Deck 4: Complex Financial Instruments

Full screen (f)

Question

Question

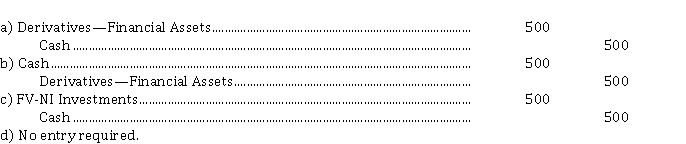

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value. The entry to record the purchase of the call option is

Question

Question

Use the following information for questions 18-19.

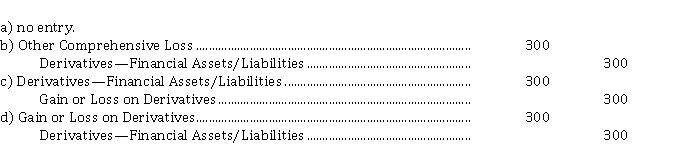

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

The entry to record the change in value of the contract on August 31, 2020 is

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

The entry to record the change in value of the contract on August 31, 2020 is

Question

Use the following information for questions 18-19.

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

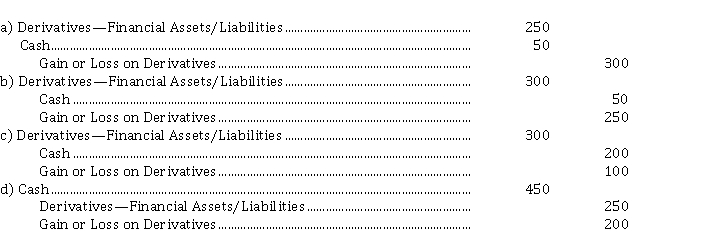

On September 5, 2020, the KRB is trading at $ 0.15 CAD. The entry to record the settlement of the contract is

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

On September 5, 2020, the KRB is trading at $ 0.15 CAD. The entry to record the settlement of the contract is

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

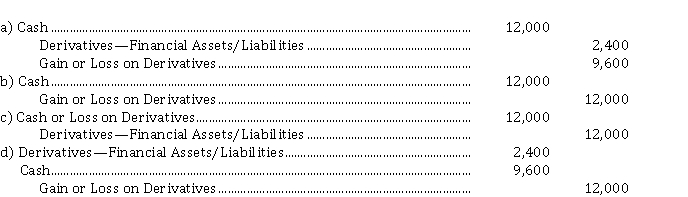

On July 5, 2020, Alpha Corp. purchased a call option for $ 2,400, giving it the right to buy 2,000 shares of Omega Corp. for $ 20 per share. On August 18, 2020, when the option value is $ 12,000, Omega settles the option for cash. The entry on Alpha's books to record the settlement is

Question

Question

Question

Question

Question

Question

At June 30, 2020, Gamma's quarter end, the adjusting entry would be

A) No entry required.

A) No entry required.

Question

Question

At December 1, 2020, Gamma's entry would be

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

On April 7, 2020, Soweto Corp. sold a $ 1,000,000 (par value), 20 year, 8% bond issue for $ 1,060,000. Each $ 1,000 bond has two detachable warrants. Each warrant permits the purchase one of Soweto's no par value common shares for $ 30. At the time of the sale, Soweto's securities had the following market values:

Question

Question

Question

On January 1, 2020, Orion Corp. granted an employee an option to purchase 5,000 of Orion's no par value common shares at $ 50 per share. The Black-Scholes option pricing model determined total compensation expense to be $ 220,000. The option became exercisable on December 31, 2021, after the employee completed two years of service. The market prices of Orion's shares were as follows:  For calendar 2021, Orion should recognize compensation expense of

For calendar 2021, Orion should recognize compensation expense of

A) $ 0.

B) $ 50,000.

C) $ 110,000.

D) $ 250,000.

For calendar 2021, Orion should recognize compensation expense ofA) $ 0.

B) $ 50,000.

C) $ 110,000.

D) $ 250,000.

Question

Question

On July 1, 2020, Juba Inc. issued 10,000, $ 7 non-cumulative, no par value preferred shares for $ 1,050,000. Attached to each share was one detachable warrant, giving the holder the right to purchase one of Juba's no par value common shares for $ 30. At this time, the shares without the warrants would normally sell for $ 1,025,000, while the market price of the warrants was $ 2.50 each. On October 31, 2020, when the market price of the common shares was $ 33.50 and the market value of the warrants was $ 3.00, 4,000 warrants were exercised. Juba adheres to IFRS. As a result of the exercise of the warrants and the issuance of the related common shares, what journal entry would Juba make?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows: Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

What amount of compensation expense should Luanda recognize for calendar 2019?

A) $ 150,000

B) $ 187,500

C) $ 225,000

D) $ 900,000

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.What amount of compensation expense should Luanda recognize for calendar 2019?

A) $ 150,000

B) $ 187,500

C) $ 225,000

D) $ 900,000

Question

Question

Question

Question

Question

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows: Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

What amount of compensation expense should Luanda recognize for calendar 2020?

A) $ 0

B) $ 25,000

C) $ 125,000

D) $ 250,000

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.What amount of compensation expense should Luanda recognize for calendar 2020?

A) $ 0

B) $ 25,000

C) $ 125,000

D) $ 250,000

Question

Question

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows: Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

On December 31, 2021, 8,000 SARs are exercised by executives. What amount of compensation expense should Luanda recognize for calendar 2021?

A) $ 65,000

B) $ 162,500

C) $ 237,500

D) $ 487,500

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.On December 31, 2021, 8,000 SARs are exercised by executives. What amount of compensation expense should Luanda recognize for calendar 2021?

A) $ 65,000

B) $ 162,500

C) $ 237,500

D) $ 487,500

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/99

Play

Full screen (f)

Deck 4: Complex Financial Instruments

1

Use the following information for questions 20-23.

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value.

