Exam 7: Optimal Risky Portfolios

Exam 1: The Investment Environment51 Questions

Exam 2: Financial Markets, Asset Classes and Financial Instruments82 Questions

Exam 3: How Securities Are Traded65 Questions

Exam 4: Mutual Funds and Other Investment Companies59 Questions

Exam 5: Risk, Return, and the Historical Record64 Questions

Exam 6: Capital Allocation to Risky Assets59 Questions

Exam 7: Optimal Risky Portfolios63 Questions

Exam 8: Index Models76 Questions

Exam 9: The Capital Asset Pricing Model71 Questions

Exam 10: Arbitrage Pricing Theory and Multifactor Models of Risk and Return62 Questions

Exam 11: The Efficient Market Hypothesis42 Questions

Exam 12: Behavioural Finance and Technical Analysis41 Questions

Exam 13: Empirical Evidence on Security Returns41 Questions

Exam 14: Bond Prices and Yields110 Questions

Exam 15: The Term Structure of Interest Rates58 Questions

Exam 16: Managing Bond Portfolios69 Questions

Exam 17: Macroeconomic and Industry Analysis67 Questions

Exam 18: Equity Valuation Models106 Questions

Exam 19: Financial Statement Analysis71 Questions

Exam 20: Options Markets: Introduction88 Questions

Exam 21: Option Valuation85 Questions

Exam 22: Futures Markets85 Questions

Exam 23: Futures, Swaps, and Risk Management51 Questions

Exam 24: Portfolio Performance Evaluation68 Questions

Exam 25: International Diversification48 Questions

Exam 26: Hedge Funds46 Questions

Exam 27: The Theory of Active Portfolio Management48 Questions

Exam 28: Investment Policy and the Framework of the Cfa Institute76 Questions

Select questions type

In a two-security minimum variance portfolio where the correlation between securities is greater than -1.0,

Free

(Multiple Choice)

4.7/5  (28)

(28)

Correct Answer: Verified

Verified

B

The risk that can be diversified away in a portfolio is referred to as ___________. I) diversifiable risk

II) unique risk

III) systematic risk

IV) firm-specific risk

Free

(Multiple Choice)

4.9/5 (35)

Correct Answer:Verified

D

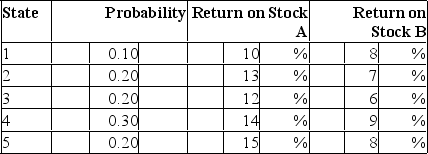

Consider the following probability distribution for stocks A and B:  The standard deviations of stocks A and B are _____ and _____, respectively.

The standard deviations of stocks A and B are _____ and _____, respectively.

Free

(Multiple Choice)

4.8/5 (30)

Correct Answer:Verified

D

Efficient portfolios of N risky securities are portfolios that

(Multiple Choice)

4.8/5 (34)

Which of the following statement(s) is(are) false regarding the selection of a portfolio from those that lie on the capital allocation line? I) Less risk-averse investors will invest more in the risk-free security and less in the optimal risky portfolio than more risk-averse investors.

II) More risk-averse investors will invest less in the optimal risky portfolio and more in the risk-free security than less risk-averse investors.

III) Investors choose the portfolio that maximizes their expected utility.

(Multiple Choice)

4.8/5 (43)

The standard deviation of a two-asset portfolio is a linear function of the assets' weights when

(Multiple Choice)

4.8/5 (38)

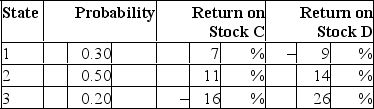

Consider the following probability distribution for stocks C and D:  The standard deviations of stocks C and D are _____ and _____, respectively.

The standard deviations of stocks C and D are _____ and _____, respectively.

(Multiple Choice)

4.9/5 (35)

The global minimum variance portfolio formed from two risky securities will be riskless when the correlation coefficient between the two securities is

(Multiple Choice)

4.8/5 (39)

The line representing all combinations of portfolio expected returns and standard deviations that can be constructed from two available assets is called the

(Multiple Choice)

4.9/5 (31)

When two risky securities that are positively correlated but not perfectly correlated are held in a portfolio,

(Multiple Choice)

4.7/5 (39)

Given an optimal risky portfolio with expected return of 6%, standard deviation of 23%, and a risk free rate of 3%, what is the slope of the best feasible CAL?

(Multiple Choice)

4.8/5 (43)

For a two-stock portfolio, what would be the preferred correlation coefficient between the two stocks?

(Multiple Choice)

4.8/5 (37)

The standard deviation of a portfolio of risky securities is

(Multiple Choice)

4.9/5 (42)

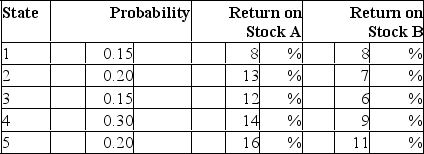

Consider the following probability distribution for stocks A and B:  If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?

If you invest 35% of your money in A and 65% in B, what would be your portfolio's expected rate of return and standard deviation?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)