Deck 7: Optimal Risky Portfolios

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

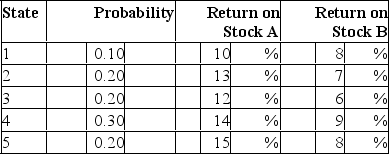

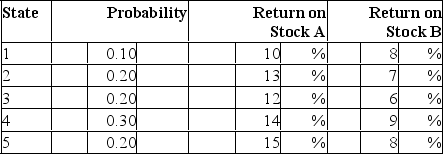

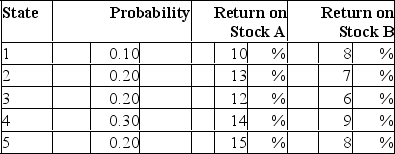

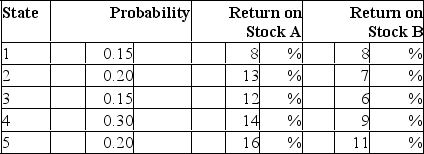

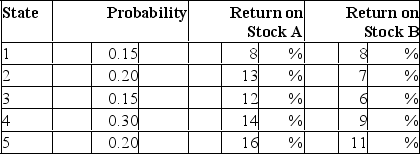

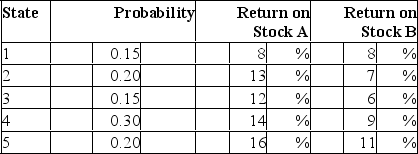

Consider the following probability distribution for stocks A and B:  The variances of stocks A and B are _____ and _____, respectively.

The variances of stocks A and B are _____ and _____, respectively.

A)1.5%; 1.9%

B)2.2%; 1.2%

C)3.2%; 2.0%

D)1.5%; 1.1%

The variances of stocks A and B are _____ and _____, respectively.A)1.5%; 1.9%

B)2.2%; 1.2%

C)3.2%; 2.0%

D)1.5%; 1.1%

Question

Question

Question

Question

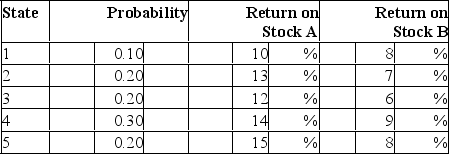

Consider the following probability distribution for stocks A and B:  The standard deviations of stocks A and B are _____ and _____, respectively.

The standard deviations of stocks A and B are _____ and _____, respectively.

A)1.5%; 1.9%

B)2.5%; 1.1%

C)3.2%; 2.0%

D)1.5%; 1.1%

The standard deviations of stocks A and B are _____ and _____, respectively.A)1.5%; 1.9%

B)2.5%; 1.1%

C)3.2%; 2.0%

D)1.5%; 1.1%

Question

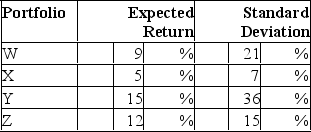

Which one of the following portfolios cannot lie on the efficient frontier as described by Markowitz?

A)Only portfolio A cannot lie on the efficient frontier.

B)Only portfolio B cannot lie on the efficient frontier.

C)Only portfolio C cannot lie on the efficient frontier.

D)Only portfolio D cannot lie on the efficient frontier.

A)Only portfolio A cannot lie on the efficient frontier.

B)Only portfolio B cannot lie on the efficient frontier.

C)Only portfolio C cannot lie on the efficient frontier.

D)Only portfolio D cannot lie on the efficient frontier.

Question

Question

Question

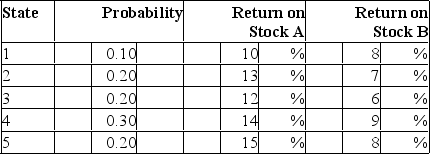

Consider the following probability distribution for stocks A and B:  If you invest 40% of your money in A and 60% in B, what would be your portfolio's expected rate of return and standard deviation?

If you invest 40% of your money in A and 60% in B, what would be your portfolio's expected rate of return and standard deviation?

A)9.9%; 3%

B)9.9%; 1.1%

C)11%; 1.1%

D)11%; 3%

If you invest 40% of your money in A and 60% in B, what would be your portfolio's expected rate of return and standard deviation?A)9.9%; 3%

B)9.9%; 1.1%

C)11%; 1.1%

D)11%; 3%

Question

Question

Question

Consider the following probability distribution for stocks A and B:  The expected rates of return of stocks A and B are _____ and _____, respectively.

The expected rates of return of stocks A and B are _____ and _____, respectively.