The intrinsic value of the option at April 1, 2020 is

A) $ 0.

B) $ 500.

C) $ 1,000.

D) $ 4,800.

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value.

The intrinsic value of the option at April 1, 2020 is

A) $ 0.

B) $ 500.

C) $ 1,000.

D) $ 4,800.

A

2

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value. The entry to record the purchase of the call option is

A

3

If a company writes an option, it

A) pays a fee and gains a right.

B) charges a fee and gives the holder a right.

C) charges a fee for handling option transactions.

D) endorses an option over to another party.

A) pays a fee and gains a right.

B) charges a fee and gives the holder a right.

C) charges a fee for handling option transactions.

D) endorses an option over to another party.

B

4

Use the following information for questions 18-19.

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

The entry to record the change in value of the contract on August 31, 2020 is

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

The entry to record the change in value of the contract on August 31, 2020 is

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

5

Use the following information for questions 18-19.

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

On September 5, 2020, the KRB is trading at $ 0.15 CAD. The entry to record the settlement of the contract is

On August 25, 2020, Beta Inc. entered into a forward contract to buy 25,000 Krubles (KRB) for $ 3,800 Canadian (CAD) on September 5, 2020. On August 31, 2020, 25,000 KRB can be purchased for $ 3,500 CAD. On September 5, Beta settles the contract but does NOT take delivery of the KRB.

On September 5, 2020, the KRB is trading at $ 0.15 CAD. The entry to record the settlement of the contract is

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

6

Gains on derivatives should

A) be booked through other comprehensive income.

B) be booked through net income.

C) be recorded as deferred revenue.

D) not be recorded.

A) be booked through other comprehensive income.

B) be booked through net income.

C) be recorded as deferred revenue.

D) not be recorded.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

7

Credit risk is the risk that

A) an instrument's price or value will change.

B) the company itself will not be able to fulfill its obligation.

C) one of the parties to the contract will fail to fulfill its obligation and cause the other party loss.

D) cash flow will change over time.

A) an instrument's price or value will change.

B) the company itself will not be able to fulfill its obligation.

C) one of the parties to the contract will fail to fulfill its obligation and cause the other party loss.

D) cash flow will change over time.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

8

Derivative instruments

A) require significant investments.

B) transfer financial risks.

C) transfer primary instruments.

D) are settled at the date of issuance.

A) require significant investments.

B) transfer financial risks.

C) transfer primary instruments.

D) are settled at the date of issuance.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

9

Derivatives exist to help companies

A) hide financial irregularities.

B) reduce interest expense.

C) manage cash flows.

D) manage risks.

A) hide financial irregularities.

B) reduce interest expense.

C) manage cash flows.

D) manage risks.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

10

The intrinsic value of an option is the

A) difference between the price of the underlying security and the strike price.

B) value due to expectations that the price of the underlying security will rise above the strike price.

C) minimum value of the option.

D) option premium value.

A) difference between the price of the underlying security and the strike price.

B) value due to expectations that the price of the underlying security will rise above the strike price.

C) minimum value of the option.

D) option premium value.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

11

A futures contract

A) is not exchange traded, therefore does not have a ready market value.

B) exposes the contracting party to credit risk.

C) does not require a margin account to be established.

D) is standardized as to amounts and dates.

A) is not exchange traded, therefore does not have a ready market value.

B) exposes the contracting party to credit risk.

C) does not require a margin account to be established.

D) is standardized as to amounts and dates.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

12

A call option is a right to

A) force another party to buy the underlying security.

B) repurchase a previously sold underlying security.

C) sell the underlying security.

D) buy the underlying security.

A) force another party to buy the underlying security.

B) repurchase a previously sold underlying security.

C) sell the underlying security.

D) buy the underlying security.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

13

Derivatives should be valued at

A) historical cost.

B) fair value or historical cost.

C) fair value.

D) discounted cost.

A) historical cost.

B) fair value or historical cost.

C) fair value.

D) discounted cost.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

14

An arbitrageur depends on

A) information asymmetry between markets.

B) hedging opportunities between markets.

C) differing credit risks.

D) differing liquidity risks.

A) information asymmetry between markets.

B) hedging opportunities between markets.

C) differing credit risks.

D) differing liquidity risks.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

15

A forward contract

A) is generally exchange traded, therefore has a ready market value.

B) creates a right but not an obligation.

C) commits the contracting parties upfront to do something in the future.

D) has no locked in time period.

A) is generally exchange traded, therefore has a ready market value.

B) creates a right but not an obligation.

C) commits the contracting parties upfront to do something in the future.

D) has no locked in time period.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

16

A put option is a right to

A) force another party to buy the underlying security.

B) repurchase a previously sold underlying security.

C) sell the underlying security.

D) buy the underlying security.

A) force another party to buy the underlying security.

B) repurchase a previously sold underlying security.

C) sell the underlying security.

D) buy the underlying security.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

17

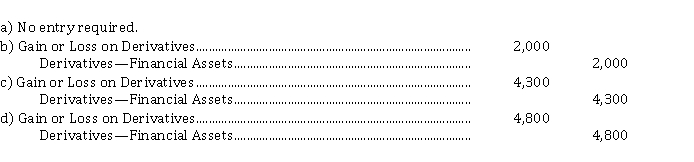

On July 5, 2020, Alpha Corp. purchased a call option for $ 2,400, giving it the right to buy 2,000 shares of Omega Corp. for $ 20 per share. On August 18, 2020, when the option value is $ 12,000, Omega settles the option for cash. The entry on Alpha's books to record the settlement is

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

18

The time value of an option is the

A) difference between the price of the underlying security and the strike price.

B) value due to expectations that the price of the underlying security will rise above the strike price.

C) minimum value of the option.

D) option premium value.

A) difference between the price of the underlying security and the strike price.

B) value due to expectations that the price of the underlying security will rise above the strike price.

C) minimum value of the option.

D) option premium value.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

19

A speculator's objective is to

A) reduce pre-existing risks.

