Deck 10: Credit Analysis Models

Full screen (f)

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

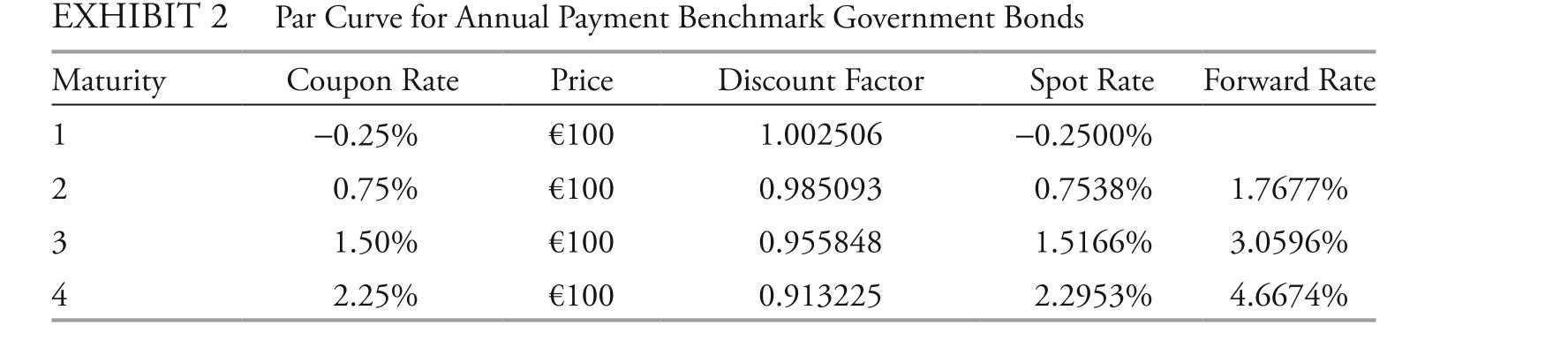

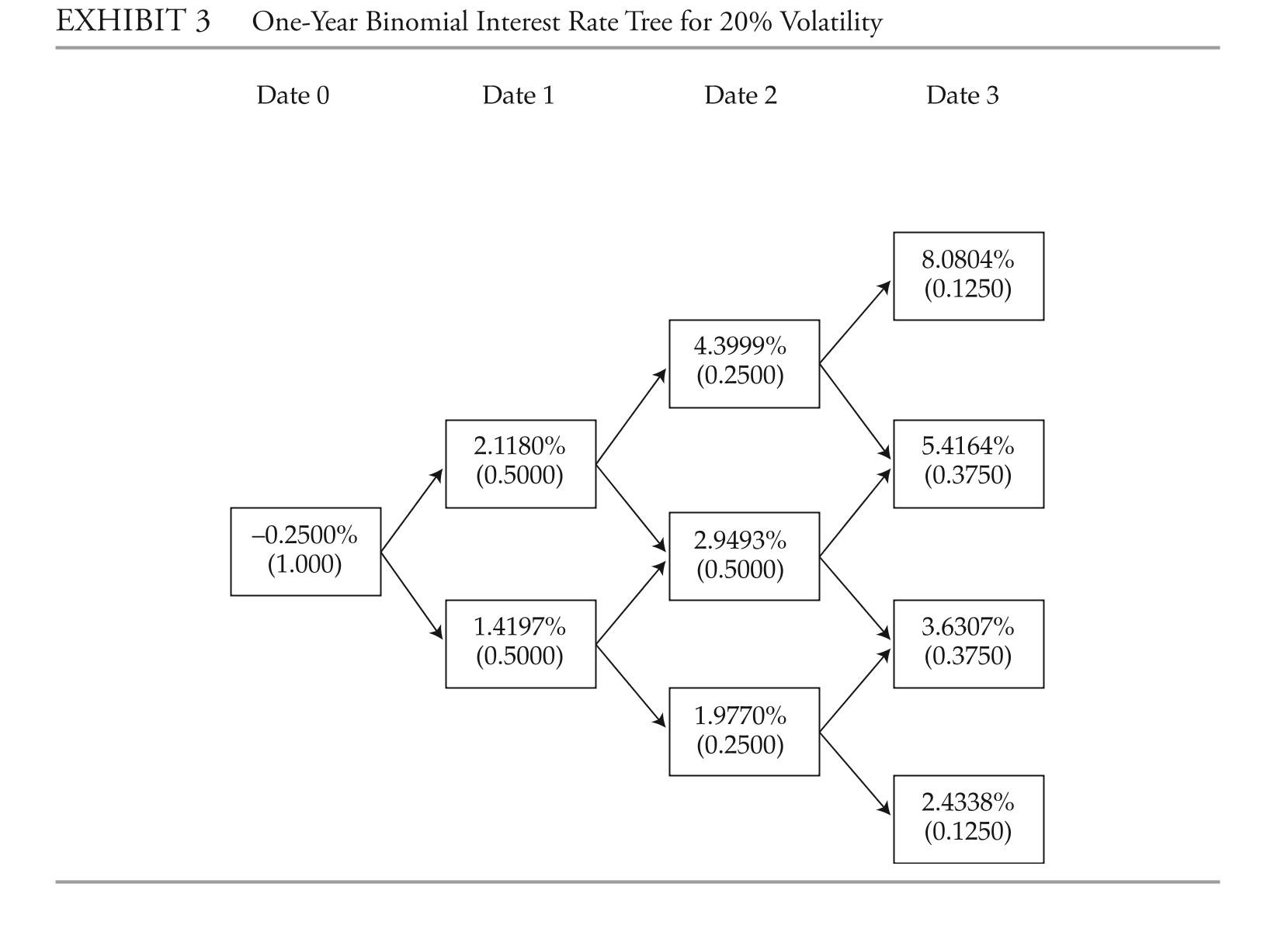

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The wealth management firm has an existing position in bond b4. The market price of b4, a floating-rate note, is €1,070. Senior management has asked ibarra to make a recom-

Mendation regarding the existing position. based on the assumptions used to calculate the

Estimated fair value only, her recommendation should be to:

A) add to the existing position.

B) hold the existing position.

C) reduce the existing position.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The wealth management firm has an existing position in bond b4. The market price of b4, a floating-rate note, is €1,070. Senior management has asked ibarra to make a recom-

Mendation regarding the existing position. based on the assumptions used to calculate the

Estimated fair value only, her recommendation should be to:

A) add to the existing position.

B) hold the existing position.

C) reduce the existing position.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

ibarra wants to know the credit spread of bond b2 over a theoretical comparable-maturity government bond with the same coupon rate as this bond. The foregoing credit spread is

Closest to:

A) 108 bps.

B) 101 bps.

C) 225 bps.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

ibarra wants to know the credit spread of bond b2 over a theoretical comparable-maturity government bond with the same coupon rate as this bond. The foregoing credit spread is

Closest to:

A) 108 bps.

B) 101 bps.

C) 225 bps.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

