Deck 16: Auditing the Production and

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

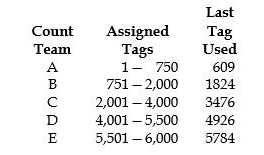

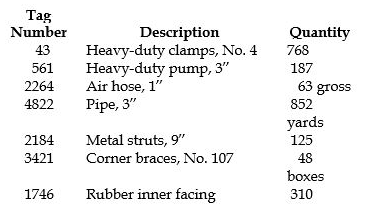

The Goren Company counts its inventory on October 31, 20X8. As a senior auditor assigned to the engagement, you observe the inventory count on this date. During the inventory observation, you encounter only minor problems, which are cleared up, to your satisfaction. On November 15, 20X8, the controller for the Goren Company informs you that the inventory summary sheets are complete and gives you a copy, part of which is reproduced here: During the inventory observation, you recorded the following inventory tag control information in your working papers:

During the inventory observation, you recorded the following test counts in your working papers:

REQUIRED: List the tag numbers identified above on your answer sheet. If you believe the information pertaining to the tag number is correct, so state. If you believe the information is incorrect, describe the error. The information you recorded during your test counts, of course, was accurate.

During the inventory observation, you recorded the following test counts in your working papers:

REQUIRED: List the tag numbers identified above on your answer sheet. If you believe the information pertaining to the tag number is correct, so state. If you believe the information is incorrect, describe the error. The information you recorded during your test counts, of course, was accurate.

Question

Question

Question

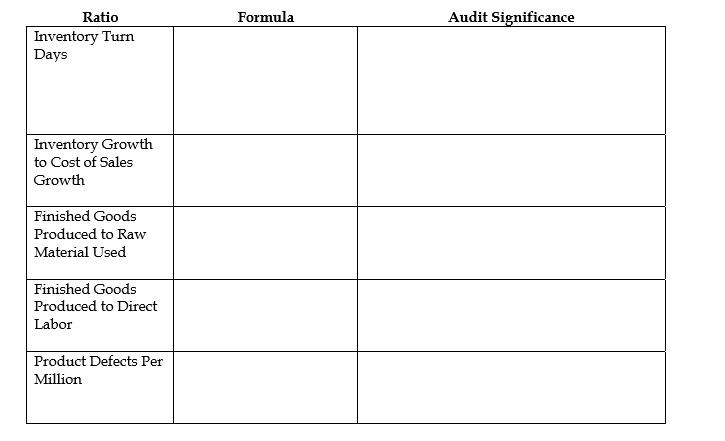

For each one of the following financial ratios, indicate the formula and identify the audit significance.

Question

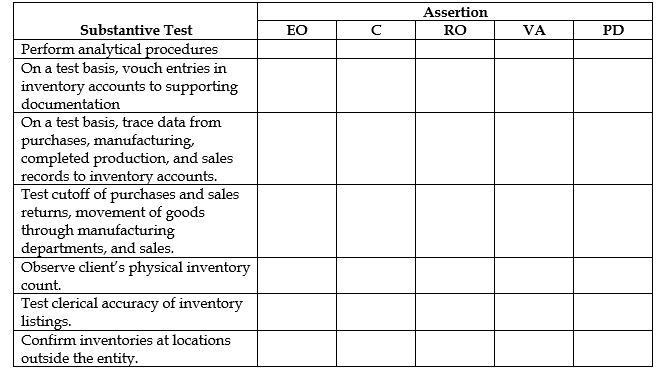

Place an "X" in the applicable column for each substantive test to identify the assertions to which each test pertains.

Question

Question

Question

Question

Question

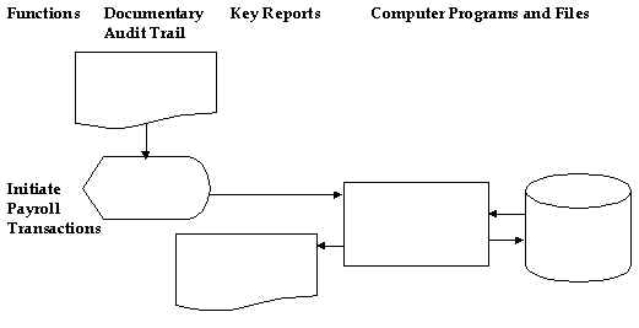

Shown below is a partial system flowchart of payroll transactions.

