Deck 8: Supply in a Competitive Market

Full screen (f)

Question

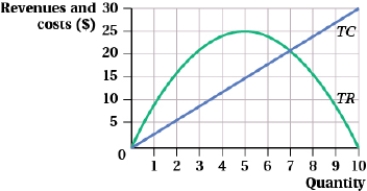

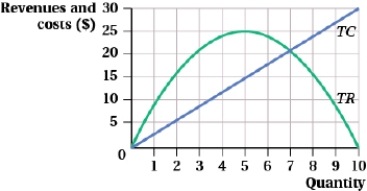

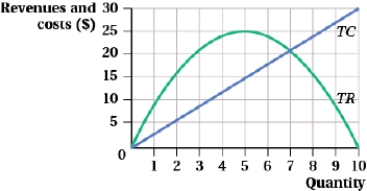

(Figure: Profit-Maximizing Output Level I) Total revenue is maximized at a quantity of ____.

A) 10

B) 7

C) 5

D) 0

A) 10

B) 7

C) 5

D) 0

Question

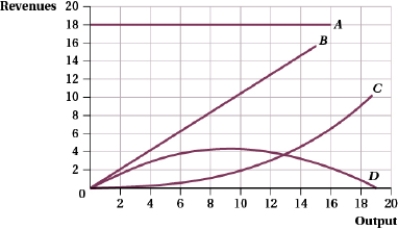

(Figure: Revenues and Output I) The total revenue curve for a perfectly competitive firm is represented by curve:

A) A.

B) B.

C) C.

D) D.

A) A.

B) B.

C) C.

D) D.

Question

Question

(Figure: Firm I) At the profit maximizing quantity, the firm's average total cost is $____.

A) 40

B) 30

C) 20

D) 0

A) 40

B) 30

C) 20

D) 0

Question

Question

Question

(Figure: Price and Quantity III) If the market price is $6, this perfectly competitive firm will earn profits of:

A) $27.

B) $54.

C) $18.

D) $78.

A) $27.

B) $54.

C) $18.

D) $78.

Question

Question

Suppose that the market for painting services is perfectly competitive. Painting companies are identical; their long-run cost functions are given by  .

.

Market demand is

) The long-run equilibrium quantity in this industry is ____.

A) 5,000

B) 4,750

C) 2,500

D) 1,900

.Market demand is

) The long-run equilibrium quantity in this industry is ____.

A) 5,000

B) 4,750

C) 2,500

D) 1,900

Question

Question

Question

Suppose that the market for painting services is perfectly competitive. Painting companies are identical; their long-run cost functions are given by  .

.

Market demand is

) The long-run equilibrium price in this industry is $____.

A) 194.5

B) 173.5

C) 162.5

D) 155.5

.Market demand is

) The long-run equilibrium price in this industry is $____.

A) 194.5

B) 173.5

C) 162.5

D) 155.5

Question

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost:  where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

, where N is the number of firms. Market demand is

) In the long-run equilibrium, the market price is $ ____.

A) 30.675

B) 26.875

C) 22.775

D) 21.345

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals , where N is the number of firms. Market demand is

) In the long-run equilibrium, the market price is $ ____.

A) 30.675

B) 26.875

C) 22.775

D) 21.345

Question

Question

(Figure: Firm I) At the profit maximizing quantity, the firm's total revenue is $____.

A) 240

B) 200

C) 120

D) 0

A) 240

B) 200

C) 120

D) 0

Question

Question

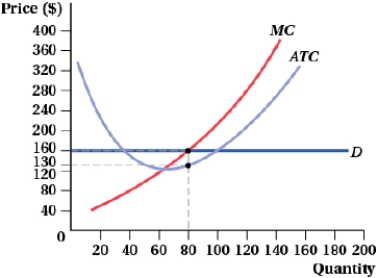

(Figure; Price and Quantity VII) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

Question

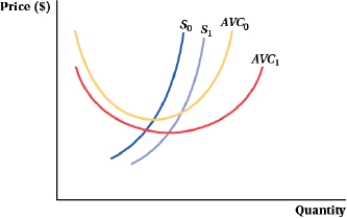

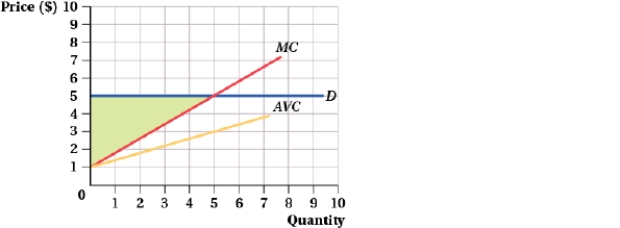

(Figure: Price and Quantity IX) What could have caused the supply and average variable cost curves to shift outward?

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

Question

Question

Question

(Figure: Price and Quantity VI) Economic profit for this firm can be calculated as:

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

Question

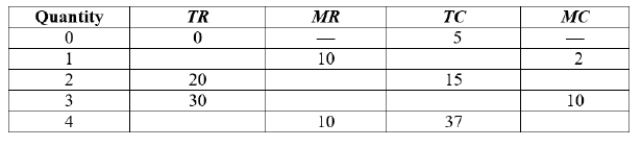

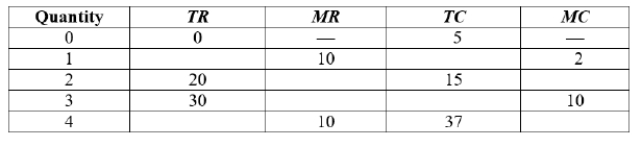

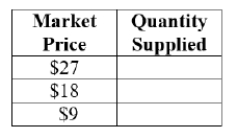

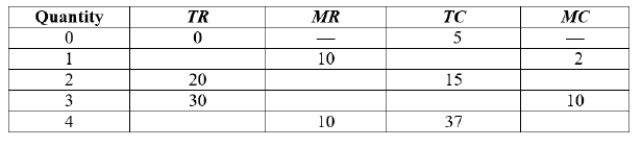

Use the following table to answer the question. At the profit maximizing quantity, the marginal revenue is $____.

A) 15

B) 12

C) 10

D) 7

A) 15

B) 12

C) 10

D) 7

Question

(Figure: Profit-Maximizing Output Level I) At the profit maximizing quantity, the slope of the total cost curve is ____.

A) 7

B) 5

C) 3

D) 1/2

A) 7

B) 5

C) 3

D) 1/2

Question

(Figure: Price and Quantity X) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

A) 700.

B) 250.

C) 1,050.

D) 500.

