Deck 18: Comparative Forms of Doing Business

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

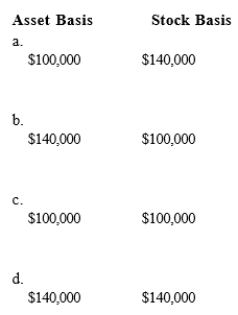

Kristine owns all of the stock of a C corporation which owns the following assets.  * Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.

* Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.

A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

* Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

Question

Question

Question

Question

Question

Question

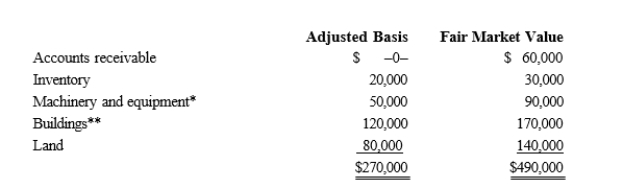

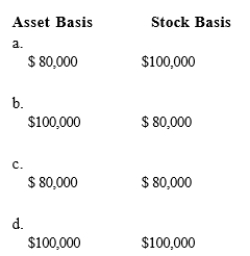

Ruchi contributes property with an adjusted basis of $80,000 and a fair market value of $100,000 to a newly formed business entity.If the entity is a partnership and the transaction qualifies under § 721, the partnership's basis for the property and the partner's basis for the partnership interest are:

Question

Question

Question

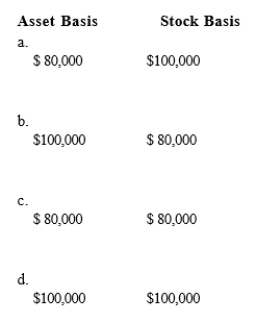

Martin contributes property with an adjusted basis of $100,000 and a fair market value of $140,000 to a newly formed business entity.If the entity is an S corporation and the transaction qualifies under § 351, the S corporation's basis for the property and the shareholder's basis for the stock are:

Question

Question

Question

Question

Question

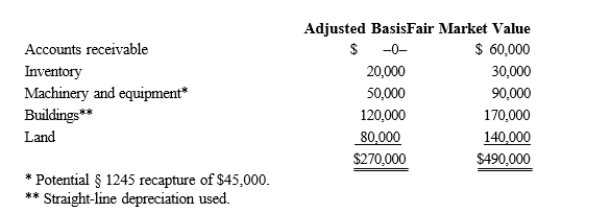

Albert's sole proprietorship owns the following assets.  Albert sells his sole proprietorship for $500,000.Calculate Albert's recognized gain or loss and classify it as capital or ordinary.

Albert sells his sole proprietorship for $500,000.Calculate Albert's recognized gain or loss and classify it as capital or ordinary.

A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

Albert sells his sole proprietorship for $500,000.Calculate Albert's recognized gain or loss and classify it as capital or ordinary.A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

Question

Question

Chen contributes property with an adjusted basis of $80,000 and a fair market value of $100,000 to a newly formed business entity.If the entity is a C corporation and the transaction qualifies under § 351, the corporation's basis for the property and the shareholder's basis for the stock are:

Question

Question

Catfish, Inc., a closely held corporation that is not a PSC, owns a 45% interest in Trout Partnership, which is classified as a passive activity.Trout's taxable loss for the current year is $250,000.During the year, Catfish receives a $60,000 cash distribution from Trout.Other relevant data for Catfish are as follows.  How much of Catfish's share of Trout's loss may it deduct in calculating its taxable income?

How much of Catfish's share of Trout's loss may it deduct in calculating its taxable income?

A)$0

B)$20,000

C)$45,000

D)$112,500

How much of Catfish's share of Trout's loss may it deduct in calculating its taxable income?A)$0

B)$20,000

C)$45,000

D)$112,500

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/84

Play

Full screen (f)

Deck 18: Comparative Forms of Doing Business

1

A limited liability company (LLC) is a hybrid business form that combines the corporate characteristic of limited liability for the owners with the tax characteristics of a partnership.

True

2

All of the shareholders of an S corporation have limited liability with respect to their ownership interests in the corporation whereas only limited partners in a limited partnership have such limited liability.

