Deck 6: Consolidated Financial Statements: on Date of Business Combination

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Pangborn Corporation paid $840,000 (including direct out-of-pocket costs) for 70% of the outstanding common stock of Siddon Company on September 30, 2006, the end of Pangborn's fiscal year. Included in the working paper elimination (in journal entry format) for Pangborn Corporation and subsidiary on that date were the following:

If Pangborn had inferred a current fair value for 100% of Siddon's total net assets from the $840,000 cost, Goodwill and Minority Interest in Net Assets of Subsidiary in the September 30, 2006, working paper elimination would have been, respectively:

If Pangborn had inferred a current fair value for 100% of Siddon's total net assets from the $840,000 cost, Goodwill and Minority Interest in Net Assets of Subsidiary in the September 30, 2006, working paper elimination would have been, respectively:

A) $100,000 and $330,000

B) $70,000 and $360,000

C) $49,000 and $231,000

D) $100,000 and $360,000

E) Some other amounts

If Pangborn had inferred a current fair value for 100% of Siddon's total net assets from the $840,000 cost, Goodwill and Minority Interest in Net Assets of Subsidiary in the September 30, 2006, working paper elimination would have been, respectively:A) $100,000 and $330,000

B) $70,000 and $360,000

C) $49,000 and $231,000

D) $100,000 and $360,000

E) Some other amounts

Question

Question

Question

Question

On March 1, 2006, Pride Corporation paid $400,000 for all the outstanding common stock of Supra Company in a business combination, for which out-of-pocket costs may be disregarded. The carrying amounts of Supra's identifiable assets and liabilities on March 1, 2006, follow:  On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.

On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.

The amount recognized as goodwill as a result of the business combination is:

A) $0

B) $25,000

C) $75,000

D) $90,000

E) Some other amount

On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.The amount recognized as goodwill as a result of the business combination is:

A) $0

B) $25,000

C) $75,000

D) $90,000

E) Some other amount

Question

On October 31, 2006, Portugal Corporation acquired 80% of the outstanding common stock of Spain Company in a business combination. Total cost of the investment, including direct out-of-pocket costs, was $480,000. The working paper elimination (in journal entry format, explanation omitted) for Portugal Corporation and Subsidiary on October 31, 2006, was as follows:  If minority interest in net assets of subsidiary had been reflected at carrying amount, rather than at current fair value, of the subsidiary's identifiable net assets, the credit to Minority Interest in Net Assets of Subsidiary in the foregoing elimination would have been:

If minority interest in net assets of subsidiary had been reflected at carrying amount, rather than at current fair value, of the subsidiary's identifiable net assets, the credit to Minority Interest in Net Assets of Subsidiary in the foregoing elimination would have been:

A) $90,000

B) $120,000

C) $60,000

D) Some other amount

If minority interest in net assets of subsidiary had been reflected at carrying amount, rather than at current fair value, of the subsidiary's identifiable net assets, the credit to Minority Interest in Net Assets of Subsidiary in the foregoing elimination would have been:A) $90,000

B) $120,000

C) $60,000

D) Some other amount

Question

On October 31, 2006, Portugal Corporation acquired 80% of the outstanding common stock of Spain Company in a business combination. Total cost of the investment, including direct out-of-pocket costs, was $480,000. The working paper elimination (in journal entry format, explanation omitted) for Portugal Corporation and Subsidiary on October 31, 2006, was as follows:  If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:

If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:

A) $120,000

B) $150,000

C) $180,000

D) Some other amount

If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:A) $120,000

B) $150,000

C) $180,000

D) Some other amount

Question

Question

Question

Question

Question

Question

Question

Question

Question

On June 30, 2006, Purdom Corporation acquired 80% of the outstanding common stock of Sudan Company. On the date of the business combination, identifiable net assets of Sudan with current fair values differing from carrying amounts were as follows:

Complete the following working paper for consolidated balance sheet of Purdom Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes.

Complete the following working paper for consolidated balance sheet of Purdom Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes.

