Deck 14: Auditing the Revenue Cycle

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

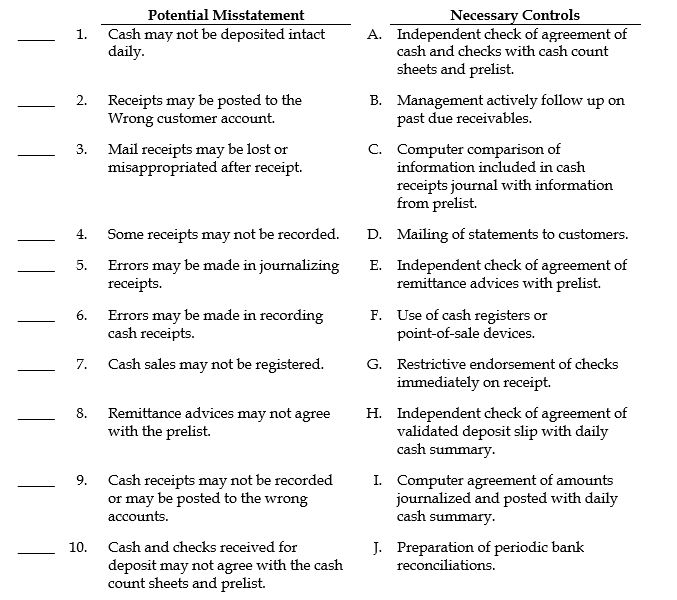

Following are a number of potential misstatements that might occur in the revenue cycle. Also listed are a number of necessary controls for this cycle.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

Question

Question

Question

Question

Question

Question

Question

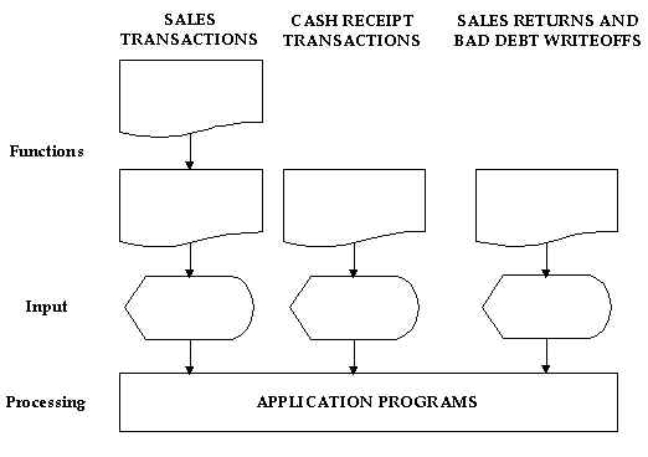

Shown below is a partial flowchart of the overview of computerized accounting operations in the revenue cycle.

REQUIRED: Label the symbols in the partial flowchart.

REQUIRED: Label the symbols in the partial flowchart.

REQUIRED: Label the symbols in the partial flowchart. Question

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/71

Play

Full screen (f)

Deck 14: Auditing the Revenue Cycle

1

The sales transaction file is a computer file of pending sales transactions.

False

2

If receivables are growing faster than sales, it may be an indication that the company is accomplishing sales growth by taking on increased credit risk.

True

3

Credit approval is given by the credit department in accordance with management's credit policies and authorized credit limits for each customer.

True

4

Cash collection may precede revenue recognition, resulting in earned revenues.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

5

The accounts receivable generated by credit sales transactions are nearly always material to the balance sheet.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

6

The misappropriation of cash could be concealed by an employee who correspondingly understates cash discounts.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

7

Inherent risk tends to be low in the revenue cycle.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

8

Once an entity sells its receivables, it no longer needs to keep a documentary record of receivables that have been sold.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

9

Proper access controls over cash require that all cash receipts be deposited intact daily, less minor disbursements made from the receipts.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

10

In comparing Accounts Receivable Growth to Sales Growth, ratios larger than 1.0 indicate that receivables are growing faster than sales.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