True

3

Of the corporate types of entities, all are subject to double taxation on current earnings.

False

4

C corporations are not subject to AMT but individuals are.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

5

For Federal income tax purposes, a business entity with two or more owners may be conducted as a partnership, C corporation, S corporation, or limited liability company.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

6

The AMT statutory rate for S corporation shareholders on the AMT base is 20%.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

7

Daniel, who is single, estimates that the profits of his business for the current tax year will be $200,000; he has no other sources of gross income.Since the 21% corporate rate is less than Daniel's marginal rate of 32%, he would save taxes operating the business as a C corporation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

8

Techniques that may permit a C corporation to avoid double taxation are available.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

9

If a C corporation has earnings and profits at least equal to the amount of a distribution, the tax consequences to the shareholders are the same regardless of whether the distribution is classified as a dividend or as a stock redemption.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

10

Some fringe benefits always provide a double benefit-a deduction for the employer and an exclusion for the employee.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

11

S corporation status always avoids double taxation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

12

An S corporation election for Federal income tax purposes also is effective for all states' income tax purposes.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

13

A sole proprietorship files Schedule C of Form 1040, a partnership files Form 1065, a C corporation files Form 1120, and an S corporation files Form 1120S.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

14

A limited partnership can indirectly avoid unlimited liability of the general partner if the general partner is a corporation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

15

A C corporation offers greater flexibility in terms of the types of owners and capital structure than an S corporation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

16

A corporation has a greater potential for raising capital than does a partnership.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

17

Each of the following can pass profits and losses through to the owners: general partnership, limited partnership, S corporation, and limited liability company.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

18

The tax treatment of S corporation shareholders with respect to fringe benefits is not the same as the tax treatment for C corporation shareholders, but is the same as the fringe benefit treatment for partners.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

19

An S corporation is not subject to the AMT, but its shareholders are because the S corporation's AMT adjustments and preferences are passed through to them.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

20

The at-risk provisions and the passive activity loss provisions decrease the tax attractiveness of investments in real estate for partnerships and for limited liability companies.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

21

Techniques that can be used to minimize the current period tax liability include:

A)Recognizing the interaction between the regular income tax liability and the alternative minimum tax liability.

B)Utilizing special allocations.

C)Having favorable treatment of certain fringe benefits.

D)Minimizing double taxation.

E)All of these can be used for effective tax planning.

A)Recognizing the interaction between the regular income tax liability and the alternative minimum tax liability.

B)Utilizing special allocations.

C)Having favorable treatment of certain fringe benefits.

D)Minimizing double taxation.

E)All of these can be used for effective tax planning.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

22

If the IRS reclassifies debt as equity, the repayment of the debt by the corporation to the shareholder automatically is treated as a dividend.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

23

The passive activity loss rules apply to S corporations but not to C corporations.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

24

Transferring funds that are deductible by the C corporation to shareholders can reduce or eliminate double taxation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

25

The Net Investment Income Tax (NIIT) is owed by both high income individuals and corporations.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

26

After an asset contribution by a partner to a partnership, the partner's basis for his or her ownership interest is the same as the basis of the assets contributed (if no liabilities are involved).

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

27

John wants to buy a business whose assets have appreciated in value.If the business is operated as a C corporation, it does not matter to John whether he purchases the assets or the stock.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

28

Molly transfers land with an adjusted basis of $28,000 and a fair market value of $65,000 to the Sand Partnership for a 30% ownership interest.The land is encumbered by a mortgage of $18,000, which the partnership assumes.Her basis for her ownership interest is $10,000 ($28,000 - $18,000).

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

29

Both Malcomb and Sandra (shareholders) loan Crow Corporation $50,000 at the market rate of 6% interest.Which of the following statements are false?

A)Crow may deduct the interest expense, and the interest income is taxable to Malcomb and Sandra.

B)When the note principal is repaid, neither Malcomb nor Sandra recognizes gross income from the repayment.

C)If the IRS were successful in reclassifying the notes as equity, the interest payments would not be deductible by Crow, and Malcomb and Sandra would still recognize income.

D)If the IRS were successful in reclassifying the notes as equity, repayment of the note principal to Malcomb and Sandra would not qualify for return of capital treatment and would most likely result in dividend income treatment for Malcomb and Sandra.

