Exam 5: Closing Entries and the Post-Closing Trial Balance Including Appendix

Exam 1: Asset, Liability, Owners Equity, Revenue, and Expense Accounts93 Questions

Exam 2: T Accounts, Debits and Credits, Trial Balance, and Financial Statements94 Questions

Exam 3: The General Journal and the General Ledger95 Questions

Exam 4: Adjusting Entries and the Work Sheet97 Questions

Exam 5: Closing Entries and the Post-Closing Trial Balance Including Appendix112 Questions

Exam 6: Bank Accounts and Cash Funds97 Questions

Exam 7: Employee Earnings and Deductions105 Questions

Exam 8: Employer Taxes, Payments, and Reports104 Questions

Exam 9: Sales and Purchases100 Questions

Exam 10: Cash Receipts and Cash Payments106 Questions

Exam 11: Work Sheet and Adjusting Entries101 Questions

Exam 12: Financial Statements, Closing Entries, and Reversing Entries104 Questions

Select questions type

The fourth step in the closing process is to close the _____________ account(s) into the ___________ account(s).

(Multiple Choice)

4.9/5  (38)

(38)

Which of the following accounts would not be involved in closing entries?

(Multiple Choice)

4.9/5 (37)

Match the terms that follow with the correct definitions.

-An accounting system in which transactions are recorded by hand.

-An accounting system in which transactions are recorded by hand.

(Short Answer)

4.8/5 (39)

The _______________ requires that revenue is recorded when it is received in cash and expenses are recorded when they are paid in cash.

(Multiple Choice)

4.9/5 (31)

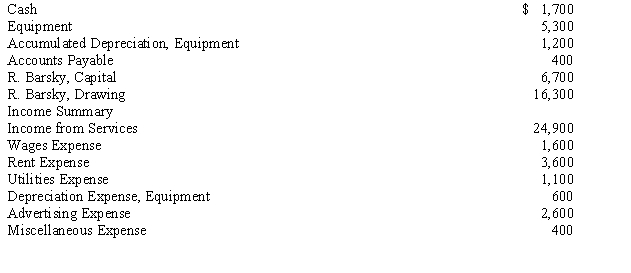

On December 31, the ledger accounts of Barsky Repair have the following balances after all adjusting entries have been posted.

Instructions:

Journalize the four closing entries in the proper order.

Instructions:

Journalize the four closing entries in the proper order.

(Essay)

4.9/5 (29)

Which of the following can be prepared by taking the account balances from the general ledger after closing?

(Multiple Choice)

4.9/5 (45)

Entries required to clear or zero the balances of temporary accounts at the end of the year are called ____________ entries.

(Multiple Choice)

4.7/5 (36)

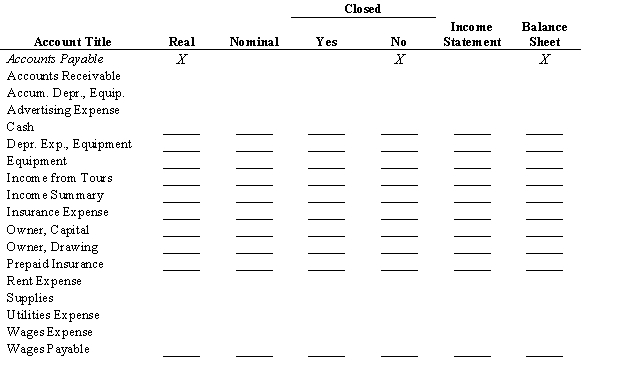

Classify the following accounts as real (permanent) or nominal (temporary), and indicate with an X whether the account is closed. Also, indicate the financial statement in which each account will appear. The Accounts Payable account is given as an example.

(Essay)

4.8/5 (37)

Yellow Co. makes a sale to a customer in January but does not receive payment until March. Yellow Co. records the sale in January. Which method of accounting is Yellow Co. using?

(Multiple Choice)

4.9/5 (27)

A post-closing trial balance will include only permanent accounts.

(True/False)

4.8/5 (29)

Match the terms that follow with the correct definitions.

-The debit to Income Summary represents the total

-The debit to Income Summary represents the total

(Short Answer)

4.9/5 (42)

The fourth step in the closing procedure is to close the Income Summary account into the Capital account.

(True/False)

5.0/5 (36)

Which of the following accounts should be closed to Income Summary at the end of the fiscal year?

(Multiple Choice)

4.8/5 (36)

The most efficient sources for closing entry information are the

(Multiple Choice)

4.9/5 (41)

Financial statements prepared during the fiscal year for periods of less than twelve months are called interim statements.

(True/False)

4.8/5 (34)

Which of the following account(s) would remain open after closing entries?

(Multiple Choice)

4.8/5 (32)

Match the terms that follow with the correct definitions.

-A feature of QuickBooks that handles transactions related to specific areas, such as customers, vendors, employees, banking, and reports.

(Short Answer)

4.7/5 (30)

Match the terms that follow with the correct definitions.

-Account that is used to assist in closing temporary-equity accounts

(Short Answer)

4.8/5 (46)

The debit to Income Summary in the second closing entry represents the total expenses.

(True/False)

4.7/5 (42)

Entries required to clear or zero the balances of the temporary accounts at the end of the year are called adjusting entries.

(True/False)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)