Deck 14: Perfect Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

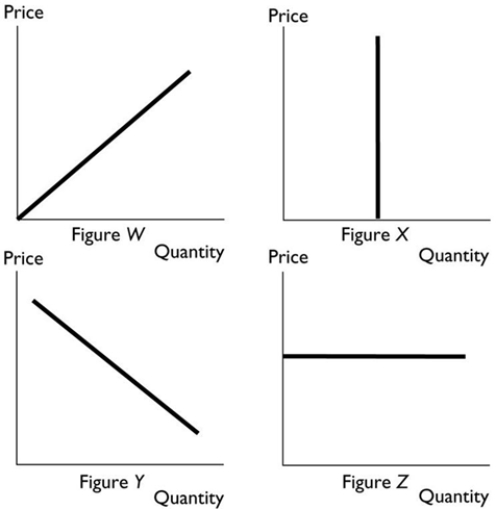

In the above, a marginal revenue curve for a perfectly competitive firm is shown in Figure

A) W.

B) X.

C) Y.

D) Z.

E) X and Figure Z.

Question

Question

Question

Question

Question

Question

Question

Question

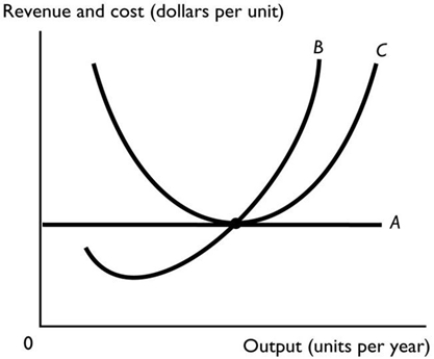

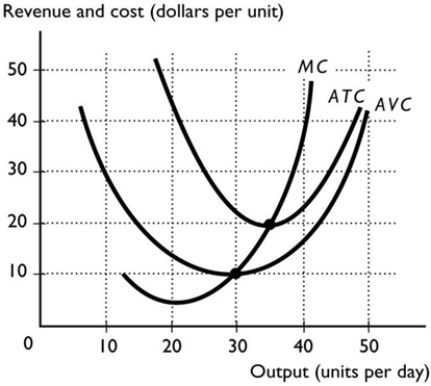

The above figure illustrates a perfectly competitive firm. Curve C represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) market demand curve.

E) AFC curve.

Question

Question

Question

A perfectly competitive firm will continue to operate in the short run when the market price is below its average total cost if the

A) price is at least equal to the minimum average variable cost.

B) total fixed costs are less than total revenue.

C) marginal revenue is greater than marginal cost.

D) marginal cost is minimised.

E) price is also less than the minimum average variable cost.

Question

Question

A perfectly competitive firm will shut down when the price is just below the minimum point on the

A) average fixed cost curve.

B) average total cost curve.

C) marginal revenue curve.

D) average variable cost curve.

E) marginal cost curve.

Question

Question

The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of potatoes. When Omar maximises his profit, Omar's profit equals

A) $16.

B) $11.

C) $80.

D) $30.

E) $105.

Question

The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of potatoes. When Omar produces 2 tonnes of potatoes, his total profit equals

A) $20.

B) -$8.

C) $28.

D) $0.

E) $48.

Question

Question

Question

Question

Question

The above figure illustrates a perfectly competitive firm. Curve B represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

Question

Question

Question

The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of potatoes. Omar's total profit is maximised when he produces ________ tonnes of potatoes.

A) 7

B) 6

C) 8

D) 3

E) 5

Question

The above figure illustrates a perfectly competitive firm. Curve A represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

Question

Question

Question

The above figure shows a perfectly competitive firm. If the market price is more than $20 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Question

Question

The above figure shows a perfectly competitive firm. If the market price is $15 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Question

Question

Question

Question

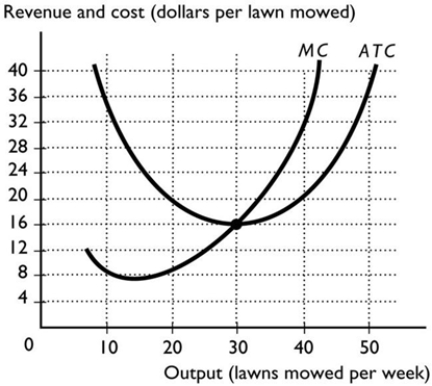

Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. If Bill's average total cost curve is ATC, his total economic ________ equals ________.

A) profit; $1,280 per week

B) loss; $800 per week

C) loss; $1,280 per week

D) profit; $480 per week

E) profit; $32 per week

Question

Question

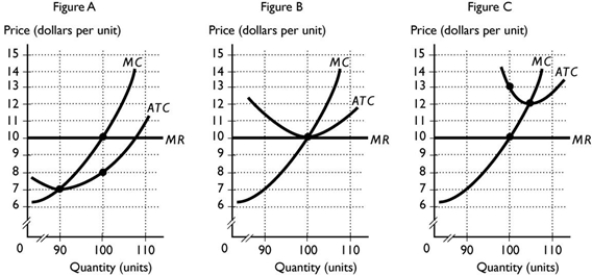

Use the figure above to answer this question. Consider a perfectly competitive firm in a short-run equilibrium. Figure ________ shows a firm in bad times because the firm makes a(n) ________.

