Deck 21: Partnerships: Changes in Ownership

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

_____ Data for the partnership of A and B follow:

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of A, B, and C under the bonus method are:

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of A, B, and C under the bonus method are:

A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of A, B, and C under the bonus method are:A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Question

_____ Data for the partnership of Able and Baker follow:

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of Able, Baker, and Cook under the recording the goodwill method are:

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of Able, Baker, and Cook under the recording the goodwill method are:

A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of Able, Baker, and Cook under the recording the goodwill method are:A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Question

_____ Data for the partnership of X and Y follow:

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. What are the balances in the capital accounts of X, Y, and Z under the bonus method?

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. What are the balances in the capital accounts of X, Y, and Z under the bonus method?

A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. What are the balances in the capital accounts of X, Y, and Z under the bonus method?A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Question

_____ Data for the partnership of X and Y follow:

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. The balances in the capital accounts of X, Y, and Z under the recording the goodwill method are:

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. The balances in the capital accounts of X, Y, and Z under the recording the goodwill method are:

A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. The balances in the capital accounts of X, Y, and Z under the recording the goodwill method are:A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Question

_____ Ames and Buell are partners who share profits and losses in the ratio of 3:2, respectively. On 8/31/06, their capital accounts were as follows:

On that date, they agreed to admit Carter as a partner with a one-third interest in the capital and profits and losses, for an investment of $50,000. The new partnership will begin with a total capital of $180,000. The partners' capital balances immediately after Carter's admission are:

On that date, they agreed to admit Carter as a partner with a one-third interest in the capital and profits and losses, for an investment of $50,000. The new partnership will begin with a total capital of $180,000. The partners' capital balances immediately after Carter's admission are:

On that date, they agreed to admit Carter as a partner with a one-third interest in the capital and profits and losses, for an investment of $50,000. The new partnership will begin with a total capital of $180,000. The partners' capital balances immediately after Carter's admission are: Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

_____ Tax basis: Assume the following data for the partnership of A and B:

A and B share profits and losses 75:25, respectively. C is admitted to a one-fifth interest in the capital and profits and losses of the partnership by contributing $40,000 (one-fifth of the net assets of the new firm) and assumes a one-fifth responsibility for present partnership obligations. The tax bases of A, B, and C after the admission of C are

A and B share profits and losses 75:25, respectively. C is admitted to a one-fifth interest in the capital and profits and losses of the partnership by contributing $40,000 (one-fifth of the net assets of the new firm) and assumes a one-fifth responsibility for present partnership obligations. The tax bases of A, B, and C after the admission of C are

A) $66,000, $37,000, and $52,000, respectively.

B) $69,000, $34,000, and $52,000, respectively.

C) $75,000, $40,000, and $40,000, respectively.

D) $75,000, $40,000, and $52,000, respectively.

E) $71,000, $36,000, and $48,000, respectively.

A and B share profits and losses 75:25, respectively. C is admitted to a one-fifth interest in the capital and profits and losses of the partnership by contributing $40,000 (one-fifth of the net assets of the new firm) and assumes a one-fifth responsibility for present partnership obligations. The tax bases of A, B, and C after the admission of C areA) $66,000, $37,000, and $52,000, respectively.

B) $69,000, $34,000, and $52,000, respectively.

C) $75,000, $40,000, and $40,000, respectively.

D) $75,000, $40,000, and $52,000, respectively.

E) $71,000, $36,000, and $48,000, respectively.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/37

Play

Full screen (f)

Deck 21: Partnerships: Changes in Ownership

1

Legally, a change in the ownership of a partnership is not a(n) ______________________________________________ of the old partnership.

dissolution

2

When a partnership change in ownership occurs and the partnership has undervalued tangible assets, a method intended to prevent an inequity from occurring among the partners that results in (a) no entries being recorded in the general ledger to revalue the assets and (b) no departure from GAAP is the ______________ ______________________________ method.

bonus

3

When a partnership change in ownership occurs and the partnership has goodwill, a method intended to prevent an inequity from occurring among the partners that results in (a) entries being recorded in the general ledger relating to the goodwill and (b) a deviation from GAAP is the __________________________________ method.

recording the goodwill

4

When a partnership change in ownership occurs and the partnership has goodwill, a method intended to prevent an inequity from occurring among the partners that results in (a) no entries being recorded in the general ledger relating to the goodwill and (b) no deviation from GAAP is the _____________________________ method.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