A)13.2%; 9%

B)14%; 10%

C)13.2%; 7.7%

D)7.7%; 13.2%

The expected rates of return of stocks A and B are _____ and _____, respectively.A)13.2%; 9%

B)14%; 10%

C)13.2%; 7.7%

D)7.7%; 13.2%

Question

Question

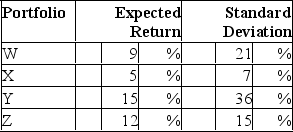

Which one of the following portfolios cannot lie on the efficient frontier as described by Markowitz?

A)Only portfolio W cannot lie on the efficient frontier.

B)Only portfolio X cannot lie on the efficient frontier.

C)Only portfolio Y cannot lie on the efficient frontier.

D)Only portfolio Z cannot lie on the efficient frontier.

A)Only portfolio W cannot lie on the efficient frontier.

B)Only portfolio X cannot lie on the efficient frontier.

C)Only portfolio Y cannot lie on the efficient frontier.

D)Only portfolio Z cannot lie on the efficient frontier.

Question

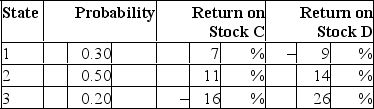

Consider the following probability distribution for stocks A and B:  The coefficient of correlation between A and B is

The coefficient of correlation between A and B is

A)0.46.

B)0.60.

C)0.58.

D)1.20.

The coefficient of correlation between A and B isA)0.46.

B)0.60.

C)0.58.

D)1.20.

Question

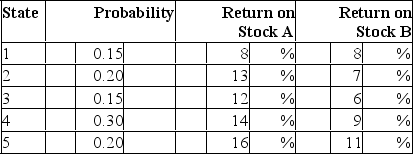

Consider the following probability distribution for stocks A and B:  The expected rate of return and standard deviation of the global minimum variance portfolio, G, are __________ and __________, respectively.

The expected rate of return and standard deviation of the global minimum variance portfolio, G, are __________ and __________, respectively.

A)10.07%; 1.05%

B)8.97%; 2.03%

C)10.07%; 3.01%

D)8.97%; 1.05%

The expected rate of return and standard deviation of the global minimum variance portfolio, G, are __________ and __________, respectively.A)10.07%; 1.05%

B)8.97%; 2.03%

C)10.07%; 3.01%

D)8.97%; 1.05%

Question

Question

Question

Question

Question

Consider the following probability distribution for stocks A and B:  If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?

If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?

A)9.9%; 3%

B)9.9%; 1.1%

C)10%; 1.7%

D)10%; 3%

If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?A)9.9%; 3%

B)9.9%; 1.1%

C)10%; 1.7%

D)10%; 3%

Question

Question

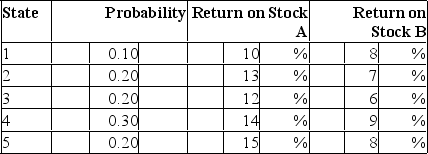

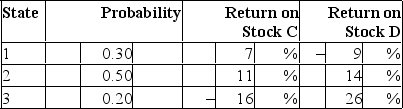

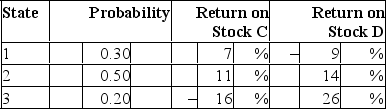

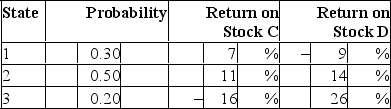

Consider the following probability distribution for stocks C and D:  The coefficient of correlation between C and D is

The coefficient of correlation between C and D is

A)0.67.

B)0.50.

C)-0.50.

D)-0.67.

The coefficient of correlation between C and D isA)0.67.

B)0.50.

C)-0.50.

D)-0.67.

Question

Question

Question

Question

Question

Consider the following probability distribution for stocks C and D:  The expected rates of return of stocks C and D are _____ and _____, respectively.

The expected rates of return of stocks C and D are _____ and _____, respectively.

A)4.4%; 9.5%

B)9.5%; 4.4%

C)6.3%; 8.7%

D)8.7%; 6.2%

The expected rates of return of stocks C and D are _____ and _____, respectively.A)4.4%; 9.5%

B)9.5%; 4.4%

C)6.3%; 8.7%

D)8.7%; 6.2%

Question

Question

Consider the following probability distribution for stocks A and B:  The standard deviations of stocks A and B are _____ and _____, respectively.

The standard deviations of stocks A and B are _____ and _____, respectively.

A)1.56%; 1.99%

B)2.45%; 1.66%

C)3.22%; 2.01%

D)1.54%; 1.11%

The standard deviations of stocks A and B are _____ and _____, respectively.A)1.56%; 1.99%

B)2.45%; 1.66%

C)3.22%; 2.01%

D)1.54%; 1.11%

Question

Question

Question

Consider the following probability distribution for stocks C and D:  If you invest 25% of your money in C and 75% in D, what would be your portfolio's expected rate of return and standard deviation?