B) take delivery of the underlying.

C) take advantage of information asymmetry.

D) maximize potential returns by being exposed to greater risks.

A) reduce pre-existing risks.

B) take delivery of the underlying.

C) take advantage of information asymmetry.

D) maximize potential returns by being exposed to greater risks.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

20

The three types of market risk are

A) currency, interest rate, and liquidity risks.

B) interest rate, other price, and credit risks.

C) currency, interest rate, and other price risks.

D) liquidity, currency, and other price risks.

A) currency, interest rate, and liquidity risks.

B) interest rate, other price, and credit risks.

C) currency, interest rate, and other price risks.

D) liquidity, currency, and other price risks.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

21

Under IFRS, mandatorily redeemable preferred shares (term preferred shares) are treated as

A) a liability.

B) equity.

C) a contra-asset.

D) either a liability or a contra-asset.

A) a liability.

B) equity.

C) a contra-asset.

D) either a liability or a contra-asset.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

22

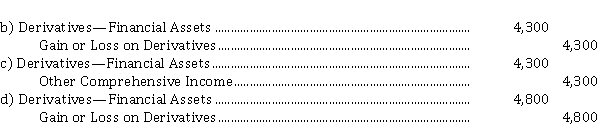

On October 5, 2020, Kappa Cloth Ltd. enters into a forward contract to purchase 10,000 metres of cotton fabric at $ 1 per metre, good until February 1, 2021. At December 31, 2020, the forward price for February 2021 delivery of cotton fabric has increased to $ 1.06 per metre. The adjusting entry at December 31, 2020 would be

A) No entry required.

B) Derivatives-Financial Assets/Liabilities 600

Unrealized Gain or Loss (OCI) 600

C) Derivatives-Financial Assets/Liabilities 600

Gain or Loss on Derivatives 600

D) Gain or Loss on Derivatives 600

Derivatives-Financial Assets/Liabilities 600

A) No entry required.

B) Derivatives-Financial Assets/Liabilities 600

Unrealized Gain or Loss (OCI) 600

C) Derivatives-Financial Assets/Liabilities 600

Gain or Loss on Derivatives 600

D) Gain or Loss on Derivatives 600

Derivatives-Financial Assets/Liabilities 600

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

23

At June 30, 2020, Gamma's quarter end, the adjusting entry would be

A) No entry required.

A) No entry required.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

24

Convertible bonds

A) have priority over all other types of bonds.

B) are usually secured by a first or second mortgage.

C) pay interest only in the event earnings are sufficient to cover the interest.

D) may usually be exchanged for common shares.

A) have priority over all other types of bonds.

B) are usually secured by a first or second mortgage.

C) pay interest only in the event earnings are sufficient to cover the interest.

D) may usually be exchanged for common shares.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

25

At December 1, 2020, Gamma's entry would be

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

26

Wang Inc. has $ 3,000,000 (par value), 8% convertible bonds outstanding. Each $ 1,000 bond is convertible into thirty no par value common shares. The bonds pay interest on January 31 and July 31. On July 31, 2020, the holders of $ 900,000 worth of bonds exercised the conversion privilege. On that date the market price of the bonds was 105, the market price of the common shares was $ 36, the carrying value of the common shares was $ 18 and the Contributed Surplus-Conversion Rights account balance was $ 450,000. The total unamortized bond premium at the date of conversion was $ 210,000. Using the book value method, Wang should record, as a result of this conversion,

A) no gain or loss.

B) a loss of $ 9,000.

C) other comprehensive income of $ 9,000.

D) a gain of $ 18,000.

A) no gain or loss.

B) a loss of $ 9,000.

C) other comprehensive income of $ 9,000.

D) a gain of $ 18,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

27

Use the following information for questions 20-23.

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value.

The time value of the option at April 1, 2020 is

A) $ 0.

B) $ 500.

C) $ 4,800.

D) $ 30,000.

On April 1, 2020, Gamma Corp. purchases a call option for $ 500, which gives Gamma the right to buy 1,000 shares of Delta Inc. for $ 30 each until December 1, 2020. Delta Inc. shares are currently trading for $ 30. At June 30, 2020, the options are trading at $ 4,800 and the shares at $ 32 each. At December 1, 2020, the options expire with no value.

The time value of the option at April 1, 2020 is

A) $ 0.

B) $ 500.

C) $ 4,800.

D) $ 30,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

28

ASPE requires that high/low (redeemable) preferred shares be presented as

A) long-term debt.

B) equity.

C) either equity or long-term debt.

D) a contra-asset.

A) long-term debt.

B) equity.

C) either equity or long-term debt.

D) a contra-asset.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following would be classified as a hybrid/compound financial instrument resulting in two elements being reported on the SFP?

A) perpetual debt

B) mandatorily redeemable preferred shares

C) debt with detachable warrants

D) puttable shares

A) perpetual debt

B) mandatorily redeemable preferred shares

C) debt with detachable warrants

D) puttable shares

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

30

Use the following information for questions 36-37.

On January 2, 2020, Perseus Corp. issued 10-year convertible bonds at 105. During 2021, all the bonds were converted into common shares having a total value equal to the total face amount of the bonds. At conversion, the market price of Perseus's common shares was 50% above its average carrying value. Perseus adheres to IFRS.

At issuance, the cash proceeds from the issuance of these bonds should be reported as

A) contributed surplus for the entire proceeds.

B) contributed surplus for the portion of the proceeds attributable to the conversion feature and as a liability for the balance.

C) a liability for the present value of the bonds and contributed surplus for the balance.

D) a liability for the entire proceeds.

On January 2, 2020, Perseus Corp. issued 10-year convertible bonds at 105. During 2021, all the bonds were converted into common shares having a total value equal to the total face amount of the bonds. At conversion, the market price of Perseus's common shares was 50% above its average carrying value. Perseus adheres to IFRS.

