Deck 22: Multifactor Models

Full screen (f)

Question

Question

Question

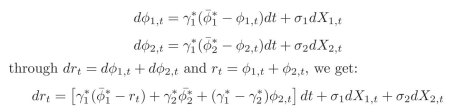

Show that, given:

Question

Question

Question

Given that we now have two stochastic factors, when writing Ito's lemma as the following  what are we implicitly assuming about them?

what are we implicitly assuming about them?

what are we implicitly assuming about them? Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 22: Multifactor Models

1

Is the 2-factor Vasicek model an afine model?

Yes, it is an afine model. It allows a closed form solution.

2

What are multifactor models?

Multifactor models are models that allow for more than one factor (that is in addition to the interest rate) to be defined by a stochastic process.

3

Show that, given:

4

In the Vasicek one factor model, the short rate determines the model. In the Vasicek two factor model, what rates drive the model?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

Does the 2-factor Vasicek model fit the yield curve?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

Given that we now have two stochastic factors, when writing Ito's lemma as the following what are we implicitly assuming about them?

what are we implicitly assuming about them? Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

Why is it considered that implied volatility of interest rate options has a "hump" shape?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

What peculiarity of a yield curve steepner makes the use of 2-factor models attractive?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

When are multifactor models used?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

What modi?cations should be included to Ito's lemma when we allow correlation between the two factors?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

How is the multivariate Ito's lemma defined?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

Can a solution always be found in order to price a security as proposed by the Feynman-Kac formula?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

In the 2-factor Hull-White model, what is the benefit of introducing θt (time dependent central tendency)?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

Under the Vasicek model, what degree of correlation do different interest rates have?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

What advantages does the 2-factor Vasicek have when fitting volatility?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

What is the difference between using a model for finding arbitrage oppor- tunities and using a model for pricing derivatives and other securities?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.