Exam 10: Credit Analysis Models

Exam 1: Fixed-Income Securities: Defining Elements28 Questions

Exam 2: Fixed-Income Markets: Issuance, Trading, and Funding31 Questions

Exam 3: Introduction to Fixed-Income Valuation44 Questions

Exam 4: Introduction to Asset-Backed Securities42 Questions

Exam 5: Understanding Fixed Income Risk and Return27 Questions

Exam 6: Fundamentals of Credit Analysis45 Questions

Exam 7: The Term Structure and Interest Rate Dynamics56 Questions

Exam 8: The Arbitrage-Free Valuation Framework17 Questions

Exam 9: Valuation and Analysis of Bonds With Embedded Options36 Questions

Exam 10: Credit Analysis Models30 Questions

Exam 11: Credit Default Swaps15 Questions

Exam 12: Overview of Fixed-Income Portfolio Management12 Questions

Exam 13: Liability-Driven and Index-Based Strategies26 Questions

Exam 14: Yield Curve Strategies32 Questions

Exam 15: Fixed-Income Active Management: Credit Strategies15 Questions

Select questions type

The following information relates to Questions

lena liecken is a senior bond analyst at taurus investment Management. Kristel Kreming,

a junior analyst, works for liecken in helping conduct fixed-income research for the firm's

portfolio managers. liecken and Kreming meet to discuss several bond positions held in the

firm's portfolios.

bonds i and ii both have a maturity of one year, an annual coupon rate of 5%, and a mar-

ket price equal to par value. The risk-free rate is 3%. historical default experiences of bonds

comparable to bonds i and ii are presented in exhibit 1.

EXHIBIT 1 Credit Risk Information for Comparable Bonds

Percentage of Bonds That Survive and Make Full Bond Recovery Rate Payment I 40\% 98\% II 35\% 99\%

Bond III

Bond III is a zero-coupon bond with three years to maturity. Liecken evaluates similar bonds and estimates a recovery rate of and a risk-neutral default probability of , assuming conditional probabilities of default. Kreming creates Exhibit 2 to compute Bond III's credit valuation adjustment. She assumes a flat yield curve at , with exposure, recovery, and loss given default values expressed per 100 of par value.

EXHIBIT 2 Analysis of Bond III Date Exposure Recovery Loss Given Default Probability of Default Probability of Survival Expected Loss Present Value of Expected Loss 0 1 94.2596 35.8186 58.4410 2.0000\% 98.0000\% 1.1688 1.1348 2 97.0874 36.8932 60.1942 1.9600\% 96.0400\% 1.1798 1.1121 3 100.0000 38.0000 62.0000 94.1192\% Sum 5.8808\% 3.5395 3.3367

Bond IV

Bond IV is an AA rated bond that matures in five years, has a coupon rate of , and a modified duration of 4.2. Liecken is concerned about whether this bond will be downgraded to an A rating, but she does not expect the bond to default during the next year. Kreming constructs a partial transition matrix, which is presented in Exhibit 3, and suggests using a model to predict the rating change of Bond IV using leverage ratios, return on assets, and macroeconomic variables.

EXHIBIT 3 Partial One-Year Corporate Transition Matrix (entries in \%) From/To AAA AA A AAA 92.00 6.00 1.00 AA 2.00 89.00 8.00 A 0.05 1.00 85.00 Credit Spread (\%) 0.50 1.00 1.75

Default Probabilities

Kreming calculates the risk-neutral probabilities, compares them with the actual default probabilities of bonds evaluated over the past 10 years, and observes that the actual and risk-neutral probabilities differ. She makes two observations regarding the comparison of these probabilities:

Observation 1: Actual default probabilities include the default risk premium associated with the uncertainty in the timing of the possible default loss.

Observation 2: The observed spread over the yield on a risk-free bond in practice includes liquidity and tax considerations, in addition to credit risk.

-Which of Kreming's observations regarding actual and risk-neutral default probabilities is correct?

Free

(Multiple Choice)

4.9/5  (27)

(27)

Correct Answer: Verified

Verified

B

The following information relates to Questions

lena liecken is a senior bond analyst at taurus investment Management. Kristel Kreming,

a junior analyst, works for liecken in helping conduct fixed-income research for the firm's

portfolio managers. liecken and Kreming meet to discuss several bond positions held in the

firm's portfolios.

bonds i and ii both have a maturity of one year, an annual coupon rate of 5%, and a mar-

ket price equal to par value. The risk-free rate is 3%. historical default experiences of bonds

comparable to bonds i and ii are presented in exhibit 1.

