not recorded the transaction or included the merchandise in its inventory. The effect of this on the balance sheet for December 31, 2013 would be:

(Multiple Choice)

4.9/5 (33)

Work-in-Process inventories are not normally subject to lower of cost and net realizable value rules.

(True/False)

4.9/5 (44)

The average cost method of inventory valuation can be applied in exactly the same way by using either the periodic or perpetual inventory system.

(True/False)

4.9/5 (35)

When the retail inventory method is used, markdowns are commonly ignored in the computation of the cost to retail ratio because:

(Multiple Choice)

4.8/5 (35)

On December 31, 2013 Trade Cards Ltd. completed a physical inventory count that reflected an inventory valuation of $25,000. Theft is suspected; therefore, a reliable estimate of what the inventory should be is needed. Relevant data are: Sales revenue, $400,000; Average gross margin rate on sales for the past three years was 30 percent; Beginning inventory $20,000, and purchases, $290,000. The estimated amount of the theft loss is:

(Multiple Choice)

4.7/5 (43)

During a year, Small Wears Ltd. (whose usual gross margin rate on sales is 30 percent) recorded sales of $10,000 and goods available for sale of $12,000. The cost of its ending inventory can be reliably estimated at:

(Multiple Choice)

4.9/5 (34)

Lower-of-cost-or-market (LCM) is to be applied to the following situation: Cost, $10; Net realizable value, $8; Replacement cost, $7; Net realizable value less normal profit, $7.50. One unit in inventory should be valued at:

(Multiple Choice)

4.8/5 (42)

Ideally, the lower-of-cost and NRV technique should be applied an item-by-item basis or by category when this is not possible.

(True/False)

4.9/5 (38)

A company uses a perpetual inventory system, and follows GAAP in preparing its external financial statements. At the end of 2002, the balance in the inventory account was $66,000; $6,000 of those goods were purchased f.o.b. shipping point and did not arrive until 2013. Purchases in 2013 were $30,000. The perpetual inventory showed an ending inventory of $72,000 for 2013. A physical count of the goods on hand at the end of 2013 showed an inventory of $60,000. What should the company report on its 2013 income statement for cost of goods sold?

(Multiple Choice)

4.8/5 (41)

Which one of the following should be excluded from inventories?

(Multiple Choice)

4.9/5 (33)

A company has been using the retail inventory method, average basis, for inventory measurement. Starting in 2013, the company changed to the FIFO retail method.

At the end of 2013, the company prepared the following retail method, "pure" FIFO basis, computation which you are to complete: Cost Retail Inventory (base) at January 1, 2002 \ 4,840 \ 8,400 Purchases 25,803 41,600 Net additional mark-ups 700 Cost ratio \ 25,803 \ 42,300=.61 Total 30,643 50,700 Sales \ 40,400 Inventory at December 31, 2002 (FIFO) \ \

(Essay)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)