5

When an existing partnership has goodwill and a new partner is being admitted, a method of dealing with the goodwill that does not deviate from GAAP but may favor the old partners if the goodwill does not materialize is the _________________ _________________________ method.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

6

When a partner leaves a partnership (and the partnership's existence is not terminated), the Revised Uniform Partnership Act refers to that as a _____________________________.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

7

When a partnership's existence is terminated, the Revised Uniform Partnership Act refers to that as a _____________________________ of the partnership.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

8

When a partner sells all or a portion of his or her partnership interest to an outside party, no entries are required on the partnership's books.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

9

An advantage to the bonus method is that no deviation from GAAP results.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

10

In partnerships, goodwill cannot be recorded unless it results from a business combination that does not qualify as a pooling of interests.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

11

In partnerships, when goodwill is recorded it cannot be amortized.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

12

When two partnerships combine in a manner that is substantively a pooling of interests, the assets of the combining partnerships cannot be revalued to their current values.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

13

When an existing partnership that has goodwill admits a new partner, the end result on the new partner's capital account will be the same under both the bonus method and the recording the goodwill method, regardless of whether the agreed-upon value of the goodwill is eventually realized.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

14

An advantage of the recording the goodwill method is that an incoming partner always gets credited to his or her capital account, as a minimum, the amount of cash contributed.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

15

An advantage of the recording the goodwill method over the bonus method is that an incoming partner eventually will end up with a greater capital balance.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

16

When a person is being admitted into a partnership that has goodwill, the amount of goodwill deemed to exist is a residual amount derived from the agreed-upon ownership percentages and profit and loss sharing ratios.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

17

_____ The purchase of an interest from one or more of the existing partners of a partnership results in

A) No entries being made in the partnership's books.

B) An entry solely within the capital accounts.

C) An entry to record the receipt of the consideration paid.

D) An entry to revalue tangible and intangible assets or to use the bonus method to give effect to such undervaluations.

E) An entry to reflect payments to the applicable existing partner(s) and receipt of a capital contribution from the new partner.

A) No entries being made in the partnership's books.

B) An entry solely within the capital accounts.

C) An entry to record the receipt of the consideration paid.

D) An entry to revalue tangible and intangible assets or to use the bonus method to give effect to such undervaluations.

E) An entry to reflect payments to the applicable existing partner(s) and receipt of a capital contribution from the new partner.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

18

_____ When a person is being admitted into a partnership and the bonus method has been selected,

A) Assets are revalued to their fair (current) values.

B) An entry is made solely within the capital accounts.

C) No entries are made in the partnership's books.

D) The new partner may receive a credit to his or her capital account that is more or less than the amount of such partner's capital contribution.

E) None of the above.

A) Assets are revalued to their fair (current) values.

B) An entry is made solely within the capital accounts.

C) No entries are made in the partnership's books.

D) The new partner may receive a credit to his or her capital account that is more or less than the amount of such partner's capital contribution.

E) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

19

_____ When a person is being admitted into a partnership and recording the goodwill method has been selected,

A) An entry is made solely within the capital accounts.

B) No entries are made in the partnership's books.

C) A credit is made only to the new partner's capital account.

D) A credit is made only to the old partner's capital account.

E) None of the above.

A) An entry is made solely within the capital accounts.

B) No entries are made in the partnership's books.

C) A credit is made only to the new partner's capital account.

D) A credit is made only to the old partner's capital account.

E) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

20

_____ When a person is being admitted into a partnership and the special profit and loss sharing provision method has been selected,

A) Tangible and/or intangible assets are revalued to their current values.

B) No entries are made in the partnership's books.

C) The new partner receives a full credit to his or her capital account equal to the amount of his or her capital contribution.

D) The new partner may receive a credit to his or her capital account that is more or less than the amount of his or her capital contribution.

E) An entry is made solely within the capital accounts.

A) Tangible and/or intangible assets are revalued to their current values.

B) No entries are made in the partnership's books.

C) The new partner receives a full credit to his or her capital account equal to the amount of his or her capital contribution.

D) The new partner may receive a credit to his or her capital account that is more or less than the amount of his or her capital contribution.

E) An entry is made solely within the capital accounts.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

21

_____ When Dubke retired from the partnership of Dubke, Logan, and Flaherty, the final settlement of Dubke's partnership interest exceeded Dubke's capital account balance. Under the bonus method, the excess

A) Was recorded as goodwill.

B) Was recorded as an expense.

C) Had no effect on the capital balances of Logan and Flaherty.

D) Reduced the capital balances of Logan and Flaherty.

E) None of the above.

