Exam 20: Additional Assurance Services: Other Information

Exam 1: The Role of the Public Accountant in the American Economy45 Questions

Exam 2: Professional Standards62 Questions

Exam 3: Professional Ethics62 Questions

Exam 4: Legal Liability of Cpas56 Questions

Exam 5: Audit Evidence and Documentation82 Questions

Exam 6: Planning the Audit; Linking Audit Procedures to Risk78 Questions

Exam 7: Internal Control92 Questions

Exam 8: Consideration of Internal Control in an Information Technology Environment63 Questions

Exam 9: Audit Sampling83 Questions

Exam 10: Cash and Financial Investments61 Questions

Exam 11: Accounts Receivable, Notes Receivable, and Revenue64 Questions

Exam 12: Inventories and Cost of Goods Sold59 Questions

Exam 13: Property, Plant, and Equipment: Depreciation and Depletion39 Questions

Exam 14: Accounts Payable and Other Liabilities50 Questions

Exam 15: Debt and Equity Capital40 Questions

Exam 16: Auditing Operations and Completing the Audit69 Questions

Exam 17: Auditors Report62 Questions

Exam 18: Integrated Audits of Public Companies43 Questions

Exam 19: Additional Assurance Services: Historical Financial Information60 Questions

Exam 20: Additional Assurance Services: Other Information51 Questions

Exam 21: Internal, Operational, and Compliance Auditing48 Questions

Select questions type

The type of service organization control (SOC) report that is for general use is:

Free

(Multiple Choice)

4.9/5  (38)

(38)

Correct Answer: Verified

Verified

C

Under the attestation standards, in which of the following circumstances is a review report least likely to be issued?

Free

(Multiple Choice)

4.7/5 (39)

Correct Answer:Verified

D

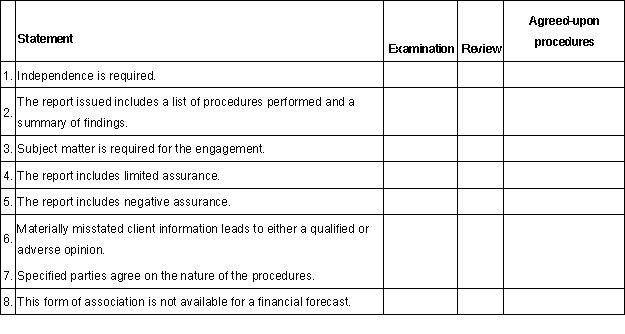

Following are a set of statements. For each statement indicate with an "X" whether it is correct with respect to an examination, a review, and/or an agreed-upon procedures engagement. Each statement may relate to none, one or more services.

Free

(Essay)

4.8/5 (31)

Correct Answer:Verified

When a financial forecast fails to disclose a significant assumption used to prepare that forecast, which of the following reports become appropriate? Qualified Adrerse A. Yes Yes B. Yes No C. No Yes D. No No

(Multiple Choice)

4.9/5 (29)

When a practitioner examines projected financial statements, the practitioner's report should include a separate paragraph that:

(Multiple Choice)

5.0/5 (43)

Which of the following engagements is most likely to consider security, availability, processing integrity, confidentiality, and privacy relating to a system?

(Multiple Choice)

4.8/5 (31)

Which of the following is a prospective financial statement for general use upon which a practitioner may appropriately report?

(Multiple Choice)

4.8/5 (44)

Which attest engagement aligns most directly with a financial statement audit in terms of assurance provided?

(Multiple Choice)

4.8/5 (34)

Which of the following is correct relating to an engagement to apply agreed-upon procedures to prospective financial statements?

(Multiple Choice)

4.8/5 (42)

Which of the following is least likely to be included in an agreed-upon procedures attestation engagement report?

(Multiple Choice)

5.0/5 (38)

An international information format designed specifically for business information is:

(Multiple Choice)

4.9/5 (38)

The AICPA has outlined auditor reports based on three services that may be provided on service organization controls (SOC). The type most directly related to SysTrust is:

(Multiple Choice)

4.8/5 (34)

Given one or more hypothetical assumptions, a responsible party may prepare an entity's expected financial position, results of operations, and changes in financial position. Such prospective financial statements are known as:

(Multiple Choice)

4.8/5 (43)

When an accountant compiles a financial forecast, the accountant's report should include a(n):

(Multiple Choice)

4.8/5 (37)

Which of the following is the least likely to be considered subject matter of an attestation engagement?

(Multiple Choice)

4.9/5 (40)

When a CPA is associated with a forecast, all of the following should be disclosed except the:

(Multiple Choice)

4.8/5 (44)

Which of the following is correct concerning a service auditor and a SysTrust report?

(Multiple Choice)

4.9/5 (33)

When reporting upon a review engagement on an entity's management discussion and analysis, the report is ordinarily:

(Multiple Choice)

4.8/5 (40)

The Warren Corporation wants to enhance the market value of its stock by including in its annual report a financial forecast for the next year. They also would like to have their auditors examine the forecast.

a. Define a financial forecast.

b. Is an examination of a financial forecast similar in scope to a review of financial statements? Explain.

(Essay)

4.9/5 (38)

The party responsible for assumptions identified in the preparation of prospective financial statements is usually:

(Multiple Choice)

4.8/5 (26)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)