Deck 9: Current Liabilities and Contingent Obligations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

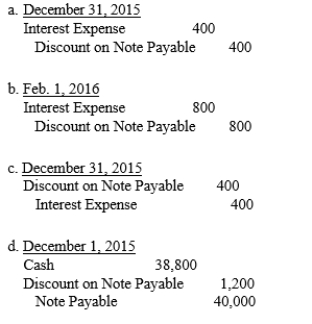

On December 1, 2015, Sons, Inc. borrowed money at the bank by signing a 90-day non-interest-bearing note for $40,000 that was discounted at 12%. Which of the following entries is not correct?

Question

Question

Question

Question

On December 31, 2016, the Wagner Company had the following liabilities:

On December 31, Wagner signed a binding agreement with its bank to refinance the 12% note through February 14, 2019, at a variable interest rate.

What is the amount of Wagner's current liabilities on December 31, 2016?

A) $150,000

B) $190,000

C) $230,000

D) $260,000

On December 31, Wagner signed a binding agreement with its bank to refinance the 12% note through February 14, 2019, at a variable interest rate.

What is the amount of Wagner's current liabilities on December 31, 2016?

A) $150,000

B) $190,000

C) $230,000

D) $260,000

Question

Question

Question

Question

Question

Question

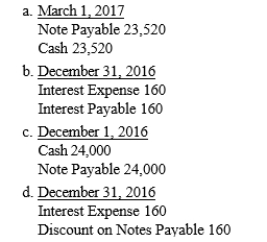

On December 1, 2016, Old Car Co. borrowed money at the bank by signing a 90-day non-interest-bearing note for $24,000 that was discounted at 8%. Which of the following entries is correct?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

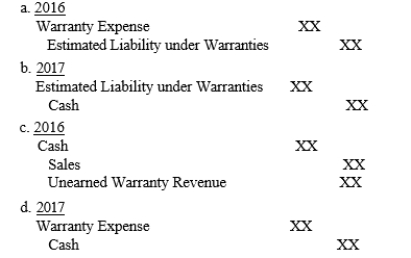

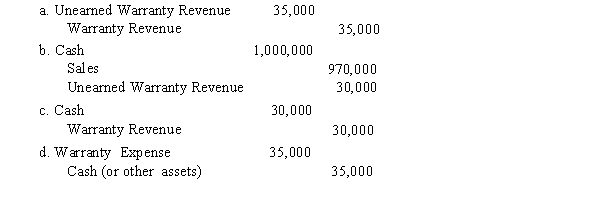

Which of the following journal entries would probably be made if the modified cash basis of accounting for warranties is in use for a sale made in 2016?

Question

American Business Services introduced a new machine on January 1, 2016. The machine carried a two-year warranty against defects. The estimated warranty costs related to dollar sales were 3% in the year of sale and 5% in the year after sale. Additional information follows: Actual Warranty  If American Business Services considers these warranties to be assurance-type and accounts for them by accruing the expense and the related liability) in the year of the sale, what amount relating to warranties should be reflected on the December 31, 2017, balance sheet?

If American Business Services considers these warranties to be assurance-type and accounts for them by accruing the expense and the related liability) in the year of the sale, what amount relating to warranties should be reflected on the December 31, 2017, balance sheet?

A) $5,300

B) $6,400

C) $6,500

D) $9,100

If American Business Services considers these warranties to be assurance-type and accounts for them by accruing the expense and the related liability) in the year of the sale, what amount relating to warranties should be reflected on the December 31, 2017, balance sheet?A) $5,300

B) $6,400

C) $6,500

D) $9,100

Question

Question

Question

Question

Question

Question

Question

Question

Question

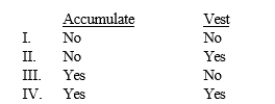

Sick pay benefits that are related to an employee's services already rendered, whose payment is probable and whose amount can reasonably be estimated, must be accrued and recognized as a current liability if the obligation relates to rights that

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Question

Question

Question

King Sales sells a certain product for $20,000. Included in this price is an implied service-type warranty of $600. Fifty machines were sold in 2016. Warranty expense incurred during 2016 amounted to $35,000. Which of the following entries would King Sales probably not make in 2016?

Question

Question

Question

Question

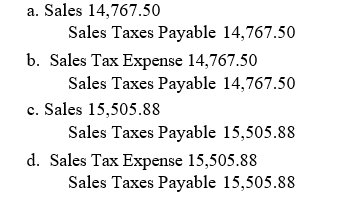

Candy's Video includes the amount of sales taxes collected directly in the price charged for merchandise, and the total amount is credited to Sales. During January, Sales was credited for $310,117.50. The January 31 adjusting entry to account for a 5% state sales tax should be

Question

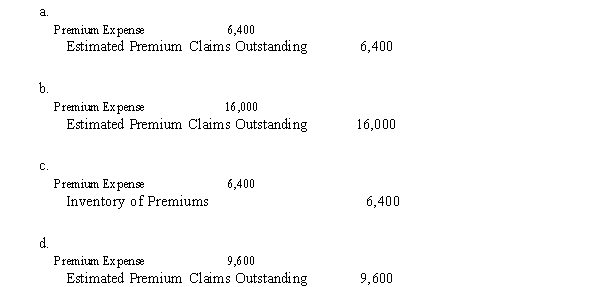

Jennifer Cakes places a coupon in each box of its product. Customers may send in five coupons and $3, and the company will send them a recipe book. Sufficient books were purchased at a cost of $5 each. A total of 400,000 boxes of product were sold in 2016. It was estimated that 6% of the coupons would be redeemed. During 2016, 8,000 coupons were redeemed. Which entry should be made at December 31, 2016?