A) A; economic loss of $4 so it must close

B) C; normal profit and can stay open in the long run

C) B; economic loss of $3 per unit

D) B; economic profit because the price exceeds average variable cost

E) A; economic loss of $4 per unit if the firm decides to operate

Question

Question

The above figure shows a perfectly competitive firm. If the market price is $20 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Question

Question

Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. Bill's average total cost curve is ATC, so his TOTAL cost of production equals

A) more than $1,800 per week.

B) more than $1,400 per week and less than $1,800 per week.

C) $0 because Bill shuts down.

D) more than $1,200 and less than $1,400 per week.

E) more than $0 and less than $1,200 per week.

Question

The above figure shows a perfectly competitive firm. If the market price is $5 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Question

Question

Use the figure above to answer this question. Consider a perfectly competitive market experiencing good times. Figure ________ shows a firm maximising profit in the short run because it produces ________ units and makes an economic profit of ________.

A) A; 100; $2 per unit

B) C; 100; $3 per unit

C) B; 100; $0 per unit

D) A; 90; $3 per unit

E) C; 110; $2 per unit

Question

Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. At this price, how many lawns will Bill mow per week?

A) Zero

B) 40

C) 50

D) More than 10 and less than 30

E) 30

Question

Question

Use the figure above to answer this question. Consider a perfectly competitive firm in a short-run equilibrium. Figure ________ shows a firm in bad times because the firm produces ________ units and makes a(n) ________.

A) A; 100; economic loss

B) B; 90; economic profit

C) C; 100; economic loss

D) A; 110; economic loss

E) C; 100; normal profit

Question

Use the figure above to answer this question. Figure ________ shows a short-run equilibrium in good times because the firm makes a(n) ________.

A) C; normal profit

B) A; normal profit

C) B; normal profit

D) B; economic loss

E) A; economic profit

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/105

Play

Full screen (f)

Deck 14: Perfect Competition

1

A perfectly competitive firm can

A) sell additional output only by lowering its price.

B) set a higher price for customers who are willing to pay more.

C) sell all of its output at the prevailing market price.

D) raise its price in order to increase its total revenue.

E) usually not sell all the output it produces, but it still 'overproduces' because there are some periods when it can sell the extra output at very profitable prices.

A) sell additional output only by lowering its price.

B) set a higher price for customers who are willing to pay more.

C) sell all of its output at the prevailing market price.

D) raise its price in order to increase its total revenue.

E) usually not sell all the output it produces, but it still 'overproduces' because there are some periods when it can sell the extra output at very profitable prices.

sell all of its output at the prevailing market price.

2

A market is classified as monopolistically competitive when

A) a small number of firms compete.

B) many firms produce a slightly differentiated product.

C) there is one firm that sells a good or service with no close substitutes.

D) many firms produce the same product.

E) there is a barrier that blocks entry by other firms.

A) a small number of firms compete.

B) many firms produce a slightly differentiated product.

C) there is one firm that sells a good or service with no close substitutes.

D) many firms produce the same product.

E) there is a barrier that blocks entry by other firms.

many firms produce a slightly differentiated product.

3

Suppose Pat's Paints is a perfectly competitive firm. If Pat's Paints' marginal revenue equals $5 per can, and Pat decides to sell 100 cans of paint, Pat's total revenue equals

A) $20.

B) $500.

C) $100.

D) $5.

E) Information on the price paint is needed.

A) $20.

B) $500.

C) $100.

D) $5.

E) Information on the price paint is needed.

$500.

4

In which market structure do firms exist in very large numbers, each firm produces an identical product, and there is freedom of entry and exit?

A) Only monopolistic competition

B) Monopoly

C) Oligopoly

D) Only perfect competition

E) Both perfect competition and monopolistic competition

A) Only monopolistic competition

B) Monopoly

C) Oligopoly

D) Only perfect competition

E) Both perfect competition and monopolistic competition

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

5

Perfect competition is characterised by all of the following EXCEPT

A) buyers and sellers are well informed about prices.

B) no restrictions on entry into or exit from the industry.

C) firms produce an identical product.

D) considerable advertising by individual firms.

E) a large number of buyers and sellers.

A) buyers and sellers are well informed about prices.

B) no restrictions on entry into or exit from the industry.

C) firms produce an identical product.

D) considerable advertising by individual firms.

E) a large number of buyers and sellers.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

6

One requirement for an industry to be perfectly competitive is that in the industry there

A) is a barrier to entry that makes the entry of new firms difficult.

B) is one firm that sells a product with no close substitutes.

C) are a few firms who control the market.

D) are many firms selling different products.

E) are many firms for whom the efficient scale of production is small.

A) is a barrier to entry that makes the entry of new firms difficult.

B) is one firm that sells a product with no close substitutes.

C) are a few firms who control the market.

D) are many firms selling different products.

E) are many firms for whom the efficient scale of production is small.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

7

In a perfectly competitive market, the type of decision a firm has to make is different in the short run than in the long run. Which of the following is an example of a perfectly competitive firm's short-run decision?