11

The sales invoice is a report sent to each customer showing the beginning balance, transactions, and the month's ending balance.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

12

Controls over approving credit will enable management to make a more reliable estimate of the size of Allowance for Uncollectible Accounts needed. This control relates to the completeness assertion.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

13

In comparing Uncollectible Accounts Expense to Accounts Receivable Write-offs, smaller ratios may indicate an inadequate estimation process.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

14

The auditor may use generalized audit software to perform sequence checks and print lists of sales invoices whose numbers are missing.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

15

In most cases there is a lesser risk of overstatement of receivables and sales than of understatement of receivables and sales.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

16

It is generally more effective to evaluate total revenues against a measure of business activity than comparing current revenues with prior-year revenues.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

17

Periodic bank reconciliations should be performed by an employee who is usually involved in executing or recording cash transactions.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

18

Delivery of goods or services is the economic event that represents change in title and establishes the right to a receivable.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

19

Virtually every company that requires an audit has a computerized accounting system.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

20

Monitoring provides management with feedback as to whether external control pertaining to revenue cycle transactions and balances are operating as intended.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

21

An auditor who does not request confirmation of receivables should document in the working papers how he or she overcame the presumption that confirmations should be requested.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

22

The possibility that an unusually heavy volume of sales returns after year-end could signal unauthorized shipments before year-end to inflate recorded sales and receivables.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

23

The audit report should indicate each account selected for confirmation, the results obtained from each request, and cross-references to the actual confirmation responses.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

24

A review of the accounts receivable trial balance may reveal receivables with credit balances that should be reclassified as current liabilities.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

25

When numerous exceptions are found, or insufficient responses are received from confirmation requests and the auditor is unable to obtain sufficient competent evidence from other substantive tests, he or she can still issue a standard auditor's report.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

26

The blank form confirmation is a way of increasing the response rate on positive confirmations.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

27

A negative confirmation is requested to be returned only if there is an error.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

28

In most cases there is a lesser risk of overstatement of receivables and sales than of understatement of receivables and sales.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

29

In the area of accounts receivable, it is normal to find a high assessment of inherent risk for the existence or occurrence assertion and for the valuation or allocation assertion.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

30

When confirmations are returned, any material differences should be investigated by the auditor.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

31

The allowance for uncollectible accounts is an accounting estimate made by management that involves both objective and subjective considerations.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

32

The sales cutoff test is made as of the balance sheet date.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

33

The auditor must be knowledgeable about the statement presentation and disclosure requirements for accounts receivable and sales under GAAP.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

34

Confirmations are usually returned directly to the client.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

35

The confirmation of accounts receivable is primarily aimed at the existence or occurrence assertion.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

36

In the process of performing the audit the auditor may benchmark company performance against others in the industry.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

37

It is necessary to confirm the pledging of receivables with customers.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

38

Since the confirmation is a request for payment, it provides strong evidence as to the collectibility of the balance.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

39

In considering the amount to write-off of past-due amounts, the auditor will pay particular attention to customers that demonstrate deteriorating payment history as the year progressed.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

40

Confirming accounts receivable is a generally accepted auditing standard.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

41

To enhance controls in the credit sales area, the warehouse should be instructed not to release goods until:

A) they communicate directly with the customer.

B) they have a completed sales invoice.

C) they receive an approved sales order.

D) the shipping department requests the goods.

E) they received a faxed copy of the sales requisition.

A) they communicate directly with the customer.

B) they have a completed sales invoice.

C) they receive an approved sales order.

D) the shipping department requests the goods.

E) they received a faxed copy of the sales requisition.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

42

A company policy states that annual vacations are mandatory for all employees. This policy is most important for employees who:

A) are not bonded.

B) handle cash receipts.

C) maintain the detailed accounting records.

D) have access to the general ledger.

E) serve as inventory clerks.

A) are not bonded.

B) handle cash receipts.

C) maintain the detailed accounting records.

D) have access to the general ledger.

