Deck 7: An Introduction to Portfolio Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

What is the expected return of the three stock portfolio described below?

A)18.45%

B)12.82%

C)13.38%

D)15.27%

E)16.67%

A)18.45%

B)12.82%

C)13.38%

D)15.27%

E)16.67%

Question

Question

Question

Question

Question

Question

Question

Question

Question

What is the expected return of the three stock portfolio described below?

A)21.33%

B)12.50%

C)32.00%

D)15.75%

E)16.80%

A)21.33%

B)12.50%

C)32.00%

D)15.75%

E)16.80%

Question

What is the expected return of the three stock portfolio described below?

A)14.89%

B)16.22%

C)12.66%

D)13.85%

E)16.99%

A)14.89%

B)16.22%

C)12.66%

D)13.85%

E)16.99%

Question

Question

Question

What is the expected return of the three stock portfolio described below?

A)18.27%

B)14.33%

C)16.33%

D)12.72%

E)16.45%

A)18.27%

B)14.33%

C)16.33%

D)12.72%

E)16.45%

Question

Question

Question

Question

What is the expected return of the three stock portfolio described below?

A)12.04%

B)12.83%

C)13.07%

D)15.89%

E)17.91%

A)12.04%

B)12.83%

C)13.07%

D)15.89%

E)17.91%

Question

Question

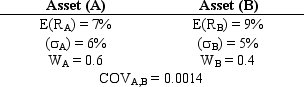

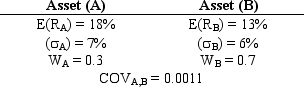

Exhibit 7.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.7. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)5.8%

B)6.1%

C)6.9%

D)7.8%

E)8.9%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.7. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)5.8%

B)6.1%

C)6.9%

D)7.8%

E)8.9%

Question

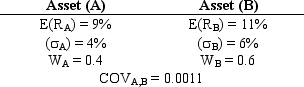

Exhibit 7.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.2. What is the standard deviation of this portfolio?

A)5.45%

B)18.64%

C)20.0%

D)22.5%

E)13.65%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.2. What is the standard deviation of this portfolio?

A)5.45%

B)18.64%

C)20.0%

D)22.5%

E)13.65%

Question

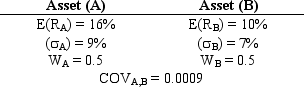

Exhibit 7.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.1. What is the standard deviation of this portfolio?

A)8.79%

B)13.75%

C)12.5%

D)7.72%

E)5.64%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.1. What is the standard deviation of this portfolio?

A)8.79%

B)13.75%

C)12.5%

D)7.72%

E)5.64%

Question

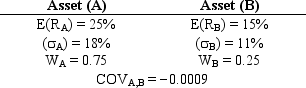

Exhibit 7.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.5. What is the standard deviation of this portfolio?

A)3.89%

B)4.61%

C)5.02%

D)6.83%

E)6.09%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.5. What is the standard deviation of this portfolio?

A)3.89%

B)4.61%

C)5.02%

D)6.83%

E)6.09%

Question

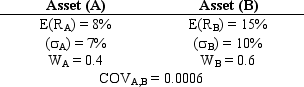

Exhibit 7.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.6. What is the standard deviation of this portfolio?

A)6.08%

B)5.89%

C)7.06%

D)6.54%

E)7.26%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.6. What is the standard deviation of this portfolio?

A)6.08%

B)5.89%

C)7.06%

D)6.54%

E)7.26%

Question

Exhibit 7.10

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.10. What is the standard deviation of this portfolio?

A)3.02%

B)4.88%

C)5.24%

D)5.98%

E)6.52%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.10. What is the standard deviation of this portfolio?