If you invest 25% of your money in C and 75% in D, what would be your portfolio's expected rate of return and standard deviation?

A)9.891%; 8.70%

B)9.945%; 11.12%

C)8.225%; 8.70%

D)10.275%; 11.12%

If you invest 25% of your money in C and 75% in D, what would be your portfolio's expected rate of return and standard deviation?A)9.891%; 8.70%

B)9.945%; 11.12%

C)8.225%; 8.70%

D)10.275%; 11.12%

Question

Consider the following probability distribution for stocks A and B:  The expected rates of return of stocks A and B are _____ and _____, respectively.

The expected rates of return of stocks A and B are _____ and _____, respectively.

A)13.2%; 9%

B)13%; 8.4%

C)13.2%; 7.7%

D)7.7%; 13.2%

The expected rates of return of stocks A and B are _____ and _____, respectively.A)13.2%; 9%

B)13%; 8.4%

C)13.2%; 7.7%

D)7.7%; 13.2%

Question

Question

Question

Question

Consider the following probability distribution for stocks A and B:  The coefficient of correlation between A and B is

The coefficient of correlation between A and B is

A)0.474.

B)0.612.

C)0.590.

D)1.206.

The coefficient of correlation between A and B isA)0.474.

B)0.612.

C)0.590.

D)1.206.

Question

Consider the following probability distribution for stocks C and D:  The standard deviations of stocks C and D are _____ and _____, respectively.

The standard deviations of stocks C and D are _____ and _____, respectively.

A)7.62%; 11.24%

B)11.24%; 7.62%

C)10.35%; 12.93%

D)12.93%; 10.35%

The standard deviations of stocks C and D are _____ and _____, respectively.A)7.62%; 11.24%

B)11.24%; 7.62%

C)10.35%; 12.93%

D)12.93%; 10.35%

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 7: Optimal Risky Portfolios

1

Efficient portfolios of N risky securities are portfolios that

A)are formed with the securities that have the highest rates of return regardless of their standard deviations.

B)have the highest rates of return for a given level of risk.

C)are selected from those securities with the lowest standard deviations regardless of their returns.

D)have the highest risk and rates of return and the highest standard deviations.

A)are formed with the securities that have the highest rates of return regardless of their standard deviations.

B)have the highest rates of return for a given level of risk.

C)are selected from those securities with the lowest standard deviations regardless of their returns.

D)have the highest risk and rates of return and the highest standard deviations.

B

2

Unique risk is also referred to as

A)systematic risk or diversifiable risk.

B)systematic risk or market risk.

C)diversifiable risk or market risk.

D)diversifiable risk or firm-specific risk.

A)systematic risk or diversifiable risk.

B)systematic risk or market risk.

C)diversifiable risk or market risk.

D)diversifiable risk or firm-specific risk.

D

3

The risk that can be diversified away is

A)firm-specific risk.

B)beta.

C)systematic risk.

D)market risk.

A)firm-specific risk.

B)beta.

C)systematic risk.

D)market risk.

A

4

Nonsystematic risk is also referred to as

A)market risk or diversifiable risk.

B)firm-specific risk or market risk.

C)diversifiable risk or market risk.

D)diversifiable risk or unique risk.

A)market risk or diversifiable risk.

B)firm-specific risk or market risk.

C)diversifiable risk or market risk.

D)diversifiable risk or unique risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

The capital allocation line provided by a risk-free security and N risky securities is

A)the line that connects the risk-free rate and the global minimum-variance portfolio of the risky securities.

B)the line that connects the risk-free rate and the portfolio of the risky securities that has the highest expected return on the efficient frontier.

C)the line tangent to the efficient frontier of risky securities drawn from the risk-free rate.

D)the horizontal line drawn from the risk-free rate.

A)the line that connects the risk-free rate and the global minimum-variance portfolio of the risky securities.

B)the line that connects the risk-free rate and the portfolio of the risky securities that has the highest expected return on the efficient frontier.

C)the line tangent to the efficient frontier of risky securities drawn from the risk-free rate.

D)the horizontal line drawn from the risk-free rate.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

The standard deviation of a portfolio of risky securities is

A)the square root of the weighted sum of the securities' variances.

B)the square root of the sum of the securities' variances.

C)the square root of the weighted sum of the securities' variances and covariances.

D)the square root of the sum of the securities' covariances.

A)the square root of the weighted sum of the securities' variances.

B)the square root of the sum of the securities' variances.

C)the square root of the weighted sum of the securities' variances and covariances.

D)the square root of the sum of the securities' covariances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

Firm-specific risk is also referred to as

A)systematic risk or diversifiable risk.

B)systematic risk or market risk.

C)diversifiable risk or market risk.

D)diversifiable risk or unique risk.

A)systematic risk or diversifiable risk.