A) Whether or not to enter or exit an industry.

B) What price to charge buyers for the product.

C) Whether or not to change its plant size.

D) How much to spend on advertising and sales promotion.

E) The profit-maximising level of output.

A) Whether or not to enter or exit an industry.

B) What price to charge buyers for the product.

C) Whether or not to change its plant size.

D) How much to spend on advertising and sales promotion.

E) The profit-maximising level of output.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

8

What is the difference between perfect competition and monopolistic competition?

A) Perfect competition has barriers to entry while monopolistic competition does not.

B) In monopolistic competition firms produce identical goods, while in perfect competition firms produce slightly different goods.

C) In perfect competition firms produce identical goods, while in monopolistic competition firms produce slightly different goods.

D) Perfect competition has a large number of small firms while monopolistic competition does not.

E) Perfect competition has minor barriers to entry, while monopolistic competition has major barriers.

A) Perfect competition has barriers to entry while monopolistic competition does not.

B) In monopolistic competition firms produce identical goods, while in perfect competition firms produce slightly different goods.

C) In perfect competition firms produce identical goods, while in monopolistic competition firms produce slightly different goods.

D) Perfect competition has a large number of small firms while monopolistic competition does not.

E) Perfect competition has minor barriers to entry, while monopolistic competition has major barriers.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

9

A firm in perfect competition is a price taker because

A) there are no good substitutes for its good.

B) its demand curve is vertical at the profit-maximising quantity.

C) many other firms produce identical products.

D) its demand curves are downward sloping.

E) it is very large.

A) there are no good substitutes for its good.

B) its demand curve is vertical at the profit-maximising quantity.

C) many other firms produce identical products.

D) its demand curves are downward sloping.

E) it is very large.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

10

We know that a perfectly competitive firm is a price taker because

A) MC and ATC are equal at the profit-maximising amount of output.

B) its MC curve slopes upward.

C) its demand curve is horizontal.

D) its ATC curve is U-shaped.

E) it has no supply curve.

A) MC and ATC are equal at the profit-maximising amount of output.

B) its MC curve slopes upward.

C) its demand curve is horizontal.

D) its ATC curve is U-shaped.

E) it has no supply curve.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

11

The firm's over-riding objective is to

A) avoid an economic loss.

B) maximise normal profit.

C) maximise total revenue.

D) earn a normal profit.

E) maximise economic profit.

A) avoid an economic loss.

B) maximise normal profit.

C) maximise total revenue.

D) earn a normal profit.

E) maximise economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

12

One requirement for an industry to be perfectly competitive is that

A) many firms sell slightly different products.

B) there are many firms selling different products.

C) there are multiple restrictions on entry into or exit from the market.

D) there are no restrictions on entry into or exit from the market.

E) sellers and buyers have imperfect information about prices.

A) many firms sell slightly different products.

B) there are many firms selling different products.

C) there are multiple restrictions on entry into or exit from the market.

D) there are no restrictions on entry into or exit from the market.

E) sellers and buyers have imperfect information about prices.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

13

Each firm in a perfectly competitive industry

A) produces a good that is slightly different from that of the other firms.

B) has an important influence on the market price of the good or service being produced.

C) attains economies of scale so that its efficient size is large compared to the market as a whole.

D) produces a good that is identical to that of the other firms.

E) has control over at least one unique resource to separate itself from its competitors.

A) produces a good that is slightly different from that of the other firms.

B) has an important influence on the market price of the good or service being produced.

C) attains economies of scale so that its efficient size is large compared to the market as a whole.

D) produces a good that is identical to that of the other firms.

E) has control over at least one unique resource to separate itself from its competitors.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

14

In which market structure does one firm sell a good or service with no close substitutes and there is a barrier blocking the entry of new firms?

A) Only oligopoly

B) Only monopoly

C) Perfect competition

D) Monopolistic competition

E) Either monopoly or oligopoly

A) Only oligopoly

B) Only monopoly

C) Perfect competition

D) Monopolistic competition

E) Either monopoly or oligopoly

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

15

A market is classified as an oligopoly when

A) many firms produce a slightly differentiated product.

B) only one firm sells a product with no close substitutes.

C) a few firms compete.

D) many firms produce the same product.

E) no matter how many firms are in the market, a barrier blocks entry by other new firms.

A) many firms produce a slightly differentiated product.

B) only one firm sells a product with no close substitutes.

C) a few firms compete.

D) many firms produce the same product.

E) no matter how many firms are in the market, a barrier blocks entry by other new firms.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following market types has the fewest number of firms?

A) Monopoly

B) Perfect competition

C) Monopolistic competition

D) Perfect competition and monopolistic competition

E) Oligopoly

A) Monopoly

B) Perfect competition

C) Monopolistic competition

D) Perfect competition and monopolistic competition

E) Oligopoly

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

17

For a perfectly competitive firm, the price of its good is equal to the firm's marginal revenue because

A) there are only a small number of firms in the market.

B) individual perfectly competitive firms cannot influence the market price by changing their output.

C) the firm's total revenue cannot be changed by anything the firms do.

D) information about price changes is hard to come by for small sellers.

E) price and marginal revenue are the same economic concepts.