REQUIRED: Label the symbols in the partial system flowchart.

REQUIRED: Label the symbols in the partial system flowchart.

Question

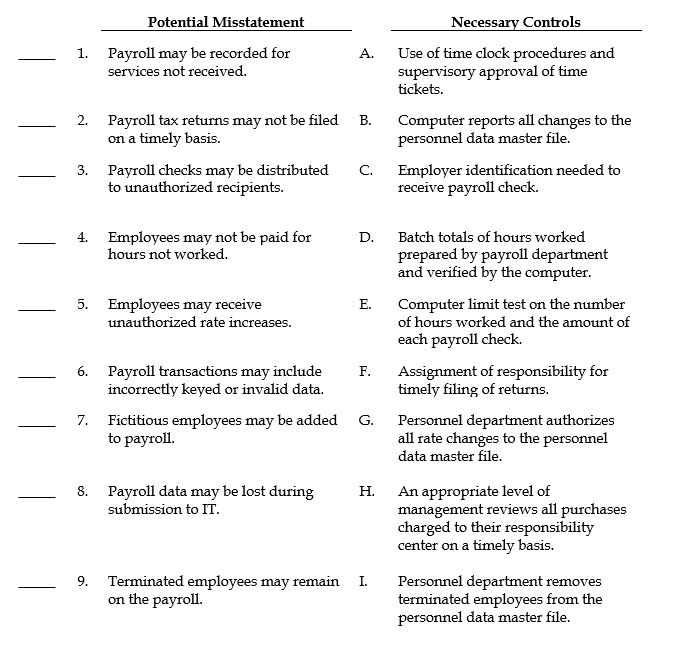

Following are a number of potential misstatements that might occur in the personnel services cycle. Also listed are a number of necessary controls for this cycle.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

Question

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/79

Play

Full screen (f)

Deck 16: Auditing the Production and

1

The production cycle interfaces with the expenditure, personnel services, and revenue cycles.

True

2

The computer file that contains each employee's gross earnings, payroll deductions, and net pay for the year-to-date by pay periods is the employee personnel file.

False

3

The auditor normally performs analytical procedures early in the audit of the personnel services cycle because they are cost effective.

True

4

Generally Accepted Auditing Standards require the auditor to supervise the taking of the client's physical inventory.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

5

In making test counts of inventory items, the auditor should record the count and give a complete and accurate description of the item in the working papers.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

6

The hiring of employees should be done in the payroll department.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

7

Payroll fraud is not a major concern for the auditor.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

8

A move ticket is a written authorization from a production department for stores to release materials for use on an approved production order.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

9

In automated systems, payroll is frequently processed using a batch approach.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

10

Observation of inventory does not provide evidence for rights and obligations.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

11

When a significant proportion of inventories is stored in a public warehouse, the auditor may not be satisfied with its existence by merely obtaining a confirmation from the warehouseman.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

12

The personnel services cycle is included in the expenditure cycle.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

13

It is customary to identify the major inventory categories in the balance sheet and the cost of goods sold in the income statement.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

14

The auditor need not inquire of management as to any goods held on consignment.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

15

When standard costs are used for manufactured inventories, the auditor's tests should include comparison of the standards with engineering specifications.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

16

When the lower of cost or market rule is used to value inventory, only the lower value need be verified.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

17

The proper use of statistical sampling may make it possible for the client to eliminate the need to count every item in the inventory on an annual basis.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

18

To express an unqualified opinion on the balance sheet, the auditor must observe the beginning and ending inventories.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

19

The auditor should review and evaluate the client's inventory-taking plans during the observation of the inventory.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

20

A clock card is used to show the hours worked, while the time ticket is used to show the specific jobs worked on during those hours.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

21

With a manufacturer, wholesaler, or retailer, however, inherent risk for inventory may be assessed at or near the maximum level for all of the following reasons except:

A) inventories are often stored at multiple sites, adding to the difficulties associated with maintaining physical controls over theft and damages, and properly accounting for goods in transit between sites.