EXHIBIT 1 Credit Risk Information for Comparable Bonds

Percentage of Bonds That Survive and Make Full Bond Recovery Rate Payment I 40\% 98\% II 35\% 99\%

Bond III

Bond III is a zero-coupon bond with three years to maturity. Liecken evaluates similar bonds and estimates a recovery rate of and a risk-neutral default probability of , assuming conditional probabilities of default. Kreming creates Exhibit 2 to compute Bond III's credit valuation adjustment. She assumes a flat yield curve at , with exposure, recovery, and loss given default values expressed per 100 of par value.

EXHIBIT 2 Analysis of Bond III Date Exposure Recovery Loss Given Default Probability of Default Probability of Survival Expected Loss Present Value of Expected Loss 0 1 94.2596 35.8186 58.4410 2.0000\% 98.0000\% 1.1688 1.1348 2 97.0874 36.8932 60.1942 1.9600\% 96.0400\% 1.1798 1.1121 3 100.0000 38.0000 62.0000 94.1192\% Sum 5.8808\% 3.5395 3.3367

Bond IV

Bond IV is an AA rated bond that matures in five years, has a coupon rate of , and a modified duration of 4.2. Liecken is concerned about whether this bond will be downgraded to an A rating, but she does not expect the bond to default during the next year. Kreming constructs a partial transition matrix, which is presented in Exhibit 3, and suggests using a model to predict the rating change of Bond IV using leverage ratios, return on assets, and macroeconomic variables.

EXHIBIT 3 Partial One-Year Corporate Transition Matrix (entries in \%) From/To AAA AA A AAA 92.00 6.00 1.00 AA 2.00 89.00 8.00 A 0.05 1.00 85.00 Credit Spread (\%) 0.50 1.00 1.75

Default Probabilities

Kreming calculates the risk-neutral probabilities, compares them with the actual default probabilities of bonds evaluated over the past 10 years, and observes that the actual and risk-neutral probabilities differ. She makes two observations regarding the comparison of these probabilities:

Observation 1: Actual default probabilities include the default risk premium associated with the uncertainty in the timing of the possible default loss.

Observation 2: The observed spread over the yield on a risk-free bond in practice includes liquidity and tax considerations, in addition to credit risk.

-based on exhibit 1, the expected future value of bond i at maturity is closest to:

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

B

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

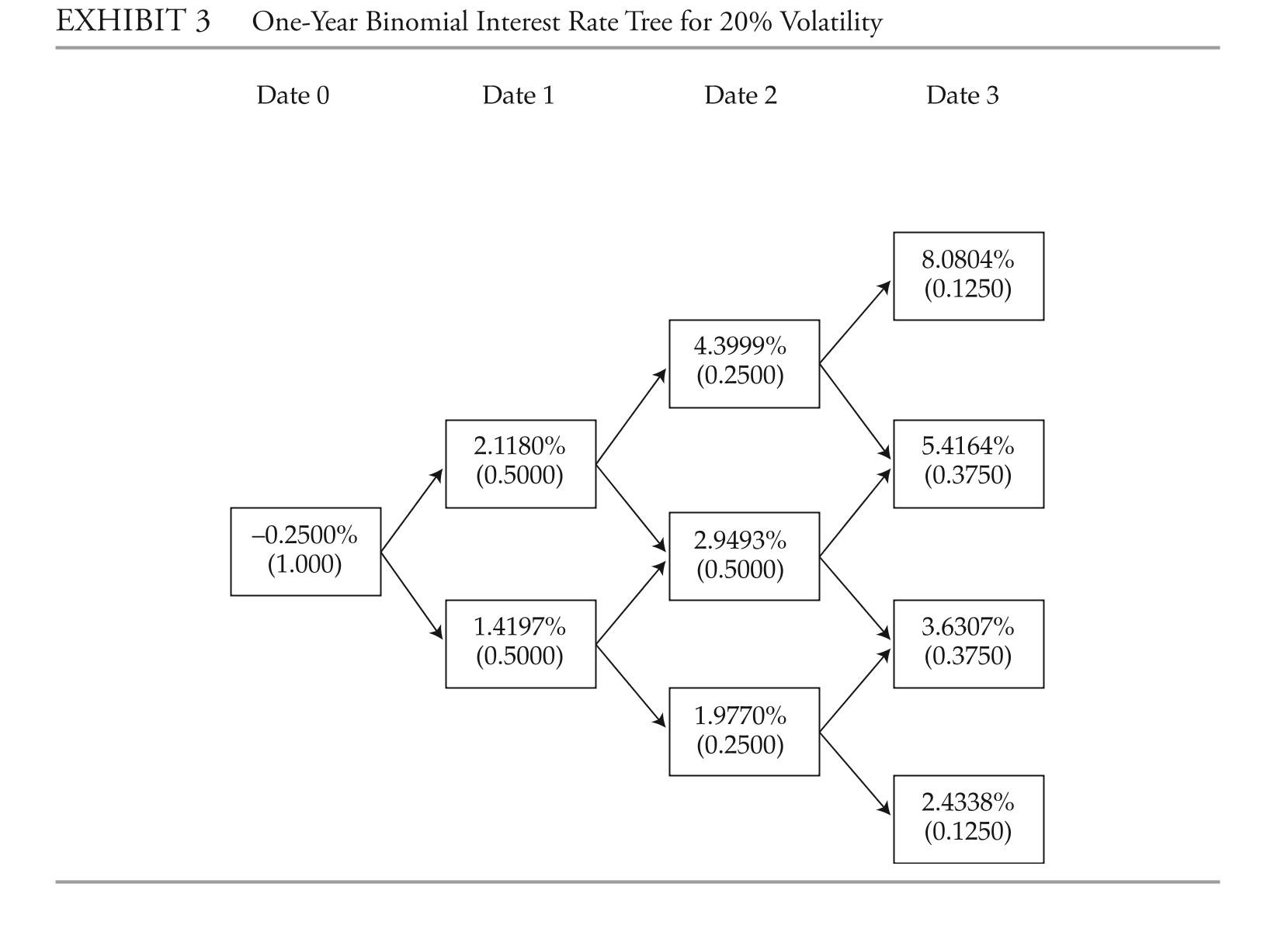

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\%  answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-in the presentation, lok is asked why the research team chose to use a reduced-form credit model instead of a structural model. Which statement is he likely to make in reply?

answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-in the presentation, lok is asked why the research team chose to use a reduced-form credit model instead of a structural model. Which statement is he likely to make in reply?

Free

(Multiple Choice)

4.7/5 (42)

Correct Answer:Verified

C

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-The fair value of bond b2 is closest to:

(Multiple Choice)

4.8/5 (36)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-The issuer of the floating-rate note b4 is in the energy industry. ibarra personally believes that oil prices are likely to increase significantly within the next year, which will lead to an

Improvement in the firm's financial health and a decline in the probability of default from 1.50% in year 1 to 0.50% in years 2, 3, and 4. based on these expectations, which of the

Following statements is correct?

(Multiple Choice)

4.7/5 (29)

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued byentre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