At issuance, the cash proceeds from the issuance of these bonds should be reported as

A) contributed surplus for the entire proceeds.

B) contributed surplus for the portion of the proceeds attributable to the conversion feature and as a liability for the balance.

C) a liability for the present value of the bonds and contributed surplus for the balance.

D) a liability for the entire proceeds.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

31

With regard to the measurement of hybrid/compound instruments,

A) IFRS requires the use of the relative fair value method.

B) IFRS requires the use of the residual method.

C) ASPE does not allow the equity component to be valued at zero.

D) After the initial measurement, the debt portion is always measured at fair value.

A) IFRS requires the use of the relative fair value method.

B) IFRS requires the use of the residual method.

C) ASPE does not allow the equity component to be valued at zero.

D) After the initial measurement, the debt portion is always measured at fair value.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

32

An advantage of issuing debt instead of equity is that

A) interest must be paid, regardless of earnings.

B) the interest is tax deductible.

C) it increases solvency or liquidity risks.

D) no leverage is possible.

A) interest must be paid, regardless of earnings.

B) the interest is tax deductible.

C) it increases solvency or liquidity risks.

D) no leverage is possible.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

33

When convertible debt is converted to common shares, IFRS requires that this is recorded by the

A) book value method.

B) relative fair value method.

C) market value method.

D) residual method.

A) book value method.

B) relative fair value method.

C) market value method.

D) residual method.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

34

Antigone Corp. issued bonds with detachable common stock warrants. Only the bonds had a known market value. Using the residual method, the value attributable to the warrants is reported as

A) Stock Warrants Distributable.

B) Other Comprehensive Income.

C) Common Shares Subscribed.

D) Contributed Surplus-Stock Warrants.

A) Stock Warrants Distributable.

B) Other Comprehensive Income.

C) Common Shares Subscribed.

D) Contributed Surplus-Stock Warrants.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following is NOT a characteristic of a non-compensatory employee stock option plan (ESOP)?

A) The plan is generally available to all employees.

B) There is only a small discount from the market price.

C) The plan requires the employee to pay an upfront premium.

D) The plan is accounted for as compensation expense.

A) The plan is generally available to all employees.

B) There is only a small discount from the market price.

C) The plan requires the employee to pay an upfront premium.

D) The plan is accounted for as compensation expense.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

36

Use the following information for questions 36-37.

On January 2, 2020, Perseus Corp. issued 10-year convertible bonds at 105. During 2021, all the bonds were converted into common shares having a total value equal to the total face amount of the bonds. At conversion, the market price of Perseus's common shares was 50% above its average carrying value. Perseus adheres to IFRS.

On conversion, Perseus would credit the Common Shares account with

A) the par value of the bonds plus the balance in the Contributed Surplus account.

B) the carrying value of the bonds plus the balance in the Contributed Surplus account.

C) the carrying value of the bonds minus the balance in the Contributed Surplus account.

D) the market value of the bonds plus the balance in the Contributed Surplus account.

On January 2, 2020, Perseus Corp. issued 10-year convertible bonds at 105. During 2021, all the bonds were converted into common shares having a total value equal to the total face amount of the bonds. At conversion, the market price of Perseus's common shares was 50% above its average carrying value. Perseus adheres to IFRS.

On conversion, Perseus would credit the Common Shares account with

A) the par value of the bonds plus the balance in the Contributed Surplus account.

B) the carrying value of the bonds plus the balance in the Contributed Surplus account.

C) the carrying value of the bonds minus the balance in the Contributed Surplus account.

D) the market value of the bonds plus the balance in the Contributed Surplus account.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

37

For convertible securities, the portion relating to the option should be classified as a(n)

A) liability.

B) asset.

C) reduction of contributed surplus.

D) addition to contributed surplus.

A) liability.

B) asset.

C) reduction of contributed surplus.

D) addition to contributed surplus.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

38

Under IFRS, a convertible debt security is recorded as a debt instrument

A) with the equity feature ignored.

B) with the equity feature described in a note.

C) and an equity component.

D) with the conversion component credited to the Common Shares account.

A) with the equity feature ignored.

B) with the equity feature described in a note.

C) and an equity component.

D) with the conversion component credited to the Common Shares account.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

39

A common reason for issuing convertible bonds is

A) to obtain debt financing at cheaper rates.

B) to avoid paying dividends on common shares.

C) to give the purchaser the option of buying preferred shares.

D) to reduce the debt-to-total assets ratio.

A) to obtain debt financing at cheaper rates.

B) to avoid paying dividends on common shares.

C) to give the purchaser the option of buying preferred shares.

D) to reduce the debt-to-total assets ratio.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

40

Dividends on term preferred shares, where the shares have been recorded as a liability, should be debited to

A) interest expense.

B) retained earnings.

C) contributed surplus.

D) other comprehensive income.

A) interest expense.

B) retained earnings.

C) contributed surplus.

D) other comprehensive income.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

41

Johannesburg Corp. has two issues of securities outstanding: no par value common shares and 8% convertible bonds with a par value of $ 8,000,000. Bond interest payment dates are June 30 and December 31. The conversion clause in the bond indenture entitles the bondholders to receive 40 common shares in exchange for each $ 1,000 bond. The value of the equity portion of the bond issue is $ 60,000. On June 30, 2020, the holders of $ 1,200,000 par value bonds exercise the conversion privilege. The market price of the bonds on that date is $ 1,100 per bond and the market price of the common shares is $ 35. The total unamortized bond discount at the date of conversion is $ 500,000. In applying the book value method, what amount should Johannesburg credit to Common Shares as a result of this conversion?

A) $ 1,284,000

B) $ 1,134,000

C) $ 1,125,000

D) $ 1,116,000

A) $ 1,284,000

B) $ 1,134,000

C) $ 1,125,000

D) $ 1,116,000

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

42

The date on which to measure the compensation element in a compensatory stock option plan (CSOP) is normally the date on which the employee

A) is granted the option.