A)3.02%

B)4.88%

C)5.24%

D)5.98%

E)6.52%

Question

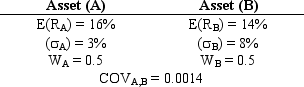

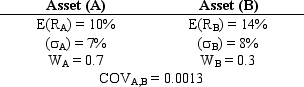

Exhibit 7.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.3. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.95%

B)9.30%

C)9.95%

D)10.20%

E)10.70%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.3. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.95%

B)9.30%

C)9.95%

D)10.20%

E)10.70%

Question

Exhibit 7.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.4. What is the standard deviation of this portfolio?

A)5.02%

B)3.88%

C)6.21%

D)4.04%

E)4.34%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.4. What is the standard deviation of this portfolio?

A)5.02%

B)3.88%

C)6.21%

D)4.04%

E)4.34%

Question

Exhibit 7.10

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)11%

B)12%

C)13%

D)14%

E)15%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)11%

B)12%

C)13%

D)14%

E)15%

Question

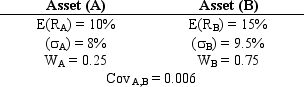

Exhibit 7.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.9. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.10%

B)11.60%

C)13.88%

D)14.50%

E)15.37%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.9. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.10%

B)11.60%

C)13.88%

D)14.50%

E)15.37%

Question

Exhibit 7.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.5. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.0%

B)12.2%

C)7.4%

D)9.1%

E)11.6%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.5. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.0%

B)12.2%

C)7.4%

D)9.1%

E)11.6%

Question

Exhibit 7.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.7. What is the standard deviation of this portfolio?

A)4.87%

B)3.62%

C)4.13%

D)5.76%

E)6.02%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.7. What is the standard deviation of this portfolio?

A)4.87%

B)3.62%

C)4.13%

D)5.76%

E)6.02%

Question

Exhibit 7.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.1. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.79%

B)12.5%

C)13.75%

D)7.72%

E)12%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.1. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.79%

B)12.5%

C)13.75%

D)7.72%

E)12%

Question

Exhibit 7.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.8. What is the standard deviation of this portfolio?

A)4.51%

B)5.94%

C)6.75%

D)7.09%

E)8.62%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.8. What is the standard deviation of this portfolio?

A)4.51%

B)5.94%

C)6.75%

D)7.09%

E)8.62%

Question

Exhibit 7.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.6. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.6 %

B)10.2%

C)13.0%

D)11.9%

E)14.0%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.6. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.6 %

B)10.2%

C)13.0%

D)11.9%

E)14.0%

Question

Exhibit 7.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.8. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)6.4%

B)9.1%

C)10.2%

D)10.8%

E)11.2%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.8. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)6.4%

B)9.1%

C)10.2%

D)10.8%

E)11.2%

Question

Exhibit 7.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.9. What is the standard deviation of this portfolio?

A)5.16%

B)5.89%

C)6.11%

D)6.57%

E)7.02%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.9. What is the standard deviation of this portfolio?

A)5.16%

B)5.89%

C)6.11%

D)6.57%

E)7.02%

Question

Exhibit 7.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.2. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)18.64%

B)20.0%

C)22.5%

D)13.65%

E)11%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.2. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)18.64%

B)20.0%

C)22.5%

D)13.65%

E)11%

Question

Exhibit 7.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.3. What is the standard deviation of this portfolio?

A)3.68%

B)4.56%

C)4.99%

D)5.16%

E)6.02%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.3. What is the standard deviation of this portfolio?

A)3.68%

B)4.56%

C)4.99%

D)5.16%

E)6.02%

Question

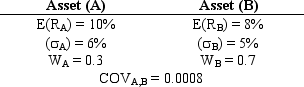

Exhibit 7.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.4. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.6%

B)8.1%

C)9.3%

D)10.2%

E)11.6%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.4. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.6%

B)8.1%

C)9.3%

D)10.2%

E)11.6%

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/97

Play

Full screen (f)

Deck 7: An Introduction to Portfolio Management

1

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Risk is defined as the uncertainty of future outcomes.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Risk is defined as the uncertainty of future outcomes.