E) serve as inventory clerks.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

43

The audit objective, "The accounts receivable balance represents gross claims on customers and agrees with the sum of the accounts receivable subsidiary ledger" is derived from the assertion of:

A) existence or occurrence.

B) completeness.

C) rights and obligations.

D) valuation or allocation.

E) presentation or disclosure.

A) existence or occurrence.

B) completeness.

C) rights and obligations.

D) valuation or allocation.

E) presentation or disclosure.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following forms may serve as the bill of lading?

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

45

Use of modern point-of-sale terminals to record over-the-counter cash sales provides all of the following except:

A) an immediate visual display for the customer to verify the accuracy of price and cash tendered.

B) a printed receipt for the customer.

C) an internal record of the transaction on a computer file or tape locked inside the terminal/register.

D) assurance that all cash sales are processed through the system.

E) printed control totals of the day's receipts processed on the device.

A) an immediate visual display for the customer to verify the accuracy of price and cash tendered.

B) a printed receipt for the customer.

C) an internal record of the transaction on a computer file or tape locked inside the terminal/register.

D) assurance that all cash sales are processed through the system.

E) printed control totals of the day's receipts processed on the device.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

46

The bonding of employees will normally be expected to:

A) "weed out" dishonest employees already hired.

B) eliminate the need for separation of duties in the cash receipts area.

C) guarantee that all employee fraud will be prevented.

D) provide reasonable assurance that all employees will perform their jobs with the utmost integrity.

E) serve as a deterrent to dishonesty.

A) "weed out" dishonest employees already hired.

B) eliminate the need for separation of duties in the cash receipts area.

C) guarantee that all employee fraud will be prevented.

D) provide reasonable assurance that all employees will perform their jobs with the utmost integrity.

E) serve as a deterrent to dishonesty.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following accounts in a merchandising company is affected by both the revenue cycle and another cycle?

A) sales

B) sales returns and allowances

C) inventory

D) accounts receivable

E) accounts payable

A) sales

B) sales returns and allowances

C) inventory

D) accounts receivable

E) accounts payable

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is not normally considered a step in the credit sales functions?

A) accepting customer orders

B) approving credit

C) shipping the sales orders

D) acquiring goods to fill the order

E) billing customers

A) accepting customer orders

B) approving credit

C) shipping the sales orders

D) acquiring goods to fill the order

E) billing customers

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

49

Auditors should evaluate new controls associated with all of the following except:

A) new product lines

B) new sources of revenues

C) management's response to new accounting standards for revenue transactions

D) related changes in personnel

E) all of the above

A) new product lines

B) new sources of revenues

C) management's response to new accounting standards for revenue transactions

D) related changes in personnel

E) all of the above

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

50

After making the deposit, the daily cash summary and the validated deposit slip should be forwarded by the cashier directly to:

A) the treasurer.

B) the accounts receivable clerk.

C) general accounting.

D) the billing department.

E) the cash receipts clerk.

A) the treasurer.

B) the accounts receivable clerk.

C) general accounting.

D) the billing department.

E) the cash receipts clerk.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

51

In a credit-merchandising environment, which of the following documents usually initiates the activity in the sales cycle?

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

52

An understanding of the revenue accounting system requires knowledge of all of the following except:

A) how sales are initiated

B) how goods and services are delivered

C) how payables are recorded

D) how cash is received

E) how sales adjustments are made

A) how sales are initiated

B) how goods and services are delivered

C) how payables are recorded

D) how cash is received

E) how sales adjustments are made

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

53

In a credit merchandising organization, the best place to vest credit approval is in:

A) accounts receivable.

B) the sales department.

C) a completely separate department.

D) the cashier area where receipts will eventually be sent.

E) the collections department.

A) accounts receivable.

B) the sales department.

C) a completely separate department.

D) the cashier area where receipts will eventually be sent.

E) the collections department.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

54

Standard control procedures over customer remittances received through the mail include having the mailroom personnel:

A) forward the remittances, unopened, directly to the cashier.

B) open the mail, restrictively endorse the checks, and then list each remittance on a multicopy prelist.

