Exam 18: Comparative Forms of Doing Business

Exam 1: Introduction to Taxation122 Questions

Exam 2: Working With the Tax Law101 Questions

Exam 3: Taxes on the Financial Statements70 Questions

Exam 4: Gross Income100 Questions

Exam 5: Business Deductions143 Questions

Exam 6: Losses and Loss Limitations147 Questions

Exam 7: Property Transactions: Basis, Gain and Loss, and Nontaxable Exchanges126 Questions

Exam 8: Property Transactions: Capital Gains and Losses, Section 1231, and Recapture Provisions119 Questions

Exam 9: Individuals As the Taxpayer132 Questions

Exam 10: Individuals: Income, Deductions, and Credits129 Questions

Exam 11: Individuals As Employees and Proprietors116 Questions

Exam 12: Corporations: Organization, Capital Structure, and Operating Rules136 Questions

Exam 13: Corporations: Earnings and Profits and Distributions127 Questions

Exam 14: Partnerships and Limited Liability Entities142 Questions

Exam 15: S Corporations109 Questions

Exam 16: Multijurisdictional Taxation91 Questions

Exam 17: Business Tax Credits and the Alternative Minimum Tax94 Questions

Exam 18: Comparative Forms of Doing Business84 Questions

Select questions type

An S corporation is not subject to the AMT, but its shareholders are because the S corporation's AMT adjustments and preferences are passed through to them.

Free

(True/False)

4.8/5  (36)

(36)

Correct Answer: Verified

Verified

True

The at-risk provisions and the passive activity loss provisions decrease the tax attractiveness of investments in real estate for partnerships and for limited liability companies.

Free

(True/False)

4.7/5 (43)

Correct Answer:Verified

True

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

-C corporation

Free

(Essay)

4.7/5 (34)

Correct Answer:Verified

a

The tax treatment of S corporation shareholders with respect to fringe benefits is not the same as the tax treatment for C corporation shareholders, but is the same as the fringe benefit treatment for partners.

(True/False)

4.8/5 (34)

Both Albert and Elva own 50% of the stock of Eagle, Inc.(a C corporation).To cover what is perceived as temporary working capital needs, each shareholder loans Eagle $200,000 with an annual interest rate of 3% (same as the Federal rate) and a maturity date of one year.The loan is made at the beginning of 2019.

a.What are the tax consequences to Albert, Elva, and Eagle if the loans are classified as debt?

b.What are the tax consequences to Albert, Elva, and Eagle if the loans are classified as equity?

(Essay)

4.9/5 (40)

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

-Organization costs

(Essay)

4.9/5 (35)

Techniques that can be used to minimize the current period tax liability include:

(Multiple Choice)

4.8/5 (37)

Both Malcomb and Sandra (shareholders) loan Crow Corporation $50,000 at the market rate of 6% interest.Which of the following statements are false?

(Multiple Choice)

4.9/5 (36)

Match the following attributes with the different forms.A particular attribute may apply to more than one entity form.

a.Ability of all owners to have limited liability.

b.Ability to pass tax attributes through to the owners.

c.Right of all owners to participate in the management of the business.

d.Number of owners is limited.

e.Ability to have multiple owners.

-S corporation

(Essay)

4.8/5 (33)

Match the following.

a.Contribution of appreciated property to the business entity by an owner is never subject to taxation.

b.Realized gains on the contribution of appreciated property to the entity are not recognized by the contributor when an 80% control requirement is satisfied.

c.Realized losses on the contribution of loss property to the entity are never recognized by the contributor.

d.Realized losses on the contribution of loss property to the entity are recognized by the contributor unless an

80% control requirement is satisfied.

e.Basis of ownership interest to the owner is dependent on whether gain or loss is recognized to the owner on the contribution of assets to the business entity.

-General partnership

(Essay)

4.7/5 (26)

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

-Sale of corporate stock by the C corporation shareholders.

(Essay)

4.7/5 (31)

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

-Regular tax rate

(Essay)

4.8/5 (40)

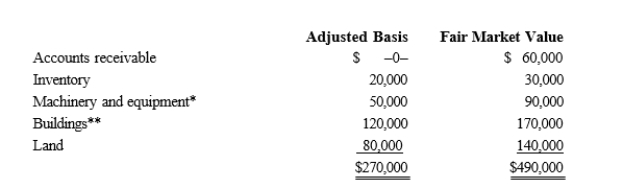

Kristine owns all of the stock of a C corporation which owns the following assets.  * Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.

* Potential § 1245 recapture of $45,000. ** Straight-line depreciation was used. Her adjusted basis for her stock is $270,000.Calculate Kristine's recognized gain or loss and classify it as capital or ordinary if she sells her stock for $500,000.

(Multiple Choice)

4.7/5 (43)

For Federal income tax purposes, a business entity with two or more owners may be conducted as a partnership, C corporation, S corporation, or limited liability company.

(True/False)

4.9/5 (33)

A sole proprietorship files Schedule C of Form 1040, a partnership files Form 1065, a C corporation files Form 1120, and an S corporation files Form 1120S.

(True/False)

4.8/5 (35)

Match the following statements.

a.Usually subject to single taxation even if the entity is incorporated.

b.Not making distributions to shareholders.

c.Rate for a corporate taxpayer is 21%.

d.Subject to double taxation.

e.Eligible for special allocations.

-Technique for minimizing double taxation

(Essay)

4.8/5 (31)

Match the following statements.

a.For the corporate taxpayer, taxed using the regular tax rates.

b.Must be capitalized, but can be amortized over 180 months.

c.For the corporate taxpayer, the rate is 21%.

d.For the corporate taxpayer, cannot be deducted at all in the current tax year.

e.For the corporate taxpayer, limited to 10% of taxable income before certain deductions.

-Net capital loss

(Essay)

4.8/5 (32)

Match the following statements.

a.Transaction in this form enables double taxation to be avoided.

b.Gain or loss is calculated separately for each asset and is subject to single taxation.

c.This is subject to double taxation.

d.The sale is treated as the sale of a capital asset under § 741 but subject to ordinary income potential under §

751.

e.This is not subject to double taxation on the sale of corporate stock.

-Sale of corporate stock by the S corporation shareholders.

(Essay)

4.9/5 (25)

Melinda's basis for her partnership interest is $250,000.If she receives a cash distribution of $290,000, her recognized gain is $40,000 and her basis for her partnership interest is reduced to $0.Melinda is still a partner after the distribution.

(True/False)

4.8/5 (36)

John wants to buy a business whose assets have appreciated in value.If the business is operated as a C corporation, it does not matter to John whether he purchases the assets or the stock.

(True/False)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)