Exam 3: Adjusting Accounts for Financial Statements

Exam 1: Introducing Financial Accounting270 Questions

Exam 2: Accounting System and Financial Statements236 Questions

Exam 3: Adjusting Accounts for Financial Statements271 Questions

Exam 4: Reporting and Analyzing Merchandising Operations263 Questions

Exam 5: Reporting and Analyzing Inventories218 Questions

Exam 6: Reporting and Analyzing Cash and Internal Controls215 Questions

Exam 7: Reporting and Analyzing Receivables207 Questions

Exam 8: Reporting and Analyzing Long-Term Assets255 Questions

Exam 9: Reporting and Analyzing Current Liabilities224 Questions

Exam 10: Reporting and Analyzing Long-Term Liabilities231 Questions

Exam 11: Reporting and Analyzing Equity248 Questions

Exam 12: Reporting and Analyzing Cash Flows226 Questions

Exam 13: Analyzing and Interpreting Financial Statements223 Questions

Exam 14: Applying Present and Future Values76 Questions

Exam 15: Investments and International Operations215 Questions

Exam 16: Reporting and Analyzing Partnerships168 Questions

Select questions type

Normally closing entries are first entered in the general journal and then posted to the work sheet.

(True/False)

5.0/5  (41)

(41)

On the work sheet, net income is entered in the Income Statement Credit column as well as the Balance Sheet Credit column.

(True/False)

4.9/5 (38)

If all columns of a completed work sheet balance, you can be sure that no errors were made in its preparation.

(True/False)

4.8/5 (28)

Financial statements can be prepared directly from the information in the adjusted trial balance.

(True/False)

4.9/5 (38)

The Retained Earnings account has a credit balance of $37,000 before closing entries are made. Total revenues for the period are $55,200, total expenses are $39,800, and dividends are $9,000. What is the correct closing entry for the expense accounts?

(Multiple Choice)

4.8/5 (37)

A company had revenues of $75,000 and expenses of $62,000 for the accounting period. The company paid $8,000 cash in dividends to the owner (sole shareholder). Which of the following entries could not be a closing entry?

(Multiple Choice)

4.8/5 (38)

Revenues, expenses, dividends, and Income Summary are called _________________ accounts because they are closed at the end of each accounting period.

(Short Answer)

4.8/5 (41)

The ___________________ account is a temporary account used only in the closing process.

(Short Answer)

4.7/5 (45)

Which of the following accounts showing a balance on the post-closing trial balance indicate an error?

(Multiple Choice)

4.8/5 (34)

An _______________________ is a listing of all of the accounts in the ledger with their account balances after adjustments are made.

(Short Answer)

4.7/5 (45)

On December 31, 2015 Carmack Company received a $215 utility bill for December that it will not pay until January 15. The adjusting entry needed on December 31 to accrue this expense is:

(Multiple Choice)

5.0/5 (45)

Cleaver Corporation has determined that the annual depreciation amount on its equipment is $7,100. The correct adjusting entry to record the depreciation for the period is:

(Multiple Choice)

4.9/5 (43)

Torsten had total assets of $149,501,000, net income of $6,242,000, and net sales of $209,203,000. Its profit margin was 2.98%.

Profit Margin = Net Income/Net Sales

Profit Margin = $6,242,000/$209,203,000 = 2.98%

(True/False)

4.8/5 (43)

Intangible assets are long-term resources that benefit business operations, usually lack physical form and have uncertain benefits.

(True/False)

4.9/5 (41)

Show the December 31 adjusting entry to record $750 of earned but unpaid salaries of employees at the end of the current accounting period.

(Essay)

4.9/5 (38)

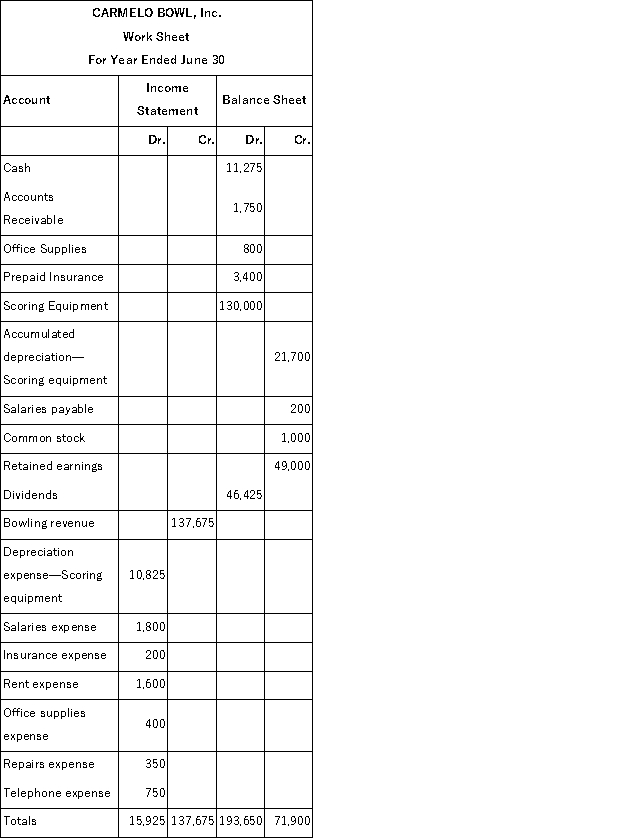

Use the following partial work sheet from Carmelo Bowl, Inc. to prepare its income statement, statement of retained earnings and a classified balance sheet (Assume the stockholders did not make any investments in the business this year.)

(Essay)

4.9/5 (44)

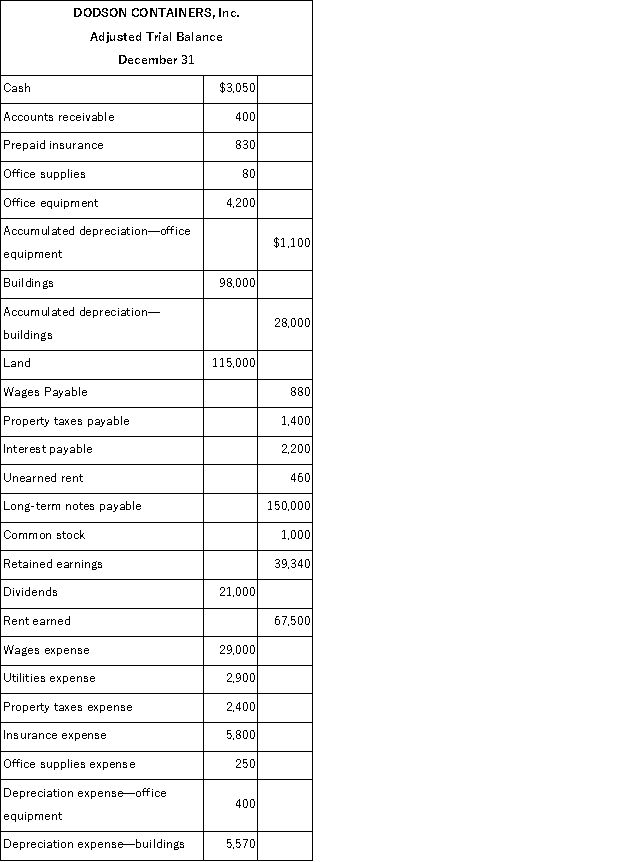

Using the information presented below, prepare an income statement from the adjusted trial balance of Dodson Containers Inc.

(Essay)

4.9/5 (33)

A company had $7,000,000 in net income for the year. Its net sales were $15,200,000 for the same period. Calculate its profit margin.

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)