B)systematic risk or market risk.

C)diversifiable risk or market risk.

D)diversifiable risk or unique risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

The risk that cannot be diversified away is

A)firm-specific risk.

B)unique.

C)nonsystematic risk.

D)market risk.

A)firm-specific risk.

B)unique.

C)nonsystematic risk.

D)market risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

Other things equal, diversification is most effective when

A)securities' returns are uncorrelated.

B)securities' returns are positively correlated.

C)securities' returns are high.

D)securities' returns are negatively correlated.

A)securities' returns are uncorrelated.

B)securities' returns are positively correlated.

C)securities' returns are high.

D)securities' returns are negatively correlated.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

Consider an investment opportunity set formed with two securities that are perfectly negatively correlated.The global-minimum variance portfolio has a standard deviation that is always

A)greater than zero.

B)equal to zero.

C)equal to the sum of the securities' standard deviations.

D)equal to -1.

A)greater than zero.

B)equal to zero.

C)equal to the sum of the securities' standard deviations.

D)equal to -1.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

No diversifiable risk is also referred to as

A)systematic risk or unique risk.

B)systematic risk or market risk.

C)unique risk or market risk.

D)unique risk or firm-specific risk.

A)systematic risk or unique risk.

B)systematic risk or market risk.

C)unique risk or market risk.

D)unique risk or firm-specific risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

Market risk is also referred to as

A)systematic risk or diversifiable risk.

B)systematic risk or non-diversifiable risk.

C)unique risk or non-diversifiable risk.

D)unique risk or diversifiable risk.

A)systematic risk or diversifiable risk.

B)systematic risk or non-diversifiable risk.

C)unique risk or non-diversifiable risk.

D)unique risk or diversifiable risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

The efficient frontier of risky assets is

A)the portion of the investment opportunity set that lies above the global minimum variance portfolio.

B)the portion of the investment opportunity set that represents the highest standard deviations.

C)the portion of the investment opportunity set that includes the portfolios with the lowest standard deviation.

D)the set of portfolios that have zero standard deviation.

A)the portion of the investment opportunity set that lies above the global minimum variance portfolio.

B)the portion of the investment opportunity set that represents the highest standard deviations.

C)the portion of the investment opportunity set that includes the portfolios with the lowest standard deviation.

D)the set of portfolios that have zero standard deviation.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statement(s) is(are) false regarding the selection of a portfolio from those that lie on the capital allocation line? I) Less risk-averse investors will invest more in the risk-free security and less in the optimal risky portfolio than more risk-averse investors.

II) More risk-averse investors will invest less in the optimal risky portfolio and more in the risk-free security than less risk-averse investors.

III) Investors choose the portfolio that maximizes their expected utility.

A)I only

B)II only

C)III only

D)I and II

II) More risk-averse investors will invest less in the optimal risky portfolio and more in the risk-free security than less risk-averse investors.

III) Investors choose the portfolio that maximizes their expected utility.

A)I only

B)II only

C)III only

D)I and II

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Systematic risk is also referred to as

A)market risk or non-diversifiable risk.

B)market risk or diversifiable risk.

C)unique risk or non-diversifiable risk.

D)unique risk or diversifiable risk.

A)market risk or non-diversifiable risk.

B)market risk or diversifiable risk.

C)unique risk or non-diversifiable risk.

D)unique risk or diversifiable risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statement(s) is(are) true regarding the variance of a portfolio of two risky securities? I) The higher the coefficient of correlation between securities, the greater the reduction in the portfolio variance.

II) There is a linear relationship between the securities' coefficient of correlation and the portfolio variance.

III) The degree to which the portfolio variance is reduced depends on the degree of correlation between securities.

A)I only

B)II only

C)III only

D)I and II

II) There is a linear relationship between the securities' coefficient of correlation and the portfolio variance.

III) The degree to which the portfolio variance is reduced depends on the degree of correlation between securities.

A)I only

B)II only

C)III only

D)I and II

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

Diversifiable risk is also referred to as

A)systematic risk or unique risk.

B)systematic risk or market risk.

C)unique risk or market risk.

D)unique risk or firm-specific risk.

A)systematic risk or unique risk.

B)systematic risk or market risk.

C)unique risk or market risk.

D)unique risk or firm-specific risk.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

The expected return of a portfolio of risky securities

A)is a weighted average of the securities' returns.

B)is the sum of the securities' returns.

C)is the weighted sum of the securities' variances and covariances.

D)is a weighted average of the securities' returns and the weighted sum of the securities' variances and covariances.

A)is a weighted average of the securities' returns.

B)is the sum of the securities' returns.

C)is the weighted sum of the securities' variances and covariances.