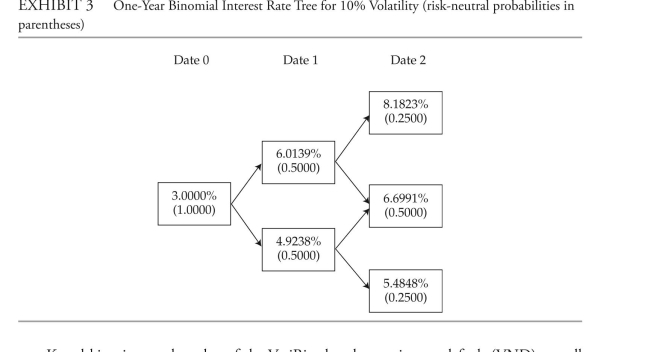

credit transition and credit spread data in exhibit 1. She assumes that market spreads and yields will remain stable over the year. EXHIBIT 1 One-Year Transition Matrix for BBB Rated Bonds and Credit Spreads AAA AA A BBB BB B CCC, CC, C Probability (\%) 0.02 0.30 4.80 85.73 6.95 1.75 0.45 Credit spread 0.60\% 0.90\% 1.10\% 1.50\% 3.40\% 6.50\% 9.50\% lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. EXHIBIT 2 Par Curve Rates for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 3.00\% 100 0.970874 3.0000\% 3.0000\% 2 4.20\% 100 0.920560 4.2255\% 5.4656\% 3 5.00\% 100 0.862314 5.0618\% 6.7547\%  Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond'scredit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.Kowalski tells lebedeva:Statement 1: The credit term structure for the most highly rated securities tends to be either flat or slightly upward sloping.Statement 2: The credit term structure for lower-rated securities is often steeper, and creditspreads widen with expectations of strong economic growth.next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuerwith a strong, competitive position. her focus is to determine the rationale for a positively sloped credit spread term structure.lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool is made up of many medium-term auto loans that are homogeneous, and each loan is small relative to the total value of the pool.

-The most appropriate response to Kowalski's question relating to the credit spread is:

Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond'scredit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.Kowalski tells lebedeva:Statement 1: The credit term structure for the most highly rated securities tends to be either flat or slightly upward sloping.Statement 2: The credit term structure for lower-rated securities is often steeper, and creditspreads widen with expectations of strong economic growth.next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuerwith a strong, competitive position. her focus is to determine the rationale for a positively sloped credit spread term structure.lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool is made up of many medium-term auto loans that are homogeneous, and each loan is small relative to the total value of the pool.

-The most appropriate response to Kowalski's question relating to the credit spread is:

(Multiple Choice)

4.9/5 (44)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-The market price of bond b1 is €875. The bond is:

(Multiple Choice)

4.7/5 (28)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-bond b3 will have a modified duration of 2.75 at the end of the year. based on the rep- resentative one-year corporate transition matrix in exhibit 7 of the reading and assuming

No default, how should the analyst adjust the bond's yield to maturity (ytM) to assess the

Expected return on the bond over the next year?

(Multiple Choice)

4.9/5 (27)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-david lok has estimated the probability of default of bond b1 to be 1.50%. he is pre- senting the approach the research team used to estimate the probability of default. Which

Of the following statements is lok likely to make in his presentation if the team used a

Reduced-form credit model?

(Multiple Choice)

4.7/5 (36)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-The wealth management firm has an existing position in bond b4. The market price of b4, a floating-rate note, is €1,070. Senior management has asked ibarra to make a recom-

Mendation regarding the existing position. based on the assumptions used to calculate the

Estimated fair value only, her recommendation should be to:

(Multiple Choice)

4.9/5 (37)

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued byentre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and yields will remain stable over the year. EXHIBIT 1 One-Year Transition Matrix for BBB Rated Bonds and Credit Spreads AAA AA A BBB BB B CCC, CC, C Probability (\%) 0.02 0.30 4.80 85.73 6.95 1.75 0.45 Credit spread 0.60\% 0.90\% 1.10\% 1.50\% 3.40\% 6.50\% 9.50\% lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. EXHIBIT 2 Par Curve Rates for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 3.00\% 100 0.970874 3.0000\% 3.0000\% 2 4.20\% 100 0.920560 4.2255\% 5.4656\% 3 5.00\% 100 0.862314 5.0618\% 6.7547\% Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond'scredit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.Kowalski tells lebedeva:Statement 1: The credit term structure for the most highly rated securities tends to be either flat or slightly upward sloping.Statement 2: The credit term structure for lower-rated securities is often steeper, and creditspreads widen with expectations of strong economic growth.next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuerwith a strong, competitive position. her focus is to determine the rationale for a positively sloped credit spread term structure.lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool is made up of many medium-term auto loans that are homogeneous, and each loan is small relative to the total value of the pool.

-dll's credit spread term structure is most consistent with the firm having:

(Multiple Choice)

4.8/5 (34)

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued byentre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and yields will remain stable over the year. EXHIBIT 1 One-Year Transition Matrix for BBB Rated Bonds and Credit Spreads AAA AA A BBB BB B CCC, CC, C Probability (\%) 0.02 0.30 4.80 85.73 6.95 1.75 0.45 Credit spread 0.60\% 0.90\% 1.10\% 1.50\% 3.40\% 6.50\% 9.50\% lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. EXHIBIT 2 Par Curve Rates for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 3.00\% 100 0.970874 3.0000\% 3.0000\% 2 4.20\% 100 0.920560 4.2255\% 5.4656\% 3 5.00\% 100 0.862314 5.0618\% 6.7547\% Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond'scredit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.Kowalski tells lebedeva:Statement 1: The credit term structure for the most highly rated securities tends to be either flat or slightly upward sloping.Statement 2: The credit term structure for lower-rated securities is often steeper, and creditspreads widen with expectations of strong economic growth.next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuerwith a strong, competitive position. her focus is to determine the rationale for a positively sloped credit spread term structure.lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool is made up of many medium-term auto loans that are homogeneous, and each loan is small relative to the total value of the pool.

