Exam 8: Supply in a Competitive Market

Exam 1: Adventures in Microeconomics20 Questions

Exam 2: Supply and Demand148 Questions

Exam 3: Using Supply and Demand to Analyze Markets146 Questions

Exam 4: Consumer Behavior130 Questions

Exam 5: Individual and Market Demand146 Questions

Exam 6: Producer Behavior142 Questions

Exam 7: Costs179 Questions

Exam 8: Supply in a Competitive Market148 Questions

Exam 9: Market Power and Monopoly162 Questions

Exam 10: Market Power and Pricing Strategies165 Questions

Exam 11: Imperfect Competition172 Questions

Exam 12: Game Theory170 Questions

Exam 13: Factor Markets94 Questions

Exam 14: Investment, Time, and Insurance117 Questions

Exam 15: General Equilibrium97 Questions

Exam 16: Asymmetric Information106 Questions

Exam 17: Externalities and Public Goods114 Questions

Exam 18: Behavioral and Experimental Economics112 Questions

Select questions type

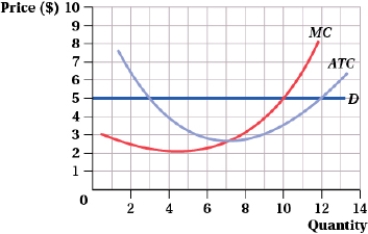

(Figure: Price and Quantity II) This firm maximizes profit by producing _____ units of output.

Free

(Multiple Choice)

4.8/5  (42)

(42)

Correct Answer: Verified

Verified

C

A perfectly competitive industry consists of many identical firms, each with a long-run average total cost of LATC = 800 - 10Q + 0.1Q2 and long-run marginal cost of LMC = 800 - 20Q + 0.3Q2. The industry's demand curve is QD = 40,000 - 70P. In long-run equilibrium, the number of firms in the industry is ____.

Free

(Multiple Choice)

4.9/5 (34)

Correct Answer:Verified

D

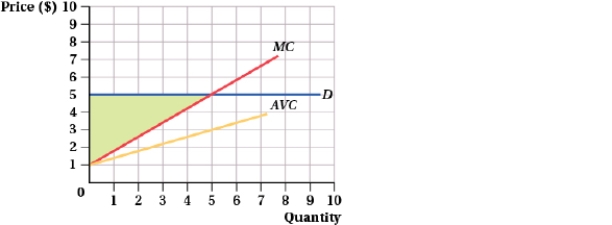

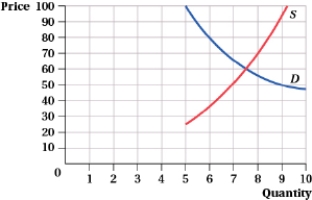

(Figure: Price and Quantity XI) Which of the following statements is (are) TRUE?  I. Producer surplus = TR - VC = $25 - $15.

II) The shaded area between the demand curve and marginal cost represents producer surplus and equals $10.

III) The firm's profit = $10 - FC.

I. Producer surplus = TR - VC = $25 - $15.

II) The shaded area between the demand curve and marginal cost represents producer surplus and equals $10.

III) The firm's profit = $10 - FC.

Free

(Multiple Choice)

4.8/5 (32)

Correct Answer:Verified

A

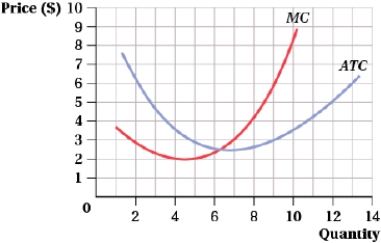

(Figure: Price and Quantity III) If the market price is $6, this perfectly competitive firm will earn profits of:

(Multiple Choice)

4.9/5 (27)

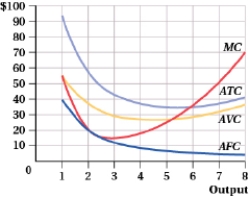

Suppose that each firm in a perfectly competitive market has a short-run total cost of TC = 75 + 500Q - 5Q2 + 0.5Q3, where MC = 500 - 10Q + 1.5Q2. The output that minimizes the firm's AVC is ____.

(Multiple Choice)

4.8/5 (37)

Suppose that the market for gourmet deli sandwiches is perfectly competitive and that the supply of workers in this industry is upward-sloping, so that wages increase as industry output increases. Delis in this market face the following total cost:  where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals

where Q is the number of sandwiches and W is the daily wage paid to workers. The wage, which depends on total industry output, equals  , where N is the number of firms. Market demand is

, where N is the number of firms. Market demand is  ) In the long-run equilibrium, the total industry output is ____.