Floating-rate note b4 is currently rated bbb by Standard & Poor's and Fitch ratings (and baa by Moody's investors Service). based on the research department assumption about

The probability of default in Question 10 and her own assumption in Question 11, which

Action does ibarra most likely expect from the credit rating agencies?

A) downgrade from bbb to bb

B) Upgrade from bbb to aaa

C) Place the issuer on watch with a positive outlook

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

Floating-rate note b4 is currently rated bbb by Standard & Poor's and Fitch ratings (and baa by Moody's investors Service). based on the research department assumption about

The probability of default in Question 10 and her own assumption in Question 11, which

Action does ibarra most likely expect from the credit rating agencies?

A) downgrade from bbb to bb

B) Upgrade from bbb to aaa

C) Place the issuer on watch with a positive outlook

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The fair value of bond b2 is closest to:

A) €1,069.34.

B) €1,111.51.

C) €1,153.68.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The fair value of bond b2 is closest to:

A) €1,069.34.

B) €1,111.51.

C) €1,153.68.

Question

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and

lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-

edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued by

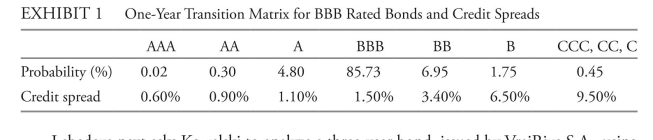

entre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and

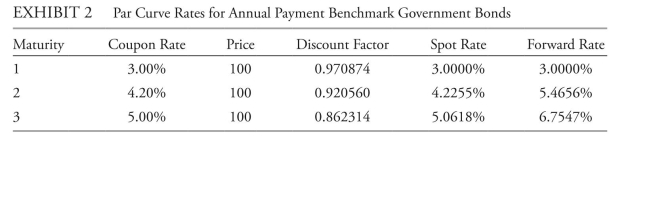

yields will remain stable over the year. lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using

lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using

an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a

par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3.

Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as well

Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as well

as the fair value of the bond. She then estimates the bond's yield to maturity and the bond's

credit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause

the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.

Kowalski tells lebedeva:

Statement 1: The credit term structure for the most highly rated securities tends to be either

flat or slightly upward sloping.

Statement 2: The credit term structure for lower-rated securities is often steeper, and credit

spreads widen with expectations of strong economic growth.

next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuer

with a strong, competitive position. her focus is to determine the rationale for a positively

sloped credit spread term structure.

lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool

is made up of many medium-term auto loans that are homogeneous, and each loan is small

relative to the total value of the pool.

Which of Kowalski's statements regarding the term structure of credit spreads is correct?

A) only Statement 1

B) only Statement 2

C) both Statement 1 and Statement 2

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and

lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-

edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued by

entre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and

yields will remain stable over the year.

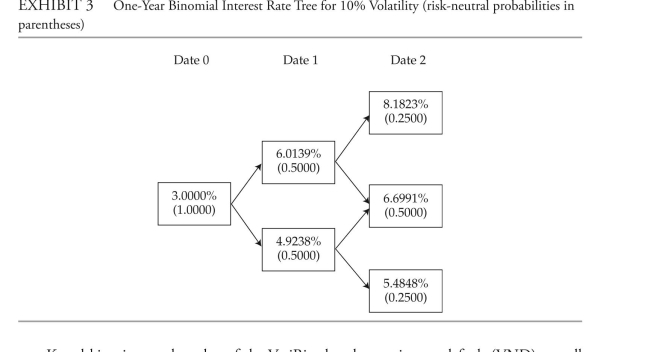

lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., usingan arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a

par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3.

Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond's

credit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause

the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.

Kowalski tells lebedeva:

Statement 1: The credit term structure for the most highly rated securities tends to be either

flat or slightly upward sloping.

Statement 2: The credit term structure for lower-rated securities is often steeper, and credit

spreads widen with expectations of strong economic growth.

next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuer

with a strong, competitive position. her focus is to determine the rationale for a positively

sloped credit spread term structure.

lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool

is made up of many medium-term auto loans that are homogeneous, and each loan is small

relative to the total value of the pool.

Which of Kowalski's statements regarding the term structure of credit spreads is correct?

A) only Statement 1

B) only Statement 2

C) both Statement 1 and Statement 2

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

Koning realizes that an increase in the recovery rate would lead to an increase in the bond's fair value, whereas an increase in the probability of default would lead to a decrease in the

Bond's fair value. he is not sure which effect would be greater, however. So, he increases

Both the recovery rate and the probability of default by 25% of their existing estimates

And recomputes the bond's fair value. The recomputed fair value is closest to:

A) €843.14.

B) €848.00.

C) €855.91.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

Koning realizes that an increase in the recovery rate would lead to an increase in the bond's fair value, whereas an increase in the probability of default would lead to a decrease in the

Bond's fair value. he is not sure which effect would be greater, however. So, he increases

Both the recovery rate and the probability of default by 25% of their existing estimates

And recomputes the bond's fair value. The recomputed fair value is closest to:

A) €843.14.

B) €848.00.

C) €855.91.

Question

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and

lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-

edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued by

entre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and

yields will remain stable over the year. lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using

an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a

par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as well

as the fair value of the bond. She then estimates the bond's yield to maturity and the bond's

credit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause

the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.

Kowalski tells lebedeva:

Statement 1: The credit term structure for the most highly rated securities tends to be either

flat or slightly upward sloping.

Statement 2: The credit term structure for lower-rated securities is often steeper, and credit

spreads widen with expectations of strong economic growth.

next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuer

with a strong, competitive position. her focus is to determine the rationale for a positively

sloped credit spread term structure.

lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool

is made up of many medium-term auto loans that are homogeneous, and each loan is small

relative to the total value of the pool.

The most appropriate response to Kowalski's question regarding credit rating migration is that it has:

A) a negative impact.

B) no impact.

C) a positive impact.