-The most appropriate response to Kowalski's question regarding credit rating migration is that it has:

(Multiple Choice)

4.9/5 (39)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-ibarra wants to know the credit spread of bond b2 over a theoretical comparable-maturity government bond with the same coupon rate as this bond. The foregoing credit spread is

Closest to:

(Multiple Choice)

5.0/5 (34)

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued byentre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and yields will remain stable over the year. EXHIBIT 1 One-Year Transition Matrix for BBB Rated Bonds and Credit Spreads AAA AA A BBB BB B CCC, CC, C Probability (\%) 0.02 0.30 4.80 85.73 6.95 1.75 0.45 Credit spread 0.60\% 0.90\% 1.10\% 1.50\% 3.40\% 6.50\% 9.50\% lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. EXHIBIT 2 Par Curve Rates for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 3.00\% 100 0.970874 3.0000\% 3.0000\% 2 4.20\% 100 0.920560 4.2255\% 5.4656\% 3 5.00\% 100 0.862314 5.0618\% 6.7547\% Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond'scredit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.Kowalski tells lebedeva:Statement 1: The credit term structure for the most highly rated securities tends to be either flat or slightly upward sloping.Statement 2: The credit term structure for lower-rated securities is often steeper, and creditspreads widen with expectations of strong economic growth.next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuerwith a strong, competitive position. her focus is to determine the rationale for a positively sloped credit spread term structure.lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool is made up of many medium-term auto loans that are homogeneous, and each loan is small relative to the total value of the pool.

-based on Kowalski's assumptions and exhibits 2 and 3, the credit spread on the Vrairive bond is closest to:

(Multiple Choice)

4.8/5 (37)

The following information relates to Questions

lena liecken is a senior bond analyst at taurus investment Management. Kristel Kreming,

a junior analyst, works for liecken in helping conduct fixed-income research for the firm's

portfolio managers. liecken and Kreming meet to discuss several bond positions held in the

firm's portfolios.

bonds i and ii both have a maturity of one year, an annual coupon rate of 5%, and a mar-

ket price equal to par value. The risk-free rate is 3%. historical default experiences of bonds

comparable to bonds i and ii are presented in exhibit 1.

EXHIBIT 1 Credit Risk Information for Comparable Bonds

Percentage of Bonds That Survive and Make Full Bond Recovery Rate Payment I 40\% 98\% II 35\% 99\%

Bond III

Bond III is a zero-coupon bond with three years to maturity. Liecken evaluates similar bonds and estimates a recovery rate of and a risk-neutral default probability of , assuming conditional probabilities of default. Kreming creates Exhibit 2 to compute Bond III's credit valuation adjustment. She assumes a flat yield curve at , with exposure, recovery, and loss given default values expressed per 100 of par value.

EXHIBIT 2 Analysis of Bond III Date Exposure Recovery Loss Given Default Probability of Default Probability of Survival Expected Loss Present Value of Expected Loss 0 1 94.2596 35.8186 58.4410 2.0000\% 98.0000\% 1.1688 1.1348 2 97.0874 36.8932 60.1942 1.9600\% 96.0400\% 1.1798 1.1121 3 100.0000 38.0000 62.0000 94.1192\% Sum 5.8808\% 3.5395 3.3367

Bond IV

Bond IV is an AA rated bond that matures in five years, has a coupon rate of , and a modified duration of 4.2. Liecken is concerned about whether this bond will be downgraded to an A rating, but she does not expect the bond to default during the next year. Kreming constructs a partial transition matrix, which is presented in Exhibit 3, and suggests using a model to predict the rating change of Bond IV using leverage ratios, return on assets, and macroeconomic variables.

