Exam 4: Complex Financial Instruments

Exam 1: Non-Financial and Current Liabilities91 Questions

Exam 2: Long-Term Financial Liabilities92 Questions

Exam 3: Shareholders Equity161 Questions

Exam 4: Complex Financial Instruments99 Questions

Exam 5: Earnings Per Share73 Questions

Exam 6: Income Taxes74 Questions

Exam 7: Pensions and Other Post-Employment Benefits106 Questions

Exam 8: Leases127 Questions

Exam 9: Accounting Changes and Error Analysis65 Questions

Exam 10: Statement of Cash Flows82 Questions

Exam 11: Other Measurement and Disclosure Issues56 Questions

Select questions type

If a company enters into a hedging contract to swap a floating interest rate for a fixed rate, by the end of the contract the interest rate incurred by the company will equal

Free

(Multiple Choice)

4.8/5  (45)

(45)

Correct Answer: Verified

Verified

C

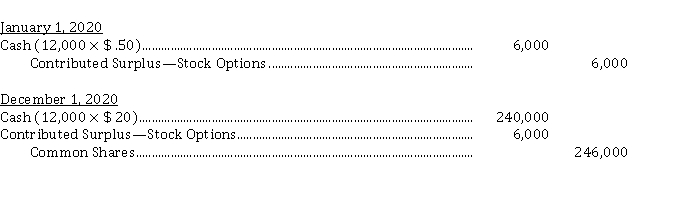

Employee share ownership plans

Grieger Inc. set up an ESOP under which employees may purchase shares of the company for $ 20 per share. The option premium is $ .50 per share and Grieger set aside 20,000 shares. On January 1, 2020, 12,000 options are purchased by employees. On December 1, 2020, all 12,000 options are exercised.

Instructions

Prepare the journal entries to record the above events.

Free

(Essay)

4.8/5 (41)

Correct Answer:Verified

An executive compensation plan in which the executive may receive compensation in cash, shares, or a combination of both, is known as

(Multiple Choice)

4.7/5 (38)

On January 1, 2020, Orion Corp. granted an employee an option to purchase 5,000 of Orion's no par value common shares at $ 50 per share. The Black-Scholes option pricing model determined total compensation expense to be $ 220,000. The option became exercisable on December 31, 2021, after the employee completed two years of service. The market prices of Orion's shares were as follows:  For calendar 2021, Orion should recognize compensation expense of

For calendar 2021, Orion should recognize compensation expense of

(Multiple Choice)

4.8/5 (33)

On June 30, 2018, Kinshasa Corp. granted stock options for 30,000 of its no par value common shares to key employees, at an option price of $ 36. On that date, the market price of the common shares was $ 32. The Black-Scholes option pricing model determined total compensation expense to be $ 720,000. The options are exercisable beginning January 1, 2021, provided the key employees are still employed by Kinshasa at the time the options are exercised. The options expire on June 30, 2022. On January 2, 2021, when the market price of the shares was $ 42, all 30,000 options were exercised. The amount of compensation expense Kinshasa should have recorded for calendar 2020 is

(Multiple Choice)

4.8/5 (34)

Convertible debt and debt with warrants

What accounting treatment is required for convertible debt? Why? What accounting treatment is required for debt issued with stock warrants? Why?

(Essay)

4.9/5 (36)

On December 1, 2020, Cairo Ltd. issued 500 of its 9%, $ 1,000 bonds at 103. Attached to each bond was one detachable warrant entitling the holder to purchase ten of Cairo's common shares. At this time, the market value of the bonds, without the warrants, was 95, and the market value of each warrant was $ 50. Using the residual method, the amount of the proceeds from the issuance that should be credited to Bonds Payable would be

(Multiple Choice)

4.8/5 (35)

Wang Inc. has $ 3,000,000 (par value), 8% convertible bonds outstanding. Each $ 1,000 bond is convertible into thirty no par value common shares. The bonds pay interest on January 31 and July 31. On July 31, 2020, the holders of $ 900,000 worth of bonds exercised the conversion privilege. On that date the market price of the bonds was 105, the market price of the common shares was $ 36, the carrying value of the common shares was $ 18 and the Contributed Surplus-Conversion Rights account balance was $ 450,000. The total unamortized bond premium at the date of conversion was $ 210,000. Using the book value method, Wang should record, as a result of this conversion,

(Multiple Choice)

4.7/5 (34)

Fair value disclosure for financial instruments - Fair Value Hierarchy

What is the Fair Value hierarchy and what information must a company provide under this hierarchy?

(Essay)

4.7/5 (43)

Redeemable preferred shares and succession planning

Explain how redeemable preferred shares are used in succession planning for small business corporations.

(Essay)

4.8/5 (37)

Dividends on term preferred shares, where the shares have been recorded as a liability, should be debited to

(Multiple Choice)

4.8/5 (32)

Forward contract

Trudel Builders Ltd. uses fir 2x6 lumber as its framing material. On November 15, 2020, Trudel enters into a forward contract for 1,500,000 board feet of lumber at $ 0.25 per board foot for March 2021 delivery. At December 31, 2020, the market price for March delivery is $ 0.26. On March 5, 2021, Trudel took delivery of 1,500,000 board feet for $ 0.25 and settled the forward contract. The market rate on this date was $ 0.28 per board foot.

Instructions

Record any required entries related to this contract.

(Essay)

4.9/5 (38)

Under IFRS, mandatorily redeemable preferred shares (term preferred shares) are treated as

(Multiple Choice)

4.8/5 (34)

Purchased call options

On April 1, 2021, Petty Ltd. purchased a call option from Fidelity Investments Corporation. The option gave Petty the right to buy 5,000 shares in Monahan Ltd., at a price of $ 50 per share. On the day Petty purchased the option, Monahan shares were trading at $ 50 each. Petty paid $ 1,000 for the options. On April 30, 2021, the Monahan shares were trading at $ 53.50 each, and the options for Monahan shares were trading at $ 18,000. On May 15, Petty settled the options in cash when the Monahan shares were trading at $ 56 and the options were trading at $ 30,000.

Instructions

a) Prepare the journal entries to record the above transactions.

b) Prepare the May 15 journal entry assuming Petty accepted the shares in Monahan instead.

(Essay)

4.8/5 (38)

When convertible debt is converted to common shares, IFRS requires that this is recorded by the

(Multiple Choice)

4.8/5 (32)

Use the following information for questions 74-76.

On January 1, 2019, Luanda Ltd. established a stock appreciation rights plan for its executives. This plan entitles them to receive cash at any time during the next four years for the difference between the market price of its common shares and a pre-established price of $ 20, on 50,000 SARs. Market prices of the shares are as follows:  Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

-What amount of compensation expense should Luanda recognize for calendar 2019?

Compensation expense relating to the plan is to be recorded over a four-year period beginning January 1, 2019.

-What amount of compensation expense should Luanda recognize for calendar 2019?

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)