A) 700.

B) 250.

C) 1,050.

D) 500.

Question

Question

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by  . The quantity at which average total cost is minimized for each firm is ____.

. The quantity at which average total cost is minimized for each firm is ____.

A) 4.5

B) 3.5

C) 2.5

D) 1.5

. The quantity at which average total cost is minimized for each firm is ____.A) 4.5

B) 3.5

C) 2.5

D) 1.5

Question

Question

Question

Question

Question

(Figure: Firm I) At the profit maximizing quantity, the firm's profit is $____.

A) 150

B) 100

C) 50

D) 0

A) 150

B) 100

C) 50

D) 0

Question

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; their long-run cost functions are given by  . Market demand is

. Market demand is

) In the long-run equilibrium in this industry, there are ____ firms in the industry.

A) 4,124.72

B) 3,941.83

C) 3,663.46

D) 3,276.32

. Market demand is ) In the long-run equilibrium in this industry, there are ____ firms in the industry.

A) 4,124.72

B) 3,941.83

C) 3,663.46

D) 3,276.32

Question

Question

Question

Question

(Figure: Price and Quantity I) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

A) 1,100

B) 800

C) 1,200

D) 400

A) 1,100

B) 800

C) 1,200

D) 400

Question

Question

Question

Question

Question

Question

Question

Use the following table to answer the question. The profit maximizing level of output is a quantity of ____.

A) 4

B) 3

C) 2

D) 1

A) 4

B) 3

C) 2

D) 1

Question

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by  . The marginal cost curve for a firm in this industry is MC (Q) = ____.

. The marginal cost curve for a firm in this industry is MC (Q) = ____.

A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

. The marginal cost curve for a firm in this industry is MC (Q) = ____.A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

Question

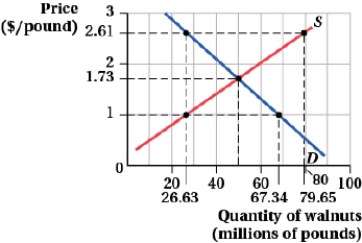

(Figure: Market for Walnuts I) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE?  I. The demand curve facing a walnut grower is perfectly elastic at $1.

I. The demand curve facing a walnut grower is perfectly elastic at $1.

II) If a walnut grower sold 80,000 pounds of walnuts, his total revenue would be $138,400.

III) If a walnut grower sold one more pound of walnuts, his total revenue would increase by $1.73.

A) I, II, and III

B) II

C) II and III

D) I

I. The demand curve facing a walnut grower is perfectly elastic at $1.II) If a walnut grower sold 80,000 pounds of walnuts, his total revenue would be $138,400.

III) If a walnut grower sold one more pound of walnuts, his total revenue would increase by $1.73.

A) I, II, and III

B) II

C) II and III

D) I

Question

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; they have long-run cost functions given by  . The quantity at which average total cost is minimized is ____.

. The quantity at which average total cost is minimized is ____.

A) 4.5

B) 3.5

C) 2.5

D) 1.5

. The quantity at which average total cost is minimized is ____.A) 4.5

B) 3.5

C) 2.5

D) 1.5

Question

Question

Question

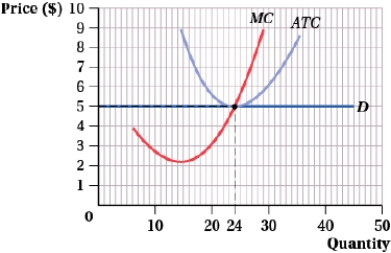

(Figure: Price and Quantity IV) Which of the following statements is (are) TRUE?  I. The firm earns $120 of profit at 24 units of output.

I. The firm earns $120 of profit at 24 units of output.

II) At prices above $5, the firm earns positive profit.

III) At a price of $4, the firm would produce more than 24 units of output to offset the lower price.

A) I

B) II and III

C) II

D) I and III

I. The firm earns $120 of profit at 24 units of output.II) At prices above $5, the firm earns positive profit.

III) At a price of $4, the firm would produce more than 24 units of output to offset the lower price.

A) I

B) II and III

C) II

D) I and III

Question

Question

(Figure: Firm I) At the profit maximizing quantity, the firm's total cost is $____.

A) 200

B) 150

C) 80

D) 0

A) 200

B) 150

C) 80

D) 0

Question

Question

Question

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; they have long-run cost functions given by  . The marginal cost curve for each firm in this industry is MC(Q) = ____.

. The marginal cost curve for each firm in this industry is MC(Q) = ____.

A) 3Q2 - 6Q + 90

B) Q2 - 3Q + 90

C) Q3 - 3Q2 + 90Q

D) 3Q3 - 6Q2 + 90Q

. The marginal cost curve for each firm in this industry is MC(Q) = ____.A) 3Q2 - 6Q + 90

B) Q2 - 3Q + 90

C) Q3 - 3Q2 + 90Q

D) 3Q3 - 6Q2 + 90Q

Question

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; their long-run cost functions are given by  . Market demand is

. Market demand is

) The long-run equilibrium quantity in this industry is ____.

A) 6,215.25

B) 6,100.25

C) 5,912.25

D) 5,845.25

. Market demand is ) The long-run equilibrium quantity in this industry is ____.

A) 6,215.25

B) 6,100.25

C) 5,912.25

D) 5,845.25

Question

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by  . The average total cost curve for a firm in this industry is ATC (Q) = ____.

. The average total cost curve for a firm in this industry is ATC (Q) = ____.

A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

. The average total cost curve for a firm in this industry is ATC (Q) = ____.A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

Question

Question

Question

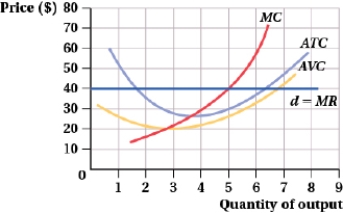

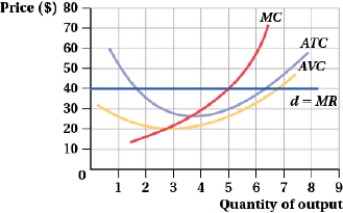

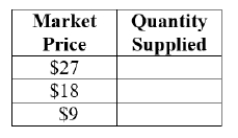

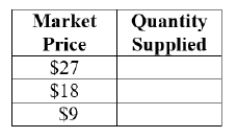

(Figure: Price and Quantity of Output I) At a market price of $9, the firm is willing to supply ____ units of the good.