EXHIBIT 3 Partial One-Year Corporate Transition Matrix (entries in \%) From/To AAA AA A AAA 92.00 6.00 1.00 AA 2.00 89.00 8.00 A 0.05 1.00 85.00 Credit Spread (\%) 0.50 1.00 1.75

Default Probabilities

Kreming calculates the risk-neutral probabilities, compares them with the actual default probabilities of bonds evaluated over the past 10 years, and observes that the actual and risk-neutral probabilities differ. She makes two observations regarding the comparison of these probabilities:

Observation 1: Actual default probabilities include the default risk premium associated with the uncertainty in the timing of the possible default loss.

Observation 2: The observed spread over the yield on a risk-free bond in practice includes liquidity and tax considerations, in addition to credit risk.

-based on exhibit 1, the loss given default for bond ii is:

(Multiple Choice)

4.8/5 (38)

The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

EXHIBIT 2 Par Curve for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 -0.25\% 100 1.002506 -0.2500\% 2 0.75\% 100 0.985093 0.7538\% 1.7677\% 3 1.50\% 100 0.955848 1.5166\% 3.0596\% 4 2.25\% 100 0.913225 2.2953\% 4.6674\% answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-The final question to lok is about covered bonds. The person asking says, "i've heard about them but don't know what they are." Which statement is lok most likely to make

To describe a covered bond?

(Multiple Choice)

4.9/5 (37)

The following information relates to Questions

anna lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and lebedeva meet to review several positions in lebedeva's portfolio.

lebedeva begins the meeting by discussing credit rating migration. Kowalski asks leb-edeva about the typical impact of credit rating migration on the expected return on a bond.

lebedeva asks Kowalski to estimate the expected return over the next year on a bond issued byentre corp. The bbb rated bond has a yield to maturity of 5.50% and a modified duration of 7.54. Kowalski calculates the expected return on the bond over the next year given the partial

credit transition and credit spread data in exhibit 1. She assumes that market spreads and yields will remain stable over the year. EXHIBIT 1 One-Year Transition Matrix for BBB Rated Bonds and Credit Spreads AAA AA A BBB BB B CCC, CC, C Probability (\%) 0.02 0.30 4.80 85.73 6.95 1.75 0.45 Credit spread 0.60\% 0.90\% 1.10\% 1.50\% 3.40\% 6.50\% 9.50\% lebedeva next asks Kowalski to analyze a three-year bond, issued by Vrairive S.a., using an arbitrage-free framework. The bond's coupon rate is 5%, with interest paid annually and a par value of 100. in her analysis, she makes the following three assumptions:

• The annual interest rate volatility is 10%.

• The recovery rate is one-third of the exposure each period.

• The hazard rate, or conditional probability of default each year, is 2.00%.

Selected information on benchmark government bonds for the Vrairive bond is presented

in exhibit 2, and the relevant binomial interest rate tree is presented in exhibit 3. EXHIBIT 2 Par Curve Rates for Annual Payment Benchmark Government Bonds Maturity Coupon Rate Price Discount Factor Spot Rate Forward Rate 1 3.00\% 100 0.970874 3.0000\% 3.0000\% 2 4.20\% 100 0.920560 4.2255\% 5.4656\% 3 5.00\% 100 0.862314 5.0618\% 6.7547\% Kowalski estimates the value of the Vrairive bond assuming no default (Vnd) as wellas the fair value of the bond. She then estimates the bond's yield to maturity and the bond'scredit spread over the benchmark in exhibit 2. Kowalski asks lebedeva, "What might cause the bond's credit spread to decrease?"

lebedeva and Kowalski next discuss the drivers of the term structure of credit spreads.Kowalski tells lebedeva:Statement 1: The credit term structure for the most highly rated securities tends to be either flat or slightly upward sloping.Statement 2: The credit term structure for lower-rated securities is often steeper, and creditspreads widen with expectations of strong economic growth.next, Kowalski analyzes the outstanding bonds of dll corporation, a high-quality issuerwith a strong, competitive position. her focus is to determine the rationale for a positively sloped credit spread term structure.lebedeva ends the meeting by asking Kowalski to recommend a credit analysis approach

for a securitized asset-backed security (abS) held in the portfolio. This non-static asset pool is made up of many medium-term auto loans that are homogeneous, and each loan is small relative to the total value of the pool.