B) has fulfilled all the conditions required to exercise the option.

C) may first exercise the option.

D) actually exercises the option.

A) is granted the option.

B) has fulfilled all the conditions required to exercise the option.

C) may first exercise the option.

D) actually exercises the option.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

43

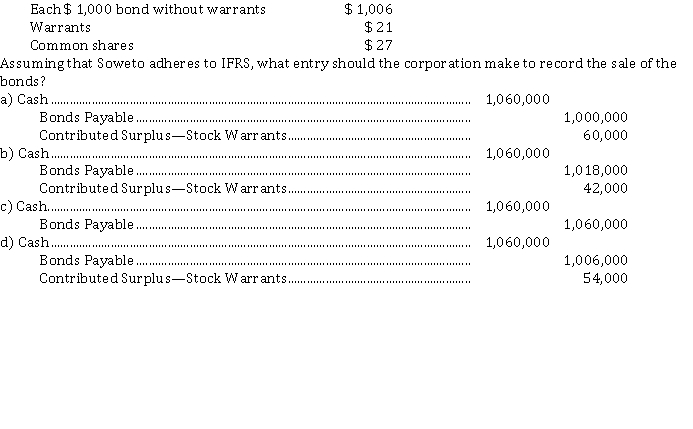

On April 7, 2020, Soweto Corp. sold a $ 1,000,000 (par value), 20 year, 8% bond issue for $ 1,060,000. Each $ 1,000 bond has two detachable warrants. Each warrant permits the purchase one of Soweto's no par value common shares for $ 30. At the time of the sale, Soweto's securities had the following market values:

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

44

During 2020, Khartoum Corp. issued four hundred $ 1,000 bonds at 104. One detachable warrant, entitling the holder to purchase 15 of Khartoum' common shares, was attached to each bond. At the date of issuance, the market value of the bonds, without the warrants, was 96. The market value of each warrant was $ 40. Using the relative fair value method, what amount should Khartoum credit to Bonds Payable from the proceeds?

A) $ 416,000

B) $ 400,000

C) $ 399,360

D) $ 384,000

A) $ 416,000

B) $ 400,000

C) $ 399,360

D) $ 384,000

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

45

Use the following information for questions 47-49.

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

What is the debit to Interest Expense on Oct 1, 2020?

A) $ 129,000

B) $ 135,000

C) $ 141,000

D) $ 143,923

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

What is the debit to Interest Expense on Oct 1, 2020?

A) $ 129,000

B) $ 135,000

C) $ 141,000

D) $ 143,923

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

46

On January 1, 2020, Orion Corp. granted an employee an option to purchase 5,000 of Orion's no par value common shares at $ 50 per share. The Black-Scholes option pricing model determined total compensation expense to be $ 220,000. The option became exercisable on December 31, 2021, after the employee completed two years of service. The market prices of Orion's shares were as follows: For calendar 2021, Orion should recognize compensation expense of

A) $ 0.

B) $ 50,000.

C) $ 110,000.

D) $ 250,000.

For calendar 2021, Orion should recognize compensation expense ofA) $ 0.

B) $ 50,000.

C) $ 110,000.

D) $ 250,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

47

Compensation expense resulting from a compensatory stock option plan (CSOP) is generally recognized

A) in the period of exercise.

B) at the grant date.

C) in the periods in which the employee performs the service.

D) over the periods of the employee's service life to retirement.

A) in the period of exercise.

B) at the grant date.

C) in the periods in which the employee performs the service.

D) over the periods of the employee's service life to retirement.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

48

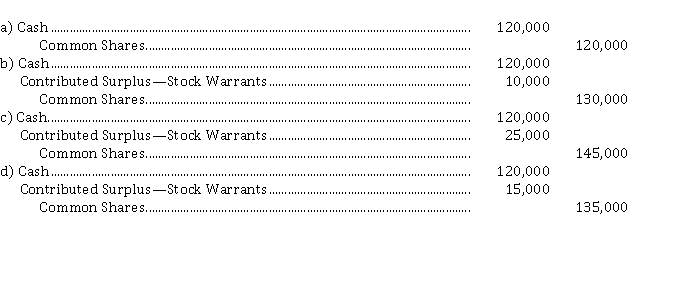

On July 1, 2020, Juba Inc. issued 10,000, $ 7 non-cumulative, no par value preferred shares for $ 1,050,000. Attached to each share was one detachable warrant, giving the holder the right to purchase one of Juba's no par value common shares for $ 30. At this time, the shares without the warrants would normally sell for $ 1,025,000, while the market price of the warrants was $ 2.50 each. On October 31, 2020, when the market price of the common shares was $ 33.50 and the market value of the warrants was $ 3.00, 4,000 warrants were exercised. Juba adheres to IFRS. As a result of the exercise of the warrants and the issuance of the related common shares, what journal entry would Juba make?

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

49

Use the following information for questions 55-56.

On May 1, 2020, Wong Ltd. issued $ 500,000, 10 year, 7% bonds at 103. Twenty detachable warrants were attached to each $ 1,000 bond, which entitled the holder to purchase one of Wong's no par value common shares for $ 40. At this time, similar bonds without warrants were selling at 96. It was determined that the fair value of Wong's common shares was $ 35, but the value of the warrants was NOT determinable. Wong is a private corporation that follows ASPE, but does NOT use the residual method.

On May 1, 2020, Wong should credit Bonds Payable for

A) $ 515,000.

B) $ 500,000.

C) $ 480,000.

D) cannot be determined from the information given.

On May 1, 2020, Wong Ltd. issued $ 500,000, 10 year, 7% bonds at 103. Twenty detachable warrants were attached to each $ 1,000 bond, which entitled the holder to purchase one of Wong's no par value common shares for $ 40. At this time, similar bonds without warrants were selling at 96. It was determined that the fair value of Wong's common shares was $ 35, but the value of the warrants was NOT determinable. Wong is a private corporation that follows ASPE, but does NOT use the residual method.