B) the wide diversity of inventory items may present special problems in determining their quality and market value.

C) inventories are vulnerable to spoilage, obsolescence, and other factors such as general economic conditions that may affect demand and salability, and thus the proper valuation of the inventories.

D) inventory may be sold subject to right of return and repurchase agreements.

E) the volume of purchases, manufacturing, and sales transactions that affects these accounts is generally high, decreasing the opportunities for misstatements to occur.

A) inventories are often stored at multiple sites, adding to the difficulties associated with maintaining physical controls over theft and damages, and properly accounting for goods in transit between sites.

B) the wide diversity of inventory items may present special problems in determining their quality and market value.

C) inventories are vulnerable to spoilage, obsolescence, and other factors such as general economic conditions that may affect demand and salability, and thus the proper valuation of the inventories.

D) inventory may be sold subject to right of return and repurchase agreements.

E) the volume of purchases, manufacturing, and sales transactions that affects these accounts is generally high, decreasing the opportunities for misstatements to occur.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

22

The use of the computer to compare production hours to direct labor hours on daily production reports relates to the:

A) valuation or allocation assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) existence or occurrence assertion.

E) presentation or disclosure assertion.

A) valuation or allocation assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) existence or occurrence assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

23

During the observation of the inventory, the auditor has no responsibility to:

A) observe the taking of the inventory by client personnel.

B) make some test counts of inventory quantities.

C) supervise the taking of the inventory.

D) make inquiries of the client concerning the inventories.

E) watch for damaged and obsolete inventory items.

A) observe the taking of the inventory by client personnel.

B) make some test counts of inventory quantities.

C) supervise the taking of the inventory.

D) make inquiries of the client concerning the inventories.

E) watch for damaged and obsolete inventory items.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following functions is not part of the production cycle?

A) acquisition of raw materials

B) processing goods in production

C) determining and recording manufacturing costs

D) maintaining the correctness of inventory balances

E) protecting inventories

A) acquisition of raw materials

B) processing goods in production

C) determining and recording manufacturing costs

D) maintaining the correctness of inventory balances

E) protecting inventories

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

25

When inventories are material and the auditor does not observe the inventory at or near the year-end, professional standards require the auditor to:

A) thoroughly test the accounting records.

B) observe some physical counts of the inventory.

C) disclaim an opinion on the financial statements.

D) resign from the engagement.

E) reperform the entire inventory count.

A) thoroughly test the accounting records.

B) observe some physical counts of the inventory.

C) disclaim an opinion on the financial statements.

D) resign from the engagement.

E) reperform the entire inventory count.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

26

To prevent terminated employees from being paid in subsequent periods, prompt notification of employee terminations should be made by the personnel department.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

27

Which one of the following analytical procedures may indicate possible inventory obsolescence problems when ratios are large?

A) inventory turnover

B) finished goods produced to raw material used

C) inventory growth to cost of sales growth

D) finished goods produced to direct labor

E) product defects per million

A) inventory turnover

B) finished goods produced to raw material used

C) inventory growth to cost of sales growth

D) finished goods produced to direct labor

E) product defects per million

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

28

Observation of inventories is a required audit procedure whenever:

A) inventories are material.

B) inventories are material and it is practicable and reasonable.

C) it is practicable and reasonable.

D) the auditor considers it to be necessary.

E) inventories are material and the auditor considers it to be necessary.

A) inventories are material.

B) inventories are material and it is practicable and reasonable.

C) it is practicable and reasonable.

D) the auditor considers it to be necessary.

E) inventories are material and the auditor considers it to be necessary.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

29

The production cycle relates to:

A) the conversion of inventory into receivables or cash.