C) forward the remittances, unopened, directly to the accounts receivable clerk.

D) open the mail, restrictively endorse the checks, then forward the remittances directly to the cashier.

E) open the mail, restrictively endorse the checks, then forward the remittances directly to the accounts receivable clerk.

A) forward the remittances, unopened, directly to the cashier.

B) open the mail, restrictively endorse the checks, and then list each remittance on a multicopy prelist.

C) forward the remittances, unopened, directly to the accounts receivable clerk.

D) open the mail, restrictively endorse the checks, then forward the remittances directly to the cashier.

E) open the mail, restrictively endorse the checks, then forward the remittances directly to the accounts receivable clerk.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

55

A company has a policy of rotating employees' assigned duties. This policy is most important for employees who:

A) are not bonded.

B) maintain the detailed accounting records.

C) handle cash receipts.

D) have access to the general ledger.

E) serve as inventory clerks.

A) are not bonded.

B) maintain the detailed accounting records.

C) handle cash receipts.

D) have access to the general ledger.

E) serve as inventory clerks.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

56

Controls designed to reduce the risk of omissions, duplications, incorrect pricing, and other types of errors in the billing process include all of the following except:

A) comparison of control totals for shipping documents with corresponding totals for sales invoices.

B) computer matching of sales invoice information with purchase order information.

C) computer matching of sales invoice information with sales order and shipping information.

D) computer-programmed checks on the mathematical accuracy of sales invoices.

E) computer matching of sales prices with an authorized price list and sales order prices in preparing the sales invoices.

A) comparison of control totals for shipping documents with corresponding totals for sales invoices.

B) computer matching of sales invoice information with purchase order information.

C) computer matching of sales invoice information with sales order and shipping information.

D) computer-programmed checks on the mathematical accuracy of sales invoices.

E) computer matching of sales prices with an authorized price list and sales order prices in preparing the sales invoices.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

57

The use of a lockbox system enhances controls over cash receipts because the post office box is directly controlled by the:

A) mailroom staff.

B) internal audit department.

C) treasurer.

D) chief financial officer.

E) company's bank.

A) mailroom staff.

B) internal audit department.

C) treasurer.

D) chief financial officer.

E) company's bank.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

58

In a credit-merchandising environment, which of the following documents serves as the basis for internal processing of an order?

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

59

In general, the first department to use the "approved customer list" as an order passes through the credit sales system will be the:

A) credit department.

B) shipping department.

C) billing department.

D) collections department.

E) sales order department.

A) credit department.

B) shipping department.

C) billing department.

D) collections department.

E) sales order department.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

60

In a credit-merchandising environment, when a customer has been "billed," it means which of the following documents has been prepared?

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

A) shipping document

B) customer order

C) material requisition

D) sales invoice

E) sales order

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

61

Following are a number of potential misstatements that might occur in the revenue cycle. Also listed are a number of necessary controls for this cycle.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

62

When the positive form of accounts receivable confirmation is used and no response is received, the auditor should normally:

A) assume the account is in error.

B) assume the account is correct.

C) send a second request.

D) send a negative confirmation.

E) contact the customer by telephone.

A) assume the account is in error.

B) assume the account is correct.

C) send a second request.

D) send a negative confirmation.

E) contact the customer by telephone.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

63

Important documents and records used in processing sales adjustments include all of the following except:

A) sales return authorization

B) receiving report

C) debit memo

D) authorization for accounts receivable write-off

E) journal entry

A) sales return authorization

B) receiving report

C) debit memo

D) authorization for accounts receivable write-off

E) journal entry

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

64

For each of the following computer controls identify the related potential misstatement.

1.The computer accounts for all goods shipped but not billed.

2.The computer matches the customer number on the sales invoice with the customer number on the sales order.

3.The computer matches the customer on the sales order with the customer master file.

4.The computer matches sales prices with the authorized price list and the sales order.

5.The computer matches the amount of the sales order with the credit authorization on the customer master file.