A) there are only a small number of firms in the market.

B) individual perfectly competitive firms cannot influence the market price by changing their output.

C) the firm's total revenue cannot be changed by anything the firms do.

D) information about price changes is hard to come by for small sellers.

E) price and marginal revenue are the same economic concepts.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

18

In which market structure are there a small number of firms competing?

A) Only monopoly

B) Only oligopoly

C) Monopolistic competition

D) Perfect competition

E) Either monopoly or oligopoly

A) Only monopoly

B) Only oligopoly

C) Monopolistic competition

D) Perfect competition

E) Either monopoly or oligopoly

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is the best example of a perfectly competitive market?

A) Athletic shoes

B) Soft drinks

C) Diamonds

D) Farming

E) Electricity distribution

A) Athletic shoes

B) Soft drinks

C) Diamonds

D) Farming

E) Electricity distribution

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

20

The characteristics that describe a perfectly competitive industry include

A) many firms selling an identical product.

B) a few firms selling to many buyers.

C) many firms selling a slightly differentiated product.

D) one firm selling to many buyers.

E) None of the above answers is correct.

A) many firms selling an identical product.

B) a few firms selling to many buyers.

C) many firms selling a slightly differentiated product.

D) one firm selling to many buyers.

E) None of the above answers is correct.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

21

Cynthia is a Victorian wheat farmer. The demand for her wheat is

A) unit elastic.

B) perfectly inelastic.

C) perfectly elastic.

D) elastic but not perfectly elastic.

E) inelastic but not perfectly inelastic.

A) unit elastic.

B) perfectly inelastic.

C) perfectly elastic.

D) elastic but not perfectly elastic.

E) inelastic but not perfectly inelastic.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

22

If a perfectly competitive firm raised the price of its product,

A) its total revenue would rise but its total cost would rise by more.

B) its profits would increase.

C) the quantity of output it sells decreases to zero.

D) the firm will be forced to advertise more.

E) rival firms will follow suit and raise their prices also.

A) its total revenue would rise but its total cost would rise by more.

B) its profits would increase.

C) the quantity of output it sells decreases to zero.

D) the firm will be forced to advertise more.

E) rival firms will follow suit and raise their prices also.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

23

For a perfectly competitive firm, profit is maximised at the output level where i. total revenue exceeds total cost by the largest amount.

Ii) marginal revenue equals marginal cost.

Iii) price equals marginal cost.

A) i only

B) i, ii and iii

C) ii and iii

D) i and ii

E) ii only

Ii) marginal revenue equals marginal cost.

Iii) price equals marginal cost.

A) i only

B) i, ii and iii

C) ii and iii

D) i and ii

E) ii only

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

24

Elsie is a perfectly competitive dairy farmer. The market price of milk was $2.40 per litre but just fell to $2.20 a litre. Elsie

A) will have to charge some customers $2.40 a litre to stay in business.

B) will be able to charge her initial customers $2.40 a litre.

C) can sell as much milk as she wants at $2.20 a litre.

D) can sell more at the lower price because the quantity demanded is higher at lower prices.

E) will produce the same amount of milk at both prices.

A) will have to charge some customers $2.40 a litre to stay in business.

B) will be able to charge her initial customers $2.40 a litre.

C) can sell as much milk as she wants at $2.20 a litre.

D) can sell more at the lower price because the quantity demanded is higher at lower prices.

E) will produce the same amount of milk at both prices.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

25

How does the demand for any one seller's product in perfect competition compare to the market demand for that product?

A) The demand for any one seller's product is perfectly elastic while the market demand curve is downward sloping.

B) The demand for any one seller is proportionally smaller but otherwise identical to the market demand.

C) The demand for any one seller's product is not perfectly elastic, while the market demand is perfectly elastic.

D) They are identical.

E) There is no demand for any one seller's competitively sold product.

A) The demand for any one seller's product is perfectly elastic while the market demand curve is downward sloping.

B) The demand for any one seller is proportionally smaller but otherwise identical to the market demand.

C) The demand for any one seller's product is not perfectly elastic, while the market demand is perfectly elastic.

D) They are identical.

E) There is no demand for any one seller's competitively sold product.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

26

In a perfectly competitive market, the market price is $23. At the current level of output, a firm has a marginal cost of $28. What should the firm do?

A) Produce less output to make more profit.

B) Raise the price of its product.

C) Nothing, it is currently maximising profit.

D) Shut down.

E) Produce a larger output to make more profit.

A) Produce less output to make more profit.

B) Raise the price of its product.

C) Nothing, it is currently maximising profit.

D) Shut down.

E) Produce a larger output to make more profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

27

As a perfectly competitive firm produces more and more of a good, its economic profit

A) first increases, then decreases.

B) does not change.

C) constantly increases.

D) first decreases, then increases.

E) constantly decreases.

A) first increases, then decreases.

B) does not change.

C) constantly increases.

D) first decreases, then increases.

E) constantly decreases.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

28

Mark owns a cattle station near Darwin. Mark is currently producing beef at an output level where marginal revenue exceeds marginal cost. In order to maximise his profit, Mark should

A) decrease his output.

B) shut down his cattle station.