A) 8

B) 7

C) 3

D) 0

A) 8

B) 7

C) 3

D) 0

Question

Question

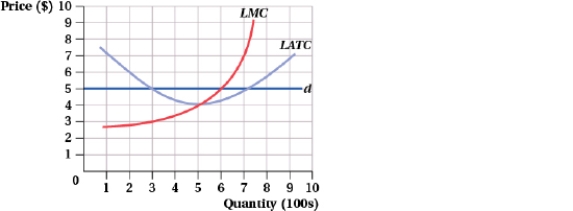

(Figure: Price and Quantity XII) Which of the following statements is (are) TRUE?  I. In the long run, this firm will produce 500 units of output.

I. In the long run, this firm will produce 500 units of output.

II) In the short run, this firm produces 600 units of output.

III) The long-run equilibrium price is $4.

IV) At a price of $5, new firms will eventually enter the market, eliminating this firm's economic profits.

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

I. In the long run, this firm will produce 500 units of output.II) In the short run, this firm produces 600 units of output.

III) The long-run equilibrium price is $4.

IV) At a price of $5, new firms will eventually enter the market, eliminating this firm's economic profits.

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

Question

Question

Question

Question

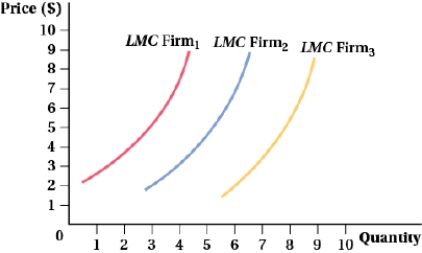

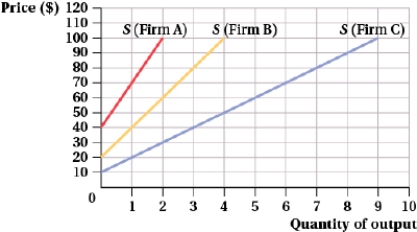

(Figure: Perfectly Competitive Firms I) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE?  I. In the long run, each firm will produce the same quantity of output.

I. In the long run, each firm will produce the same quantity of output.

II) Firm 1 is the highest-cost producer and Firm 3 is the lowest-cost producer.

III) Firm 3 will produce the most output in the long run.

A) II

B) III

C) II and III

D) I

I. In the long run, each firm will produce the same quantity of output.II) Firm 1 is the highest-cost producer and Firm 3 is the lowest-cost producer.

III) Firm 3 will produce the most output in the long run.

A) II

B) III

C) II and III

D) I

Question

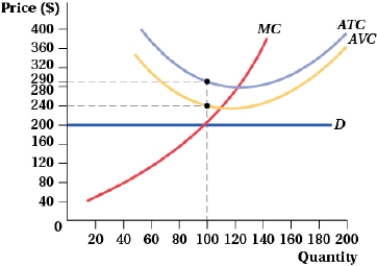

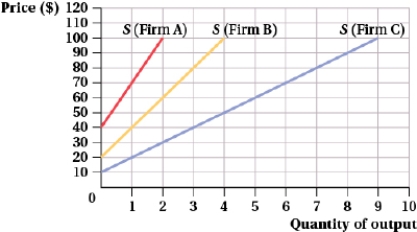

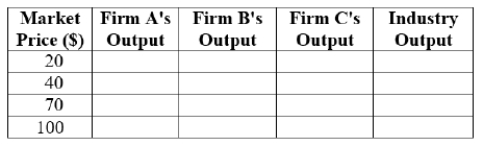

(Figure: Price and Quantity of Output and Table I) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. At a market price of $100, the industry output is ____.

A) 15

B) 9.5

C) 4

D) 1

A) 15

B) 9.5

C) 4

D) 1

Question

(Figure: Price and Quantity of Output I) At a market price of $18, the firm is willing to supply ____ units of the good.

A) 8

B) 7

C) 5

D) 0

A) 8

B) 7

C) 5

D) 0

Question

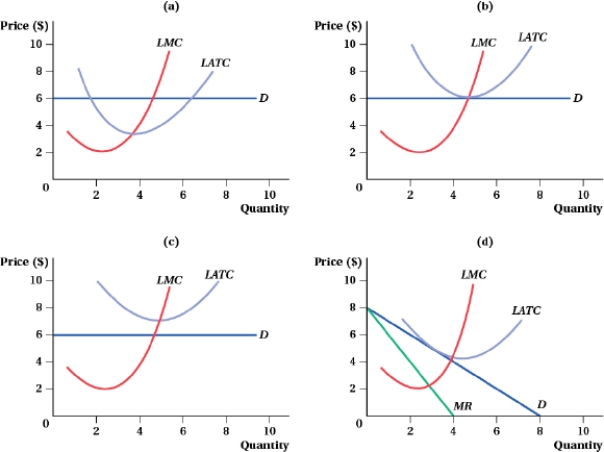

(Figure: Representative Firm I) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

A) panel a

B) panel b

C) panel c

D) panel d

A) panel a

B) panel b

C) panel c

D) panel d

Question

(Figure: Price and Quantity of Output I) At a market price of $27, the firm is willing to supply ____ units of the good.

A) 8

B) 7

C) 5

D) 0

A) 8

B) 7

C) 5

D) 0

Question

Question

(Figure: Price and Quantity of Output and Table I) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. At a market price of $20, the industry output is ____.

A) 15

B) 9.5

C) 4

D) 1

A) 15

B) 9.5

C) 4

D) 1

Question

(Figure: Price and Quantity II) This firm maximizes profit by producing _____ units of output.

A) 3

B) 7

C) 10

D) 12

A) 3

B) 7

C) 10

D) 12

Question

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost:  where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

, where N is the number of firms. Market demand is

) In the long-run equilibrium, there are ____ firms in the industry.

A) 59.375

B) 55.475

C) 51.685

D) 44.985

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals , where N is the number of firms. Market demand is

) In the long-run equilibrium, there are ____ firms in the industry.

A) 59.375

B) 55.475

C) 51.685

D) 44.985

Question

Question

(Figure: Profit-Maximizing Output Level I) At the profit maximizing quantity, the slope of the total revenue curve is ____.

A) 7

B) 5

C) 4

D) 3

A) 7

B) 5

C) 4

D) 3

Question

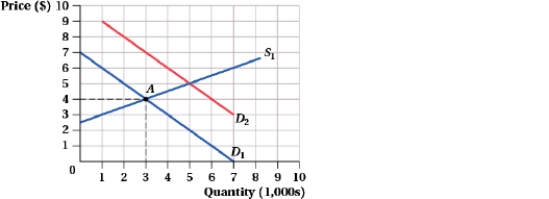

(Figure: Long Run Output I) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Question

Question

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost:  where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

, where N is the number of firms. Market demand is

) In the long-run equilibrium, the total industry output is ____.