On May 1, 2020, Wong should credit Bonds Payable for

A) $ 515,000.

B) $ 500,000.

C) $ 480,000.

D) cannot be determined from the information given.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

50

In 2019, Algiers Inc. issued 10,000 no par value convertible preferred shares for $ 103 each. One preferred share can be converted into three shares of Algiers' no par value common shares at the option of the shareholder. In August 2020, all of the preferred shares were converted into common shares. The market value of the common shares at the date of the conversion was $ 30 per share. What amount should be credited to Common Shares as a result of this conversion?

A) $ 300,000

B) $ 500,000

C) $ 900,000

D) $ 1,030,000

A) $ 300,000

B) $ 500,000

C) $ 900,000

D) $ 1,030,000

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

51

On December 1, 2020, Cairo Ltd. issued 500 of its 9%, $ 1,000 bonds at 103. Attached to each bond was one detachable warrant entitling the holder to purchase ten of Cairo's common shares. At this time, the market value of the bonds, without the warrants, was 95, and the market value of each warrant was $ 50. Using the residual method, the amount of the proceeds from the issuance that should be credited to Bonds Payable would be

A) $ 475,000.

B) $ 489,250.

C) $ 500,000.

D) $ 515,000.

A) $ 475,000.

B) $ 489,250.

C) $ 500,000.

D) $ 515,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

52

Lagos Inc. issued bonds with detachable warrants for $ 5,000,000 (par value). The bonds have a present value of $ 4,934,400. The fair value of the warrants is determined to be $ 220,000. Using the relative fair value method, how much of the issue price should be allocated to the warrants?

A) $ 65,600

B) $ 211,200

C) $ 213,500

D) $ 220,000

A) $ 65,600

B) $ 211,200

C) $ 213,500

D) $ 220,000

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

53

Wang Inc. has $ 3,000,000 (par value), 8% convertible bonds outstanding. Each $ 1,000 bond is convertible into thirty no par value common shares. The bonds pay interest on January 31 and July 31. On July 31, 2020, the holders of $ 900,000 worth of bonds exercised the conversion privilege. On that date the market price of the bonds was 105, the market price of the common shares was $ 36, the carrying value of the common shares was $ 18 and the Contributed Surplus-Conversion Rights account balance was $ 450,000. The total unamortized bond premium at the date of conversion was $ 210,000. Using the book value method, Wang should record, as a result of this conversion,

A) a credit of $ 135,000 to Contributed Surplus-Conversion Rights.

B) a debit of $ 135,000 to Contributed Surplus-Conversion Rights.

C) a credit of $ 63,000 to Bonds Payable.

D) a debit of $ 210,000 to Bonds Payable.

A) a credit of $ 135,000 to Contributed Surplus-Conversion Rights.

B) a debit of $ 135,000 to Contributed Surplus-Conversion Rights.

C) a credit of $ 63,000 to Bonds Payable.

D) a debit of $ 210,000 to Bonds Payable.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

54

On July 1, 2020, an interest payment date, $ 180,000 (par value) of Lusaka Corp. bonds were converted into 3,600 of their no par common shares. At this time, the unamortized discount on the bonds was $ 7,200. When the bonds were originally issued, the equity portion of the bond was valued at $ 1,700. Using the book value method, Lusaka would record

A) an $ 174,500 increase in Common Shares.

B) an $ 172,800 increase in Common Shares.

C) an $ 171,100 increase in Common Shares.

D) no change to Contributed Surplus.

A) an $ 174,500 increase in Common Shares.

B) an $ 172,800 increase in Common Shares.

C) an $ 171,100 increase in Common Shares.

D) no change to Contributed Surplus.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

55

Bissau Ltd. issued $ 4,000,000, 5-year, 8% convertible bonds at par. Bonds pay interest annually. Each $ 1,000 bond is convertible to 200 of Bissau's no par value common shares, which are currently trading at $ 25 each. The current market rate for similar non-convertible bonds is 10%. Assuming Bissau adheres to IFRS, the value to be recorded for the conversion option is

A) $ 0.

B) $ 5,000.

C) $ 100,000.

D) $ 303,267.

A) $ 0.

B) $ 5,000.

C) $ 100,000.

D) $ 303,267.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

56

Use the following information for questions 55-56.

On May 1, 2020, Wong Ltd. issued $ 500,000, 10 year, 7% bonds at 103. Twenty detachable warrants were attached to each $ 1,000 bond, which entitled the holder to purchase one of Wong's no par value common shares for $ 40. At this time, similar bonds without warrants were selling at 96. It was determined that the fair value of Wong's common shares was $ 35, but the value of the warrants was NOT determinable. Wong is a private corporation that follows ASPE, but does NOT use the residual method.

On May 1, 2020, Wong should credit Contributed Surplus-Stock Warrants for

A) $ 35,000.

B) $ 20,000.

C) $ 15,000.

D) $ 0.

On May 1, 2020, Wong Ltd. issued $ 500,000, 10 year, 7% bonds at 103. Twenty detachable warrants were attached to each $ 1,000 bond, which entitled the holder to purchase one of Wong's no par value common shares for $ 40. At this time, similar bonds without warrants were selling at 96. It was determined that the fair value of Wong's common shares was $ 35, but the value of the warrants was NOT determinable. Wong is a private corporation that follows ASPE, but does NOT use the residual method.

On May 1, 2020, Wong should credit Contributed Surplus-Stock Warrants for

A) $ 35,000.

B) $ 20,000.

C) $ 15,000.

D) $ 0.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

57

Use the following information for questions 47-49.

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

What was the effective interest rate on the bonds when they were issued?

A) 9%

B) above 9%

C) below 9%

D) cannot determine from the information given

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

What was the effective interest rate on the bonds when they were issued?