C) increase his output.

D) not change his output.

E) probably change his output, but more information is needed to determine if he should increase, decrease or not change it.

A) decrease his output.

B) shut down his cattle station.

C) increase his output.

D) not change his output.

E) probably change his output, but more information is needed to determine if he should increase, decrease or not change it.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

29

In perfect competition, marginal revenue

A) is zero.

B) increases as more is sold.

C) is equal to the market price.

D) is always greater than marginal cost.

E) decreases as more is sold.

A) is zero.

B) increases as more is sold.

C) is equal to the market price.

D) is always greater than marginal cost.

E) decreases as more is sold.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

30

Jennifer's Bakery Shop produces baked goods in a perfectly competitive market. If Jennifer decides to produce her 100th batch of cookies, the marginal cost is $120. She can sell this batch of cookies at a market price of $110. To maximise her profit, Jennifer should

A) shut down.

B) charge $120 for this batch.

C) not produce this additional batch.

D) produce this batch of cookies because its MR exceeds its MC.

E) produce this batch of cookies because it will help lower her average fixed cost.

A) shut down.

B) charge $120 for this batch.

C) not produce this additional batch.

D) produce this batch of cookies because its MR exceeds its MC.

E) produce this batch of cookies because it will help lower her average fixed cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

31

If the market price of a product is $14 and all sellers are price takers, then which of the following is correct?

A) Each seller's total revenue line is graphed as an upward-sloping straight line.

B) Each seller's total revenue is graphed as an upside-down U-shaped curve.

C) Each seller can earn more total revenue by raising the price he or she charges to above $14.

D) The demand curve for each seller's product is a downward-sloping straight line.

E) The demand curve for each seller's product is a downward sloping but not necessarily straight line.

A) Each seller's total revenue line is graphed as an upward-sloping straight line.

B) Each seller's total revenue is graphed as an upside-down U-shaped curve.

C) Each seller can earn more total revenue by raising the price he or she charges to above $14.

D) The demand curve for each seller's product is a downward-sloping straight line.

E) The demand curve for each seller's product is a downward sloping but not necessarily straight line.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

32

Suppose that a perfectly competitive firm's marginal revenue equals $12 when it sells 10 units of output. If the marginal cost of producing the 10th unit is $14, to maximise its profit the firm should

A) increase the price it charges for its product.

B) shut down.

C) increase its production.

D) decrease its production.

E) do nothing because it is already maximising its profit.

A) increase the price it charges for its product.

B) shut down.

C) increase its production.

D) decrease its production.

E) do nothing because it is already maximising its profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

33

In the above, a marginal revenue curve for a perfectly competitive firm is shown in Figure

A) W.

B) X.

C) Y.

D) Z.

E) X and Figure Z.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

34

A firm maximises its profit by producing the amount of output such that

A) marginal revenue equals marginal cost.

B) marginal cost is minimised.

C) marginal revenue is maximised.

D) marginal revenue exceeds marginal cost by some amount.

E) marginal revenue exceeds marginal cost by the maximum amount possible.

A) marginal revenue equals marginal cost.

B) marginal cost is minimised.

C) marginal revenue is maximised.

D) marginal revenue exceeds marginal cost by some amount.

E) marginal revenue exceeds marginal cost by the maximum amount possible.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

35

A perfectly competitive firm is earning an economic profit when total fixed costs increase. Assuming the firm does not shut down, in the short run the firm will

A) continue producing the same quantity as before and continue making the same economic profit as before.

B) produce less output to decrease total costs.

C) charge a higher price.

D) produce more output so the extra revenue will cover the increased costs.

E) continue producing the same quantity as before but will make less economic profit.

A) continue producing the same quantity as before and continue making the same economic profit as before.

B) produce less output to decrease total costs.

C) charge a higher price.

D) produce more output so the extra revenue will cover the increased costs.

E) continue producing the same quantity as before but will make less economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

36

A firm's marginal revenue is

A) the change in total revenue minus the change in total cost.

B) the change in total revenue that results from a one-unit increase in the quantity sold.

C) the change in total revenue that results from an increase in the demand for the good or service.

D) total revenue minus total cost.

E) less than the market price for a perfectly competitive firm.

A) the change in total revenue minus the change in total cost.

B) the change in total revenue that results from a one-unit increase in the quantity sold.

C) the change in total revenue that results from an increase in the demand for the good or service.

D) total revenue minus total cost.

E) less than the market price for a perfectly competitive firm.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

37

Jerry's Jellybean Factory produces 2,000 kilograms of jellybeans per month and sells them in a perfectly competitive market. The marginal cost is $3 per kilogram, the average variable cost is $2 per kilogram, and the beans sell for $4 per kilogram. Jerry

A) could increase his profit by producing fewer beans.

B) is maximising profit.

C) could increase his profit by producing more beans.

D) is incurring an economic loss and should shut down.

E) could increase his profit by raising the price of his beans.

A) could increase his profit by producing fewer beans.

B) is maximising profit.

C) could increase his profit by producing more beans.

D) is incurring an economic loss and should shut down.

E) could increase his profit by raising the price of his beans.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

38

If a firm in a perfectly competitive market faces an equilibrium price of $5, its marginal revenue

A) will be less than $5.