Complete the following working paper for consolidated balance sheet of Purdom Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes. Question

On May 31, 2006, Ping Corporation paid $300,000, including direct out-of-pocket costs of the business combination, for 82% of the outstanding common stock of Spring Company, which became a subsidiary. Differences between current fair values and carrying amounts of identifiable net assets of Spring Company on May 31, 2006, were limited to the following:

Complete the following working paper for consolidated balance sheet of Ping Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes.

Complete the following working paper for consolidated balance sheet of Ping Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes.

Explanation of elimination: (a)

Explanation of elimination: (a)

Complete the following working paper for consolidated balance sheet of Ping Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes. Explanation of elimination: (a) Question

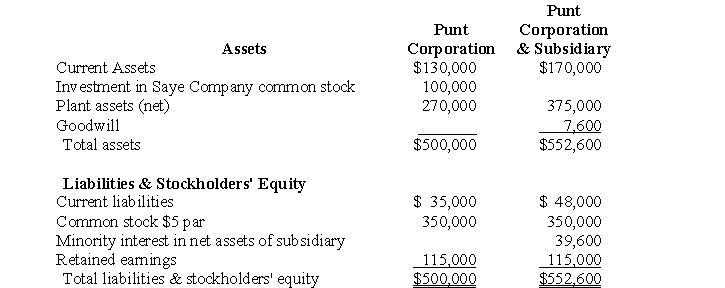

Punt Corporation acquired a controlling interest in Saye Company for cash. The separate balance sheet of Punt and the consolidated balance sheet immediately after the business combination were as follows:

Plant assets of Saye Company were undervalued by $15,000 on the date of the business combination; the remainder of Punt's cost was assigned to goodwill. The retained earnings of Saye on the date of the business combination amounted to $37,000.

Plant assets of Saye Company were undervalued by $15,000 on the date of the business combination; the remainder of Punt's cost was assigned to goodwill. The retained earnings of Saye on the date of the business combination amounted to $37,000.

a. Prepare the separate balance sheet of Saye Company on the date of the business combination.

b. What percentage of the common stock of Saye was acquired by Punt?

c. Prepare the working paper elimination (in journal entry format) for Punt Corporation and subsidiary on the date of the business combination.

Plant assets of Saye Company were undervalued by $15,000 on the date of the business combination; the remainder of Punt's cost was assigned to goodwill. The retained earnings of Saye on the date of the business combination amounted to $37,000.a. Prepare the separate balance sheet of Saye Company on the date of the business combination.

b. What percentage of the common stock of Saye was acquired by Punt?

c. Prepare the working paper elimination (in journal entry format) for Punt Corporation and subsidiary on the date of the business combination.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/39

Play

Full screen (f)

Deck 6: Consolidated Financial Statements: on Date of Business Combination

1

In a business combination that establishes a parent company-subsidiary affiliation, the subsidiary prepares journal entries on the date of the combination to increase the carrying amounts of its net assets to current fair values.

False

2

A parent company's journal entries to record a business combination with a subsidiary do not include debits and credits to recognize the assets and liabilities of the subsidiary.

True

3

Only the balance sheet is consolidated on the date of a business combination of a parent company and subsidiary.

True

4

A controlling financial interest traditionally has been defined as the investor corporation's ownership of more than 50% of the investee corporation's outstanding common stock.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

5

All out-of-pocket costs of a business combination reduce additional paid-in capital of the combinor.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

6

Consolidated financial statements emphasize the legal form of the parent company-subsidiary relationship.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

7

Finance-related subsidiaries may be excluded from consolidation at the election of the parent company's management.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

8

A parent company's control of a subsidiary may be achieved both directly and indirectly, the latter through another subsidiary of the parent.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

9

A debit to Goodwill-Subsidiary in a working paper elimination (in journal entry format) for a parent company and its wholly owned subsidiary indicates that the current fair values of the subsidiary's identifiable net assets exceeded their carrying amounts on the date of the business combination.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

10

A subsidiary's paid-in capital ledger accounts always are eliminated in the preparation of a consolidated balance sheet for the parent company and the subsidiary.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

11

Goodwill recognized in a business combination of a parent company and a partially owned subsidiary is attributable to the subsidiary.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

12

A widely used method of accounting for business combinations involving a partially owned subsidiary values goodwill at the amount acquired by the parent company.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