True

2

Exhibit 7B.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 1)2 - r1.2 E( 1) E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2 E( 1) E( 2)]

-Refer to Exhibit 7B.1. Show the minimum portfolio variance for a portfolio of two risky assets when r1.2 = -1.

A)E( 1) /[E( 1) + E( 2)]

B)E( 1) /[E( 1) -E( 2)]

C)E( 2) /[E( 1) + E( 2)]

D)E( 2) /[E( 1) -E( 2)]

E)None of the above

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 1)2 - r1.2 E( 1) E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2 E( 1) E( 2)]

-Refer to Exhibit 7B.1. Show the minimum portfolio variance for a portfolio of two risky assets when r1.2 = -1.

A)E( 1) /[E( 1) + E( 2)]

B)E( 1) /[E( 1) -E( 2)]

C)E( 2) /[E( 1) + E( 2)]

D)E( 2) /[E( 1) -E( 2)]

E)None of the above

E( 2) /[E( 1) + E( 2)]

3

An investor is risk neutral if she chooses the asset with lower risk given a choice of several assets with equal returns.

False

4

In a three asset portfolio the standard deviation of the portfolio is one third of the square root of the sum of the individual standard deviations.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

5

Combining assets that are not perfectly correlated does affect both the expected return of the portfolio as well as the risk of the portfolio.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

6

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Prior to the work of Markowitz in the late 1950's and early 1960's, portfolio managers did not have a well-developed, quantitative means of measuring risk.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Prior to the work of Markowitz in the late 1950's and early 1960's, portfolio managers did not have a well-developed, quantitative means of measuring risk.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

7

Markowitz assumed that, given an expected return, investors prefer to minimize risk.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

8

For a two stock portfolio containing Stocks i and j, the correlation coefficient of returns (rij) is equal to the square root of the covariance (covij).

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

9

The expected return and standard deviation of a portfolio of risky assets is equal to the weighted average of the individual asset's expected returns and standard deviation.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

10

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Refer to Exhibit 7A.1. What weight of security 1 gives the minimum portfolio variance when r1.2 = .60, E( 1) = .10 and E( 2) = .16?

A).0244

B).3679

C).5697

D).6309

E).9756

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Refer to Exhibit 7A.1. What weight of security 1 gives the minimum portfolio variance when r1.2 = .60, E( 1) = .10 and E( 2) = .16?

A).0244

B).3679

C).5697

D).6309

E).9756

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

11

Exhibit 7B.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 1)2 - r1.2 E( 1) E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2 E( 1) E( 2)]

-Refer to Exhibit 7B.1. What is the value of W1 when r1.2 = -1 and E( 1) = .10 and E( 2) = .12?

A)45.46%

B)50.00%

C)59.45%

D)54.55%

E)74.55%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 1)2 - r1.2 E( 1) E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2 E( 1) E( 2)]

-Refer to Exhibit 7B.1. What is the value of W1 when r1.2 = -1 and E( 1) = .10 and E( 2) = .12?

A)45.46%

B)50.00%

C)59.45%

D)54.55%

E)74.55%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

12

Increasing the correlation among assets in a portfolio results in an increase in the standard deviation of the portfolio.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

13

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-A good portfolio is a collection of individually good assets.

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-A good portfolio is a collection of individually good assets.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

14

Assuming that everyone agrees on the efficient frontier (given a set of costs), there would be consensus that the optimal portfolio on the frontier would be where the ratio of return per unit of risk was greatest.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

15

The correlation coefficient and the covariance are measures of the extent to which two random variables move together.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

16

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Refer to Exhibit 7A.1. Show the minimum portfolio variance for a two stock portfolio when r1.2 = 1.

A)E( 2)/ [E( 1) - E( 2)]

B)E( 2)/[E( 1) + E( 2)]

C)E( 1) /[E( 1) -E( 2)]

D)E( 1) /[E( 1) + E( 2)]

E)None of the above

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Refer to Exhibit 7A.1. Show the minimum portfolio variance for a two stock portfolio when r1.2 = 1.