B) may be either greater or less than $5.

C) will be any amount but $5.

D) will also be $5.

E) will be greater than $5.

A) will be less than $5.

B) may be either greater or less than $5.

C) will be any amount but $5.

D) will also be $5.

E) will be greater than $5.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

39

For a perfectly competitive firm, profit maximisation occurs when output is such that

A) average total cost (ATC) is minimised.

B) total revenue (TR) equals total cost (TC).

C) total cost (TC) is minimised.

D) marginal revenue (MR) = marginal cost (MC).

E) total revenue (TR) is maximised.

A) average total cost (ATC) is minimised.

B) total revenue (TR) equals total cost (TC).

C) total cost (TC) is minimised.

D) marginal revenue (MR) = marginal cost (MC).

E) total revenue (TR) is maximised.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

40

In a perfectly competitive industry, when a firm is producing so that its total revenue equals its total cost, the firm is

A) making zero economic profit.

B) making an economic profit.

C) definitely not maximising its profit.

D) incurring an economic loss.

E) None of the above answers is correct because the relationship between total revenue and total cost has nothing to do with the firm's profit or loss.

A) making zero economic profit.

B) making an economic profit.

C) definitely not maximising its profit.

D) incurring an economic loss.

E) None of the above answers is correct because the relationship between total revenue and total cost has nothing to do with the firm's profit or loss.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

41

The above figure illustrates a perfectly competitive firm. Curve C represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) market demand curve.

E) AFC curve.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

42

Suppose a perfectly competitive firm's minimum average variable cost is $3 when it produces 50. If the price is $2 and the firm's marginal cost is $2, the firm should

A) continue to produce 50.

B) continue to produce, but produce less than 50.

C) shut down.

D) continue to produce, but produce more than 50.

E) continue to operate, but to determine the amount of production requires more information than is given.

A) continue to produce 50.

B) continue to produce, but produce less than 50.

C) shut down.

D) continue to produce, but produce more than 50.

E) continue to operate, but to determine the amount of production requires more information than is given.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following will increase a perfectly competitive seller's short-run supply and shift the firm's short-run supply curve rightward?

A) A decrease in average fixed costs.

B) An increase in the market price.

C) A decrease in marginal cost.

D) Both answers A and B are correct.

E) Both answers A and C are correct.

A) A decrease in average fixed costs.

B) An increase in the market price.

C) A decrease in marginal cost.

D) Both answers A and B are correct.

E) Both answers A and C are correct.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

44

A perfectly competitive firm will continue to operate in the short run when the market price is below its average total cost if the

A) price is at least equal to the minimum average variable cost.

B) total fixed costs are less than total revenue.

C) marginal revenue is greater than marginal cost.

D) marginal cost is minimised.

E) price is also less than the minimum average variable cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following is true if a firm shuts down? i. The price is less than minimum average variable cost.

Ii) The firm is able to avoid an economic loss.

Iii) The firm incurs a loss equal to its total variable cost.

A) i only

B) i and ii

C) iii only

D) ii only

E) i and iii

Ii) The firm is able to avoid an economic loss.

Iii) The firm incurs a loss equal to its total variable cost.

A) i only

B) i and ii

C) iii only

D) ii only

E) i and iii

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

46

A perfectly competitive firm will shut down when the price is just below the minimum point on the

A) average fixed cost curve.

B) average total cost curve.

C) marginal revenue curve.

D) average variable cost curve.

E) marginal cost curve.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

47

If a perfectly competitive firm finds that the price exceeds its ATC, then the firm

A) will raise its price to increase its economic profit.

B) will lower its price to increase its economic profit.

C) is incurring an economic loss.

D) is making zero economic profit.

E) is making an economic profit.

A) will raise its price to increase its economic profit.

B) will lower its price to increase its economic profit.

C) is incurring an economic loss.

D) is making zero economic profit.

E) is making an economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

48

The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of potatoes. When Omar maximises his profit, Omar's profit equals

A) $16.

B) $11.

C) $80.

D) $30.

E) $105.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

49

The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of potatoes. When Omar produces 2 tonnes of potatoes, his total profit equals

A) $20.

B) -$8.

C) $28.

D) $0.

E) $48.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

50

A perfectly competitive firm's short-run supply curve is

A) its marginal cost curve below the marginal revenue curve.

B) its marginal revenue curve below the ATC curve.

C) horizontal at the market price.

D) its total cost curve above the AVC.

E) its marginal cost curve above the AVC curve.

A) its marginal cost curve below the marginal revenue curve.

B) its marginal revenue curve below the ATC curve.

C) horizontal at the market price.

D) its total cost curve above the AVC.

E) its marginal cost curve above the AVC curve.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

51

The largest loss a profit-maximising perfectly competitive firm can incur in the short run equals its

A) total variable cost.

B) average total cost multiplied by the number of units produced.

C) total fixed cost.

D) marginal cost multiplied by the number of units produced.

E) average variable cost multiplied by output.

A) total variable cost.

B) average total cost multiplied by the number of units produced.

C) total fixed cost.

D) marginal cost multiplied by the number of units produced.