) In the long-run equilibrium, the total industry output is ____.

(Multiple Choice)

4.9/5 (33)

Suppose that a firm is producing where 0 < MR < MC. If the firm produced one less unit of output, total revenue would ____ and total cost would ____.

(Multiple Choice)

4.9/5 (42)

Suppose the market for sprouts is in long-run equilibrium. In the short run, what will happen if an E. coli outbreak reduces the demand for sprouts?

(Multiple Choice)

4.9/5 (47)

Suppose that a firm is producing where MR > MC. If the firm produced one more unit of output, total revenue would ____ and total cost would ____.

(Multiple Choice)

4.8/5 (34)

Suppose that the long-run total cost curve for each firm is given by TC = 1,000 + 100Q - 10Q2 + Q3. Also, suppose there is free entry and exit. To find the quantity where ATC is minimized, solve the following equation for Q:

(Multiple Choice)

4.8/5 (37)

A perfectly competitive industry in long-run equilibrium comprises 200 identical firms. In one of the firms, the workers unionize and receive a 20% wage increase. What happens to the unionized firm in the short run and the long run? Supplement your answer with a graph.

(Essay)

4.9/5 (31)

Suppose that there are 1,000 firms in a perfectly competitive industry, each with a short-run total cost curve given by TC = 800 + 8Q + 0.1Q2 and marginal cost curve given by MC = 8 + 0.2Q. The short-run profit-maximizing output level for each firm at a market price of $20 is ____.

(Multiple Choice)

4.7/5 (23)

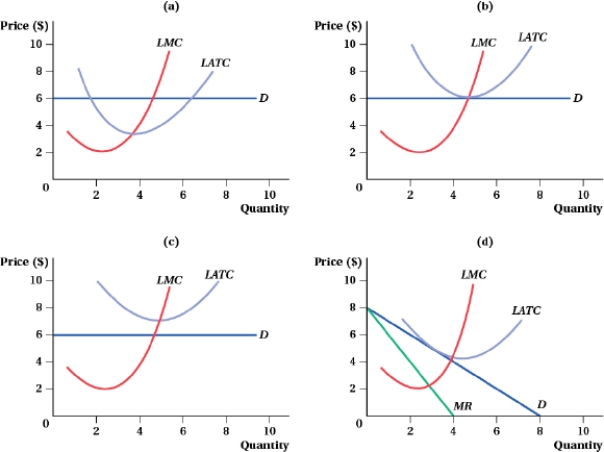

(Figure: Representative Firm I) Which panel shows a representative firm (operating in a perfectly competitive industry) in a long-run equilibrium?

(Multiple Choice)

4.9/5 (32)

(Graph: Short-Run Equilibrium I)

Using the graphs, indicate the short-run equilibrium in this market and calculate any associated profits.

(Essay)

4.8/5 (40)

Suppose a perfectly competitive industry has 300 firms, and the short-run supply curve for each firm is given by Q = 2P. What is the short-run industry supply curve?

(Multiple Choice)

4.7/5 (36)

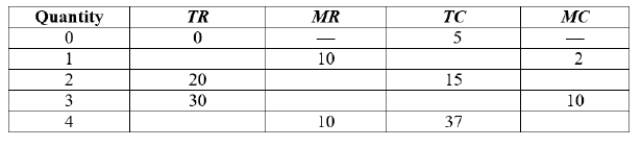

Use the following table to answer the question. At a quantity of 2, the marginal revenue is $____.

(Multiple Choice)

4.9/5 (28)

Suppose that the cost curves of the firms do not change when (identical) firms enter or exit the market. Under this scenario, a change in demand will _____ in a change in the market quantity because the number of firms will _____.

(Multiple Choice)

4.8/5 (41)

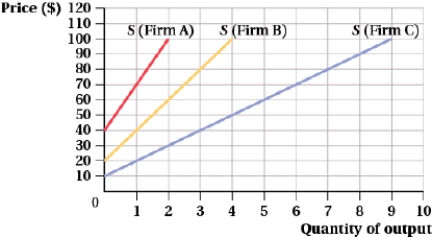

(Figure: Price and Quantity of Output and Table I) For simplicity, assume that there are only three firms in a perfectly competitive industry; their short-run supply curves are depicted in the graph.  Complete the following table.

Complete the following table.

(Essay)

4.9/5 (36)

(Figure: Revenues and Output I) The total revenue curve for a perfectly competitive firm is represented by curve:

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)