A) 296.875

B) 287.475

C) 237.685

D) 224.985

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals , where N is the number of firms. Market demand is

) In the long-run equilibrium, the total industry output is ____.

A) 296.875

B) 287.475

C) 237.685

D) 224.985

Question

Use the following table to answer the question. At a quantity of 1, the total cost is $____.

A) 15

B) 12

C) 10

D) 7

A) 15

B) 12

C) 10

D) 7

Question

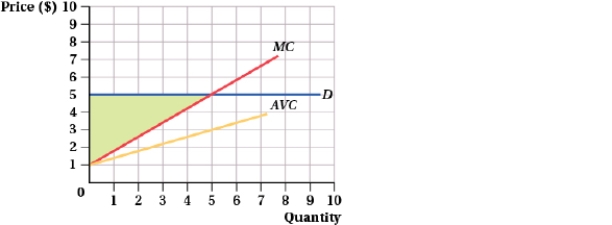

(Figure: Price and Quantity XI) Which of the following statements is (are) TRUE?  I. Producer surplus = TR - VC = $25 - $15.

I. Producer surplus = TR - VC = $25 - $15.

II) The shaded area between the demand curve and marginal cost represents producer surplus and equals $10.

III) The firm's profit = $10 - FC.

A) I, II, and III

B) II

C) I and III

D) III

I. Producer surplus = TR - VC = $25 - $15.II) The shaded area between the demand curve and marginal cost represents producer surplus and equals $10.

III) The firm's profit = $10 - FC.

A) I, II, and III

B) II

C) I and III

D) III

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/148

Play

Full screen (f)

Deck 8: Supply in a Competitive Market

1

(Figure: Profit-Maximizing Output Level I) Total revenue is maximized at a quantity of ____.

A) 10

B) 7

C) 5

D) 0

A) 10

B) 7

C) 5

D) 0

C

2

(Figure: Revenues and Output I) The total revenue curve for a perfectly competitive firm is represented by curve:

A) A.

B) B.

C) C.

D) D.

A) A.

B) B.

C) C.

D) D.

B

3

Suppose that the long-run total cost curve for each firm is given by TC = 500Q - 20Q2 + Q3, where Q is the quantity of the product. Also, suppose there is free entry and exit. To find the quantity where ATC is minimized, the firm would need to solve the following equation for Q:

A) 500 - 40Q + 3Q2 = 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2 = 500 - 20Q + Q2.

C) 500Q - 20Q2 + Q3 = 500 - 20Q + Q2.

D) It would be impossible to do this without more information.

A) 500 - 40Q + 3Q2 = 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2 = 500 - 20Q + Q2.

C) 500Q - 20Q2 + Q3 = 500 - 20Q + Q2.

D) It would be impossible to do this without more information.

B

4

(Figure: Firm I) At the profit maximizing quantity, the firm's average total cost is $____.

A) 40

B) 30

C) 20

D) 0

A) 40

B) 30

C) 20

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

5

If the long-run total cost curve for each firm is given by TC = 60Q - 70Q2 + 4Q3, in the long run, the marginal cost is:

A) 60 - 70Q + 4Q2.

B) 60 - 140Q + 12Q2.

C) 60Q - 70Q2 + 4Q3.

D) -70Q2 + 4Q3.

A) 60 - 70Q + 4Q2.

B) 60 - 140Q + 12Q2.

C) 60Q - 70Q2 + 4Q3.

D) -70Q2 + 4Q3.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

6

Suppose that the perfectly competitive market for granola bars is made up of identical firms with long-run total cost functions given by TC(Q) =8Q3-40Q2 + 200Q. Assume that these cost functions are independent of the number of firms in the market and that firms may enter or exit the market freely. Market demand is QD = 8,000 - 3.5P, where price is in cents. In the long-run equilibrium, each firm produces a quantity of ____ bars.

A) 3.5

B) 3

C) 2.5

D) 2

A) 3.5

B) 3

C) 2.5

D) 2

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

7

(Figure: Price and Quantity III) If the market price is $6, this perfectly competitive firm will earn profits of:

A) $27.

B) $54.

C) $18.

D) $78.

A) $27.

B) $54.

C) $18.

D) $78.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

8

In a perfectly competitive industry, the long-run equilibrium price is $12. If a technological innovation lowers production costs, the long-run equilibrium price will:

A) fall below $12.

B) initially fall but then return to $12.

C) initially rise but then return to $12.

D) rise above $12.

A) fall below $12.

B) initially fall but then return to $12.

C) initially rise but then return to $12.

D) rise above $12.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

9

Suppose that the market for painting services is perfectly competitive. Painting companies are identical; their long-run cost functions are given by .

Market demand is

) The long-run equilibrium quantity in this industry is ____.

A) 5,000

B) 4,750

C) 2,500

D) 1,900

.Market demand is

) The long-run equilibrium quantity in this industry is ____.

A) 5,000

B) 4,750

C) 2,500

D) 1,900

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

10

Suppose that a firm is earning a 12% return on capital in a perfectly competitive industry, and the market return outside the industry is 9.5%. Which of the following statements is (are) TRUE?

A) In the short run, the firm is making a below-market return of 2.5%.

B) In the short run, the firm is making a negative return on capital of 2.5%.

C) In the long run, the firm's return on capital will be 0%.

D) In the long run, the firm's return on capital will be 9.5%.

A) In the short run, the firm is making a below-market return of 2.5%.

B) In the short run, the firm is making a negative return on capital of 2.5%.

C) In the long run, the firm's return on capital will be 0%.

D) In the long run, the firm's return on capital will be 9.5%.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

11

A firm's short-run total cost is TC = 10,100 + 7,700Q - 100Q2 + Q3/3, and its marginal cost is MC = 7,700 - 200Q + Q2. What is the firm's shutdown price?

A) $45

B) $200

C) $1,100

D) $18

A) $45

B) $200

C) $1,100

D) $18

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

12

Suppose that the market for painting services is perfectly competitive. Painting companies are identical; their long-run cost functions are given by .

Market demand is

) The long-run equilibrium price in this industry is $____.

A) 194.5

B) 173.5

C) 162.5

D) 155.5

.Market demand is

) The long-run equilibrium price in this industry is $____.

A) 194.5

B) 173.5

C) 162.5

D) 155.5

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

13

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost: where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

, where N is the number of firms. Market demand is

) In the long-run equilibrium, the market price is $ ____.