Question

Question

Question

Question

Question

Question

Albert Corp. introduced a new machine on January 1, 2016. The machine carried a two-year assurance-type warranty against defects. The estimated warranty costs related to dollar sales were 3% in the year of sale and 5% in the year after sale. Additional information follows: Actual Warranty  If the company uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale, what amount relating to warranty expense should be reflected on the December 31, 2017 income statement?

If the company uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale, what amount relating to warranty expense should be reflected on the December 31, 2017 income statement?

A) $2,200

B) $4,800

C) $5,200

D) $7,400

If the company uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale, what amount relating to warranty expense should be reflected on the December 31, 2017 income statement?A) $2,200

B) $4,800

C) $5,200

D) $7,400

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Exhibit 9-5

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of expenditures for warranty costs for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of expenditures for warranty costs for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Question

Question

Question

Exhibit 9-5

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of warranty expense for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of warranty expense for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/125

Play

Full screen (f)

Deck 9: Current Liabilities and Contingent Obligations

1

Bonus agreements can be structured in various ways. A typical bonus calculation could involve income before or after taxes and income before or after the bonus.

True

2

Assets and liabilities with differing implications for financial flexibility should be reported together.

False

3

Which of the following statements does not describe an essential characteristic of a liability?

A) A liability is a present obligation that will be settled by a probable future transfer or use of assets.

B) The obligated entity has little or no discretion to avoid the future sacrifice.

C) The identity of the recipient must be known to the obligated party.

D) The transaction or event obligating the enterprise has already occurred.

A) A liability is a present obligation that will be settled by a probable future transfer or use of assets.

B) The obligated entity has little or no discretion to avoid the future sacrifice.

C) The identity of the recipient must be known to the obligated party.

D) The transaction or event obligating the enterprise has already occurred.

C

4

Which of the following is a legal liability?

A) sick pay that may be taken as time off

B) sales taxes payable to the state

C) gambling debt owed

D) bribes due to foreign traders

A) sick pay that may be taken as time off

B) sales taxes payable to the state

C) gambling debt owed

D) bribes due to foreign traders

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

5

Assume that a company is facing a loss contingency. GAAP requires the company to categorize the likelihood of occurrence of a future event that will confirm the loss as being plausible, remotely plausible, or remote.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

6

The ability to refinance short-term obligations on a long-term basis can be demonstrated if the company has already refinanced those obligations after the date of the balance sheet but before it is issued.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

7

Assume that a company is facing a loss contingency. GAAP requires the company to recognize a liability even if the company cannot determine whether or not the event has occurred.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

8

Under current standards of the FASB, liabilities include

A) only legal obligations.

B) both legal and illegal obligations.

C) both legal and nonlegal obligations.

D) legal, nonlegal, and illegal obligations.

A) only legal obligations.

B) both legal and illegal obligations.

C) both legal and nonlegal obligations.

D) legal, nonlegal, and illegal obligations.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following is not an issue associated with liabilities?

A) Identification

B) Valuation and Measurement

C) Assessment

D) Reporting

A) Identification

B) Valuation and Measurement

C) Assessment

D) Reporting

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

10

Vacation pay and year-end bonuses would be considered legal liabilities.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

11

Liabilities are defined as probable future sacrifices of economic benefits arising from present obligations of a company to provide services or assets in the future as defined by the FASB.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

12

All of the following are examples of legal liabilities except

A) notes payable.

B) sales tax payable.

C) sick pay payable may be taken as time off).

D) property taxes payable.

A) notes payable.

B) sales tax payable.

C) sick pay payable may be taken as time off).

D) property taxes payable.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

13

The FASB recommends that assets and liabilities with differing liquidities be arranged as separate items in the balance sheet.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

14

Which is not a characteristic of a liability?

A) There will be a probable future transfer or use of assets.

B) There is little or no discretion to avoid the future sacrifice.

C) The obligating transaction or event must have already happened.

D) A legally enforceable claim must be present.

A) There will be a probable future transfer or use of assets.

B) There is little or no discretion to avoid the future sacrifice.

C) The obligating transaction or event must have already happened.

D) A legally enforceable claim must be present.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

15

Short-term debt that is expected to be refinanced on a long-term basis may be excluded from the current liability classification if the company has the intent to refinance or the ability to refinance.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

16

The FASB is concerned with the accurate portrayal of liquidity because users evaluate future cash flows in their decision making practices.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not a characteristic of a liability?

A) It will be settled by a future transfer of assets.

B) The company has no discretion to avoid the future sacrifice.

C) The obligating event has already happened.

D) All of these are characteristics of a liability.

A) It will be settled by a future transfer of assets.

B) The company has no discretion to avoid the future sacrifice.

C) The obligating event has already happened.

D) All of these are characteristics of a liability.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following statements is true?

A) One of the essential characteristics of a liability is that the transaction or other event obligating the entity will probably occur in the future.

B) In order for there to be a liability, a duty or responsibility must be present that obligates a particular entity.

C) In order for there to be a liability, a legally enforceable claim must be present.