E)All of these are true.

A)Crow may deduct the interest expense, and the interest income is taxable to Malcomb and Sandra.

B)When the note principal is repaid, neither Malcomb nor Sandra recognizes gross income from the repayment.

C)If the IRS were successful in reclassifying the notes as equity, the interest payments would not be deductible by Crow, and Malcomb and Sandra would still recognize income.

D)If the IRS were successful in reclassifying the notes as equity, repayment of the note principal to Malcomb and Sandra would not qualify for return of capital treatment and would most likely result in dividend income treatment for Malcomb and Sandra.

E)All of these are true.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

30

If an S corporation distributes appreciated property as a dividend, it must recognize gain related to the appreciation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

31

Arnold purchases a building for $750,000 that is going to be used by his wholly owned corporation.Which of the following statements are correct?

A)If Arnold contributes the building to the corporation, there will be no gross income in the current year and a carryover basis of $750,000.

B)If Arnold leases the building to the corporation, lease-rental payments of $30,000 per year to Arnold will result in a $30,000 deduction for the corporation.

C)If Arnold leases the building to the corporation, lease-rental payments of $30,000 per year to Arnold will result in $30,000 of gross income for Arnold.

D)Leasing the building to the corporation will contribute to the tax avoidance objective of minimizing double taxation.

E)All of these statements are correct.

A)If Arnold contributes the building to the corporation, there will be no gross income in the current year and a carryover basis of $750,000.

B)If Arnold leases the building to the corporation, lease-rental payments of $30,000 per year to Arnold will result in a $30,000 deduction for the corporation.

C)If Arnold leases the building to the corporation, lease-rental payments of $30,000 per year to Arnold will result in $30,000 of gross income for Arnold.

D)Leasing the building to the corporation will contribute to the tax avoidance objective of minimizing double taxation.

E)All of these statements are correct.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

32

If lease rental payments to a noncorporate shareholder-lessor are classified as unreasonable, the taxable income of a C corporation increases and the gross income of the shareholder increases.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

33

Melinda's basis for her partnership interest is $250,000.If she receives a cash distribution of $290,000, her recognized gain is $40,000 and her basis for her partnership interest is reduced to $0.Melinda is still a partner after the distribution.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

34

A benefit of an S corporation when compared with a C corporation is that it is subject to Federal income tax only in limited circumstances.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

35

Wally contributes land (adjusted basis of $30,000; fair market value of $100,000) to an S corporation in a transaction that qualifies under § 351.The corporation subsequently sells the land for $120,000, recognizing a gain of $90,000 ($120,000 - $30,000).If Wally owns 30% of the stock, $76,000 [$70,000 + 30%($20,000)] of the $90,000 recognized gain is allocated to Wally.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

36

Mercedes owns a 30% interest in Magenta Partnership (basis of $52,000), which she sells to Calvin for $65,000. Mercedes' recognized gain of $13,000 is classified as capital gain.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

37

The special allocation opportunities that are available to partnerships are available to S corporations only if affected shareholders elect to do so.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

38

A shareholder's basis in the stock of an S corporation is increased by corporate profits and decreased by losses.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

39

An individual who owes the NIIT cannot also be subject to the additional Medicare tax.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

40

The profits of a business owned by Taylor (60%) and Maggie (40%) for the current tax year are $100,000.If the business is a C corporation or an S corporation, there is no effect on Taylor's basis in her stock.If the business is a partnership or an LLC, Taylor's basis in her partnership interest or basis in her stock is increased by $60,000.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

41

Kristine owns all of the stock of a C corporation which owns the following assets. * Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.

A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

* Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

42

Tuan and Ella are going to establish a business.They expect the business to be very successful in the long-run, but project losses of approximately $100,000 for each of the first five years.Due to potential environmental concerns, limited liability is a requisite for the owners.Which form of business entity should they select?

A)General partnership.

B)Limited partnership.

C)C corporation.

D)S corporation.

A)General partnership.

B)Limited partnership.

C)C corporation.