A)E( 2)/ [E( 1) - E( 2)]

B)E( 2)/[E( 1) + E( 2)]

C)E( 1) /[E( 1) -E( 2)]

D)E( 1) /[E( 1) + E( 2)]

E)None of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

17

A basic assumption of the Markowitz model is that investors base decisions solely on expected return and risk.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

18

As the number of risky assets in a portfolio increases, the total risk of the portfolio decreases.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

19

If the covariance of two stocks is positive, these stocks tend to move together over time.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

20

The combination of two assets that are completely negatively correlated provides maximum returns.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

21

If equal risk is added moving along the envelope curve containing the best possible combinations the return will

A)Decrease at an increasing rate.

B)Decrease at a decreasing rate.

C)Increase at an increasing rate.

D)Increase at a decreasing rate.

E)Remain constant.

A)Decrease at an increasing rate.

B)Decrease at a decreasing rate.

C)Increase at an increasing rate.

D)Increase at a decreasing rate.

E)Remain constant.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

22

A portfolio is considered to be efficient if:

A)No other portfolio offers higher expected returns with the same risk.

B)No other portfolio offers lower risk with the same expected return.

C)There is no portfolio with a higher return.

D)Choices a and b

E)All of the above

A)No other portfolio offers higher expected returns with the same risk.

B)No other portfolio offers lower risk with the same expected return.

C)There is no portfolio with a higher return.

D)Choices a and b

E)All of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

23

Investors choose a portfolio on the efficient frontier based on their utility functions that reflect their attitudes towards risk.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

24

The probability of an adverse outcome is a definition of

A)Statistics.

B)Variance.

C)Random.

D)Risk.

E)Semi-variance above the mean.

A)Statistics.

B)Variance.

C)Random.

D)Risk.

E)Semi-variance above the mean.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

25

The set of portfolios with the maximum rate of return for every given risk level is known as the optimal frontier.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

26

Given a portfolio of stocks, the envelope curve containing the set of best possible combinations is known as the

A)Efficient portfolio.

B)Utility curve.

C)Efficient frontier.

D)Last frontier.

E)Capital asset pricing model.

A)Efficient portfolio.

B)Utility curve.

C)Efficient frontier.

D)Last frontier.

E)Capital asset pricing model.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

27

Semivariance, when applied to portfolio theory, is concerned with

A)The square root of deviations from the mean.

B)All deviations below the mean.

C)All deviations above the mean.

D)All deviations.

E)The summation of the squared deviations from the mean.

A)The square root of deviations from the mean.

B)All deviations below the mean.

C)All deviations above the mean.

D)All deviations.

E)The summation of the squared deviations from the mean.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

28

A portfolio is efficient if no other asset or portfolios offer higher expected return with the same (or lower) risk or lower risk with the same (or higher) expected return.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

29

The purpose of calculating the covariance between two stocks is to provide a(n) ____ measure of their movement together.

A)Absolute

B)Relative

C)Indexed

D)Loglinear

E)Squared

A)Absolute

B)Relative

C)Indexed

D)Loglinear

E)Squared

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

30

The Markowitz model is based on several assumptions regarding investor behavior. Which of the following is not such any assumption?

A)Investors consider each investment alternative as being represented by a probability distribution of expected returns over some holding period.

B)Investors maximize one-period expected utility.

C)Investors estimate the risk of the portfolio on the basis of the variability of expected returns.

D)Investors base decisions solely on expected return and risk.

E)None of the above (that is, all are assumptions of the Markowitz model)

A)Investors consider each investment alternative as being represented by a probability distribution of expected returns over some holding period.

B)Investors maximize one-period expected utility.

C)Investors estimate the risk of the portfolio on the basis of the variability of expected returns.

D)Investors base decisions solely on expected return and risk.

E)None of the above (that is, all are assumptions of the Markowitz model)

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

31

Markowitz believes that any asset or portfolio of assets can be described by ____ parameter(s).