A) 30.675

B) 26.875

C) 22.775

D) 21.345

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals , where N is the number of firms. Market demand is

) In the long-run equilibrium, the market price is $ ____.

A) 30.675

B) 26.875

C) 22.775

D) 21.345

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

14

In a perfectly competitive industry, the equilibrium price is $56 and the minimum average total cost of the industry's firms is $40. If this is a constant-cost industry, we can expect that in the long run, firms will _____ the market, shifting the industry's short-run supply curve _____.

A) enter; outward until the minimum average total cost rises to $56

B) enter; outward until the new equilibrium price is $40

C) enter; inward until firms are making positive profit

D) exit; inward until firms are breaking even

A) enter; outward until the minimum average total cost rises to $56

B) enter; outward until the new equilibrium price is $40

C) enter; inward until firms are making positive profit

D) exit; inward until firms are breaking even

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

15

(Figure: Firm I) At the profit maximizing quantity, the firm's total revenue is $____.

A) 240

B) 200

C) 120

D) 0

A) 240

B) 200

C) 120

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

16

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2. In long-run equilibrium, the market price is $____.

A) 660

B) 550

C) 440

D) 330

A) 660

B) 550

C) 440

D) 330

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

17

(Figure; Price and Quantity VII) If this firm operates, it earns a profit of _____, but if it shuts down, it earns a profit of _____.

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

A) $4,000; $0

B) -$9,000; -$5,000

C) -$5,000; -$9,000

D) -$2,500; -$4,000

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

18

(Figure: Price and Quantity IX) What could have caused the supply and average variable cost curves to shift outward?

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

A) a decrease in average fixed costs

B) a decrease in wages

C) an increase in input prices

D) an increase in rental payments or property taxes

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

19

Economists assume that firms maximize:

A) the difference between marginal revenue and marginal cost.

B) TR = PQ.

C) π = TR - TC.

D) P - ATC, the profit per unit of output.

A) the difference between marginal revenue and marginal cost.

B) TR = PQ.

C) π = TR - TC.

D) P - ATC, the profit per unit of output.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is (are) TRUE?

I) Free entry to a perfectly competitive industry results in the industry's firms earning zero economic profit in the long run, except for the most efficient producers, who may earn economic rent.

II) In a perfectly competitive market, long-run equilibrium is characterized by LMC < P < LATC.

III) If a competitive industry is in long-run equilibrium, a decrease in demand causes firms to earn negative profit because the market price will fall below average total cost.

A) I, II, and III

B) II and III

C) I and III

D) I

I) Free entry to a perfectly competitive industry results in the industry's firms earning zero economic profit in the long run, except for the most efficient producers, who may earn economic rent.

II) In a perfectly competitive market, long-run equilibrium is characterized by LMC < P < LATC.

III) If a competitive industry is in long-run equilibrium, a decrease in demand causes firms to earn negative profit because the market price will fall below average total cost.

A) I, II, and III

B) II and III

C) I and III

D) I

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

21

(Figure: Price and Quantity VI) Economic profit for this firm can be calculated as:

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

A) (160 - 130) × 80.

B) (160 × 80) - 30.

C) 80 - 30.

D) (160 - 30) × 80.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

22

Use the following table to answer the question. At the profit maximizing quantity, the marginal revenue is $____.

A) 15

B) 12

C) 10

D) 7

A) 15

B) 12

C) 10

D) 7

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

23

(Figure: Profit-Maximizing Output Level I) At the profit maximizing quantity, the slope of the total cost curve is ____.

A) 7

B) 5

C) 3

D) 1/2

A) 7

B) 5

C) 3

D) 1/2

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

24

(Figure: Price and Quantity X) In this perfectly competitive industry, there are 100 firms with a short-run supply curve represented by S1 and 50 firms with a short-run supply curve represented by S2. At a market price of $4.50, industry output is:

A) 700.

B) 250.

C) 1,050.

D) 500.

A) 700.

B) 250.

C) 1,050.

D) 500.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

25

Suppose that the perfectly competitive market for granola bars is made up of identical firms with long-run total cost functions given by TC(Q) = 8Q3 - 40Q2 + 200Q. Assume that these cost functions are independent of the number of firms in the market and that firms may enter or exit the market freely. Market demand is QD = 8,000 - 3.5P, where price is in cents. The long-run equilibrium price is $____.

A) 2.00

B) 1.75

C) 1.50

D) 1.25

A) 2.00

B) 1.75

C) 1.50

D) 1.25

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

26

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by . The quantity at which average total cost is minimized for each firm is ____.

A) 4.5

B) 3.5

C) 2.5

D) 1.5

. The quantity at which average total cost is minimized for each firm is ____.A) 4.5

B) 3.5

C) 2.5

D) 1.5

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

27

In a perfectly competitive market, each firm has a long-run total cost given by LTC = 100Q - 10Q2 + 1/3Q3 and long-run marginal cost curve given by LMC = 100 - 20Q + Q2. What is the market's long-run equilibrium price?

A) $8.50

B) $33

C) $70

D) $25

A) $8.50

B) $33

C) $70

D) $25

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

28

If the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3, in the long run, the marginal cost is:

A) 1,000.

B) 100Q - 10Q2 + Q3.

C) 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2.

A) 1,000.

B) 100Q - 10Q2 + Q3.

C) 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

29

A firm should _____ output whenever MR exceeds MC because _____.

A) reduce; revenues will rise by more than costs, increasing the firm's profit

B) reduce; total revenues exceed total costs

C) expand; revenues will rise by more than costs, increasing the firm's profit

D) not change; selling more output will increase marginal revenue by less than marginal cost

A) reduce; revenues will rise by more than costs, increasing the firm's profit

B) reduce; total revenues exceed total costs

C) expand; revenues will rise by more than costs, increasing the firm's profit

D) not change; selling more output will increase marginal revenue by less than marginal cost

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

30

Suppose that each firm in a perfectly competitive market has a short-run total cost of TC = 75 + 500Q - 5Q2 + 0.5Q3, where MC = 500 - 10Q + 1.5Q2. The output that minimizes the firm's AVC is ____.

A) 10

B) 7

C) 5

D) 0

A) 10

B) 7

C) 5

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

31

(Figure: Firm I) At the profit maximizing quantity, the firm's profit is $____.

A) 150

B) 100

C) 50

D) 0

A) 150

B) 100

C) 50

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

32

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; their long-run cost functions are given by . Market demand is

) In the long-run equilibrium in this industry, there are ____ firms in the industry.