D)S corporation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

43

Khalid contributes land (fair market value of $700,000; adjusted basis of $200,000) and Dan contributes $700,000 cash to form Teal Partnership.Both Khalid and Dan own a 50% interest.One year later, Teal sells the land for $800,000.How much gain is recognized by each partner?

A)$600,000 to Khalid, $0 to Dan.

B)$550,000 to Khalid, $50,000 to Dan.

C)$300,000 to Khalid, $300,000 to Dan.

D)$50,000 to Khalid, $50,000 to Dan.

A)$600,000 to Khalid, $0 to Dan.

B)$550,000 to Khalid, $50,000 to Dan.

C)$300,000 to Khalid, $300,000 to Dan.

D)$50,000 to Khalid, $50,000 to Dan.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

44

Both Thu and Tuan own one-half of the stock of Wren, Inc., a C corporation.Each shareholder holds a stock basis of $175,000.Wren has accumulated E & P of $300,000.Wren's taxable income for the current year is $100,000, and it distributes $75,000 to each shareholder.Thu's stock basis at the end of the year is:

A)$0.

B)$100,000.

C)$150,000.

D)$175,000.

A)$0.

B)$100,000.

C)$150,000.

D)$175,000.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

45

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

Sole proprietorship

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

Sole proprietorship

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

46

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of corporate stock by the S corporation shareholders.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of corporate stock by the S corporation shareholders.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

47

Ruchi contributes property with an adjusted basis of $80,000 and a fair market value of $100,000 to a newly formed business entity.If the entity is a partnership and the transaction qualifies under § 721, the partnership's basis for the property and the partner's basis for the partnership interest are:

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

48

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

S corporation

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

S corporation

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

49

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of corporate stock by the C corporation shareholders.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of corporate stock by the C corporation shareholders.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

50

Martin contributes property with an adjusted basis of $100,000 and a fair market value of $140,000 to a newly formed business entity.If the entity is an S corporation and the transaction qualifies under § 351, the S corporation's basis for the property and the shareholder's basis for the stock are:

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

51

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

C corporation

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

C corporation

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

52

Alice contributes equipment (fair market value of $82,000; adjusted basis of $20,000), subject to a $14,000 liability, to form Orange Partnership, a general partnership.Mary contributes $68,000 cash.Alice and Mary share equally in partnership profits and losses.What is Alice's and Mary's basis for their partnership interests?

A)$6,000 to Alice, $68,000 to Mary.

B)$6,000 to Alice, $75,000 to Mary.

C)$13,000 to Alice, $75,000 to Mary.

D)$20,000 to Alice, $68,000 to Mary.

A)$6,000 to Alice, $68,000 to Mary.

B)$6,000 to Alice, $75,000 to Mary.

C)$13,000 to Alice, $75,000 to Mary.

D)$20,000 to Alice, $68,000 to Mary.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

53

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

Limited partnership

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

Limited partnership

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

54

Both Tracy and Cabel own one-half of the stock of Finch, Inc., an S corporation with no accumulated E & P. Tracy's basis in the Finch stock is $225,000.Finch's taxable income for the current year is $100,000, and it distributes $180,000 to each shareholder.Tracy's stock basis at the end of the year is:

A)$-0-.

B)$45,000.

C)$95,000.

D)$100,000.

A)$-0-.

B)$45,000.

C)$95,000.

D)$100,000.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

55

Albert's sole proprietorship owns the following assets. Albert sells his sole proprietorship for $500,000.Calculate Albert's recognized gain or loss and classify it as capital or ordinary.

A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

Albert sells his sole proprietorship for $500,000.Calculate Albert's recognized gain or loss and classify it as capital or ordinary.A)$230,000 ordinary income.

B)$230,000 capital gain.

C)$115,000 ordinary income and $115,000 capital gain.

D)$110,000 ordinary income and $120,000 capital gain.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

56

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of the individual assets of an unincorporated sole proprietorship by the owner.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of the individual assets of an unincorporated sole proprietorship by the owner.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

57

Chen contributes property with an adjusted basis of $80,000 and a fair market value of $100,000 to a newly formed business entity.If the entity is a C corporation and the transaction qualifies under § 351, the corporation's basis for the property and the shareholder's basis for the stock are:

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

58

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of the corporate assets by the C corporation.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of the corporate assets by the C corporation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

59

Catfish, Inc., a closely held corporation that is not a PSC, owns a 45% interest in Trout Partnership, which is classified as a passive activity.Trout's taxable loss for the current year is $250,000.During the year, Catfish receives a $60,000 cash distribution from Trout.Other relevant data for Catfish are as follows. How much of Catfish's share of Trout's loss may it deduct in calculating its taxable income?