A) Was recorded as goodwill.

B) Was recorded as an expense.

C) Had no effect on the capital balances of Logan and Flaherty.

D) Reduced the capital balances of Logan and Flaherty.

E) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

22

_____ Data for the partnership of A and B follow:

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of A, B, and C under the bonus method are:

A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of A, B, and C under the bonus method are:A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

23

_____ Data for the partnership of Able and Baker follow:

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of Able, Baker, and Cook under the recording the goodwill method are:

A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Cook is to be admitted into the partnership and is to have a one-fifth interest in capital and profits with a cash contribution of $40,000. The balances in the capital accounts of Able, Baker, and Cook under the recording the goodwill method are:A) $80,000, $60,000, and $40,000, respectively.

B) $92,000, $68,000, and $40,000, respectively.

C) $95,000, $65,000, and $40,000, respectively.

D) $82,400, $61,600, and $36,000, respectively.

E) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

24

_____ Data for the partnership of X and Y follow:

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. What are the balances in the capital accounts of X, Y, and Z under the bonus method?

A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. What are the balances in the capital accounts of X, Y, and Z under the bonus method?A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

25

_____ Data for the partnership of X and Y follow:

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. The balances in the capital accounts of X, Y, and Z under the recording the goodwill method are:

A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Z is to be admitted into the partnership and is to have a one-third interest in capital and profits with a cash contribution of $30,000. The balances in the capital accounts of X, Y, and Z under the recording the goodwill method are:A) $44,000, $36,000, and $40,000, respectively.

B) $56,000, $44,000, and $20,000, respectively.

C) $50,000, $40,000, and $30,000, respectively.

D) $50,000, $40,000, and $40,000, respectively.

E) $50,000, $40,000, and $45,000, respectively.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

26

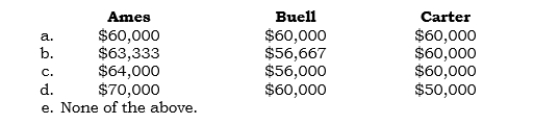

_____ Ames and Buell are partners who share profits and losses in the ratio of 3:2, respectively. On 8/31/06, their capital accounts were as follows:

On that date, they agreed to admit Carter as a partner with a one-third interest in the capital and profits and losses, for an investment of $50,000. The new partnership will begin with a total capital of $180,000. The partners' capital balances immediately after Carter's admission are:

On that date, they agreed to admit Carter as a partner with a one-third interest in the capital and profits and losses, for an investment of $50,000. The new partnership will begin with a total capital of $180,000. The partners' capital balances immediately after Carter's admission are: Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

27

_____ At 12/31/06, Reed and Quinn are partners with capital balances of $40,000 and $20,000, and they share profits and losses in the ratio of 2:1, respectively. On this date, Poe is admitted into the partnership. Poe invests $17,000 cash for a one-fifth interest in the capital and profit of the new partnership. Assume that goodwill is not to be recorded. The credit to be made to Poe's capital account at 12/31/06 is:

A) $12,000

B) $15,000

C) $15,400

D) $17,000

E) None of the above.

A) $12,000

B) $15,000

C) $15,400

D) $17,000

E) None of the above.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

28

_____ Diller decided to withdraw from the partnership. Diller's share of the partnership profits and losses was 25%. Upon withdrawing from the partnership, Diller was paid $91,000 in final settlement for his interest. The total of the partners' capital accounts before recognition of partnership goodwill prior to Diller's withdrawal was $370,000. After Diller's withdrawal, the remaining partners' capital accounts, excluding their share of goodwill, totaled $310,000. The total agreed-upon goodwill of the firm is:

A) $15,000

B) $31,000

C) $60,000

D) $124,000

E) $240,000

A) $15,000

B) $31,000

C) $60,000

D) $124,000

E) $240,000

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

29

_____ X and Y are partners and have capital balances of $70,000 and $30,000, respectively. X and Y share profits and losses in the ratio 6:4, respectively. Z is admitted into the partnership by purchasing one-fifth of the capital interests of X and Y for a total price of $25,000. The capital balances of X, Y, and Z will be:

A) $56,000, $24,000, and $20,000, respectively.

B) $56,000, $24,000, and $25,000, respectively.

C) $73,000, $32,000, and $20,000, respectively.

D) $70,000, $30,000, and $25,000, respectively.

E) $70,000, $30,000, and $20,000, respectively.

A) $56,000, $24,000, and $20,000, respectively.

B) $56,000, $24,000, and $25,000, respectively.