A)One

B)Two

C)Three

D)Four

E)Five

A)One

B)Two

C)Three

D)Four

E)Five

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

32

The optimal portfolio is identified at the point of tangency between the efficient frontier and the

A)highest possible utility curve.

B)lowest possible utility curve.

C)middle range utility curve.

D)steepest utility curve.

E)flattest utility curve.

A)highest possible utility curve.

B)lowest possible utility curve.

C)middle range utility curve.

D)steepest utility curve.

E)flattest utility curve.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

33

As the correlation coefficient between two assets decreases, the shape of the efficient frontier

A)approaches a horizontal straight line.

B)bends out.

C)bends in.

D)approaches a vertical straight line.

E)none of the above.

A)approaches a horizontal straight line.

B)bends out.

C)bends in.

D)approaches a vertical straight line.

E)none of the above.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following statements about the correlation coefficient is false?

A)The values range between-1 to +1.

B)A value of +1 implies that the returns for the two stocks move together in a completely linear manner.

C)A value of -1 implies that the returns move in a completely opposite direction.

D)A value of zero means that the returns are independent.

E)None of the above (that is, all statements are true)

A)The values range between-1 to +1.

B)A value of +1 implies that the returns for the two stocks move together in a completely linear manner.

C)A value of -1 implies that the returns move in a completely opposite direction.

D)A value of zero means that the returns are independent.

E)None of the above (that is, all statements are true)

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

35

In a two stock portfolio, if the correlation coefficient between two stocks were to decrease over time, everything else remaining constant, the portfolio's risk would

A)Decrease.

B)Remain constant.

C)Increase.

D)Fluctuate positively and negatively.

E)Be a negative value.

A)Decrease.

B)Remain constant.

C)Increase.

D)Fluctuate positively and negatively.

E)Be a negative value.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

36

A portfolio manager is considering adding another security to his portfolio. The correlations of the 5 alternatives available are listed below. Which security would enable the highest level of risk diversification?

A)0.0

B)0.25

C)-0.25

D)-0.75

E)1.0

A)0.0

B)0.25

C)-0.25

D)-0.75

E)1.0

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

37

An individual investor's utility curves specify the tradeoffs he or she is willing to make between

A)high risk and low risk assets.

B)high return and low return assets.

C)covariance and correlation.

D)return and risk.

E)efficient portfolios.

A)high risk and low risk assets.

B)high return and low return assets.

C)covariance and correlation.

D)return and risk.

E)efficient portfolios.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

38

You are given a two asset portfolio with a fixed correlation coefficient. If the weights of the two assets are varied the expected portfolio return would be ____ and the expected portfolio standard deviation would be ____.

A)Nonlinear, elliptical

B)Nonlinear, circular

C)Linear, elliptical

D)Linear, circular

E)Circular, elliptical

A)Nonlinear, elliptical

B)Nonlinear, circular

C)Linear, elliptical

D)Linear, circular

E)Circular, elliptical

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

39

When individuals evaluate their portfolios they should evaluate

A)All the U.S.and non-U.S.stocks.

B)All marketable securities.

C)All marketable securities and other liquid assets.

D)All assets.

E)All assets and liabilities.

A)All the U.S.and non-U.S.stocks.

B)All marketable securities.

C)All marketable securities and other liquid assets.

D)All assets.

E)All assets and liabilities.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

40

A measure that only considers deviations above the mean is semi-variance.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

41

The slope of the utility curves for a strongly risk-averse investor, relative to the slope of the utility curves for a less risk-averse investor, will

A)Be steeper.

B)Be flatter.

C)Be vertical.

D)Be horizontal.

E)None of the above.

A)Be steeper.

B)Be flatter.

C)Be vertical.

D)Be horizontal.

E)None of the above.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

42

What is the expected return of the three stock portfolio described below?