B) activities involving the acquisition of and payment for goods and services.

C) exchanges of goods and services with customers.

D) events and activities that pertain to executive and employee compensation.

E) the conversion of raw materials into finished goods.

A) the conversion of inventory into receivables or cash.

B) activities involving the acquisition of and payment for goods and services.

C) exchanges of goods and services with customers.

D) events and activities that pertain to executive and employee compensation.

E) the conversion of raw materials into finished goods.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

30

Most companies structure their stock option plans to meet the requirements of APB No. 25 and use the intrinsic value approach.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

31

The risk of underpayment in payroll is minimal because employees will complain when they are underpaid.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

32

Auditors are often concerned about the completeness assertion in the payroll cycle.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

33

Payroll checks should be signed by authorized personnel in the payroll department.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

34

The most significant issue associated with incentive compensation plans relates to adequate disclosures in the financial statements.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

35

When statistical sampling methods are used by the client in determining inventories, professional standards require that the auditor ascertain the following except that the:

A) sampling plan has statistical validity.

B) sampling plan has been properly applied.

C) results in terms of reliability are reasonable.

D) appropriate tests of transactions have been applied.

E) results in terms of precision are reasonable.

A) sampling plan has statistical validity.

B) sampling plan has been properly applied.

C) results in terms of reliability are reasonable.

D) appropriate tests of transactions have been applied.

E) results in terms of precision are reasonable.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

36

Observation of inventories is a required audit procedure whenever inventories are material.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

37

In companies where inventories are at multiple locations, the auditor's observations ordinarily should include:

A) all inventory locations.

B) a random sample of locations.

C) several inventory locations picked by the auditor.

D) a representative sample of locations.

E) all significant inventory locations.

A) all inventory locations.

B) a random sample of locations.

C) several inventory locations picked by the auditor.

D) a representative sample of locations.

E) all significant inventory locations.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

38

The auditor's strategy in performing test counts during the inventory observation is to:

A) concentrate tests on high dollar items and take a representative sample of other items.

B) test all high dollar items.

C) randomly select all test items.

D) concentrate tests in areas where employees seem to be disregarding the inventory instructions.

E) sequentially select all test items.

A) concentrate tests on high dollar items and take a representative sample of other items.

B) test all high dollar items.

C) randomly select all test items.

D) concentrate tests in areas where employees seem to be disregarding the inventory instructions.

E) sequentially select all test items.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

39

Defined benefit pension plans are normally subject to requirements of the Employee Retirement Income Security Act (ERISA) of 1974, which usually requires a separate audit of the pension plan.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

40

The test for terminated employees begins with the selection of termination notices.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following manufacturing functions is not an integral part of inventory production?

A) Issuing raw materials.

B) Maintaining correctness of inventory balances.

C) Processing goods in production.

D) Protecting inventories.

E) Transferring completed work to finished goods.

A) Issuing raw materials.

B) Maintaining correctness of inventory balances.

C) Processing goods in production.

D) Protecting inventories.

E) Transferring completed work to finished goods.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

42

The specific audit objective "factory labor is correctly classified as direct and indirect labor" is derived from the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

43

Reviewing data pertaining to inventory quality relates primarily to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) valuation or allocation assertion.

D) rights and obligations assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) valuation or allocation assertion.

D) rights and obligations assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

44

The taking of a physical inventory by a client is normally done according to a plan or a list of instructions. The client's instructions should include the following matters except:

A) date of the counts.

B) names of employees responsible for observing the inventory taking.

C) locations to be counted.

D) segregation or identification of goods not owned.

E) detailed instructions on how the counts are to be made.

A) date of the counts.

B) names of employees responsible for observing the inventory taking.

C) locations to be counted.

D) segregation or identification of goods not owned.

E) detailed instructions on how the counts are to be made.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

45

A company has a policy that all terminated employees must have an "exit interview" with a member of the personnel department, who documents the discussion. This control relates to the:

A) valuation or allocation assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) presentation or disclosure assertion.