A) 4,124.72

B) 3,941.83

C) 3,663.46

D) 3,276.32

. Market demand is ) In the long-run equilibrium in this industry, there are ____ firms in the industry.

A) 4,124.72

B) 3,941.83

C) 3,663.46

D) 3,276.32

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

33

In the market for lock washers, a perfectly competitive market, the current equilibrium price is $5 per box. Washer King, one of the many producers of washers, has a daily short-run total cost given by TC = 190 + 0.20Q + 0.0025Q2, where Q measures boxes of washers. Washer King's corresponding marginal cost is MC = 0.20 + 0.005Q. How many boxes of washers should Washer King produce per day to maximize profit?

A) 280

B) 960

C) 1,450

D) 2,125

A) 280

B) 960

C) 1,450

D) 2,125

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

34

Suppose that a firm is producing where MR > MC. If the firm produced one more unit of output, total revenue would ____ and total cost would ____.

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

35

Suppose that each firm in a perfectly competitive market has a short-run total cost of TC = 75 + 500Q - 5Q2 + 0.5Q3, where MC = 500 - 10Q + 1.5Q2. The firm's shutdown price is $____.

A) 500

B) 487.50

C) 480

D) 477.50

A) 500

B) 487.50

C) 480

D) 477.50

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

36

(Figure: Price and Quantity I) The graph shows a firm's marginal cost curve. This firm operates in a perfectly competitive industry with market demand and supply curves given by Qd = 100 - 8P and QS = -20 + 2P, where Q is measured in millions of units. Based on the figure, how many units of output will the firm produce at the equilibrium price?

A) 1,100

B) 800

C) 1,200

D) 400

A) 1,100

B) 800

C) 1,200

D) 400

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

37

Suppose that the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3. Also, suppose there is free entry and exit. To find the quantity where ATC is minimized, solve the following equation for Q:

A) 100 - 20Q + 3Q2 = 1,000 + 100Q - 10Q2 + Q3.

B) 100 - 20Q + 3Q2 = 100 - 10Q + Q2.

C) 100 - 20Q + 3Q2 = 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2 = 1,000(Q + 100 - 10Q + Q2).

A) 100 - 20Q + 3Q2 = 1,000 + 100Q - 10Q2 + Q3.

B) 100 - 20Q + 3Q2 = 100 - 10Q + Q2.

C) 100 - 20Q + 3Q2 = 1,000/Q + 100 - 10Q + Q2.

D) 100 - 20Q + 3Q2 = 1,000(Q + 100 - 10Q + Q2).

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

38

Suppose that a firm is producing where 0 < MR < MC. If the firm produced one less unit of output, total revenue would ____ and total cost would ____.

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

39

If the long-run total cost curve for each firm is given by TC = 500Q - 20Q2 + Q3, where Q is the quantity of the product, in the long run, the marginal cost is:

A) 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2.

C) 500 - 20Q + Q2.

D) -20Q2 + Q3.

A) 500Q - 20Q2 + Q3.

B) 500 - 40Q + 3Q2.

C) 500 - 20Q + Q2.

D) -20Q2 + Q3.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

40

Suppose the market for sprouts is in long-run equilibrium. In the short run, what will happen if an E. coli outbreak reduces the demand for sprouts?

A) The marginal cost curve will shift downward for each producer, leaving prices unchanged.

B) The market price of sprouts will fall, causing each firm to produce fewer sprouts.

C) Existing firms will expand output to make up for the decrease in demand.

D) The marginal cost curve will shift upward for each producer, causing prices to rise and profits to fall.

A) The marginal cost curve will shift downward for each producer, leaving prices unchanged.

B) The market price of sprouts will fall, causing each firm to produce fewer sprouts.

C) Existing firms will expand output to make up for the decrease in demand.

D) The marginal cost curve will shift upward for each producer, causing prices to rise and profits to fall.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

41

In the lemonade stand industry, Lucia is representative of a low-cost provider and Carlos is representative of a high-cost provider. The minimum average total cost of the high-cost producers is $5. The low-cost producers have a long-run total cost curve given by LTC = 5Q -1.5Q2 + 0.33Q3, where LMC = 5 - 3Q + Q2. In this case, Lucia can earn an economic rent of $____ for being a low-cost producer.

A) 9

B) 7.50

C) 6

D) 4.50

A) 9

B) 7.50

C) 6

D) 4.50

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following statements is (are) TRUE of price-taking firms?

I) ΔTR/ΔQ = P = MR

II) Price takers must lower their price to sell additional units of output because demand curves slope downward.

III) If a price taker decides to increase output, the market price will decrease.

IV) Examples of price takers include McDonald's, Burger King, Wendy's, and SONIC Drive-in.

A) II and III

B) I, II, III, and IV

C) I

D) II and IV

I) ΔTR/ΔQ = P = MR

II) Price takers must lower their price to sell additional units of output because demand curves slope downward.

III) If a price taker decides to increase output, the market price will decrease.

IV) Examples of price takers include McDonald's, Burger King, Wendy's, and SONIC Drive-in.

A) II and III

B) I, II, III, and IV

C) I

D) II and IV

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

43

Use the following table to answer the question. The profit maximizing level of output is a quantity of ____.

A) 4

B) 3

C) 2

D) 1

A) 4

B) 3

C) 2

D) 1

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

44

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by . The marginal cost curve for a firm in this industry is MC (Q) = ____.

A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

. The marginal cost curve for a firm in this industry is MC (Q) = ____.A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

45

(Figure: Market for Walnuts I) The graph depicts the perfectly competitive market for walnuts. Which of the following statements is (are) TRUE? I. The demand curve facing a walnut grower is perfectly elastic at $1.

II) If a walnut grower sold 80,000 pounds of walnuts, his total revenue would be $138,400.

III) If a walnut grower sold one more pound of walnuts, his total revenue would increase by $1.73.

A) I, II, and III

B) II

C) II and III

D) I

I. The demand curve facing a walnut grower is perfectly elastic at $1.II) If a walnut grower sold 80,000 pounds of walnuts, his total revenue would be $138,400.

III) If a walnut grower sold one more pound of walnuts, his total revenue would increase by $1.73.

A) I, II, and III

B) II

C) II and III

D) I

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

46

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; they have long-run cost functions given by . The quantity at which average total cost is minimized is ____.