A)18.45%

B)12.82%

C)13.38%

D)15.27%

E)16.67%

A)18.45%

B)12.82%

C)13.38%

D)15.27%

E)16.67%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

43

A positive covariance between two variables indicates that

A)the two variables move in different directions.

B)the two variables move in the same direction.

C)the two variables are low risk.

D)the two variables are high risk.

E)the two variables are risk free.

A)the two variables move in different directions.

B)the two variables move in the same direction.

C)the two variables are low risk.

D)the two variables are high risk.

E)the two variables are risk free.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

44

Between 1980 and 1990, the standard deviation of the returns for the NIKKEI and the DJIA indexes were 0.19 and 0.06, respectively, and the covariance of these index returns was 0.0014. What was the correlation coefficient between the two market indicators?

A)8.1428

B)0.0233

C)0.0073

D)0.2514

E)0.1228

A)8.1428

B)0.0233

C)0.0073

D)0.2514

E)0.1228

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

45

When assessing the risk impact of adding a new security to a portfolio, it is necessary to consider the

A)New securities variance

B)Variance of every security in the portfolio

C)Weight of every security in the portfolio

D)Average covariance of the new security with every security in the portfolio

E)All of the above

A)New securities variance

B)Variance of every security in the portfolio

C)Weight of every security in the portfolio

D)Average covariance of the new security with every security in the portfolio

E)All of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

46

All of the following are common risk measurements except

A)Standard deviation

B)Variance

C)Semivariance

D)Covariance

E)Range of returns

A)Standard deviation

B)Variance

C)Semivariance

D)Covariance

E)Range of returns

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

47

Between 1980 and 2000, the standard deviation of the returns for the NIKKEI and the DJIA indexes were 0.08 and 0.10, respectively, and the covariance of these index returns was 0.0007. What was the correlation coefficient between the two market indicators?

A).0906

B).0985

C).0796

D).0875

E).0654

A).0906

B).0985

C).0796

D).0875

E).0654

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

48

All of the following are assumptions of the Markowitz model except

A)Risk is measured based on the variability of returns.

B)Investors maximize one-period expected utility.

C)Investors' utility curves demonstrate properties of diminishing marginal utility of wealth.

D)Investors base decisions solely on expected return and time.

E)All of the above

A)Risk is measured based on the variability of returns.

B)Investors maximize one-period expected utility.

C)Investors' utility curves demonstrate properties of diminishing marginal utility of wealth.

D)Investors base decisions solely on expected return and time.

E)All of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

49

Between 1986 and 1996, the standard deviation of the returns for the NYSE and the DJIA indexes were 0.10 and 0.09, respectively, and the covariance of these index returns was 0.0009. What was the correlation coefficient between the two market indicators?

A).1000

B).1100

C).1258

D).1322

E).1164

A).1000

B).1100

C).1258

D).1322

E).1164

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

50

The most important criteria when adding new investments to a portfolio is the

A)Expected return of the new investment.

B)Standard deviation of the new investment.

C)Correlation of the new investment with the portfolio.

D)Both a and b

E)All of the above are equally important

A)Expected return of the new investment.

B)Standard deviation of the new investment.

C)Correlation of the new investment with the portfolio.

D)Both a and b

E)All of the above are equally important

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

51

What is the expected return of the three stock portfolio described below?

A)21.33%

B)12.50%

C)32.00%

D)15.75%

E)16.80%

A)21.33%

B)12.50%

C)32.00%

D)15.75%

E)16.80%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

52

What is the expected return of the three stock portfolio described below?

A)14.89%

B)16.22%

C)12.66%

D)13.85%

E)16.99%

A)14.89%

B)16.22%

C)12.66%

D)13.85%

E)16.99%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

53

The slope of the efficient frontier is calculated as follows

A).E(Rportfolio)/E( portfolio)

B).E( portfolio)/ E(Rportfolio)

C). E(Rportfolio)/ E( portfolio)

D). E( portfolio)/ E(Rportfolio)

E)None of the above

A).E(Rportfolio)/E( portfolio)

B).E( portfolio)/ E(Rportfolio)

C). E(Rportfolio)/ E( portfolio)

D). E( portfolio)/ E(Rportfolio)

E)None of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

54

A positive relationship between expected return and expected risk is consistent with

A)investors being risk seekers.

