Exam 20: Aggregate Demand and Aggregate Supply

Exam 1: Ten Principles of Economics438 Questions

Exam 2: Thinking Like an Economist620 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand700 Questions

Exam 5: Elasticity and Its Application598 Questions

Exam 6: Supply, Demand, and Government Policies648 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets547 Questions

Exam 8: Application: the Costs of Taxation514 Questions

Exam 9: Application: International Trade496 Questions

Exam 10: Measuring a Nations Income522 Questions

Exam 11: Measuring the Cost of Living545 Questions

Exam 12: Production and Growth507 Questions

Exam 13: Saving, Investment, and the Financial System567 Questions

Exam 14: The Basic Tools of Finance513 Questions

Exam 15: Unemployment699 Questions

Exam 16: The Monetary System517 Questions

Exam 17: Money Growth and Inflation487 Questions

Exam 18: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 19: A Macroeconomic Theory of the Open Economy484 Questions

Exam 20: Aggregate Demand and Aggregate Supply563 Questions

Exam 21: The Influence of Monetary and Fiscal Policy on Aggregate Demand511 Questions

Exam 22: The Short-Run Trade-Off Between Inflation and Unemployment516 Questions

Exam 23: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

Other things the same, if workers and firms expected inflation to be 2%, but it is only 1% then

(Multiple Choice)

4.8/5  (39)

(39)

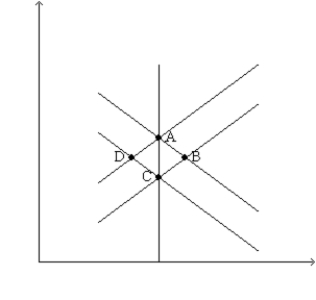

Figure 33-7.  -Refer to Financial Crisis. In the long run, if the Fed does not respond, the change in price expectations created by the crisis shifts

-Refer to Financial Crisis. In the long run, if the Fed does not respond, the change in price expectations created by the crisis shifts

(Multiple Choice)

4.9/5 (25)

The only way to rationalize an upward slope for the short-run aggregate-supply curve is to argue that wages are sticky in the short run.

(True/False)

4.8/5 (37)

Which of the following rises when the U.S. price level falls?

(Multiple Choice)

4.9/5 (30)

Suppose the economy is in long-run equilibrium. If there is a sharp increase in the minimum wage as well as an increase in taxes, then in the short run, real GDP will

(Multiple Choice)

4.8/5 (34)

John Maynard Keynes advocated policies that would increase aggregate demand as a way to decrease unemployment caused by recessions.

(True/False)

4.9/5 (29)

The equation: quantity of output supplied = natural rate of output + aactual price level - expected price level), where a is a positive number, represents

(Multiple Choice)

4.7/5 (37)

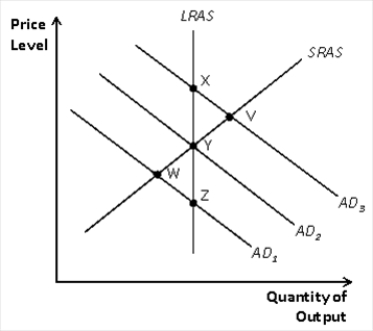

Figure 33-4  -Refer to Figure 33-4. If the economy is at A and there is a fall in aggregate demand, in the short run the economy

-Refer to Figure 33-4. If the economy is at A and there is a fall in aggregate demand, in the short run the economy

(Multiple Choice)

4.8/5 (31)

If the central bank increased the money supply in response to a decrease in short-run aggregate supply, unemployment would return towards its natural rate, but prices would rise even more.

(True/False)

4.9/5 (32)

Who is credited for the original development of the model of aggregate demand and aggregate supply?

(Essay)

4.7/5 (23)

Suppose the economy is in long-run equilibrium. In a short span of time, there is a sharp rise in the stock market, an increase in government purchases, an increase in the money supply and a decline in the value of the dollar. In the short run

(Multiple Choice)

4.8/5 (40)

According to the aggregate demand and aggregate supply model, in the long run a decrease in the money supply leads to

(Multiple Choice)

4.8/5 (35)

Other things the same, a decrease in the price level makes the dollars people hold worth

(Multiple Choice)

4.8/5 (38)

Which part of real GDP fluctuates most over the course of the business cycle?

(Multiple Choice)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)