E) average variable cost multiplied by output.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

52

In the short run, a perfectly competitive firm

A) can possibly make an economic profit or possibly incur an economic loss.

B) can make only zero economic profit.

C) produces the level of output that sets the average total cost equal to the market price.

D) can change only its fixed inputs.

E) can vary all its inputs.

A) can possibly make an economic profit or possibly incur an economic loss.

B) can make only zero economic profit.

C) produces the level of output that sets the average total cost equal to the market price.

D) can change only its fixed inputs.

E) can vary all its inputs.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

53

For a perfectly competitive wheat grower in New South Wales, the marginal revenue curve is

A) downward sloping.

B) U-shaped.

C) vertical at the profit-maximising quantity of production.

D) the same as its demand curve.

E) upward sloping.

A) downward sloping.

B) U-shaped.

C) vertical at the profit-maximising quantity of production.

D) the same as its demand curve.

E) upward sloping.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

54

The above figure illustrates a perfectly competitive firm. Curve B represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

55

The market supply in the short run for the perfectly competitive industry is

A) divided up according to each firm's selling price.

B) the sum of the supply schedules of all firms.

C) set at the maximum price a buyer will pay for one unit.

D) equal to the average of each firm's supply schedule.

E) the same as each producer's supply.

A) divided up according to each firm's selling price.

B) the sum of the supply schedules of all firms.

C) set at the maximum price a buyer will pay for one unit.

D) equal to the average of each firm's supply schedule.

E) the same as each producer's supply.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

56

If the market price is lower than a perfectly competitive firm's average total cost, the firm will

A) shut down if the price exceeds the average fixed cost.

B) continue to produce if the price exceeds the average variable cost.

C) immediately shut down.

D) shut down if the price is less than the average fixed cost.

E) continue to produce if the price exceeds the average fixed cost.

A) shut down if the price exceeds the average fixed cost.

B) continue to produce if the price exceeds the average variable cost.

C) immediately shut down.

D) shut down if the price is less than the average fixed cost.

E) continue to produce if the price exceeds the average fixed cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

57

The above table has the total revenue and total cost schedule for Omar, a perfectly competitive grower of potatoes. Omar's total profit is maximised when he produces ________ tonnes of potatoes.

A) 7

B) 6

C) 8

D) 3

E) 5

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

58

The above figure illustrates a perfectly competitive firm. Curve A represents the

A) MR curve.

B) ATC curve.

C) MC curve.

D) AVC curve.

E) AFC curve.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

59

If a perfectly competitive seller is maximising profit and is making zero economic profit, which of the following will this seller do?

A) Go to work in the next-best earning opportunity.

B) Remain open but decrease production in order to make an economic profit.

C) Shut down, with a loss equal to total fixed cost.

D) Continue at the current output, making zero economic profit.

E) Increase production in order to make an economic profit.

A) Go to work in the next-best earning opportunity.

B) Remain open but decrease production in order to make an economic profit.

C) Shut down, with a loss equal to total fixed cost.

D) Continue at the current output, making zero economic profit.

E) Increase production in order to make an economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

60

A perfectly competitive firm is a price taker because

A) it faces a vertical demand curve.

B) many other firms produce the same product.

C) a few firms compete.

D) many firms produce a slightly differentiated product.

E) only one firm produces the product.

A) it faces a vertical demand curve.

B) many other firms produce the same product.

C) a few firms compete.

D) many firms produce a slightly differentiated product.

E) only one firm produces the product.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

61

The above figure shows a perfectly competitive firm. If the market price is more than $20 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

62

For a perfectly competitive banana producer whose average total cost curve does not change, an economic profit could turn into an economic loss if the

A) marginal cost curve shifts downward.

B) market demand for bananas does not change.

C) market demand for bananas decreases.

D) market demand for bananas increases.

E) price of bananas rises.

A) marginal cost curve shifts downward.

B) market demand for bananas does not change.

C) market demand for bananas decreases.

D) market demand for bananas increases.

E) price of bananas rises.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

63

The above figure shows a perfectly competitive firm. If the market price is $15 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

64

A perfectly competitive firm is producing 50 units of output and selling at the market price of $23. The firm's average total cost is $20. What is the firm's total cost?

A) $23

B) $150

C) $1,000

D) $1,150

E) $20

A) $23

B) $150

C) $1,000

D) $1,150

E) $20

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

65

If the market price is $50 per unit for a good produced in a perfectly competitive market and the firm's average total cost is $52, then the firm

A) makes zero economic profit.

B) makes an economic profit of $2 per unit.

C) incurs an economic loss of $2 per unit.

D) incurs a total economic loss of $52.

E) More information is needed to determine the firm's economic profit or loss per unit.

A) makes zero economic profit.

B) makes an economic profit of $2 per unit.

C) incurs an economic loss of $2 per unit.

D) incurs a total economic loss of $52.

E) More information is needed to determine the firm's economic profit or loss per unit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

66

The market for watermelons in Adelaide is perfectly competitive. A watermelon producer making zero economic profit could make an economic profit if the

A) average total cost of selling watermelons does not change.

B) marginal cost of selling watermelons rises.

C) average total cost of selling watermelons falls.