B)investors being risk avoiders.

C)investors being risk averse.

D)all of the above.

E)none of the above.

A)investors being risk seekers.

B)investors being risk avoiders.

C)investors being risk averse.

D)all of the above.

E)none of the above.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

55

What is the expected return of the three stock portfolio described below?

A)18.27%

B)14.33%

C)16.33%

D)12.72%

E)16.45%

A)18.27%

B)14.33%

C)16.33%

D)12.72%

E)16.45%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

56

Between 1994 and 2004, the standard deviation of the returns for the S&P 500 and the NYSE indexes were 0.27 and 0.14, respectively, and the covariance of these index returns was 0.03. What was the correlation coefficient between the two market indicators?

A)1.26

B)0.7937

C)0.2142

D)0.1111

E)0.44

A)1.26

B)0.7937

C)0.2142

D)0.1111

E)0.44

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

57

Between 1975 and 1985, the standard deviation of the returns for the NYSE and the S&P 500 indexes were 0.06 and 0.07, respectively, and the covariance of these index returns was 0.0008. What was the correlation coefficient between the two market indicators?

A).1525

B).1388

C).1458

D).1622

E).1064

A).1525

B).1388

C).1458

D).1622

E).1064

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

58

Between 1990 and 2000, the standard deviation of the returns for the NIKKEI and the DJIA indexes were 0.18 and 0.16, respectively, and the covariance of these index returns was 0.003. What was the correlation coefficient between the two market indicators?

A)9.6

B)0.0187

C)0.1042

D)0.0166

E)0.343

A)9.6

B)0.0187

C)0.1042

D)0.0166

E)0.343

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

59

What is the expected return of the three stock portfolio described below?

A)12.04%

B)12.83%

C)13.07%

D)15.89%

E)17.91%

A)12.04%

B)12.83%

C)13.07%

D)15.89%

E)17.91%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

60

A portfolio of two securities that are perfectly positively correlated has

A)A standard deviation that is the weighted average of the individual securities standard deviations.

B)An expected return that is the weighted average of the individual securities expected returns.

C)No diversification benefit over holding either of the securities independently.

D)Both b and c

E)All of the above

A)A standard deviation that is the weighted average of the individual securities standard deviations.

B)An expected return that is the weighted average of the individual securities expected returns.

C)No diversification benefit over holding either of the securities independently.

D)Both b and c

E)All of the above

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

61

Exhibit 7.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.7. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)5.8%

B)6.1%

C)6.9%

D)7.8%

E)8.9%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.7. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)5.8%

B)6.1%

C)6.9%

D)7.8%

E)8.9%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

62

Exhibit 7.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.2. What is the standard deviation of this portfolio?

A)5.45%

B)18.64%

C)20.0%

D)22.5%

E)13.65%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.2. What is the standard deviation of this portfolio?

A)5.45%

B)18.64%

C)20.0%

D)22.5%

E)13.65%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

63

Exhibit 7.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.1. What is the standard deviation of this portfolio?

A)8.79%

B)13.75%

C)12.5%

D)7.72%

E)5.64%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.1. What is the standard deviation of this portfolio?

A)8.79%

B)13.75%

C)12.5%

D)7.72%

E)5.64%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

64

Exhibit 7.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.5. What is the standard deviation of this portfolio?

A)3.89%

B)4.61%

C)5.02%

D)6.83%

E)6.09%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.5. What is the standard deviation of this portfolio?

A)3.89%

B)4.61%

C)5.02%

D)6.83%

E)6.09%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

65

Exhibit 7.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.6. What is the standard deviation of this portfolio?