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and

lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-

edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued by

entre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and

yields will remain stable over the year.

lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., usingan arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a

par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3.

Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond's

credit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause

the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.

Kowalski tells lebedeva:

Statement 1: The credit term structure for the most highly rated securities tends to be either

flat or slightly upward sloping.

Statement 2: The credit term structure for lower-rated securities is often steeper, and credit

spreads widen with expectations of strong economic growth.

next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuer

with a strong, competitive position. her focus is to determine the rationale for a positively

sloped credit spread term structure.

lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool

is made up of many medium-term auto loans that are homogeneous, and each loan is small

relative to the total value of the pool.

The most appropriate response to Kowalski's question regarding credit rating migration is that it has:

A) a negative impact.

B) no impact.

C) a positive impact.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

bond b3 will have a modified duration of 2.75 at the end of the year. based on the rep- resentative one-year corporate transition matrix in exhibit 7 of the reading and assuming

No default, how should the analyst adjust the bond's yield to maturity (ytM) to assess the

Expected return on the bond over the next year?

A) add 7.7 bps to ytM.

B) Subtract 7.7 bps from ytM.

C) Subtract 9.0 bps from ytM.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

bond b3 will have a modified duration of 2.75 at the end of the year. based on the rep- resentative one-year corporate transition matrix in exhibit 7 of the reading and assuming

No default, how should the analyst adjust the bond's yield to maturity (ytM) to assess the

Expected return on the bond over the next year?

A) add 7.7 bps to ytM.

B) Subtract 7.7 bps from ytM.

C) Subtract 9.0 bps from ytM.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

as previously mentioned, ibarra is considering a future interest rate volatility of 20% and an upward-sloping yield curve, as shown in exhibit 2. based on her analysis, the fair value

Of bond b2 is closest to:

A) €1,101.24.

B) €1,141.76.

C) €1,144.63.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

as previously mentioned, ibarra is considering a future interest rate volatility of 20% and an upward-sloping yield curve, as shown in exhibit 2. based on her analysis, the fair value

Of bond b2 is closest to:

A) €1,101.24.

B) €1,141.76.

C) €1,144.63.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The issuer of the floating-rate note b4 is in the energy industry. ibarra personally believes that oil prices are likely to increase significantly within the next year, which will lead to an

Improvement in the firm's financial health and a decline in the probability of default from 1.50% in year 1 to 0.50% in years 2, 3, and 4. based on these expectations, which of the

Following statements is correct?

A) The cVa will decrease to €22.99.

B) The note's fair value will increase to €1,177.26.

C) The value of the Frn, assuming no default, will increase to €1,173.55.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The issuer of the floating-rate note b4 is in the energy industry. ibarra personally believes that oil prices are likely to increase significantly within the next year, which will lead to an

Improvement in the firm's financial health and a decline in the probability of default from 1.50% in year 1 to 0.50% in years 2, 3, and 4. based on these expectations, which of the

Following statements is correct?

A) The cVa will decrease to €22.99.

B) The note's fair value will increase to €1,177.26.

C) The value of the Frn, assuming no default, will increase to €1,173.55.

Question

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and

lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-

edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued by

entre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and

yields will remain stable over the year. lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using

an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a

par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as well

as the fair value of the bond. She then estimates the bond's yield to maturity and the bond's

credit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause

the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.

Kowalski tells lebedeva:

Statement 1: The credit term structure for the most highly rated securities tends to be either

flat or slightly upward sloping.

Statement 2: The credit term structure for lower-rated securities is often steeper, and credit

spreads widen with expectations of strong economic growth.

next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuer

with a strong, competitive position. her focus is to determine the rationale for a positively

sloped credit spread term structure.

lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool

is made up of many medium-term auto loans that are homogeneous, and each loan is small

relative to the total value of the pool.

The most appropriate response to Kowalski's question relating to the credit spread is:

A) an increase in the hazard rate.

B) an increase in the loss given default.

C) a decrease in the risk-neutral probability of default.

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and

lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-

edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued by

entre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and

yields will remain stable over the year.

lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., usingan arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a

par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3.

Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond's

credit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause

the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.

Kowalski tells lebedeva:

Statement 1: The credit term structure for the most highly rated securities tends to be either

flat or slightly upward sloping.

