Exam 7: An Introduction to Portfolio Management

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

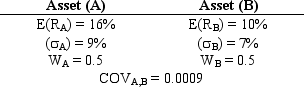

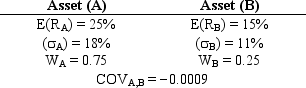

Exhibit 7.6

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.6. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.6. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

Free

(Multiple Choice)

4.9/5  (36)

(36)

Correct Answer: Verified

Verified

C

The optimal portfolio is identified at the point of tangency between the efficient frontier and the

Free

(Multiple Choice)

4.9/5 (40)

Correct Answer:Verified

A

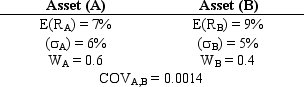

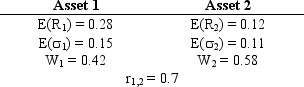

Exhibit 7.14

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A and B have a correlation coefficient of -0.8. The stocks' expected returns and standard deviations are in the table below. A portfolio consisting of 40% of stock A and 60% of stock B is constructed.

-What is the standard deviation of an equally weighted portfolio of two stocks with a covariance of 0.009, if the standard deviation of the first stock is 15% and the standard deviation of the second stock is 20%?

-What is the standard deviation of an equally weighted portfolio of two stocks with a covariance of 0.009, if the standard deviation of the first stock is 15% and the standard deviation of the second stock is 20%?

Free

(Multiple Choice)

4.8/5 (34)

Correct Answer:Verified

D

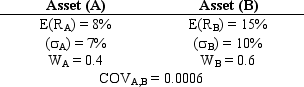

Exhibit 7.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.7. What is the standard deviation of this portfolio?

-Refer to Exhibit 7.7. What is the standard deviation of this portfolio?

(Multiple Choice)

4.9/5 (30)

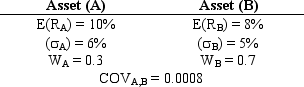

Exhibit 7.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.5. What is the standard deviation of this portfolio?

-Refer to Exhibit 7.5. What is the standard deviation of this portfolio?

(Multiple Choice)

4.8/5 (34)

A portfolio is efficient if no other asset or portfolios offer higher expected return with the same (or lower) risk or lower risk with the same (or higher) expected return.

(True/False)

4.8/5 (32)

Exhibit 7.4

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.4. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.4. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.8/5 (34)

Markowitz assumed that, given an expected return, investors prefer to minimize risk.

(True/False)

4.7/5 (40)

When individuals evaluate their portfolios they should evaluate

(Multiple Choice)

4.8/5 (37)

A measure that only considers deviations above the mean is semi-variance.

(True/False)

4.8/5 (32)

In a three asset portfolio the standard deviation of the portfolio is one third of the square root of the sum of the individual standard deviations.

(True/False)

4.9/5 (41)

Assuming that everyone agrees on the efficient frontier (given a set of costs), there would be consensus that the optimal portfolio on the frontier would be where the ratio of return per unit of risk was greatest.

(True/False)

4.8/5 (37)

Exhibit 7.14

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A and B have a correlation coefficient of -0.8. The stocks' expected returns and standard deviations are in the table below. A portfolio consisting of 40% of stock A and 60% of stock B is constructed.

-Refer to Exhibit 7.14. What is the standard deviation of the stock A and B portfolio?

(Multiple Choice)

4.9/5 (40)

The Markowitz model is based on several assumptions regarding investor behavior. Which of the following is not such any assumption?

(Multiple Choice)

4.8/5 (44)

Exhibit 7.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.2. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.2. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.9/5 (45)

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-Risk is defined as the uncertainty of future outcomes.

(True/False)

4.9/5 (41)

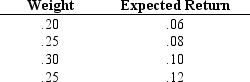

Exhibit 7.12

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Given the following weights and expected security returns, calculate the expected return for the portfolio.

-Given the following weights and expected security returns, calculate the expected return for the portfolio.

(Multiple Choice)

4.8/5 (35)

Exhibit 7.11

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.11. Calculate the expected return of the two stock portfolio.

-Refer to Exhibit 7.11. Calculate the expected return of the two stock portfolio.

(Multiple Choice)

4.8/5 (40)

An individual investor's utility curves specify the tradeoffs he or she is willing to make between

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)