D) In order to have a liability, the identity of the recipient must be known.

A) One of the essential characteristics of a liability is that the transaction or other event obligating the entity will probably occur in the future.

B) In order for there to be a liability, a duty or responsibility must be present that obligates a particular entity.

C) In order for there to be a liability, a legally enforceable claim must be present.

D) In order to have a liability, the identity of the recipient must be known.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

19

Compensated absences include vacation, holiday, sick, or other activities for which the company pays its employees.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

20

The ability to utilize financial resources and to adapt to changes in the business environment is referred to as a company's financial flexibility.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

21

The Lawrence Company records its trade accounts payable net of any cash discounts. At the end of 2016, Lawrence had a balance of $300,000 in its trade accounts payable account before any adjustments related to the following items:

1) Goods shipped to Lawrence FOB shipping point were in transit on December 31. The invoice price of the goods was $50,000, with a 2% discount allowed for prompt payment.

Goods shipped to Lawrence FOB destination on December 29 arrived on January 2, 2017.

2) The invoice price of the goods was $9,000, with a 4% discount allowed for payment within 20 days.

On December 10, Lawrence had recorded a shipment received. The recorded invoice price

3) was $24,750, net, with a 1% discount allowed for payment within 14 days. At the end of the year, payment had not been made.

At what amount should Lawrence report trade accounts payable on its December 31, 2016 balance sheet?

A) $349,000

B) $349,250

C) $357,680

D) $357,930

1) Goods shipped to Lawrence FOB shipping point were in transit on December 31. The invoice price of the goods was $50,000, with a 2% discount allowed for prompt payment.

Goods shipped to Lawrence FOB destination on December 29 arrived on January 2, 2017.

2) The invoice price of the goods was $9,000, with a 4% discount allowed for payment within 20 days.

On December 10, Lawrence had recorded a shipment received. The recorded invoice price

3) was $24,750, net, with a 1% discount allowed for payment within 14 days. At the end of the year, payment had not been made.

At what amount should Lawrence report trade accounts payable on its December 31, 2016 balance sheet?

A) $349,000

B) $349,250

C) $357,680

D) $357,930

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

22

On December 1, 2015, Sons, Inc. borrowed money at the bank by signing a 90-day non-interest-bearing note for $40,000 that was discounted at 12%. Which of the following entries is not correct?

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

23

Discount on Notes Payable should be classified as a

A) current asset.

B) contra account to Notes Payable.

C) part of shareholders' equity.

D) companion account to Notes Payable.

A) current asset.

B) contra account to Notes Payable.

C) part of shareholders' equity.

D) companion account to Notes Payable.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

24

Cooper's inventory has been financed 100% with a long-term note. The note is coming due in 2016. Cooper has received a commitment from a new lender that permits five-year refinancing of debt up to an amount equal to 50% of inventory, which is expected to range between $14,000 and $20,000 in 2016. At December 31, 2015, how much of the company's currently maturing note payable can be classified as long-term debt?

A) $7,000

B) $6,000

C) $10,000

D) $9,000

A) $7,000

B) $6,000

C) $10,000

D) $9,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following dividends is not considered a current liability when declared?

A) property dividends

B) stock dividends

C) scrip dividends

D) cash dividends

A) property dividends

B) stock dividends

C) scrip dividends

D) cash dividends

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

26

On December 31, 2016, the Wagner Company had the following liabilities:

On December 31, Wagner signed a binding agreement with its bank to refinance the 12% note through February 14, 2019, at a variable interest rate.

What is the amount of Wagner's current liabilities on December 31, 2016?

A) $150,000

B) $190,000

C) $230,000

D) $260,000

On December 31, Wagner signed a binding agreement with its bank to refinance the 12% note through February 14, 2019, at a variable interest rate.

What is the amount of Wagner's current liabilities on December 31, 2016?

A) $150,000

B) $190,000

C) $230,000

D) $260,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

27

Analysts use the quick ratio also known as the acid test ratio) and the current ratio. The use of both ratios has become common because

A) the quick ratio is much easier to compute than the current ratio.

B) interpretation of the current ratio is more difficult because of its complexity.

C) the acid test is a more severe test of a company's liquidity.

D) the acid test a better measure of management's effectiveness.

A) the quick ratio is much easier to compute than the current ratio.

B) interpretation of the current ratio is more difficult because of its complexity.

C) the acid test is a more severe test of a company's liquidity.

D) the acid test a better measure of management's effectiveness.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

28

Short-term debt expected to be refinanced

A) may be classified as long-term if both the intent to refinance and the ability to refinance exist.

B) must always be reported as a current liability.

C) may be classified as long-term if off-balance-sheet financing has been obtained.

D) may be classified as long-term if there is an intent to refinance.

A) may be classified as long-term if both the intent to refinance and the ability to refinance exist.

B) must always be reported as a current liability.

C) may be classified as long-term if off-balance-sheet financing has been obtained.

D) may be classified as long-term if there is an intent to refinance.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following statements is false?

A) A dividend payable in shares of the issuing company's stock is not reported as a current liability.

B) Interest and dividends accrue as a liability as time passes.

C) The declaration of a dividend may not result in a current liability.

D) Undeclared dividends in arrears on cumulative preferred stock are not recognized as a liability.

A) A dividend payable in shares of the issuing company's stock is not reported as a current liability.

B) Interest and dividends accrue as a liability as time passes.