D)is a weighted average of the securities' returns and the weighted sum of the securities' variances and covariances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

The variance of a portfolio of risky securities

A)is a weighted sum of the securities' variances.

B)is the sum of the securities' variances.

C)is the weighted sum of the securities' variances and covariances.

D)is the sum of the securities' covariances.

A)is a weighted sum of the securities' variances.

B)is the sum of the securities' variances.

C)is the weighted sum of the securities' variances and covariances.

D)is the sum of the securities' covariances.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statement(s) is(are) false regarding the variance of a portfolio of two risky securities? I) The higher the coefficient of correlation between securities, the greater the reduction in the portfolio variance.

II) There is a linear relationship between the securities' coefficient of correlation and the portfolio variance.

III) The degree to which the portfolio variance is reduced depends on the degree of correlation between securities.

A)I only

B)II only

C)III only

D)I and II

II) There is a linear relationship between the securities' coefficient of correlation and the portfolio variance.

III) The degree to which the portfolio variance is reduced depends on the degree of correlation between securities.

A)I only

B)II only

C)III only

D)I and II

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

Consider the following probability distribution for stocks A and B: The variances of stocks A and B are _____ and _____, respectively.

A)1.5%; 1.9%

B)2.2%; 1.2%

C)3.2%; 2.0%

D)1.5%; 1.1%

The variances of stocks A and B are _____ and _____, respectively.A)1.5%; 1.9%

B)2.2%; 1.2%

C)3.2%; 2.0%

D)1.5%; 1.1%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

The measure of risk in a Markowitz efficient frontier is

A)specific risk.

B)standard deviation of returns.

C)reinvestment risk.

D)beta.

A)specific risk.

B)standard deviation of returns.

C)reinvestment risk.

D)beta.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Which statement about portfolio diversification is correct?

A)Proper diversification can eliminate systematic risk.

B)The risk-reducing benefits of diversification do not occur meaningfully until at least 50-60 individual securities have been purchased.

C)Because diversification reduces a portfolio's total risk, it necessarily reduces the portfolio's expected return.

D)Typically, as more securities are added to a portfolio, total risk would be expected to decrease at a decreasing rate.

A)Proper diversification can eliminate systematic risk.

B)The risk-reducing benefits of diversification do not occur meaningfully until at least 50-60 individual securities have been purchased.

C)Because diversification reduces a portfolio's total risk, it necessarily reduces the portfolio's expected return.

D)Typically, as more securities are added to a portfolio, total risk would be expected to decrease at a decreasing rate.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

The unsystematic risk of a specific security

A)is likely to be higher in an increasing market.

B)results from factors unique to the firm.

C)depends on market volatility.

D)cannot be diversified away.

A)is likely to be higher in an increasing market.

B)results from factors unique to the firm.

C)depends on market volatility.

D)cannot be diversified away.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

Consider the following probability distribution for stocks A and B: The standard deviations of stocks A and B are _____ and _____, respectively.

A)1.5%; 1.9%

B)2.5%; 1.1%

C)3.2%; 2.0%

D)1.5%; 1.1%

The standard deviations of stocks A and B are _____ and _____, respectively.A)1.5%; 1.9%

B)2.5%; 1.1%

C)3.2%; 2.0%

D)1.5%; 1.1%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

Which one of the following portfolios cannot lie on the efficient frontier as described by Markowitz?

A)Only portfolio A cannot lie on the efficient frontier.

B)Only portfolio B cannot lie on the efficient frontier.

C)Only portfolio C cannot lie on the efficient frontier.

D)Only portfolio D cannot lie on the efficient frontier.

A)Only portfolio A cannot lie on the efficient frontier.

B)Only portfolio B cannot lie on the efficient frontier.

C)Only portfolio C cannot lie on the efficient frontier.

D)Only portfolio D cannot lie on the efficient frontier.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

Portfolio theory as described by Markowitz is most concerned with

A)the elimination of systematic risk.

B)the effect of diversification on portfolio risk.

C)the identification of unsystematic risk.

D)active portfolio management to enhance returns.

A)the elimination of systematic risk.

B)the effect of diversification on portfolio risk.

C)the identification of unsystematic risk.

D)active portfolio management to enhance returns.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

For a two-stock portfolio, what would be the preferred correlation coefficient between the two stocks?

A)+1.00

B)+0.50

C)0.00

D)-1.00

A)+1.00

B)+0.50

C)0.00

D)-1.00

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

Consider the following probability distribution for stocks A and B: If you invest 40% of your money in A and 60% in B, what would be your portfolio's expected rate of return and standard deviation?

A)9.9%; 3%

B)9.9%; 1.1%

C)11%; 1.1%

D)11%; 3%

If you invest 40% of your money in A and 60% in B, what would be your portfolio's expected rate of return and standard deviation?A)9.9%; 3%

B)9.9%; 1.1%

C)11%; 1.1%

D)11%; 3%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

Given an optimal risky portfolio with expected return of 6%, standard deviation of 23%, and a risk free rate of 3%, what is the slope of the best feasible CAL?