A) 9%

B) above 9%

C) below 9%

D) cannot determine from the information given

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

58

On March 1, 2020, Rabat Corp. sold $ 300,000 (par value), 20 year, 8% bonds at 104. Each $ 1,000 bond was issued with 25 detachable warrants, each of which entitled the bondholder to purchase for $ 50 one of Rabat's no par value common shares. The bonds without the warrants would normally sell at 95. At this time, the market value of Rabat's common shares was $ 40 per share and the market value of each warrant was $ 2.00. Using the relative fair value method, what amount should Rabat record on March 1, 2020 as Contributed Surplus-Stock Warrants?

A) $ 10,800

B) $ 12,600

C) $ 15,000

D) $ 15,600

A) $ 10,800

B) $ 12,600

C) $ 15,000

D) $ 15,600

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

59

Under a (non-compensatory) employee stock option plan (ESOP), when an option is sold to an employee, the employer debits Cash and credits

A) Common Shares.

B) Stock Option Payable.

C) Contributed Surplus - Stock Options.

D) Stock Option Revenue.

A) Common Shares.

B) Stock Option Payable.

C) Contributed Surplus - Stock Options.

D) Stock Option Revenue.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

60

Use the following information for questions 47-49.

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

What is the amount of the unamortized bond discount on April 1, 2021 relating to the bonds that were converted?

A) $ 64,246

B) $ 46,800

C) $ 43,200

D) $ 44,400

On July 2, 2020, Martineau Ltd. issued $ 6,000,000 (par value), 9%, ten-year convertible bonds at 98. The bonds were dated April 1, 2020 with interest payable quarterly on July 1, October 1, January 1 and April 1. If the bonds had NOT been convertible, they would have sold for 96.1. The bond discount is amortized on a straight-line basis. On April 1, 2021, $ 1,200,000 of these bonds were converted into 500 no par common shares. Accrued interest was paid in cash at the time of conversion.

What is the amount of the unamortized bond discount on April 1, 2021 relating to the bonds that were converted?

A) $ 64,246

B) $ 46,800

C) $ 43,200

D) $ 44,400

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

61

Hedge accounting is

A) mandatory.

B) mandatory if specified criteria are met.

C) optional until December 2021 and mandatory thereafter.

D) optional.

A) mandatory.

B) mandatory if specified criteria are met.

C) optional until December 2021 and mandatory thereafter.

D) optional.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

62

The payment to executives from a performance-type plan is NEVER based on the

A) market price of the common shares.

B) return on assets (investment).

C) return on common shareholders' equity.

D) sales.

A) market price of the common shares.

B) return on assets (investment).

C) return on common shareholders' equity.

D) sales.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

63

If a SAR is determined to be an equity instrument, it would be valued at

A) grant date and not revised at subsequent interim dates.

B) each interim date.

C) exercise date.

D) grant date and revalued at exercise date.

A) grant date and not revised at subsequent interim dates.

B) each interim date.

C) exercise date.

D) grant date and revalued at exercise date.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

64

Using IFRS, hedge accounting allows the gain or loss on the hedge transaction to

A) be booked through net income.

B) be booked through other comprehensive income.

C) not be booked.

D) not be booked until the hedge closes.

A) be booked through net income.

B) be booked through other comprehensive income.

C) not be booked.

D) not be booked until the hedge closes.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

65

On December 31, 2018, in order to retain certain key executives, Entebbe Corporation granted them stock options. 25,000 options were granted at an option price of $ 40 per share. Market prices of the shares were as follows: December 31, 2019 $ 35 per share

December 31, 2020 $ 39 per share

The options were granted as compensation for services to be rendered over a two-year period beginning January 1, 2019. The Black-Scholes option pricing model determined total compensation expense to be $ 500,000. The amount of compensation expense Entebbe should have recorded for calendar 2020 is

A) $ 250,000.

B) $ 500,000.

C) $ 875,000.

D) $ 1,000,000.

December 31, 2020 $ 39 per share

The options were granted as compensation for services to be rendered over a two-year period beginning January 1, 2019. The Black-Scholes option pricing model determined total compensation expense to be $ 500,000. The amount of compensation expense Entebbe should have recorded for calendar 2020 is

A) $ 250,000.

B) $ 500,000.

C) $ 875,000.

D) $ 1,000,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

66

Hedging is the use of

A) derivatives or other instruments to increase returns.

B) derivatives or other instruments to offset risks.

C) debt to offset risks.

D) forward contracts.

A) derivatives or other instruments to increase returns.

B) derivatives or other instruments to offset risks.

C) debt to offset risks.

D) forward contracts.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

67

Definition of derivative instruments

Define and explain derivative instruments.

Define and explain derivative instruments.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

68

An executive compensation plan in which the executive may receive compensation in cash, shares, or a combination of both, is known as

A) a nonqualified shares option plan.

B) a performance-type plan.

C) a stock appreciation rights plan.

D) both a performance-type and a stock appreciation rights plan.

A) a nonqualified shares option plan.

B) a performance-type plan.

C) a stock appreciation rights plan.

D) both a performance-type and a stock appreciation rights plan.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

69

A fair value hedge protects the company against

A) errors in valuation of derivative instruments.

B) a future transaction that has not yet been recognized.

C) an existing exposure related to an existing asset or liability.

D) fluctuations in exchange rates.

A) errors in valuation of derivative instruments.

B) a future transaction that has not yet been recognized.

C) an existing exposure related to an existing asset or liability.

D) fluctuations in exchange rates.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

70

Compensation expense resulting from a performance-type plan is generally

A) determined at the measurement date.

B) recognized in the period of the grant.

C) allocated to the periods subsequent to the measurement date.

D) recognized in the period of exercise.

A) determined at the measurement date.

B) recognized in the period of the grant.

C) allocated to the periods subsequent to the measurement date.

D) recognized in the period of exercise.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

71

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows: Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

What amount of compensation expense should Luanda recognize for calendar 2019?

A) $ 150,000

B) $ 187,500

C) $ 225,000

D) $ 900,000

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.What amount of compensation expense should Luanda recognize for calendar 2019?