C) The declaration of a dividend may not result in a current liability.

D) Undeclared dividends in arrears on cumulative preferred stock are not recognized as a liability.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

30

On the balance sheet, liabilities are generally classified as

A) current or long-term.

B) legal or nonlegal.

C) material or immaterial.

D) probable or estimated.

A) current or long-term.

B) legal or nonlegal.

C) material or immaterial.

D) probable or estimated.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

31

Management of current liabilities arises, in part, because of a concern over

A) profitability.

B) liquidity.

C) timeliness.

D) materiality.

A) profitability.

B) liquidity.

C) timeliness.

D) materiality.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

32

On December 1, 2016, Old Car Co. borrowed money at the bank by signing a 90-day non-interest-bearing note for $24,000 that was discounted at 8%. Which of the following entries is correct?

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

33

Beta, Inc. had $10,000 of notes payable coming due on January 10, 2016. As of December 31, 2015, Beta was negotiating with the lender to extend the due date of the note by two additional years. On January 5, 2016, the company used $2,000 of excess cash to pay off part of the note. On January 8, 2016, the refinancing was completed, the $2,000 payment was refunded and added back to the note balance, and the note was extended for another two years. On Beta's December 31, 2015 balance sheet, which was issued on April 1, 2016, how much of the $10,000 note should be shown as current?

A) $10,000

B) $0

C) $8,000

D) $2,000

A) $10,000

B) $0

C) $8,000

D) $2,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

34

With regard to liabilities, liquidity refers to

A) a company's ability to convert its assets to cash to pay for its liabilities.

B) a company's ability to use its financial resources to adapt to change.

C) a company's operating cycle.

D) only liabilities and not assets.

A) a company's ability to convert its assets to cash to pay for its liabilities.

B) a company's ability to use its financial resources to adapt to change.

C) a company's operating cycle.

D) only liabilities and not assets.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements regarding the gross and net methods for recording trade accounts payable is true?

A) The net method overstates accounts payable at the end of the accounting period.

B) The net method is more widely used in practice than is the gross method.

C) The gross method more accurately measures liquidity.

D) The net method highlights management inefficiency because purchase discounts lost are recorded whenever an invoice is paid after the cash discount period has expired.

A) The net method overstates accounts payable at the end of the accounting period.

B) The net method is more widely used in practice than is the gross method.

C) The gross method more accurately measures liquidity.

D) The net method highlights management inefficiency because purchase discounts lost are recorded whenever an invoice is paid after the cash discount period has expired.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

36

On January 1, 2016, the Pruett Company signed a six-month, non-interest-bearing note payable for $170,000 and received $162,800 from Your Neighborhood Bank. On January 31, 2016, what amount should Pruett record for interest expense, and what is the net carrying value of the note?

A) $1,200; $161,600

B) $0; $170,000

C) $7,200; $170,000

D) $1,200; $164,000

A) $1,200; $161,600

B) $0; $170,000

C) $7,200; $170,000

D) $1,200; $164,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following statements is true?

A) If ability to refinance a currently maturing obligation is present, the obligation should be classified as noncurrent debt.

B) If no reasonable estimate can be made of the minimum amount expected to be available for future refinancing, the entire outstanding short-term obligation must be disclosed as a noncurrent obligation.

C) The FASB has concluded that obligations that are due on demand should be classified as current liabilities, even though liquidation of the liabilities is not expected within the next year or operating cycle, whichever is longer.

D) If a refinancing is soon to be accomplished by issuing common stock, a currently maturing short-term obligation should be included in shareholders' equity on the current balance sheet.

A) If ability to refinance a currently maturing obligation is present, the obligation should be classified as noncurrent debt.

B) If no reasonable estimate can be made of the minimum amount expected to be available for future refinancing, the entire outstanding short-term obligation must be disclosed as a noncurrent obligation.

C) The FASB has concluded that obligations that are due on demand should be classified as current liabilities, even though liquidation of the liabilities is not expected within the next year or operating cycle, whichever is longer.

D) If a refinancing is soon to be accomplished by issuing common stock, a currently maturing short-term obligation should be included in shareholders' equity on the current balance sheet.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

38

Current liabilities are obligations whose liquidation is reasonably expected to require the use of existing current assets or the creation of other current liabilities within

A) one year or operating cycle, whichever is longer.

B) one year.

C) one year or operating cycle, whichever is shorter.

D) an operating cycle.

A) one year or operating cycle, whichever is longer.

B) one year.

C) one year or operating cycle, whichever is shorter.

D) an operating cycle.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

39

Current liabilities are obligations of a company that it expects to liquidate within

A) one year.

B) the normal operating cycle.

C) the normal operating cycle or one year, whichever is longer.

D) the normal operating cycle or one year, whichever is shorter.

A) one year.

B) the normal operating cycle.

C) the normal operating cycle or one year, whichever is longer.

D) the normal operating cycle or one year, whichever is shorter.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

40

The operating cycle is typically defined as the time it requires to convert

A) cash to inventory to receivables.

B) raw materials to finished goods.

C) finished goods to receivables to cash.

D) cash to inventory to receivables to cash.

A) cash to inventory to receivables.

B) raw materials to finished goods.

C) finished goods to receivables to cash.

D) cash to inventory to receivables to cash.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

41

All of the following payroll taxes are levied against the employer except

A) FICA taxes.

B) federal unemployment taxes.