A)0.64

B)0.39

C)0.08

D)0.13

A)0.64

B)0.39

C)0.08

D)0.13

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is not a source of systematic risk?

A)The business cycle

B)Interest rates

C)Personnel changes

D)The inflation rate

A)The business cycle

B)Interest rates

C)Personnel changes

D)The inflation rate

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

32

Consider the following probability distribution for stocks A and B: The expected rates of return of stocks A and B are _____ and _____, respectively.

A)13.2%; 9%

B)14%; 10%

C)13.2%; 7.7%

D)7.7%; 13.2%

The expected rates of return of stocks A and B are _____ and _____, respectively.A)13.2%; 9%

B)14%; 10%

C)13.2%; 7.7%

D)7.7%; 13.2%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

The individual investor's optimal portfolio is designated by

A)the point of tangency with the indifference curve and the capital allocation line.

B)the point of highest reward to variability ratio in the opportunity set.

C)the point of tangency with the opportunity set and the capital allocation line.

D)the point of the highest reward to variability ratio in the indifference curve.

A)the point of tangency with the indifference curve and the capital allocation line.

B)the point of highest reward to variability ratio in the opportunity set.

C)the point of tangency with the opportunity set and the capital allocation line.

D)the point of the highest reward to variability ratio in the indifference curve.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

Which one of the following portfolios cannot lie on the efficient frontier as described by Markowitz?

A)Only portfolio W cannot lie on the efficient frontier.

B)Only portfolio X cannot lie on the efficient frontier.

C)Only portfolio Y cannot lie on the efficient frontier.

D)Only portfolio Z cannot lie on the efficient frontier.

A)Only portfolio W cannot lie on the efficient frontier.

B)Only portfolio X cannot lie on the efficient frontier.

C)Only portfolio Y cannot lie on the efficient frontier.

D)Only portfolio Z cannot lie on the efficient frontier.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

Consider the following probability distribution for stocks A and B: The coefficient of correlation between A and B is

A)0.46.

B)0.60.

C)0.58.

D)1.20.

The coefficient of correlation between A and B isA)0.46.

B)0.60.

C)0.58.

D)1.20.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

Consider the following probability distribution for stocks A and B: The expected rate of return and standard deviation of the global minimum variance portfolio, G, are __________ and __________, respectively.

A)10.07%; 1.05%

B)8.97%; 2.03%

C)10.07%; 3.01%

D)8.97%; 1.05%

The expected rate of return and standard deviation of the global minimum variance portfolio, G, are __________ and __________, respectively.A)10.07%; 1.05%

B)8.97%; 2.03%

C)10.07%; 3.01%

D)8.97%; 1.05%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

In a two-security minimum variance portfolio where the correlation between securities is greater than -1.0,

A)the security with the higher standard deviation will be weighted more heavily.

B)the security with the higher standard deviation will be weighted less heavily.

C)the two securities will be equally weighted.

D)the risk will be zero.

A)the security with the higher standard deviation will be weighted more heavily.

B)the security with the higher standard deviation will be weighted less heavily.

C)the two securities will be equally weighted.

D)the risk will be zero.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

Security X has expected return of 12% and standard deviation of 18%.Security Y has expected return of 15% and standard deviation of 26%.If the two securities have a correlation coefficient of 0.7, what is their covariance?

A)0.038

B)0.070

C)0.018

D)0.033

A)0.038

B)0.070

C)0.018

D)0.033

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

The global minimum variance portfolio formed from two risky securities will be riskless when the correlation coefficient between the two securities is

A)0.0.

B)1.0.

C)0.5.

D)-1.0.

A)0.0.

B)1.0.

C)0.5.

D)-1.0.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

An investor who wishes to form a portfolio that lies to the right of the optimal risky portfolio on the capital allocation line must

A)lend some of her money at the risk-free rate.

B)borrow some money at the risk-free rate and invest in the optimal risky portfolio.

C)invest only in risky securities.

D)borrow some money at the risk-free rate, invest in the optimal risky portfolio, and invest only in risky securities

A)lend some of her money at the risk-free rate.

B)borrow some money at the risk-free rate and invest in the optimal risky portfolio.

C)invest only in risky securities.

D)borrow some money at the risk-free rate, invest in the optimal risky portfolio, and invest only in risky securities

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

Consider the following probability distribution for stocks A and B: If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?