C) $73,000, $32,000, and $20,000, respectively.

D) $70,000, $30,000, and $25,000, respectively.

E) $70,000, $30,000, and $20,000, respectively.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

30

When a partner is admitted into a partnership, the amount of existing partnership liabilities for which the new partner becomes responsible is treated for income tax-reporting purposes as ___________________________________.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

31

When a partner retires from a partnership, the balance in that partner's capital account that is distributed to that partner is treated as ________________________ for income tax-reporting purposes.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

32

When a partner retires from a partnership, the amount of existing partnership liabilities for which the retiring partner is no longer responsible is treated for income tax-reporting purposes as _______________________________________.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

33

A gain or loss for income tax-reporting purposes on a partner's disposal of a partnership interest is computed by comparing the partner's __________________ to his or her _________________________________.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

34

When a partner withdraws from a partnership, the partner's gain or loss for income tax-reporting purposes is not made by comparing his or her proceeds with the balance in his or her capital account.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

35

_____ When a partner withdraws from a partnership, the determination of the withdrawing partner's gain or loss for income tax-reporting purposes is made by comparing:

A) (1) The partner's proceeds with (2) the balance in his or her capital account.

B) (1) The amount of cash received with (2) his or her tax basis.

C) (1) The partner's capital balance with (2) his or her share of existing partnership liabilities for which he or she is relieved of responsibility.

D) (1) The partner's proceeds plus his or or her share of existing partnership liabilities for which he or she is relieved of responsibility with (2) his or her tax basis.

E) (1) The partner's tax basis plus his or her share of existing partnership liabilities for which he or she is relieved of responsibility with (2) his or her proceeds.

A) (1) The partner's proceeds with (2) the balance in his or her capital account.

B) (1) The amount of cash received with (2) his or her tax basis.

C) (1) The partner's capital balance with (2) his or her share of existing partnership liabilities for which he or she is relieved of responsibility.

D) (1) The partner's proceeds plus his or or her share of existing partnership liabilities for which he or she is relieved of responsibility with (2) his or her tax basis.

E) (1) The partner's tax basis plus his or her share of existing partnership liabilities for which he or she is relieved of responsibility with (2) his or her proceeds.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

36

_____ A, B, and C are in partnership and share profits and losses equally. C is retiring. The balance in C's capital account is $60,000. C is to be given a cash bonus of $5,000 as a result of unrecorded goodwill. The partnership has liabilities of $18,000 at the time of C's withdrawal. C's tax basis is $55,000. C's taxable gain or loss is:

A) A gain of $4,000.

B) A gain of $5,000.

C) A gain of $10,000.

D) A gain of $11,000.

E) A gain of $16,000.

A) A gain of $4,000.

B) A gain of $5,000.

C) A gain of $10,000.

D) A gain of $11,000.

E) A gain of $16,000.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

37

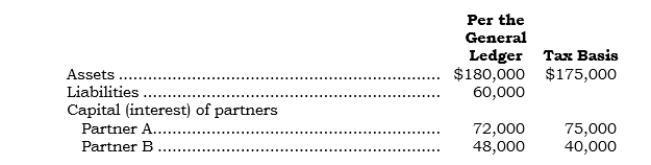

_____ Tax basis: Assume the following data for the partnership of A and B:

A and B share profits and losses 75:25, respectively. C is admitted to a one-fifth interest in the capital and profits and losses of the partnership by contributing $40,000 (one-fifth of the net assets of the new firm) and assumes a one-fifth responsibility for present partnership obligations. The tax bases of A, B, and C after the admission of C are

A) $66,000, $37,000, and $52,000, respectively.

B) $69,000, $34,000, and $52,000, respectively.

C) $75,000, $40,000, and $40,000, respectively.

D) $75,000, $40,000, and $52,000, respectively.

E) $71,000, $36,000, and $48,000, respectively.

A and B share profits and losses 75:25, respectively. C is admitted to a one-fifth interest in the capital and profits and losses of the partnership by contributing $40,000 (one-fifth of the net assets of the new firm) and assumes a one-fifth responsibility for present partnership obligations. The tax bases of A, B, and C after the admission of C areA) $66,000, $37,000, and $52,000, respectively.

B) $69,000, $34,000, and $52,000, respectively.

C) $75,000, $40,000, and $40,000, respectively.

D) $75,000, $40,000, and $52,000, respectively.

E) $71,000, $36,000, and $48,000, respectively.

Unlock Deck

Unlock for access to all 37 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 37 flashcards in this deck.