-Given the description of the asset pool of the abS, Kowalski should recommend a:

(Multiple Choice)

4.9/5 (23)

The following information relates to Questions

lena liecken is a senior bond analyst at taurus investment Management. Kristel Kreming,

a junior analyst, works for liecken in helping conduct fixed-income research for the firm's

portfolio managers. liecken and Kreming meet to discuss several bond positions held in the

firm's portfolios.

bonds i and ii both have a maturity of one year, an annual coupon rate of 5%, and a mar-

ket price equal to par value. The risk-free rate is 3%. historical default experiences of bonds

comparable to bonds i and ii are presented in exhibit 1.

EXHIBIT 1 Credit Risk Information for Comparable Bonds

Percentage of Bonds That Survive and Make Full Bond Recovery Rate Payment I 40\% 98\% II 35\% 99\%

Bond III

Bond III is a zero-coupon bond with three years to maturity. Liecken evaluates similar bonds and estimates a recovery rate of and a risk-neutral default probability of , assuming conditional probabilities of default. Kreming creates Exhibit 2 to compute Bond III's credit valuation adjustment. She assumes a flat yield curve at , with exposure, recovery, and loss given default values expressed per 100 of par value.

EXHIBIT 2 Analysis of Bond III Date Exposure Recovery Loss Given Default Probability of Default Probability of Survival Expected Loss Present Value of Expected Loss 0 1 94.2596 35.8186 58.4410 2.0000\% 98.0000\% 1.1688 1.1348 2 97.0874 36.8932 60.1942 1.9600\% 96.0400\% 1.1798 1.1121 3 100.0000 38.0000 62.0000 94.1192\% Sum 5.8808\% 3.5395 3.3367

Bond IV

Bond IV is an AA rated bond that matures in five years, has a coupon rate of , and a modified duration of 4.2. Liecken is concerned about whether this bond will be downgraded to an A rating, but she does not expect the bond to default during the next year. Kreming constructs a partial transition matrix, which is presented in Exhibit 3, and suggests using a model to predict the rating change of Bond IV using leverage ratios, return on assets, and macroeconomic variables.

EXHIBIT 3 Partial One-Year Corporate Transition Matrix (entries in \%) From/To AAA AA A AAA 92.00 6.00 1.00 AA 2.00 89.00 8.00 A 0.05 1.00 85.00 Credit Spread (\%) 0.50 1.00 1.75

Default Probabilities

Kreming calculates the risk-neutral probabilities, compares them with the actual default probabilities of bonds evaluated over the past 10 years, and observes that the actual and risk-neutral probabilities differ. She makes two observations regarding the comparison of these probabilities:

Observation 1: Actual default probabilities include the default risk premium associated with the uncertainty in the timing of the possible default loss.

Observation 2: The observed spread over the yield on a risk-free bond in practice includes liquidity and tax considerations, in addition to credit risk.

-based on exhibit 1, the risk-neutral default probability for bond i is closest to:

(Multiple Choice)

5.0/5 (28)

The following information relates to Questions

lena liecken is a senior bond analyst at taurus investment Management. Kristel Kreming,

a junior analyst, works for liecken in helping conduct fixed-income research for the firm's

portfolio managers. liecken and Kreming meet to discuss several bond positions held in the

firm's portfolios.

bonds i and ii both have a maturity of one year, an annual coupon rate of 5%, and a mar-

ket price equal to par value. The risk-free rate is 3%. historical default experiences of bonds

comparable to bonds i and ii are presented in exhibit 1.

EXHIBIT 1 Credit Risk Information for Comparable Bonds

Percentage of Bonds That Survive and Make Full Bond Recovery Rate Payment I 40\% 98\% II 35\% 99\%

Bond III

Bond III is a zero-coupon bond with three years to maturity. Liecken evaluates similar bonds and estimates a recovery rate of and a risk-neutral default probability of , assuming conditional probabilities of default. Kreming creates Exhibit 2 to compute Bond III's credit valuation adjustment. She assumes a flat yield curve at , with exposure, recovery, and loss given default values expressed per 100 of par value.