6.The computer matches the sales invoice information with underlying shipping information.

7.The computer matches all goods pulled from the inventory (perpetual) to the approved sales order.

8.The computer compares the invoice date with the accounting period when the goods were shipped.

9.The computer matches prenumbered shipping documents with the approved sales for each shipment.

10.The computer prints a report of all unfilled sales orders.

1.The computer accounts for all goods shipped but not billed.

2.The computer matches the customer number on the sales invoice with the customer number on the sales order.

3.The computer matches the customer on the sales order with the customer master file.

4.The computer matches sales prices with the authorized price list and the sales order.

5.The computer matches the amount of the sales order with the credit authorization on the customer master file.

6.The computer matches the sales invoice information with underlying shipping information.

7.The computer matches all goods pulled from the inventory (perpetual) to the approved sales order.

8.The computer compares the invoice date with the accounting period when the goods were shipped.

9.The computer matches prenumbered shipping documents with the approved sales for each shipment.

10.The computer prints a report of all unfilled sales orders.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

65

The test of balances to evaluate the adequacy of the allowance for uncollectible accounts does not involve which of the following?

A) footing and crossfooting the aged trial balance of accounts receivable and agreeing the total to the general ledger balance

B) considering evidence concerning the collectibility of past due amounts

C) testing the aging of the amounts shown in the aging categories on the aged trial balance

D) considering evidence concerning the collectibility of current amounts

E) assessing the reasonableness of the percentages used to compute the allowance component required for each aging category and the adequacy of the overall allowance

A) footing and crossfooting the aged trial balance of accounts receivable and agreeing the total to the general ledger balance

B) considering evidence concerning the collectibility of past due amounts

C) testing the aging of the amounts shown in the aging categories on the aged trial balance

D) considering evidence concerning the collectibility of current amounts

E) assessing the reasonableness of the percentages used to compute the allowance component required for each aging category and the adequacy of the overall allowance

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

66

The summary of the results from confirming accounts receivable contained in the auditor's working papers would not normally provide statistical data on the:

A) market value of the confirmation sample.

B) number of confirmations sent and responses received.

C) proportion of the population total covered by the sample.

D) relationship between the audited and book values of items included in the sample.

E) dollar value of confirmations sent.

A) market value of the confirmation sample.

B) number of confirmations sent and responses received.

C) proportion of the population total covered by the sample.

D) relationship between the audited and book values of items included in the sample.

E) dollar value of confirmations sent.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

67

In the processing of accounts receivable confirmations, the auditor would not normally be expected to:

A) agree the information to the corresponding customer's account.

B) personally deposit the requests in the mail.

C) include his/her own return address envelope.

D) maintain custody of the confirmations until they are mailed.

E) personally prepare the confirmations.

A) agree the information to the corresponding customer's account.

B) personally deposit the requests in the mail.

C) include his/her own return address envelope.

D) maintain custody of the confirmations until they are mailed.

E) personally prepare the confirmations.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

68

Shown below is a partial flowchart of the overview of computerized accounting operations in the revenue cycle.

REQUIRED: Label the symbols in the partial flowchart.

REQUIRED: Label the symbols in the partial flowchart. Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

69

In most merchandising firm audits, the auditor's concern over sales adjustment transactions is based upon the:

A) sheer number and value of these transactions.

B) implication these transactions have for operating efficiency.

C) poor controls normally found over these transactions and the inherent lack of documentation.

D) lack of proper authorization for these transactions.

E) potential use of these transactions to conceal a theft of cash.

A) sheer number and value of these transactions.

B) implication these transactions have for operating efficiency.

C) poor controls normally found over these transactions and the inherent lack of documentation.

D) lack of proper authorization for these transactions.

E) potential use of these transactions to conceal a theft of cash.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

70

In understanding the client's business and industry, briefly describe the sales and collection process for a (1) household appliance manufacturer and (2) manufacturer of electronic computers.

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

72

Match between columns

Unlock Deck

Unlock for access to all 71 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 71 flashcards in this deck.