E) existence or occurrence assertion.

A) valuation or allocation assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) presentation or disclosure assertion.

E) existence or occurrence assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

46

When the weekly payroll edit run rejects an item, follow-up to see that the data is corrected and resubmitted is the responsibility of the:

A) data control department.

B) timekeeping department.

C) payroll department.

D) data entry department.

E) personnel department.

A) data control department.

B) timekeeping department.

C) payroll department.

D) data entry department.

E) personnel department.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

47

Inherent risk for the valuation or allocation assertion will be high in the personnel services cycle when:

A) employee turnover is low.

B) factory workers are paid based on production.

C) payroll checks are drawn from a separate imprest bank account.

D) pay periods are weekly.

E) employee absenteeism is minimal.

A) employee turnover is low.

B) factory workers are paid based on production.

C) payroll checks are drawn from a separate imprest bank account.

D) pay periods are weekly.

E) employee absenteeism is minimal.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following accounts would not be directly affected by transactions in the personnel services cycle?

A) manufacturing overhead

B) commissions expense

C) work in process inventory

D) employee federal income taxes withheld

E) payroll taxes payable

A) manufacturing overhead

B) commissions expense

C) work in process inventory

D) employee federal income taxes withheld

E) payroll taxes payable

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

49

Payroll functions include all of the following except:

A) preparing attendance and timekeeping data.

B) terminating employees.

C) authorizing payroll changes.

D) preparing attendance data.

E) paying the payroll.

A) preparing attendance and timekeeping data.

B) terminating employees.

C) authorizing payroll changes.

D) preparing attendance data.

E) paying the payroll.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

50

Confirmation of inventories in public warehouses cannot provide evidence concerning the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) presentation or disclosure assertion.

E) valuation or allocation assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) presentation or disclosure assertion.

E) valuation or allocation assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

51

Testing the inventory pricing relates primarily to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) presentation or disclosure assertion.

E) valuation or allocation assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) presentation or disclosure assertion.

E) valuation or allocation assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

52

Completed time tickets and clock cards are sent by:

A) personnel to timekeeping.

B) payroll to timekeeping.

C) timekeeping to payroll.

D) timekeeping to personnel, which forwards them to payroll.

E) timekeeping to payroll, which forwards them to personnel.

A) personnel to timekeeping.

B) payroll to timekeeping.

C) timekeeping to payroll.

D) timekeeping to personnel, which forwards them to payroll.

E) timekeeping to payroll, which forwards them to personnel.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

53

The request for a change in job classification or a wage rate increase is usually initiated by the:

A) personnel department based on information in the personnel files.

B) employee in question.

C) employee's supervisor.

D) payroll department.

E) personnel manager.

A) personnel department based on information in the personnel files.

B) employee in question.

C) employee's supervisor.

D) payroll department.

E) personnel manager.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following is a form used by employees to record the hours worked daily during a pay period?

A) Clock card.

B) Time ticket.

C) Labor cost distribution summary.

D) Move ticket.

E) Daily production report.

A) Clock card.

B) Time ticket.

C) Labor cost distribution summary.

D) Move ticket.

E) Daily production report.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

55

The observation of inventory relates primarily to the:

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

A) existence or occurrence assertion.

B) completeness assertion.

C) rights and obligations assertion.

D) valuation or allocation assertion.

E) presentation or disclosure assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

56

A record of the disciplinary actions brought against a particular employee would most likely be found in the:

A) employee personnel file.

B) personnel data master file.

C) employee earnings master file.

D) payroll register.

E) employee earnings transaction file.

A) employee personnel file.

B) personnel data master file.

C) employee earnings master file.

D) payroll register.

E) employee earnings transaction file.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

57

Responsibility for updating of the personnel data master file should rest with authorized employees in the:

A) payroll department.

B) employee's operating department.

C) controller's department.

D) personnel department.

E) data control department.

A) payroll department.

B) employee's operating department.

C) controller's department.