EXHIBIT 2 Analysis of Bond III Date Exposure Recovery Loss Given Default Probability of Default Probability of Survival Expected Loss Present Value of Expected Loss 0 1 94.2596 35.8186 58.4410 2.0000\% 98.0000\% 1.1688 1.1348 2 97.0874 36.8932 60.1942 1.9600\% 96.0400\% 1.1798 1.1121 3 100.0000 38.0000 62.0000 94.1192\% Sum 5.8808\% 3.5395 3.3367

Bond IV

Bond IV is an AA rated bond that matures in five years, has a coupon rate of , and a modified duration of 4.2. Liecken is concerned about whether this bond will be downgraded to an A rating, but she does not expect the bond to default during the next year. Kreming constructs a partial transition matrix, which is presented in Exhibit 3, and suggests using a model to predict the rating change of Bond IV using leverage ratios, return on assets, and macroeconomic variables.

EXHIBIT 3 Partial One-Year Corporate Transition Matrix (entries in \%) From/To AAA AA A AAA 92.00 6.00 1.00 AA 2.00 89.00 8.00 A 0.05 1.00 85.00 Credit Spread (\%) 0.50 1.00 1.75

Default Probabilities

Kreming calculates the risk-neutral probabilities, compares them with the actual default probabilities of bonds evaluated over the past 10 years, and observes that the actual and risk-neutral probabilities differ. She makes two observations regarding the comparison of these probabilities:

Observation 1: Actual default probabilities include the default risk premium associated with the uncertainty in the timing of the possible default loss.

Observation 2: The observed spread over the yield on a risk-free bond in practice includes liquidity and tax considerations, in addition to credit risk.

-Kreming's suggested model for bond iV is a:

(Multiple Choice)

4.9/5 (34)

The following information relates to Questions

lena liecken is a senior bond analyst at taurus investment Management. Kristel Kreming,

a junior analyst, works for liecken in helping conduct fixed-income research for the firm's

portfolio managers. liecken and Kreming meet to discuss several bond positions held in the

firm's portfolios.

bonds i and ii both have a maturity of one year, an annual coupon rate of 5%, and a mar-

ket price equal to par value. The risk-free rate is 3%. historical default experiences of bonds

comparable to bonds i and ii are presented in exhibit 1.

EXHIBIT 1 Credit Risk Information for Comparable Bonds

Percentage of Bonds That Survive and Make Full Bond Recovery Rate Payment I 40\% 98\% II 35\% 99\%

Bond III

Bond III is a zero-coupon bond with three years to maturity. Liecken evaluates similar bonds and estimates a recovery rate of and a risk-neutral default probability of , assuming conditional probabilities of default. Kreming creates Exhibit 2 to compute Bond III's credit valuation adjustment. She assumes a flat yield curve at , with exposure, recovery, and loss given default values expressed per 100 of par value.

EXHIBIT 2 Analysis of Bond III Date Exposure Recovery Loss Given Default Probability of Default Probability of Survival Expected Loss Present Value of Expected Loss 0 1 94.2596 35.8186 58.4410 2.0000\% 98.0000\% 1.1688 1.1348 2 97.0874 36.8932 60.1942 1.9600\% 96.0400\% 1.1798 1.1121 3 100.0000 38.0000 62.0000 94.1192\% Sum 5.8808\% 3.5395 3.3367

Bond IV

Bond IV is an AA rated bond that matures in five years, has a coupon rate of , and a modified duration of 4.2. Liecken is concerned about whether this bond will be downgraded to an A rating, but she does not expect the bond to default during the next year. Kreming constructs a partial transition matrix, which is presented in Exhibit 3, and suggests using a model to predict the rating change of Bond IV using leverage ratios, return on assets, and macroeconomic variables.

EXHIBIT 3 Partial One-Year Corporate Transition Matrix (entries in \%) From/To AAA AA A AAA 92.00 6.00 1.00 AA 2.00 89.00 8.00 A 0.05 1.00 85.00 Credit Spread (\%) 0.50 1.00 1.75

Default Probabilities

Kreming calculates the risk-neutral probabilities, compares them with the actual default probabilities of bonds evaluated over the past 10 years, and observes that the actual and risk-neutral probabilities differ. She makes two observations regarding the comparison of these probabilities:

Observation 1: Actual default probabilities include the default risk premium associated with the uncertainty in the timing of the possible default loss.

Observation 2: The observed spread over the yield on a risk-free bond in practice includes liquidity and tax considerations, in addition to credit risk.

-based on exhibit 2, the credit valuation adjustment (cVa) for bond iii is closest to:

(Multiple Choice)

5.0/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)