A)$0

B)$20,000

C)$45,000

D)$112,500

How much of Catfish's share of Trout's loss may it deduct in calculating its taxable income?A)$0

B)$20,000

C)$45,000

D)$112,500

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

60

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

General partnership

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

General partnership

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

61

Match the following.

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

General partnership

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

General partnership

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

62

Match the following statements.

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

Technique for minimizing double taxation

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

Technique for minimizing double taxation

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

63

Both Albert and Elva own 50% of the stock of Eagle, Inc.(a C corporation).To cover what is perceived as temporary working capital needs, each shareholder loans Eagle $200,000 with an annual interest rate of 3% (same as the Federal rate) and a maturity date of one year.The loan is made at the beginning of 2019.

a.What are the tax consequences to Albert, Elva, and Eagle if the loans are classified as debt?

b.What are the tax consequences to Albert, Elva, and Eagle if the loans are classified as equity?

a.What are the tax consequences to Albert, Elva, and Eagle if the loans are classified as debt?

b.What are the tax consequences to Albert, Elva, and Eagle if the loans are classified as equity?

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

64

Match the following.

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

Limited partnership

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

Limited partnership

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

65

Blue, Inc., records taxable income before salary payments of $700,000 to its president who has a marginal rate of 32%.

a.Calculate the tax liability to Blue if the president's salary is $400,000 and if it is $100,000.

b.What tax benefit is there of paying the higher salary to the president?

c.What negative tax result may occur associated with the payment of the higher salary?

a.Calculate the tax liability to Blue if the president's salary is $400,000 and if it is $100,000.

b.What tax benefit is there of paying the higher salary to the president?

c.What negative tax result may occur associated with the payment of the higher salary?

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

66

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Net capital loss

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Net capital loss

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

67

Match the following statements.

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

Partnerships

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

Partnerships

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

68

Match the following statements.

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

Regular tax rate

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

Regular tax rate

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

69

Match the following.

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

S corporation

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

S corporation

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

70

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Charitable contributions

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Charitable contributions

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

71

Kirby, the sole shareholder of Falcon, Inc., leases a building to the corporation.The taxable income of the corporation for the tax year before deducting the lease payments is projected to be $500,000.

a.What are the tax consequences to Kirby and to Falcon if Kirby leases a building to the corporation for $400,000?

b.Is there a potential pitfall? How would it change the tax consequences to Kirby and to

Falcon?

a.What are the tax consequences to Kirby and to Falcon if Kirby leases a building to the corporation for $400,000?

b.Is there a potential pitfall? How would it change the tax consequences to Kirby and to

Falcon?

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

72

Match the following statements.

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

S corporations

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

S corporations

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

73

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Net capital gain

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Net capital gain

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

74

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Organization costs

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Organization costs

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

75

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of an ownership interest by a partner.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

Sale of an ownership interest by a partner.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

76

Jane is going to invest $90,000 in a business entity that she will manage.Her projected share of the loss for the first year is $36,000.Jane' marginal tax rate is 32%.Determine the cash flow benefit of the loss to her if the business form is:

a.A general partnership.

b.An S corporation.

c.An LLC.

d.A C corporation.

a.A general partnership.

b.An S corporation.

c.An LLC.

d.A C corporation.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

77

Match the following.

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

C corporation

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

C corporation

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

78

Candace, who is in the 32% tax bracket, is establishing a business that could have potential environmental liability problems.Therefore, she is trying to decide between the C corporation form and the S corporation form.She projects that the business will generate earnings of about $75,000 each year.Advise Candace on the tax consequences of each entity form.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

79

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Regular tax rate

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

Regular tax rate

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

80

Match the following statements.

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

C corporations

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

C corporations

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 84 flashcards in this deck.