Exam 8: A: Perfect Competition

Exam 1: The Art and Science of Economic Analysis147 Questions

Exam 1: Appendix: Understanding Graphs64 Questions

Exam 2: Economic Tools and Economics Systems195 Questions

Exam 3: Economic Decision Makers200 Questions

Exam 4: Demand, Supply, and Markets232 Questions

Exam 5: Elasticity of Demand and Supply238 Questions

Exam 6: Consumer Choice and Demand170 Questions

Exam 7: Production and Cost in the Firm209 Questions

Exam 8: A: Perfect Competition249 Questions

Exam 8: B: Perfect Competition22 Questions

Exam 9: A: Monopoly249 Questions

Exam 9: B: Monopoly13 Questions

Exam 10: Monopolistic Competition and Oligopoly226 Questions

Exam 11: Resource Markets216 Questions

Exam 12: Labor Markets and Labor Unions213 Questions

Exam 13: Capital, Interest, and Corporate Finance186 Questions

Exam 14: Transaction Costs, Imperfect Information, and Behavioral Economics186 Questions

Exam 15: Economic Regulation and Antitrust Policy182 Questions

Exam 16: Public Goods and Public Choice139 Questions

Exam 17: Externalities and the Environment194 Questions

Exam 18: Income Distribution and Poverty125 Questions

Exam 19: International Trade163 Questions

Exam 20: International Finance231 Questions

Exam 21: Economic Development110 Questions

Select questions type

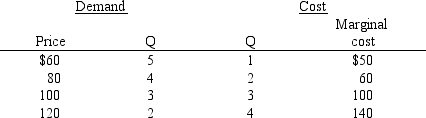

NARRBEGIN: Exhibit 8-1-1

Exhibit 8-1

-The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. Exhibit 8-1 shows cost data for one firm and demand data for one consumer. How many cords of firewood wil be bought and sold in equilibrium?

-The perfectly competitive firewood market is composed of 1,000 identical consumers and 1,000 identical firms. Exhibit 8-1 shows cost data for one firm and demand data for one consumer. How many cords of firewood wil be bought and sold in equilibrium?

Free

(Multiple Choice)

4.9/5  (39)

(39)

Correct Answer: Verified

Verified

C

If a firm is producing at an output where the total revenue curve crosses the total cost curve,

Free

(Multiple Choice)

4.8/5 (29)

Correct Answer:Verified

E

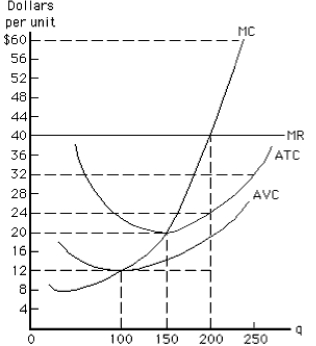

NARRBEGIN: Exhibit 8-10

Exhibit 8-10

-At the profit-maximizing output level, the firm represented in Exhibit 8-10 experiences

-At the profit-maximizing output level, the firm represented in Exhibit 8-10 experiences

(Multiple Choice)

4.7/5 (44)

Long-run equilibrium for a perfectly competitive firm occurs when

(Multiple Choice)

4.9/5 (35)

A Midwestern wheat farmer faces a horizontal demand curve because

(Multiple Choice)

4.8/5 (34)

Marginal revenue is the change in total revenue from selling one more unit of output.

(True/False)

4.9/5 (30)

After an increase in demand in a constant-cost industry, firms will find themselves with higher average cost curves.

(True/False)

4.8/5 (27)

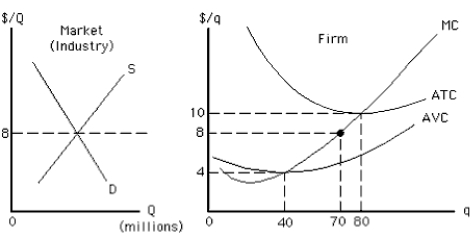

NARRBEGIN: Exhibit 8-7

Exhibit 8-7

-For the profit maximizing perfectly competitive firm represented in Exhibit 8-7, which of the following is true?

-For the profit maximizing perfectly competitive firm represented in Exhibit 8-7, which of the following is true?

(Multiple Choice)

4.9/5 (37)

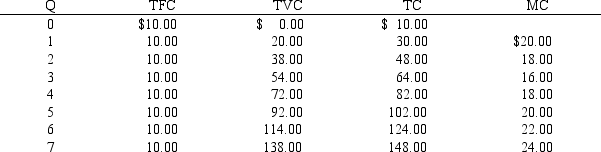

NARRBEGIN: Exhibit 8-5-1

Exhibit 8-5

-Consider Exhibit 8-5. If the market price is $15, the minimum loss this perfectly competitive firm can incur is

-Consider Exhibit 8-5. If the market price is $15, the minimum loss this perfectly competitive firm can incur is

(Multiple Choice)

4.8/5 (32)

NARRBEGIN: Exhibit 8-18-1

Exhibit 8-18

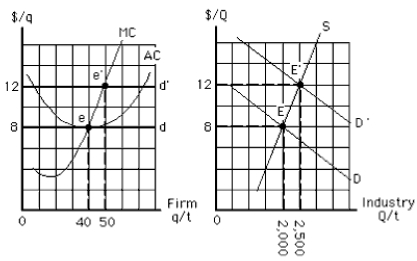

-Assuming all of the firms are identical, how many firms are in the industry before and after the demand shift depicted in Exhibit 8-18?

-Assuming all of the firms are identical, how many firms are in the industry before and after the demand shift depicted in Exhibit 8-18?

(Multiple Choice)

4.8/5 (41)

If price is less than its minimum average variable cost, a perfectly competitive firm that continues to produce in the short run

(Multiple Choice)

4.9/5 (39)

If a market is such that, at the market equilibrium quantity, the benefit of the last unit produced just equals its marginal cost

(Multiple Choice)

4.9/5 (35)

Marginal revenue is the change in total revenue from using one more unit of an input in the short run.

(True/False)

4.8/5 (40)

If a perfectly competitive firm charges the market price of $14 per unit,

(Multiple Choice)

4.8/5 (40)

Farmer Fanny sells her crops in a perfectly competitive market. If she produces 500 bushels for total revenue of $2,500 and if harvesting the 501st bushel would raise her total cost from $2,500 to $2,505, her

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)