D) personnel department.

E) data control department.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

58

A programmed routine in the edit run for payroll lists all employees who worked more than 50 hours during the week for review. This is an example of a:

A) validity check.

B) reasonableness check.

C) sequence check.

D) self-checking check.

E) independent check.

A) validity check.

B) reasonableness check.

C) sequence check.

D) self-checking check.

E) independent check.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

59

Payroll functions include all of the following except:

A) planning and controlling production.

B) preparing the payroll.

C) hiring employees.

D) protecting unclaimed wages.

E) recording the payroll.

A) planning and controlling production.

B) preparing the payroll.

C) hiring employees.

D) protecting unclaimed wages.

E) recording the payroll.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

60

Printed outputs from the payroll computer run that are sent to data control include all of the following except:

A) an exceptions and control report that is reviewed by data control before distributing the other printed output.

B) a copy of the payroll register that is returned along with the clock cards and time tickets to the payroll department for comparison with the original batch transmittal data.

C) a second copy of the payroll register and prenumbered payroll checks that are sent to the treasurer's office.

D) a summary of the payroll checks that is sent to the treasurer's office.

E) a general ledger summary that is sent to accounting showing the payroll entry generated by the payroll program.

A) an exceptions and control report that is reviewed by data control before distributing the other printed output.

B) a copy of the payroll register that is returned along with the clock cards and time tickets to the payroll department for comparison with the original batch transmittal data.

C) a second copy of the payroll register and prenumbered payroll checks that are sent to the treasurer's office.

D) a summary of the payroll checks that is sent to the treasurer's office.

E) a general ledger summary that is sent to accounting showing the payroll entry generated by the payroll program.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

61

Listed below are five assertion categories coded by the letters A through E.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories included in the balance sheet physically exist.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories included in the balance sheet physically exist.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

62

The extent of the auditor's inventory test count would least depend on which of the following?

A) The nature and composition of the inventory.

B) The care exercised by client employees in taking the inventory.

C) The effectiveness of controls pertaining to maintenance of perpetual records.

D) The effectiveness of controls pertaining to the safeguarding of the inventory.

E) The existence of inventory at multiple locations.

A) The nature and composition of the inventory.

B) The care exercised by client employees in taking the inventory.

C) The effectiveness of controls pertaining to maintenance of perpetual records.

D) The effectiveness of controls pertaining to the safeguarding of the inventory.

E) The existence of inventory at multiple locations.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

63

List, by assertion category, the specific audit objectives for the personnel services cycle.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

64

Which if the following is not a component of determining and recording manufacturing costs?

A) Charging direct materials and direct labor to work in process.

B) Transferring costs between production departments.

C) Assigning manufacturing overhead to work in process.

D) Maintaining correctness of inventory balances.

E) Transferring the cost of completed production to finished goods.

A) Charging direct materials and direct labor to work in process.

B) Transferring costs between production departments.

C) Assigning manufacturing overhead to work in process.

D) Maintaining correctness of inventory balances.

E) Transferring the cost of completed production to finished goods.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

65

In assessing control risk in the personnel services cycle, of least concern to the auditor is:

A) payments to fictitious employees.

B) payments to actual employees for hours not worked.

C) failure to pay actual employees for hours worked.

D) payment to actual employees at higher than authorized rates.

E) payments to actual employees for hours worked.

A) payments to fictitious employees.

B) payments to actual employees for hours not worked.

C) failure to pay actual employees for hours worked.

D) payment to actual employees at higher than authorized rates.

E) payments to actual employees for hours worked.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

66

The checks that are generated by an automated system are normally sent directly from computer processing to the:

A) data control department, which forwards them to the treasurer.

B) data control department, which forwards them to the payroll department.

C) personnel department.

D) payroll department.

E) treasurer.

A) data control department, which forwards them to the treasurer.

B) data control department, which forwards them to the payroll department.

C) personnel department.

D) payroll department.