A) 4.5

B) 3.5

C) 2.5

D) 1.5

. The quantity at which average total cost is minimized is ____.A) 4.5

B) 3.5

C) 2.5

D) 1.5

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

47

Pitch (a sticky black substance made from petroleum) is a key input in the production of clay targets. If the price of pitch falls, clay target manufacturers will encounter an _____ shift of their marginal cost curve and an_____ shift of their average variable cost.

A) inward; inward

B) outward; outward

C) inward; outward

D) outward; inward

A) inward; inward

B) outward; outward

C) inward; outward

D) outward; inward

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

48

Marginal cost can be calculated as:

A) the derivative of total cost with respect to quantity.

B) the derivative of variable cost with respect to quantity.

C) Either option

D) Neither option

A) the derivative of total cost with respect to quantity.

B) the derivative of variable cost with respect to quantity.

C) Either option

D) Neither option

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

49

(Figure: Price and Quantity IV) Which of the following statements is (are) TRUE? I. The firm earns $120 of profit at 24 units of output.

II) At prices above $5, the firm earns positive profit.

III) At a price of $4, the firm would produce more than 24 units of output to offset the lower price.

A) I

B) II and III

C) II

D) I and III

I. The firm earns $120 of profit at 24 units of output.II) At prices above $5, the firm earns positive profit.

III) At a price of $4, the firm would produce more than 24 units of output to offset the lower price.

A) I

B) II and III

C) II

D) I and III

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

50

A perfectly competitive industry has 100 high-cost producers, each with a short-run supply curve given by QH = 16P, and 100 low-cost producers, each with a short-run supply curve given by QL = 24P.

The industry demand curve is given by Qd = 100,000 - 1,000P. At market equilibrium, industry producer surplus is:

A) $800,000.

B) $20,000.

C) $4,000.

D) $1.2 million.

The industry demand curve is given by Qd = 100,000 - 1,000P. At market equilibrium, industry producer surplus is:

A) $800,000.

B) $20,000.

C) $4,000.

D) $1.2 million.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

51

(Figure: Firm I) At the profit maximizing quantity, the firm's total cost is $____.

A) 200

B) 150

C) 80

D) 0

A) 200

B) 150

C) 80

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

52

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2. The industry's demand curve is QD = 40,000 - 70P. In long-run equilibrium, the number of firms in the industry is ____.

A) 60

B) 50

C) 40

D) 30

A) 60

B) 50

C) 40

D) 30

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

53

Under free entry and exit, to find the quantity where ATC is minimized, the firm can:

A) set marginal cost equal to average total cost and solve for Q.

B) take the first-order condition of average total cost with respect to Q and solve for Q.

C) Either A or B

D) Neither A nor B

A) set marginal cost equal to average total cost and solve for Q.

B) take the first-order condition of average total cost with respect to Q and solve for Q.

C) Either A or B

D) Neither A nor B

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

54

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; they have long-run cost functions given by . The marginal cost curve for each firm in this industry is MC(Q) = ____.

A) 3Q2 - 6Q + 90

B) Q2 - 3Q + 90

C) Q3 - 3Q2 + 90Q

D) 3Q3 - 6Q2 + 90Q

. The marginal cost curve for each firm in this industry is MC(Q) = ____.A) 3Q2 - 6Q + 90

B) Q2 - 3Q + 90

C) Q3 - 3Q2 + 90Q

D) 3Q3 - 6Q2 + 90Q

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

55

Suppose that the market for ice cream sandwiches is perfectly competitive. Firms that produce ice cream sandwiches are identical; their long-run cost functions are given by . Market demand is

) The long-run equilibrium quantity in this industry is ____.

A) 6,215.25

B) 6,100.25

C) 5,912.25

D) 5,845.25

. Market demand is ) The long-run equilibrium quantity in this industry is ____.

A) 6,215.25

B) 6,100.25

C) 5,912.25

D) 5,845.25

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

56

Suppose that the market for painting services is perfectly competitive. Painting companies are identical and have long-run cost functions given by . The average total cost curve for a firm in this industry is ATC (Q) = ____.

A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

. The average total cost curve for a firm in this industry is ATC (Q) = ____.A) 18Q2 - 60Q + 200

B) 6Q2 - 30Q + 200

C) 6Q3 - 30Q2 + 200Q

D) 18Q3 - 30Q2 + 200Q

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

57

Suppose that a firm is producing where 0 < MR < MC. If the firm produced one less unit of output, total revenue would ____ and profit would ____.

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

A) increase; increase

B) increase; decrease

C) decrease; increase

D) decrease; decrease

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

58

The perfectly competitive firm's short-run supply curve is:

A) the portion of its marginal cost curve that lies above average variable cost.

B) the portion of its marginal cost curve that lies above average total cost.

C) its average variable cost curve, which lies above marginal revenue.

D) its average total cost curve, which lies above marginal revenue.

A) the portion of its marginal cost curve that lies above average variable cost.

B) the portion of its marginal cost curve that lies above average total cost.

C) its average variable cost curve, which lies above marginal revenue.

D) its average total cost curve, which lies above marginal revenue.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

59

(Figure: Price and Quantity of Output I) At a market price of $9, the firm is willing to supply ____ units of the good.

A) 8

B) 7

C) 3

D) 0

A) 8

B) 7

C) 3

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

60

With which of the following scenarios should a perfectly competitive firm shut down in the short run?

I) P = $80, VC = $180,000, and Q = 2,000

II) TR = $45,000, AVC = $500, ATC = $600, and Q = $84

III) P = $11.55, ATC = $15, and AFC = $2

A) II

B) III

C) II and III

D) I and III

I) P = $80, VC = $180,000, and Q = 2,000

II) TR = $45,000, AVC = $500, ATC = $600, and Q = $84

III) P = $11.55, ATC = $15, and AFC = $2

A) II

B) III

C) II and III

D) I and III

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

61

(Figure: Price and Quantity XII) Which of the following statements is (are) TRUE? I. In the long run, this firm will produce 500 units of output.

II) In the short run, this firm produces 600 units of output.

III) The long-run equilibrium price is $4.

IV) At a price of $5, new firms will eventually enter the market, eliminating this firm's economic profits.

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

I. In the long run, this firm will produce 500 units of output.II) In the short run, this firm produces 600 units of output.

III) The long-run equilibrium price is $4.

IV) At a price of $5, new firms will eventually enter the market, eliminating this firm's economic profits.

A) I, II, III, and IV

B) III and IV

C) I and II

D) III

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

62

A street vendor's annual license fee was recently increased by the city. The street vendor's:

A) marginal cost curve will shift out, along with her average variable cost curve.

B) marginal cost curve will shift in, along with her average variable cost curve.

C) marginal and average variable cost curves will not be affected.