A)9.9%; 3%

B)9.9%; 1.1%

C)10%; 1.7%

D)10%; 3%

If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?A)9.9%; 3%

B)9.9%; 1.1%

C)10%; 1.7%

D)10%; 3%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

Given an optimal risky portfolio with expected return of 12%, standard deviation of 26%, and a risk free rate of 3%, what is the slope of the best feasible CAL?

A)0.64

B)0.14

C)0.08

D)0.35

A)0.64

B)0.14

C)0.08

D)0.35

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

Consider the following probability distribution for stocks C and D: The coefficient of correlation between C and D is

A)0.67.

B)0.50.

C)-0.50.

D)-0.67.

The coefficient of correlation between C and D isA)0.67.

B)0.50.

C)-0.50.

D)-0.67.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

Given an optimal risky portfolio with expected return of 16%, standard deviation of 20%, and a risk-free rate of 4%, what is the slope of the best feasible CAL?

A)0.60

B)0.14

C)0.08

D)0.36

A)0.60

B)0.14

C)0.08

D)0.36

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

Security X has expected return of 14% and standard deviation of 22%.Security Y has expected return of 16% and standard deviation of 28%.If the two securities have a correlation coefficient of 0.8, what is their covariance?

A)0.038

B)0.049

C)0.018

D)0.013

A)0.038

B)0.049

C)0.018

D)0.013

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

The line representing all combinations of portfolio expected returns and standard deviations that can be constructed from two available assets is called the

A)risk/reward tradeoff line.

B)capital allocation line.

C)efficient frontier.

D)portfolio opportunity set.

A)risk/reward tradeoff line.

B)capital allocation line.

C)efficient frontier.

D)portfolio opportunity set.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

The separation property refers to the conclusion that

A)the determination of the best risky portfolio is objective, and the choice of the best complete portfolio is subjective.

B)the choice of the best complete portfolio is objective, and the determination of the best risky portfolio is objective.

C)the choice of inputs to be used to determine the efficient frontier is objective, and the choice of the best CAL is subjective.

D)the determination of the best CAL is objective, and the choice of the inputs to be used to determine the efficient frontier is subjective.

A)the determination of the best risky portfolio is objective, and the choice of the best complete portfolio is subjective.

B)the choice of the best complete portfolio is objective, and the determination of the best risky portfolio is objective.

C)the choice of inputs to be used to determine the efficient frontier is objective, and the choice of the best CAL is subjective.

D)the determination of the best CAL is objective, and the choice of the inputs to be used to determine the efficient frontier is subjective.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Consider the following probability distribution for stocks C and D: The expected rates of return of stocks C and D are _____ and _____, respectively.

A)4.4%; 9.5%

B)9.5%; 4.4%

C)6.3%; 8.7%

D)8.7%; 6.2%

The expected rates of return of stocks C and D are _____ and _____, respectively.A)4.4%; 9.5%

B)9.5%; 4.4%

C)6.3%; 8.7%

D)8.7%; 6.2%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

The risk that can be diversified away in a portfolio is referred to as ___________. I) diversifiable risk

II) unique risk

III) systematic risk

IV) firm-specific risk

A)I, III, and IV

B)II, III, and IV

C)III and IV

D)I, II, and IV

II) unique risk

III) systematic risk

IV) firm-specific risk

A)I, III, and IV

B)II, III, and IV

C)III and IV

D)I, II, and IV

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Consider the following probability distribution for stocks A and B: The standard deviations of stocks A and B are _____ and _____, respectively.

A)1.56%; 1.99%

B)2.45%; 1.66%

C)3.22%; 2.01%

D)1.54%; 1.11%

The standard deviations of stocks A and B are _____ and _____, respectively.A)1.56%; 1.99%

B)2.45%; 1.66%

C)3.22%; 2.01%

D)1.54%; 1.11%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

When two risky securities that are positively correlated but not perfectly correlated are held in a portfolio,

A)the portfolio standard deviation will be greater than the weighted average of the individual security standard deviations.

B)the portfolio standard deviation will be less than the weighted average of the individual security standard deviations.

C)the portfolio standard deviation will be equal to the weighted average of the individual security standard deviations.

D)the portfolio standard deviation will always be equal to the securities' covariance. Whenever two securities are less than perfectly positively correlated, the standard deviation of the portfolio of the two assets will be less than the weighted average of the two securities' standard deviations.There is some benefit to diversification in this case.

A)the portfolio standard deviation will be greater than the weighted average of the individual security standard deviations.

B)the portfolio standard deviation will be less than the weighted average of the individual security standard deviations.

C)the portfolio standard deviation will be equal to the weighted average of the individual security standard deviations.

D)the portfolio standard deviation will always be equal to the securities' covariance. Whenever two securities are less than perfectly positively correlated, the standard deviation of the portfolio of the two assets will be less than the weighted average of the two securities' standard deviations.There is some benefit to diversification in this case.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

In words, the covariance considers the probability of each scenario happening and the interaction between

A)securities' returns relative to their variances.