A) $ 150,000

B) $ 187,500

C) $ 225,000

D) $ 900,000

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

72

If a company enters into a hedging contract to swap a floating interest rate for a fixed rate, by the end of the contract the interest rate incurred by the company will equal

A) the difference between the fixed and the floating rate.

B) the floating rate.

C) the fixed rate.

D) whichever rate is highest.

A) the difference between the fixed and the floating rate.

B) the floating rate.

C) the fixed rate.

D) whichever rate is highest.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

73

Purchased call options

On April 1, 2021, Petty Ltd. purchased a call option from Fidelity Investments Corporation. The option gave Petty the right to buy 5,000 shares in Monahan Ltd., at a price of $ 50 per share. On the day Petty purchased the option, Monahan shares were trading at $ 50 each. Petty paid $ 1,000 for the options. On April 30, 2021, the Monahan shares were trading at $ 53.50 each, and the options for Monahan shares were trading at $ 18,000. On May 15, Petty settled the options in cash when the Monahan shares were trading at $ 56 and the options were trading at $ 30,000.

Instructions

a) Prepare the journal entries to record the above transactions.

b) Prepare the May 15 journal entry assuming Petty accepted the shares in Monahan instead.

On April 1, 2021, Petty Ltd. purchased a call option from Fidelity Investments Corporation. The option gave Petty the right to buy 5,000 shares in Monahan Ltd., at a price of $ 50 per share. On the day Petty purchased the option, Monahan shares were trading at $ 50 each. Petty paid $ 1,000 for the options. On April 30, 2021, the Monahan shares were trading at $ 53.50 each, and the options for Monahan shares were trading at $ 18,000. On May 15, Petty settled the options in cash when the Monahan shares were trading at $ 56 and the options were trading at $ 30,000.

Instructions

a) Prepare the journal entries to record the above transactions.

b) Prepare the May 15 journal entry assuming Petty accepted the shares in Monahan instead.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

74

Put options

On November 15, 2020, Marvel Inc. purchases a trading investment for $ 150,000. Marvel also enters into a put option to sell the shares for $ 150,000. At December 31, 2020, the investment is valued at $ 155,000.

Instructions

Record any adjusting entries required at December 31, 2020 in connection with the above transactions.

On November 15, 2020, Marvel Inc. purchases a trading investment for $ 150,000. Marvel also enters into a put option to sell the shares for $ 150,000. At December 31, 2020, the investment is valued at $ 155,000.

Instructions

Record any adjusting entries required at December 31, 2020 in connection with the above transactions.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

75

On January 1, 2018, Tunis Inc. granted stock options for 50,000 of its no par value common shares to key employees, at an option price of $ 25. On that date, the market price of the common shares was $ 23. The Black-Scholes option pricing model determined total compensation expense to be $ 375,000. The options are exercisable beginning January 1, 2021, provided the key employees are still employed by Tunis at the time the options are exercised. The options expire on January 1, 2022. On January 2, 2021, when the market price of the shares was $ 29 per share, all 50,000 options were exercised. The amount of compensation expense Tunis should have recorded for calendar 2020 is

A) $ 0.

B) $ 50,000.

C) $ 125,000.

D) $ 187,500.

A) $ 0.

B) $ 50,000.

C) $ 125,000.

D) $ 187,500.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

76

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows: Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

What amount of compensation expense should Luanda recognize for calendar 2020?

A) $ 0

B) $ 25,000

C) $ 125,000

D) $ 250,000

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.What amount of compensation expense should Luanda recognize for calendar 2020?

A) $ 0

B) $ 25,000

C) $ 125,000

D) $ 250,000

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

77

On June 30, 2018, Kinshasa Corp. granted stock options for 30,000 of its no par value common shares to key employees, at an option price of $ 36. On that date, the market price of the common shares was $ 32. The Black-Scholes option pricing model determined total compensation expense to be $ 720,000. The options are exercisable beginning January 1, 2021, provided the key employees are still employed by Kinshasa at the time the options are exercised. The options expire on June 30, 2022. On January 2, 2021, when the market price of the shares was $ 42, all 30,000 options were exercised. The amount of compensation expense Kinshasa should have recorded for calendar 2020 is

A) $ 120,000.

B) $ 288,000.

C) $ 360,000.

D) $ 720,000.

A) $ 120,000.

B) $ 288,000.

C) $ 360,000.

D) $ 720,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

78

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows: Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

On December 31, 2021, 8,000 SARs are exercised by executives. What amount of compensation expense should Luanda recognize for calendar 2021?

A) $ 65,000

B) $ 162,500

C) $ 237,500

D) $ 487,500

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.On December 31, 2021, 8,000 SARs are exercised by executives. What amount of compensation expense should Luanda recognize for calendar 2021?

A) $ 65,000

B) $ 162,500

C) $ 237,500

D) $ 487,500

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

79

On January 2, 2020, for past services rendered, Zeus Corp. granted Joanna Wood, its president, 18,000 stock appreciation rights that are exercisable immediately and expire on January 2, 2021. On exercise, Wood is entitled to receive cash for the excess of the market price of the shares on the exercise date over the market price on the grant date. Wood did NOT exercise any of the rights during 2020. The market price of Zeus's shares was $ 35 on January 2, 2020, and $ 45 on December 31, 2020. As a result of the stock appreciation rights, Zeus should recognize compensation expense for 2020 of

A) $ 0.

B) $ 180,000.

C) $ 630,000.

D) $ 810,000.

A) $ 0.

B) $ 180,000.

C) $ 630,000.

D) $ 810,000.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

80

The date on which to measure the compensation in a stock appreciation rights plan is the

A) date of grant.

B) date of exercise.

C) end of each interim period up to the date of exercise.

D) date that the market price exceeds the option price.

A) date of grant.

B) date of exercise.

C) end of each interim period up to the date of exercise.

D) date that the market price exceeds the option price.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 99 flashcards in this deck.