Statement 2: The credit term structure for lower-rated securities is often steeper, and credit

spreads widen with expectations of strong economic growth.

next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuer

with a strong, competitive position. her focus is to determine the rationale for a positively

sloped credit spread term structure.

lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool

is made up of many medium-term auto loans that are homogeneous, and each loan is small

relative to the total value of the pool.

The most appropriate response to Kowalski's question relating to the credit spread is:

A) an increase in the hazard rate.

B) an increase in the loss given default.

C) a decrease in the risk-neutral probability of default.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

in the presentation, lok is asked why the research team chose to use a reduced-form credit model instead of a structural model. Which statement is he likely to make in reply?

A) Structural models are outdated, having been developed in the 1970s; reduced-form models are more modern, having been developed in the 1990s.

B) Structural models are overly complex because they require use of option pricing mod- els, whereas reduced-form models use regression analysis.

C) Structural models require "inside" information known to company management, whereas reduced-form models can use publicly available data on the firm.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

in the presentation, lok is asked why the research team chose to use a reduced-form credit model instead of a structural model. Which statement is he likely to make in reply?

A) Structural models are outdated, having been developed in the 1970s; reduced-form models are more modern, having been developed in the 1990s.

B) Structural models are overly complex because they require use of option pricing mod- els, whereas reduced-form models use regression analysis.

C) Structural models require "inside" information known to company management, whereas reduced-form models can use publicly available data on the firm.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

ibarra is interested in analyzing how a simultaneous decrease in the recovery rate and the probability of default would affect the fair value of bond b2. She decreases both the

Recovery rate and the probability of default by 25% of their existing estimates and recom-

Putes the bond's fair value. The recomputed fair value is closest to:

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

ibarra is interested in analyzing how a simultaneous decrease in the recovery rate and the probability of default would affect the fair value of bond b2. She decreases both the

Recovery rate and the probability of default by 25% of their existing estimates and recom-

Putes the bond's fair value. The recomputed fair value is closest to:

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

during the presentation about how the research team estimates the probability of default for a particular bond issuer, lok is asked for his thoughts on the shape of the

Term structure of credit spreads. Which statement is he most likely to include in his

Response?

A) The term structure of credit spreads typically is flat or slightly upward sloping for high-quality investment-grade bonds. high-yield bonds are more sensitive to the

Credit cycle, however, and can have a more upwardly sloped term structure of credit

Spreads than investment-grade bonds or even an inverted curve.

B) The term structure of credit spreads for corporate bonds is always upward sloping, the more so the weaker the credit quality because probabilities of default are positively

Correlated with the time to maturity.

C) There is no consistent pattern to the term structure of credit spreads. The shape of the credit term structure depends entirely on industry factors.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

during the presentation about how the research team estimates the probability of default for a particular bond issuer, lok is asked for his thoughts on the shape of the

Term structure of credit spreads. Which statement is he most likely to include in his

Response?

A) The term structure of credit spreads typically is flat or slightly upward sloping for high-quality investment-grade bonds. high-yield bonds are more sensitive to the

Credit cycle, however, and can have a more upwardly sloped term structure of credit

Spreads than investment-grade bonds or even an inverted curve.

B) The term structure of credit spreads for corporate bonds is always upward sloping, the more so the weaker the credit quality because probabilities of default are positively

Correlated with the time to maturity.

C) There is no consistent pattern to the term structure of credit spreads. The shape of the credit term structure depends entirely on industry factors.

Question

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,

the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-

sion. The rounded results are reported in the solutions.

The final question to lok is about covered bonds. The person asking says, "i've heard about them but don't know what they are." Which statement is lok most likely to make

To describe a covered bond?

A) a covered bond is issued in a non-domestic currency. The currency risk is then fully hedged using a currency swap or a package of foreign exchange forward contracts.

B) a covered bond is issued with an attached credit default swap. it essentially is a "risk- free" government bond.

C) a covered bond is a senior debt obligation giving recourse to the issuer as well as a predetermined underlying collateral pool, often commercial or residential mortgages.

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-

ment firm. Marten Koning is a junior analyst in the same department, and david lok is a

member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some

similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1

includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed

bond description

b1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth

management firm's research team has estimated that the risk-neutral probability of

default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is

30%.

b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.

ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the

analysis with the assumptions that there is no interest rate volatility and that the government

bond yield curve is flat at 3%.

ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest

rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses

these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-

tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning, the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra,

the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve preci-