A)6.08%

B)5.89%

C)7.06%

D)6.54%

E)7.26%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.6. What is the standard deviation of this portfolio?

A)6.08%

B)5.89%

C)7.06%

D)6.54%

E)7.26%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

66

Exhibit 7.10

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.10. What is the standard deviation of this portfolio?

A)3.02%

B)4.88%

C)5.24%

D)5.98%

E)6.52%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.10. What is the standard deviation of this portfolio?

A)3.02%

B)4.88%

C)5.24%

D)5.98%

E)6.52%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

67

Exhibit 7.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.3. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.95%

B)9.30%

C)9.95%

D)10.20%

E)10.70%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.3. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.95%

B)9.30%

C)9.95%

D)10.20%

E)10.70%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

68

Exhibit 7.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.4. What is the standard deviation of this portfolio?

A)5.02%

B)3.88%

C)6.21%

D)4.04%

E)4.34%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.4. What is the standard deviation of this portfolio?

A)5.02%

B)3.88%

C)6.21%

D)4.04%

E)4.34%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

69

Exhibit 7.10

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)11%

B)12%

C)13%

D)14%

E)15%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)11%

B)12%

C)13%

D)14%

E)15%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

70

Exhibit 7.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.9. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.10%

B)11.60%

C)13.88%

D)14.50%

E)15.37%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.9. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.10%

B)11.60%

C)13.88%

D)14.50%

E)15.37%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

71

Exhibit 7.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.5. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.0%

B)12.2%

C)7.4%

D)9.1%

E)11.6%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.5. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.0%

B)12.2%

C)7.4%

D)9.1%

E)11.6%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

72

Exhibit 7.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.7. What is the standard deviation of this portfolio?

A)4.87%

B)3.62%

C)4.13%

D)5.76%

E)6.02%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.7. What is the standard deviation of this portfolio?

A)4.87%

B)3.62%

C)4.13%

D)5.76%

E)6.02%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

73

Exhibit 7.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.1. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.79%

B)12.5%

C)13.75%

D)7.72%

E)12%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.1. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.79%

B)12.5%

C)13.75%

D)7.72%

E)12%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

74

Exhibit 7.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.8. What is the standard deviation of this portfolio?

A)4.51%

B)5.94%

C)6.75%

D)7.09%

E)8.62%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.8. What is the standard deviation of this portfolio?

A)4.51%

B)5.94%

C)6.75%

D)7.09%

E)8.62%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

75

Exhibit 7.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.6. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.6 %

B)10.2%

C)13.0%

D)11.9%

E)14.0%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.6. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)10.6 %

B)10.2%

C)13.0%

D)11.9%

E)14.0%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

76

Exhibit 7.8

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.8. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)6.4%

B)9.1%

C)10.2%

D)10.8%

E)11.2%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.8. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)6.4%

B)9.1%

C)10.2%

D)10.8%

E)11.2%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

77

Exhibit 7.9

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.9. What is the standard deviation of this portfolio?

A)5.16%

B)5.89%

C)6.11%

D)6.57%

E)7.02%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.9. What is the standard deviation of this portfolio?

A)5.16%

B)5.89%

C)6.11%

D)6.57%

E)7.02%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

78

Exhibit 7.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.2. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)18.64%

B)20.0%

C)22.5%

D)13.65%

E)11%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.2. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)18.64%

B)20.0%

C)22.5%

D)13.65%

E)11%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

79

Exhibit 7.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.3. What is the standard deviation of this portfolio?

A)3.68%

B)4.56%

C)4.99%

D)5.16%

E)6.02%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Refer to Exhibit 7.3. What is the standard deviation of this portfolio?

A)3.68%

B)4.56%

C)4.99%

D)5.16%

E)6.02%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

80

Exhibit 7.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.4. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.6%

B)8.1%

C)9.3%

D)10.2%

E)11.6%

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.4. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

A)8.6%

B)8.1%

C)9.3%

D)10.2%

E)11.6%

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 97 flashcards in this deck.