C) state unemployment taxes.

D) federal income taxes withheld.

A) FICA taxes.

B) federal unemployment taxes.

C) state unemployment taxes.

D) federal income taxes withheld.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following journal entries would probably be made if the modified cash basis of accounting for warranties is in use for a sale made in 2016?

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

43

American Business Services introduced a new machine on January 1, 2016. The machine carried a two-year warranty against defects. The estimated warranty costs related to dollar sales were 3% in the year of sale and 5% in the year after sale. Additional information follows: Actual Warranty If American Business Services considers these warranties to be assurance-type and accounts for them by accruing the expense and the related liability) in the year of the sale, what amount relating to warranties should be reflected on the December 31, 2017, balance sheet?

A) $5,300

B) $6,400

C) $6,500

D) $9,100

If American Business Services considers these warranties to be assurance-type and accounts for them by accruing the expense and the related liability) in the year of the sale, what amount relating to warranties should be reflected on the December 31, 2017, balance sheet?A) $5,300

B) $6,400

C) $6,500

D) $9,100

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

44

Exhibit 9-2

In 2015, the Magtag Company sold 16,000 ovens. Magtag estimated that 14% of the machines would require repairs under the two-year assurance-type warranty at an average cost of $60. During 2015, Magtag had an actual outlay of

$62,000 for repairs under warranty. Magtag uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-2. At what amount should the company record warranty expense for 2015?

A) $42,000

B) $62,000

C) $134,400

D) $116,000

In 2015, the Magtag Company sold 16,000 ovens. Magtag estimated that 14% of the machines would require repairs under the two-year assurance-type warranty at an average cost of $60. During 2015, Magtag had an actual outlay of

$62,000 for repairs under warranty. Magtag uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-2. At what amount should the company record warranty expense for 2015?

A) $42,000

B) $62,000

C) $134,400

D) $116,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

45

According to current GAAP, which of the following is not a condition suggesting that an accrual for vacation pay should be made?

A) The obligation must relate to rights that vest.

B) The payment of compensation is probable.

C) The obligation must relate to employee services already rendered.

D) The amount can be reasonably estimated.

A) The obligation must relate to rights that vest.

B) The payment of compensation is probable.

C) The obligation must relate to employee services already rendered.

D) The amount can be reasonably estimated.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

46

Exhibit 9-1

The Happy Cereal Company includes a premium in each box of its cereal. For four premiums plus $2.00, customers are entitled to a plastic wiggle worm that costs Happy $4.50 each. Happy expects 60% of the premiums to be redeemed. In 2016, Happy sold 500,000 boxes of cereal and distributed 25,000 wiggle worms.

Refer to Exhibit 9-1. What is Happy's estimated liability for unredeemed premiums on December 31, 2016?

A) $125,000

B) $187,500

C) $225,000

D) $337,500

The Happy Cereal Company includes a premium in each box of its cereal. For four premiums plus $2.00, customers are entitled to a plastic wiggle worm that costs Happy $4.50 each. Happy expects 60% of the premiums to be redeemed. In 2016, Happy sold 500,000 boxes of cereal and distributed 25,000 wiggle worms.

Refer to Exhibit 9-1. What is Happy's estimated liability for unredeemed premiums on December 31, 2016?

A) $125,000

B) $187,500

C) $225,000

D) $337,500

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

47

Exhibit 9-1

The Happy Cereal Company includes a premium in each box of its cereal. For four premiums plus $2.00, customers are entitled to a plastic wiggle worm that costs Happy $4.50 each. Happy expects 60% of the premiums to be redeemed. In 2016, Happy sold 500,000 boxes of cereal and distributed 25,000 wiggle worms.

Refer to Exhibit 9-1. What is Happy's premium expense for 2016?

A) $125,000

B) $187,500

C) $225,000

D) $337,500

The Happy Cereal Company includes a premium in each box of its cereal. For four premiums plus $2.00, customers are entitled to a plastic wiggle worm that costs Happy $4.50 each. Happy expects 60% of the premiums to be redeemed. In 2016, Happy sold 500,000 boxes of cereal and distributed 25,000 wiggle worms.

Refer to Exhibit 9-1. What is Happy's premium expense for 2016?

A) $125,000

B) $187,500

C) $225,000

D) $337,500

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

48

The Antarctica Company closes its books annually on December 31, while the city in which it is located has a fiscal year beginning on April 1 and ending on March 31. Taxes on property are assessed on April 1 of each year. Property taxes in the amount of $360,000 and $390,000 were assessed on April 1, 2015 and 2016, respectively. For the year ended December 31, 2016, the Antarctica Company would report property tax expense of

A) $360,000.

B) $370,000.

C) $382,500.

D) $390,000.

A) $360,000.

B) $370,000.

C) $382,500.

D) $390,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

49

Exhibit 9-2

In 2015, the Magtag Company sold 16,000 ovens. Magtag estimated that 14% of the machines would require repairs under the two-year assurance-type warranty at an average cost of $60. During 2015, Magtag had an actual outlay of

$62,000 for repairs under warranty. Magtag uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-2. What amount should the company report for estimated liability under warranties at the end of 2015?

A) $72,400

B) $62,000

C) $48,000

D) $84,000

In 2015, the Magtag Company sold 16,000 ovens. Magtag estimated that 14% of the machines would require repairs under the two-year assurance-type warranty at an average cost of $60. During 2015, Magtag had an actual outlay of

$62,000 for repairs under warranty. Magtag uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-2. What amount should the company report for estimated liability under warranties at the end of 2015?

