Exam 14: Perfect Competition

Exam 1: Getting Started121 Questions

Exam 2: The Australian and Global Economies84 Questions

Exam 3: The Economic Problem70 Questions

Exam 4: Demand and Supply139 Questions

Exam 5: Elasticities of Demand and Supply125 Questions

Exam 6: Efficiency and Fairness of Markets130 Questions

Exam 7: Government Actions in Markets96 Questions

Exam 8: Taxes99 Questions

Exam 9: Global Markets in Action108 Questions

Exam 10: Externalities109 Questions

Exam 11: Public Goods and Common Resources66 Questions

Exam 12: Consumer Choice and Demand78 Questions

Exam 13: Production and Cost106 Questions

Exam 14: Perfect Competition105 Questions

Exam 15: Monopoly143 Questions

Exam 16: Monopolistic Competition82 Questions

Exam 17: Oligopoly71 Questions

Exam 18: Markets for Factors of Production74 Questions

Exam 19: Economic Inequality53 Questions

Select questions type

The market for watermelons in Adelaide is perfectly competitive. A watermelon producer making zero economic profit could make an economic profit if the

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

C

One requirement for an industry to be perfectly competitive is that

Free

(Multiple Choice)

4.8/5 (37)

Correct Answer:Verified

D

A perfectly competitive market is in equilibrium and then demand decreases. The decrease in demand means the market price will ________ and eventually there will be ________.

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

D

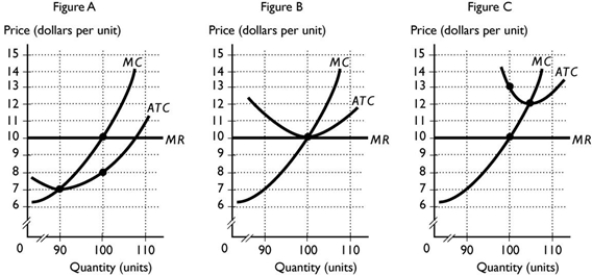

-Use the figure above to answer this question. Consider a perfectly competitive firm in a short-run equilibrium. Figure ________ shows a firm in bad times because the firm makes a(n) ________.

-Use the figure above to answer this question. Consider a perfectly competitive firm in a short-run equilibrium. Figure ________ shows a firm in bad times because the firm makes a(n) ________.

(Multiple Choice)

4.9/5 (31)

For a perfectly competitive firm, profit maximisation occurs when output is such that

(Multiple Choice)

4.9/5 (31)

If the market price is $50 per unit for a good produced in a perfectly competitive market and the firm's average total cost is $52, then the firm

(Multiple Choice)

4.9/5 (29)

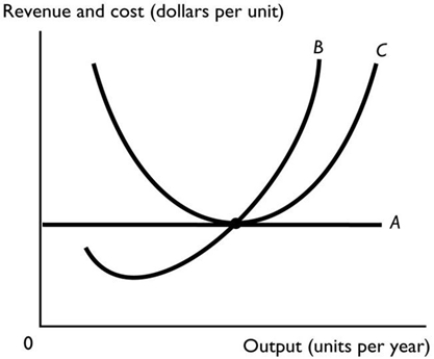

-The above figure illustrates a perfectly competitive firm. Curve A represents the

-The above figure illustrates a perfectly competitive firm. Curve A represents the

(Multiple Choice)

4.9/5 (34)

-The corn market is perfectly competitive, with thousands of corn farmers. In the 2000s, the price of corn soared so that new farmers entered the corn market. Initially, entry ________ the economic profit of the initial corn farmers and in the long run the initial corn farmers ________.

(Multiple Choice)

4.9/5 (42)

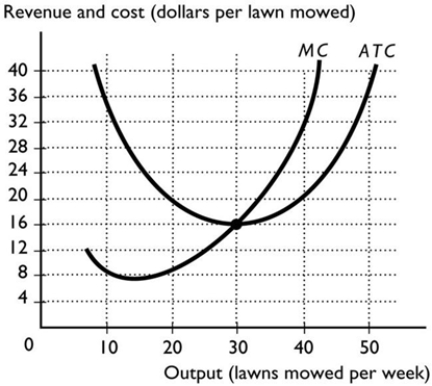

-Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. If Bill's average total cost curve is ATC, his total economic ________ equals ________.

-Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. If Bill's average total cost curve is ATC, his total economic ________ equals ________.

(Multiple Choice)

4.9/5 (34)

For a perfectly competitive beef farmer, if the price does not change, an economic profit could turn into an economic loss if the

(Multiple Choice)

4.8/5 (44)

If a firm in a perfectly competitive market faces an equilibrium price of $5, its marginal revenue

(Multiple Choice)

4.8/5 (32)

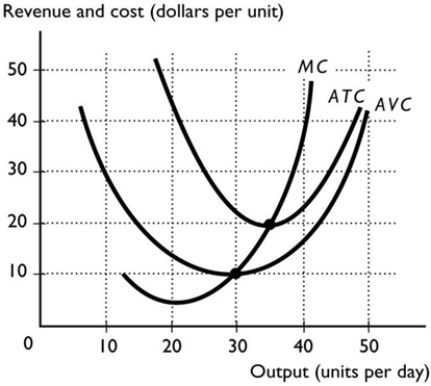

-The above figure shows a perfectly competitive firm. If the market price is $20 per unit, the firm

-The above figure shows a perfectly competitive firm. If the market price is $20 per unit, the firm

(Multiple Choice)

4.8/5 (32)

How does the demand for any one seller's product in perfect competition compare to the market demand for that product?

(Multiple Choice)

4.7/5 (48)

-Bill owns a lawn-care company in Bendigo, whose cost curves are illustrated in the above figure. The market equilibrium price in this perfectly competitive market equals $32 per lawn mowed. Bill's average total cost curve is ATC, so his TOTAL cost of production equals

(Multiple Choice)

4.9/5 (35)

In a perfectly competitive industry, when a firm is producing so that its total revenue equals its total cost, the firm is

(Multiple Choice)

4.9/5 (32)

For a perfectly competitive banana producer whose average total cost curve does not change, an economic profit could turn into an economic loss if the

(Multiple Choice)

4.9/5 (39)

Jennifer's Bakery Shop produces baked goods in a perfectly competitive market. If Jennifer decides to produce her 100th batch of cookies, the marginal cost is $120. She can sell this batch of cookies at a market price of $110. To maximise her profit, Jennifer should

(Multiple Choice)

4.9/5 (43)

Which of the following market types has the fewest number of firms?

(Multiple Choice)

5.0/5 (49)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)