D) total variable cost curve will rotate upward.

A) marginal cost curve will shift out, along with her average variable cost curve.

B) marginal cost curve will shift in, along with her average variable cost curve.

C) marginal and average variable cost curves will not be affected.

D) total variable cost curve will rotate upward.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

63

Why is the type of product sold in an industry an important characteristic?

A) A firm that can differentiate its product from that of rivals may be able to charge a higher price for a superior product.

B) A firm that sells intangible goods is usually considered a monopoly.

C) Expensive products are usually sold by perfectly competitive firms.

D) Service industries cannot differentiate their products, which makes it easy for new firms to enter the industry.

A) A firm that can differentiate its product from that of rivals may be able to charge a higher price for a superior product.

B) A firm that sells intangible goods is usually considered a monopoly.

C) Expensive products are usually sold by perfectly competitive firms.

D) Service industries cannot differentiate their products, which makes it easy for new firms to enter the industry.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

64

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2. The industry's demand curve is QD = 40,000 - 70P. In long-run equilibrium, the total quantity purchase by consumers is ____.

A) 2,000

B) 1,800

C) 1,500

D) 1,200

A) 2,000

B) 1,800

C) 1,500

D) 1,200

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

65

(Figure: Perfectly Competitive Firms I) The graph represents three perfectly competitive firms. Which of the following statements is (are) TRUE? I. In the long run, each firm will produce the same quantity of output.

II) Firm 1 is the highest-cost producer and Firm 3 is the lowest-cost producer.

III) Firm 3 will produce the most output in the long run.

A) II

B) III

C) II and III

D) I

I. In the long run, each firm will produce the same quantity of output.II) Firm 1 is the highest-cost producer and Firm 3 is the lowest-cost producer.

III) Firm 3 will produce the most output in the long run.

A) II

B) III

C) II and III

D) I

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

66

(Figure: Price and Quantity of Output and Table I) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. At a market price of $100, the industry output is ____.

A) 15

B) 9.5

C) 4

D) 1

A) 15

B) 9.5

C) 4

D) 1

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

67

(Figure: Price and Quantity of Output I) At a market price of $18, the firm is willing to supply ____ units of the good.

A) 8

B) 7

C) 5

D) 0

A) 8

B) 7

C) 5

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

68

(Figure: Representative Firm I) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

A) panel a

B) panel b

C) panel c

D) panel d

A) panel a

B) panel b

C) panel c

D) panel d

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

69

(Figure: Price and Quantity of Output I) At a market price of $27, the firm is willing to supply ____ units of the good.

A) 8

B) 7

C) 5

D) 0

A) 8

B) 7

C) 5

D) 0

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

70

A perfectly competitive firm maximizes profit by producing 500 units of output, selling each unit for $10. The firm's average variable cost is $7 and average fixed cost is $2. What is the firm's producer surplus?

A) $500

B) $1,500

C) $1,000

D) $1

A) $500

B) $1,500

C) $1,000

D) $1

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

71

(Figure: Price and Quantity of Output and Table I) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph. At a market price of $20, the industry output is ____.

A) 15

B) 9.5

C) 4

D) 1

A) 15

B) 9.5

C) 4

D) 1

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

72

(Figure: Price and Quantity II) This firm maximizes profit by producing _____ units of output.

A) 3

B) 7

C) 10

D) 12

A) 3

B) 7

C) 10

D) 12

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

73

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost: where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

, where N is the number of firms. Market demand is

) In the long-run equilibrium, there are ____ firms in the industry.

A) 59.375

B) 55.475

C) 51.685

D) 44.985

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals , where N is the number of firms. Market demand is

) In the long-run equilibrium, there are ____ firms in the industry.

A) 59.375

B) 55.475

C) 51.685

D) 44.985

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

74

Suppose the long-run equilibrium price in a perfectly competitive market is $100. When demand increases, if it is a(n) _____ industry, the long-run equilibrium price will _____ to reflect a _____ long-run average total cost.

A) decreasing-cost; rise; lower

B) increasing-cost; rise; lower

C) decreasing-cost; fall; lower

D) increasing-cost; fall; higher

A) decreasing-cost; rise; lower

B) increasing-cost; rise; lower

C) decreasing-cost; fall; lower

D) increasing-cost; fall; higher

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

75

(Figure: Profit-Maximizing Output Level I) At the profit maximizing quantity, the slope of the total revenue curve is ____.

A) 7

B) 5

C) 4

D) 3

A) 7

B) 5

C) 4

D) 3

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

76

(Figure: Long Run Output I) Initially, the constant-cost industry was in long-run equilibrium at point A when the demand for the good increased to D2. How much output will be produced in the long run as a result of the demand increase?

A) 3,000

B) 5,000

C) 6,000

D) 7,000

A) 3,000

B) 5,000

C) 6,000

D) 7,000

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

77

In a perfectly competitive market with 2,000 firms, output is zero at prices less than $10. At prices of $10 to $19.99, each firm will produce 100 units of output. At any price of $20 or more, each firm will produce 300 units of output. As this industry expands output, however, prices of the key inputs to production increase substantially. The total industry output at a market price of $33 is:

A) between 200,000 and 800,000.

B) 600,000 or less.

C) greater than 600,000.

D) 800,000.

A) between 200,000 and 800,000.

B) 600,000 or less.

C) greater than 600,000.

D) 800,000.

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

78

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost: where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

, where N is the number of firms. Market demand is

) In the long-run equilibrium, the total industry output is ____.

A) 296.875

B) 287.475

C) 237.685

D) 224.985

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals , where N is the number of firms. Market demand is

) In the long-run equilibrium, the total industry output is ____.

A) 296.875

B) 287.475

C) 237.685

D) 224.985

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

79

Use the following table to answer the question. At a quantity of 1, the total cost is $____.

A) 15

B) 12

C) 10

D) 7

A) 15

B) 12

C) 10

D) 7

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

80

(Figure: Price and Quantity XI) Which of the following statements is (are) TRUE? I. Producer surplus = TR - VC = $25 - $15.

II) The shaded area between the demand curve and marginal cost represents producer surplus and equals $10.

III) The firm's profit = $10 - FC.

A) I, II, and III

B) II

C) I and III

D) III

I. Producer surplus = TR - VC = $25 - $15.II) The shaded area between the demand curve and marginal cost represents producer surplus and equals $10.

III) The firm's profit = $10 - FC.

A) I, II, and III

B) II

C) I and III

D) III

Unlock Deck

Unlock for access to all 148 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 148 flashcards in this deck.