A) $72,400

B) $62,000

C) $48,000

D) $84,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

50

GAAP relating to compensated absences

A) applies to items such as vacation pay, severance pay, sick pay, and other long-term fringe benefits.

B) establishes the same accruing standards for vacation pay, holiday pay, and sick pay.

C) requires the use of current pay rates to accrue for compensated absences.

D) does not require the accrual of accumulated nonvested sick pay.

A) applies to items such as vacation pay, severance pay, sick pay, and other long-term fringe benefits.

B) establishes the same accruing standards for vacation pay, holiday pay, and sick pay.

C) requires the use of current pay rates to accrue for compensated absences.

D) does not require the accrual of accumulated nonvested sick pay.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

51

Lucas Company provides a bonus compensation plan under which key employees receive bonuses equal to 10% of Lucas's income after deducting income taxes but before deducting the bonus. If income before income tax and the bonus is $400,000 and the income tax rate is 30%, the bonuses should total

A) $27,160.

B) $28,866.

C) $36,400.

D) $40,000.

A) $27,160.

B) $28,866.

C) $36,400.

D) $40,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

52

Sick pay benefits that are related to an employee's services already rendered, whose payment is probable and whose amount can reasonably be estimated, must be accrued and recognized as a current liability if the obligation relates to rights that

A) I

B) II

C) III

D) IV

A) I

B) II

C) III

D) IV

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

53

Which payroll tax is imposed on both the employee and the employer?

A) federal income tax

B) state unemployment tax

C) FICA tax

D) federal unemployment tax

A) federal income tax

B) state unemployment tax

C) FICA tax

D) federal unemployment tax

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

54

Cunningham, a branch manager, is allowed a bonus of 10% of income after bonus and tax. If the tax rate is 30% and income before bonus and tax is $200,000, what is Mr. Cunningham's bonus?

A) $13,084

B) $14,000

C) $14,433

D) $20,000

A) $13,084

B) $14,000

C) $14,433

D) $20,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

55

King Sales sells a certain product for $20,000. Included in this price is an implied service-type warranty of $600. Fifty machines were sold in 2016. Warranty expense incurred during 2016 amounted to $35,000. Which of the following entries would King Sales probably not make in 2016?

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

56

Concerning accounting for warranties, which of the following statements is true?

A) Federal income tax regulations require companies to accrue warranty expense in the year of the sale.

B) The modified cash basis method is required for tax reporting.

C) The modified cash basis method uses a percentage of completion approach to warranty revenue recognition.

D) The modified cash basis recognizes warranty expense when cash is received on the sale.

A) Federal income tax regulations require companies to accrue warranty expense in the year of the sale.

B) The modified cash basis method is required for tax reporting.

C) The modified cash basis method uses a percentage of completion approach to warranty revenue recognition.

D) The modified cash basis recognizes warranty expense when cash is received on the sale.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

57

Unearned revenue also called deferred revenue) can occur when

A) services are provided prior to receipt of cash.

B) goods are sold on account.

C) services are provided after the receipt of cash.

D) goods are sold for cash.

A) services are provided prior to receipt of cash.

B) goods are sold on account.

C) services are provided after the receipt of cash.

D) goods are sold for cash.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

58

Voluntary payroll deductions may include all of the following except

A) charity donations.

B) 401K deductions.

C) group health insurance.

D) FICA taxes.

A) charity donations.

B) 401K deductions.

C) group health insurance.

D) FICA taxes.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

59

Candy's Video includes the amount of sales taxes collected directly in the price charged for merchandise, and the total amount is credited to Sales. During January, Sales was credited for $310,117.50. The January 31 adjusting entry to account for a 5% state sales tax should be

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

60

Jennifer Cakes places a coupon in each box of its product. Customers may send in five coupons and $3, and the company will send them a recipe book. Sufficient books were purchased at a cost of $5 each. A total of 400,000 boxes of product were sold in 2016. It was estimated that 6% of the coupons would be redeemed. During 2016, 8,000 coupons were redeemed. Which entry should be made at December 31, 2016?

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following contingencies is usually accrued?

A) risk of loss from fire

B) expected proceeds from insurance settlement

C) bad debts

D) discovery of possible mineral reserves on company property

A) risk of loss from fire

B) expected proceeds from insurance settlement

C) bad debts

D) discovery of possible mineral reserves on company property

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

62

Barlo Lunch Snacks places a coupon in each box of its cracker product. Customers may send in five coupons and $3, and the company will send them a recipe book. Sufficient books were purchased at a cost of $5 each. A total of 500,000 boxes of product were sold in 2016. It was estimated that 4% of the coupons would be redeemed. During 2016, 9,000 coupons were redeemed. What is Barlo's premium expense for 2016?

A) $4,400

B) $8,000

C) $20,000

D) $40,000

A) $4,400

B) $8,000

C) $20,000

D) $40,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

63

A probable loss contingency is reasonably estimated within a range of possible amounts. No amount within the range is a better estimate than any other amount within the range. The amount that should be accrued should be

A) zero.

B) the lower amount of the range.

C) the upper amount of the range.

D) the average amount within the range.

A) zero.

B) the lower amount of the range.

C) the upper amount of the range.