B)securities' returns relative to their mean returns.

C)securities' returns relative to other securities' returns.

D)the level of return a security has in that scenario and the overall portfolio return.

A)securities' returns relative to their variances.

B)securities' returns relative to their mean returns.

C)securities' returns relative to other securities' returns.

D)the level of return a security has in that scenario and the overall portfolio return.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

Consider the following probability distribution for stocks C and D: If you invest 25% of your money in C and 75% in D, what would be your portfolio's expected rate of return and standard deviation?

A)9.891%; 8.70%

B)9.945%; 11.12%

C)8.225%; 8.70%

D)10.275%; 11.12%

If you invest 25% of your money in C and 75% in D, what would be your portfolio's expected rate of return and standard deviation?A)9.891%; 8.70%

B)9.945%; 11.12%

C)8.225%; 8.70%

D)10.275%; 11.12%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

Consider the following probability distribution for stocks A and B: The expected rates of return of stocks A and B are _____ and _____, respectively.

A)13.2%; 9%

B)13%; 8.4%

C)13.2%; 7.7%

D)7.7%; 13.2%

The expected rates of return of stocks A and B are _____ and _____, respectively.A)13.2%; 9%

B)13%; 8.4%

C)13.2%; 7.7%

D)7.7%; 13.2%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

Given an optimal risky portfolio with expected return of 12%, standard deviation of 26%, and a risk free rate of 5%, what is the slope of the best feasible CAL?

A)0.64

B)0.27

C)0.08

D)0.33

A)0.64

B)0.27

C)0.08

D)0.33

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

The standard deviation of a two-asset portfolio is a linear function of the assets' weights when

A)the assets have a correlation coefficient less than zero.

B)the assets have a correlation coefficient equal to zero.

C)the assets have a correlation coefficient greater than zero.

D)the assets have a correlation coefficient equal to one.

A)the assets have a correlation coefficient less than zero.

B)the assets have a correlation coefficient equal to zero.

C)the assets have a correlation coefficient greater than zero.

D)the assets have a correlation coefficient equal to one.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

Consider two perfectly negatively correlated risky securities, K and L.K has an expected rate of return of 13% and a standard deviation of 19%.L has an expected rate of return of 10% and a standard deviation of 16%. The weights of K and L in the global minimum variance portfolio are _____ and _____, respectively.

A)0.24; 0.76

B)0.50; 0.50

C)0.46; 0.54

D)0.45; 0.55

A)0.24; 0.76

B)0.50; 0.50

C)0.46; 0.54

D)0.45; 0.55

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

Consider the following probability distribution for stocks A and B: The coefficient of correlation between A and B is

A)0.474.

B)0.612.

C)0.590.

D)1.206.

The coefficient of correlation between A and B isA)0.474.

B)0.612.

C)0.590.

D)1.206.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Consider the following probability distribution for stocks C and D: The standard deviations of stocks C and D are _____ and _____, respectively.

A)7.62%; 11.24%

B)11.24%; 7.62%

C)10.35%; 12.93%

D)12.93%; 10.35%

The standard deviations of stocks C and D are _____ and _____, respectively.A)7.62%; 11.24%

B)11.24%; 7.62%

C)10.35%; 12.93%

D)12.93%; 10.35%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

As the number of securities in a portfolio is increased, what happens to the average portfolio standard deviation?

A)It increases at an increasing rate.

B)It increases at a decreasing rate.

C)It decreases at an increasing rate.

D)It decreases at a decreasing rate.

A)It increases at an increasing rate.

B)It increases at a decreasing rate.

C)It decreases at an increasing rate.

D)It decreases at a decreasing rate.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

Security X has expected return of 7% and standard deviation of 14%.Security Y has expected return of 11% and standard deviation of 22%.If the two securities have a correlation coefficient of -0.45, what is their covariance?

A)0.0388

B)-0.0108

C)0.0184

D)-0.0139

A)0.0388

B)-0.0108

C)0.0184

D)-0.0139

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

Security M has expected return of 17% and standard deviation of 32%.Security S has expected return of 13% and standard deviation of 19%.If the two securities have a correlation coefficient of 0.78, what is their covariance?

A)0.038

B)0.049

C)0.047

D)0.045

A)0.038

B)0.049

C)0.047

D)0.045

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

Consider two perfectly negatively correlated risky securities, K and L.K has an expected rate of return of 13% and a standard deviation of 19%.L has an expected rate of return of 10% and a standard deviation of 16%. The risk-free portfolio that can be formed with the two securities will earn _____ rate of return.

A)9.5%

B)11.4%

C)10.9%

D)9.9%

A)9.5%

B)11.4%

C)10.9%

D)9.9%

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.