D) average total cost of selling watermelons rises.

E) marginal cost of selling watermelons does not change.

A) average total cost of selling watermelons does not change.

B) marginal cost of selling watermelons rises.

C) average total cost of selling watermelons falls.

D) average total cost of selling watermelons rises.

E) marginal cost of selling watermelons does not change.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

67

Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. If Bill's average total cost curve is ATC, his total economic ________ equals ________.

A) profit; $1,280 per week

B) loss; $800 per week

C) loss; $1,280 per week

D) profit; $480 per week

E) profit; $32 per week

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

68

For a perfectly competitive beef farmer, if the price does not change, an economic profit could turn into an economic loss if the

A) average fixed cost decreases.

B) average total cost curve does not change.

C) average total cost curve shifts upward.

D) average total cost curve shifts downward.

E) marginal cost curve shifts downward.

A) average fixed cost decreases.

B) average total cost curve does not change.

C) average total cost curve shifts upward.

D) average total cost curve shifts downward.

E) marginal cost curve shifts downward.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

69

Use the figure above to answer this question. Consider a perfectly competitive firm in a short-run equilibrium. Figure ________ shows a firm in bad times because the firm makes a(n) ________.

A) A; economic loss of $4 so it must close

B) C; normal profit and can stay open in the long run

C) B; economic loss of $3 per unit

D) B; economic profit because the price exceeds average variable cost

E) A; economic loss of $4 per unit if the firm decides to operate

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

70

If a perfectly competitive firm finds that price is less than ATC, then the firm

A) is making zero economic profit.

B) is incurring an economic loss.

C) will raise its price to increase its economic profit.

D) is making an economic profit.

E) will lower its price to increase its economic profit.

A) is making zero economic profit.

B) is incurring an economic loss.

C) will raise its price to increase its economic profit.

D) is making an economic profit.

E) will lower its price to increase its economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

71

The above figure shows a perfectly competitive firm. If the market price is $20 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

72

Suppose that marginal revenue for a perfectly competitive firm is $20. When the firm produces 10 units, its marginal cost is $20, its average total cost is $22 and its average variable cost is $17. Then, to maximise its profit in the short run, the firm

A) should shut down.

B) must decrease its output to increase its profit.

C) must increase its output to increase its profit.

D) should stay open and incur an economic loss of $20.

E) should not change its production because it is already maximising its profit and is making an economic profit.

A) should shut down.

B) must decrease its output to increase its profit.

C) must increase its output to increase its profit.

D) should stay open and incur an economic loss of $20.

E) should not change its production because it is already maximising its profit and is making an economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

73

Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. Bill's average total cost curve is ATC, so his TOTAL cost of production equals

A) more than $1,800 per week.

B) more than $1,400 per week and less than $1,800 per week.

C) $0 because Bill shuts down.

D) more than $1,200 and less than $1,400 per week.

E) more than $0 and less than $1,200 per week.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

74

The above figure shows a perfectly competitive firm. If the market price is $5 per unit, the firm

A) will definitely shut down to minimise its losses.

B) will stay open to produce and will make zero economic profit.

C) will stay open to produce and will incur an economic loss.

D) will stay open to produce and will make an economic profit.

E) might shut down but more information is needed about the fixed cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

75

If Henry, a perfectly competitive lime grower in Renmark, can sell his limes at a price greater than his average total cost, Henry will

A) make zero economic profit.

B) have an incentive to shut down.

C) incur an economic loss.

D) incur an accounting loss.

E) make an economic profit.

A) make zero economic profit.

B) have an incentive to shut down.

C) incur an economic loss.

D) incur an accounting loss.

E) make an economic profit.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

76

Use the figure above to answer this question. Consider a perfectly competitive market experiencing good times. Figure ________ shows a firm maximising profit in the short run because it produces ________ units and makes an economic profit of ________.

A) A; 100; $2 per unit

B) C; 100; $3 per unit

C) B; 100; $0 per unit

D) A; 90; $3 per unit

E) C; 110; $2 per unit

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

77

Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. At this price, how many lawns will Bill mow per week?

A) Zero

B) 40

C) 50

D) More than 10 and less than 30

E) 30

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

78

A perfectly competitive firm definitely makes an economic profit in the short run if price is

A) greater than average total cost.

B) equal to average total cost.

C) equal to marginal cost.

D) greater than average variable cost.

E) greater than marginal cost.

A) greater than average total cost.

B) equal to average total cost.

C) equal to marginal cost.

D) greater than average variable cost.

E) greater than marginal cost.

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

79

Use the figure above to answer this question. Consider a perfectly competitive firm in a short-run equilibrium. Figure ________ shows a firm in bad times because the firm produces ________ units and makes a(n) ________.

A) A; 100; economic loss

B) B; 90; economic profit

C) C; 100; economic loss

D) A; 110; economic loss

E) C; 100; normal profit

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

80

Use the figure above to answer this question. Figure ________ shows a short-run equilibrium in good times because the firm makes a(n) ________.

A) C; normal profit

B) A; normal profit

C) B; normal profit

D) B; economic loss

E) A; economic profit

Unlock Deck

Unlock for access to all 105 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 105 flashcards in this deck.