D) the average amount within the range.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

64

A gain contingency that is reasonably possible and for which the amount can be reasonably estimated should be

A) accrued.

B) disclosed but not accrued.

C) neither accrued nor disclosed.

D) classified as an appropriation of retained earnings.

A) accrued.

B) disclosed but not accrued.

C) neither accrued nor disclosed.

D) classified as an appropriation of retained earnings.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

65

The Park Company is affected by the following contingencies at the end of 2016:

1) Expropriation of Park's foreign assets, valued at $3,000,000, appears reasonably possible.

2) Parks' legal counsel has concluded that it is probable that the company will be required to pay damages of $500,000 in a lawsuit.

3) It appears remotely possible that a major customer will be unable to repay Parks on a note receivable for $100,000.

4) Parks' controller estimates that $250,000 of the company's pledged receivables are likely to be uncollectible, and the lender will require Parks to honor the amounts.

What total amount should Parks accrue for loss contingencies in 2016?

A) $750,000

B) $850,000

C) $3,500,000

D) $3,850,000

1) Expropriation of Park's foreign assets, valued at $3,000,000, appears reasonably possible.

2) Parks' legal counsel has concluded that it is probable that the company will be required to pay damages of $500,000 in a lawsuit.

3) It appears remotely possible that a major customer will be unable to repay Parks on a note receivable for $100,000.

4) Parks' controller estimates that $250,000 of the company's pledged receivables are likely to be uncollectible, and the lender will require Parks to honor the amounts.

What total amount should Parks accrue for loss contingencies in 2016?

A) $750,000

B) $850,000

C) $3,500,000

D) $3,850,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

66

Albert Corp. introduced a new machine on January 1, 2016. The machine carried a two-year assurance-type warranty against defects. The estimated warranty costs related to dollar sales were 3% in the year of sale and 5% in the year after sale. Additional information follows: Actual Warranty If the company uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale, what amount relating to warranty expense should be reflected on the December 31, 2017 income statement?

A) $2,200

B) $4,800

C) $5,200

D) $7,400

If the company uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale, what amount relating to warranty expense should be reflected on the December 31, 2017 income statement?A) $2,200

B) $4,800

C) $5,200

D) $7,400

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

67

The Salty Chip Company includes one coupon having no expiration date with its deluxe snack pack. Upon return of 10 coupons, Salty Chip will send a silver chip clip, which costs Salty Chip $1.50 each. Past experience indicates that 30% of coupons issued will be redeemed. Salty Chip began this promotion in 2015 and sold 1,000,000 deluxe snack packs. During 2015, 90,000 coupons were received and 9,000 chip clips were distributed to customers. The December 31, 2015 balance sheet should include a liability for coupons outstanding of

A) $18,000.

B) $180,000.

C) $31,500.

D) $50,000.

A) $18,000.

B) $180,000.

C) $31,500.

D) $50,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

68

The modified cash basis to determine warranty expense

A) violates the matching concept.

B) requires recognition in the period of sale of the estimated warranty expense and warranty liability.

C) separates accounting for two components of the sales price: the price of the product and the price of the warranty.

D) records warranty expense when the merchandise under warranty is sold.

A) violates the matching concept.

B) requires recognition in the period of sale of the estimated warranty expense and warranty liability.

C) separates accounting for two components of the sales price: the price of the product and the price of the warranty.

D) records warranty expense when the merchandise under warranty is sold.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

69

Exhibit 9-4

During 2016, the Thomas Company began selling a new type of machine that carries a two-year assurance-type warranty against all defects. Based on past industry and company experience, estimated warranty costs should total

$2,000 per machine sold. During 2016, sales and actual warranty expenditures were $4,000,000 80 machines) and

$44,000, respectively. Thomas uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-4. What amount should Thomas report as its warranty expense for 2016?

A) $0

B) $ 44,000

C) $160,000

D) $320,000

During 2016, the Thomas Company began selling a new type of machine that carries a two-year assurance-type warranty against all defects. Based on past industry and company experience, estimated warranty costs should total

$2,000 per machine sold. During 2016, sales and actual warranty expenditures were $4,000,000 80 machines) and

$44,000, respectively. Thomas uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-4. What amount should Thomas report as its warranty expense for 2016?

A) $0

B) $ 44,000

C) $160,000

D) $320,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

70

Concerning accounting for warranties, which of the following statements is false?

A) The GAAP approach of accruing warranty expense and the related liability) in the year of the sale is not an acceptable method for federal income tax purposes.

B) The modified cash basis is the most conceptually sound method for financial reporting.

C) In accounting for service-type warranties, companies much report warranty expense in the period of sale.

D) The modified cash basis recognizes warranty expense when cash is paid for the repairs to merchandise under warranty.

A) The GAAP approach of accruing warranty expense and the related liability) in the year of the sale is not an acceptable method for federal income tax purposes.

B) The modified cash basis is the most conceptually sound method for financial reporting.

C) In accounting for service-type warranties, companies much report warranty expense in the period of sale.

D) The modified cash basis recognizes warranty expense when cash is paid for the repairs to merchandise under warranty.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

71

Exhibit 9-3

John Company includes three coupons in each package of cookies it sells. In exchange for 20 coupons, a customer will receive a cookie sheet. John estimates that 30% of the coupons will be redeemed. In 2016, John sold 4,000,000 boxes of cookies and purchased 150,000 Cookie sheets at $2.50 each. During the year, 970,000 coupons were redeemed.