E) treasurer.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

67

The Goren Company counts its inventory on October 31, 20X8. As a senior auditor assigned to the engagement, you observe the inventory count on this date. During the inventory observation, you encounter only minor problems, which are cleared up, to your satisfaction. On November 15, 20X8, the controller for the Goren Company informs you that the inventory summary sheets are complete and gives you a copy, part of which is reproduced here: During the inventory observation, you recorded the following inventory tag control information in your working papers:

During the inventory observation, you recorded the following test counts in your working papers:

REQUIRED: List the tag numbers identified above on your answer sheet. If you believe the information pertaining to the tag number is correct, so state. If you believe the information is incorrect, describe the error. The information you recorded during your test counts, of course, was accurate.

During the inventory observation, you recorded the following test counts in your working papers:

REQUIRED: List the tag numbers identified above on your answer sheet. If you believe the information pertaining to the tag number is correct, so state. If you believe the information is incorrect, describe the error. The information you recorded during your test counts, of course, was accurate.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

68

Listed below are five assertion categories coded by the letters A through E.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

The reporting entity has legal title to the inventories at the balance sheet date.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

The reporting entity has legal title to the inventories at the balance sheet date.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

69

For proper control, unclaimed checks should be stored by the:

A) treasurer's department.

B) payroll department.

C) personnel department.

D) data control department.

E) timekeeping department.

A) treasurer's department.

B) payroll department.

C) personnel department.

D) data control department.

E) timekeeping department.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

70

For each one of the following financial ratios, indicate the formula and identify the audit significance.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

71

Place an "X" in the applicable column for each substantive test to identify the assertions to which each test pertains.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

72

A common form of employee compensation for many companies involves the use of stock options. The auditor should determine all of the following except:

A) the types of incentive compensation plans used to compensate officers and employees

B) the ranking of officer compensation for the company within its industry, including stock options and all other types of executive compensation

C) how compensation expense is determined

D) how compensation expense is allocated to various accounting periods

E) the adequacy of disclosure related to incentive compensation plans

A) the types of incentive compensation plans used to compensate officers and employees

B) the ranking of officer compensation for the company within its industry, including stock options and all other types of executive compensation

C) how compensation expense is determined

D) how compensation expense is allocated to various accounting periods

E) the adequacy of disclosure related to incentive compensation plans

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

73

On an SEC engagement, an auditor wishes to determine the officers who receive the greatest total compensation. This objective is related primarily to the:

A) existence or occurrence assertion.

B) rights and obligations assertion.

C) valuation or allocation assertion.

D) presentation or disclosure assertion.

E) completeness assertion.

A) existence or occurrence assertion.

B) rights and obligations assertion.

C) valuation or allocation assertion.

D) presentation or disclosure assertion.

E) completeness assertion.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

74

Listed below are five assertion categories coded by the letters A through E.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories are properly stated at the lower of cost or market.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories are properly stated at the lower of cost or market.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

75

Listed below are five assertion categories coded by the letters A through E.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories and cost of goods sold are properly identified and classified in the financial statements.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories and cost of goods sold are properly identified and classified in the financial statements.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

76

Shown below is a partial system flowchart of payroll transactions.

REQUIRED: Label the symbols in the partial system flowchart.

REQUIRED: Label the symbols in the partial system flowchart.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

77

Following are a number of potential misstatements that might occur in the personnel services cycle. Also listed are a number of necessary controls for this cycle.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

REQUIRED: For each potential misstatement, indicate, using the assigned letter, the necessary control that would most likely prevent or detect the misstatement.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

78

Listed below are five assertion categories coded by the letters A through E.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories include all materials, products, and supplies on hand at the balance sheet date.

A.Completeness

D.Valuation or Allocation

B.Existence or Occurrence

E.Presentation and Disclosure

C.Rights and Obligations

REQUIRED: Match the transaction audit objectives with the codes for the assertion categories above.

Inventories include all materials, products, and supplies on hand at the balance sheet date.

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

80

Match between columns

Unlock Deck

Unlock for access to all 79 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 79 flashcards in this deck.