Refer to Exhibit 9-3. What amount should John record as premium expense for 2016?

A) $121,250

B) $450,000

C) $375,000

D) $500,000

John Company includes three coupons in each package of cookies it sells. In exchange for 20 coupons, a customer will receive a cookie sheet. John estimates that 30% of the coupons will be redeemed. In 2016, John sold 4,000,000 boxes of cookies and purchased 150,000 Cookie sheets at $2.50 each. During the year, 970,000 coupons were redeemed.

Refer to Exhibit 9-3. What amount should John record as premium expense for 2016?

A) $121,250

B) $450,000

C) $375,000

D) $500,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

72

Gain contingencies should

A) be accrued if they are probable and can be reasonably estimated.

B) not be accrued in the accounts.

C) be accrued only if they are the result of litigation or government appropriation.

D) never be accrued or disclosed in the footnotes.

A) be accrued if they are probable and can be reasonably estimated.

B) not be accrued in the accounts.

C) be accrued only if they are the result of litigation or government appropriation.

D) never be accrued or disclosed in the footnotes.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following loss contingencies is not usually accrued?

A) product warranty obligations

B) premium offer obligations

C) risk of loss from fire

D) noncollectibility of receivables

A) product warranty obligations

B) premium offer obligations

C) risk of loss from fire

D) noncollectibility of receivables

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

74

Exhibit 9-4

During 2016, the Thomas Company began selling a new type of machine that carries a two-year assurance-type warranty against all defects. Based on past industry and company experience, estimated warranty costs should total

$2,000 per machine sold. During 2016, sales and actual warranty expenditures were $4,000,000 80 machines) and

$44,000, respectively. Thomas uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-4. What amount should Thomas report as its estimated warranty liability at December 31, 2016?

A) $0

B) $44,000

C) $120,000

D) $116,000

During 2016, the Thomas Company began selling a new type of machine that carries a two-year assurance-type warranty against all defects. Based on past industry and company experience, estimated warranty costs should total

$2,000 per machine sold. During 2016, sales and actual warranty expenditures were $4,000,000 80 machines) and

$44,000, respectively. Thomas uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale.

Refer to Exhibit 9-4. What amount should Thomas report as its estimated warranty liability at December 31, 2016?

A) $0

B) $44,000

C) $120,000

D) $116,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

75

Exhibit 9-3

John Company includes three coupons in each package of cookies it sells. In exchange for 20 coupons, a customer will receive a cookie sheet. John estimates that 30% of the coupons will be redeemed. In 2016, John sold 4,000,000 boxes of cookies and purchased 150,000 Cookie sheets at $2.50 each. During the year, 970,000 coupons were redeemed.

Refer to Exhibit 9-3. What amount should John report as estimated premium claims outstanding at December 31, 2016?

A) $121,250

B) $328,750

C) $450,000

D) $500,000

John Company includes three coupons in each package of cookies it sells. In exchange for 20 coupons, a customer will receive a cookie sheet. John estimates that 30% of the coupons will be redeemed. In 2016, John sold 4,000,000 boxes of cookies and purchased 150,000 Cookie sheets at $2.50 each. During the year, 970,000 coupons were redeemed.

Refer to Exhibit 9-3. What amount should John report as estimated premium claims outstanding at December 31, 2016?

A) $121,250

B) $328,750

C) $450,000

D) $500,000

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

76

The FASB established the use of the terms "probable," "reasonably possible," and "remote." It adopted these terms because

A) the available statistical techniques are not exact enough.

B) the likelihood of occurrence of future events can vary over a wide range.

C) future gains are not easy to estimate.

D) unnecessary estimates should not be recorded in the financial records.

A) the available statistical techniques are not exact enough.

B) the likelihood of occurrence of future events can vary over a wide range.

C) future gains are not easy to estimate.

D) unnecessary estimates should not be recorded in the financial records.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

77

Exhibit 9-5

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of expenditures for warranty costs for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of expenditures for warranty costs for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

78

When a contingency must be accrued under IFRS, the charge is referred to as

A) an endowment.

B) a provision.

C) an appropriation.

D) a risk expense.

A) an endowment.

B) a provision.

C) an appropriation.

D) a risk expense.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

79

Which of the following statements is true?

A) No loss contingencies should be disclosed if there is just a reasonable possibility of a loss.

B) Indirect guarantees should normally be accrued.

C) In the case of loss contingencies, accrual can be made even if the exact payee and payment date are not known.

D) Losses may be accrued for unasserted claims and other potential unfiled lawsuits.

A) No loss contingencies should be disclosed if there is just a reasonable possibility of a loss.

B) Indirect guarantees should normally be accrued.

C) In the case of loss contingencies, accrual can be made even if the exact payee and payment date are not known.

D) Losses may be accrued for unasserted claims and other potential unfiled lawsuits.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

80

Exhibit 9-5

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of warranty expense for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Backhoe Company estimates its annual warranty costs to be 4% of annual net sales. Backhoe uses the GAAP approach of accruing warranty expense and the related liability) in the year of the sale. The following information relates to the calendar year 2015:

Refer to Exhibit 9-5. The amount of warranty expense for 2015 is

A) $80,000.

B) $120,000.

C) $140,000.

D) $240,000.

Unlock Deck

Unlock for access to all 125 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 125 flashcards in this deck.