13

In a business combination resulting in a parent company-subsidiary affiliation, the parent company's Investment in Subsidiary Common Stock ledger account is not closed, as it is in other types of business combinations.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

14

Under the parent company concept of consolidated financial statements, the minority interest in net assets of a subsidiary is displayed as a liability.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

15

Because minority stockholders exercise no ownership control over the operations of either the parent company or the subsidiary, minority stockholders in substance might be considered a special class of creditors of the consolidated entity.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

16

The Financial Accounting Standards Board requires push-down accounting in the separate financial statements of subsidiaries.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

17

The terms and variable interest entity are synonymous.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

18

In a business combination resulting in a parent company-subsidiary relationship, differences between current fair values and carrying amounts of the subsidiary's identifiable net assets on the date of the combination are:

A) Disregarded

B) Entered in the accounting records of the subsidiary

C) Accounted for in appropriately titled ledger accounts in the parent company's accounting records

D) Provided in a working paper elimination

E) Accounted for in some other manner

A) Disregarded

B) Entered in the accounting records of the subsidiary

C) Accounted for in appropriately titled ledger accounts in the parent company's accounting records

D) Provided in a working paper elimination

E) Accounted for in some other manner

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

19

Pangborn Corporation paid $840,000 (including direct out-of-pocket costs) for 70% of the outstanding common stock of Siddon Company on September 30, 2006, the end of Pangborn's fiscal year. Included in the working paper elimination (in journal entry format) for Pangborn Corporation and subsidiary on that date were the following:

If Pangborn had inferred a current fair value for 100% of Siddon's total net assets from the $840,000 cost, Goodwill and Minority Interest in Net Assets of Subsidiary in the September 30, 2006, working paper elimination would have been, respectively:

A) $100,000 and $330,000

B) $70,000 and $360,000

C) $49,000 and $231,000

D) $100,000 and $360,000

E) Some other amounts

If Pangborn had inferred a current fair value for 100% of Siddon's total net assets from the $840,000 cost, Goodwill and Minority Interest in Net Assets of Subsidiary in the September 30, 2006, working paper elimination would have been, respectively:A) $100,000 and $330,000

B) $70,000 and $360,000

C) $49,000 and $231,000

D) $100,000 and $360,000

E) Some other amounts

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

20

On March 31, 2006, Preston Corporation acquired for cash at $25 a share all 300,000 shares of the outstanding common stock of Sexton Company. Out-of-pocket costs of the business combination may be disregarded. Sexton's balance sheet on March 31, 2006, had net assets of $6,000,000. Additionally, the current fair value of Preston's plant assets on March 31, 2006, was $800,000 in excess of carrying amount. The amount to be shown for the balance sheet caption "Goodwill" in the March 31, 2006, consolidated balance sheet of Preston Corporation and its wholly owned subsidiary, Sexton Company, is:

A) $0

B) $700,000

C) $800,000

D) $1,500,000

E) Some other amount

A) $0

B) $700,000

C) $800,000

D) $1,500,000

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

21

Consolidated financial statements are prepared when a parent-subsidiary relationship exists, in recognition of the accounting principle or concept of:

A) Materiality

B) Entity

C) Reliability

D) Going concern

A) Materiality

B) Entity

C) Reliability

D) Going concern

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

22

Consolidated financial statements are not appropriate if:

A) The subsidiary is in the process of bankruptcy reorganization

B) There is a minority interest in the subsidiary

C) The subsidiary has a substantial amount of long-term debt payable to outsiders

D) The parent company makes substantial purchases of material from the subsidiary

A) The subsidiary is in the process of bankruptcy reorganization

B) There is a minority interest in the subsidiary

C) The subsidiary has a substantial amount of long-term debt payable to outsiders

D) The parent company makes substantial purchases of material from the subsidiary

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

23

On March 1, 2006, Pride Corporation paid $400,000 for all the outstanding common stock of Supra Company in a business combination, for which out-of-pocket costs may be disregarded. The carrying amounts of Supra's identifiable assets and liabilities on March 1, 2006, follow: On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.

The amount recognized as goodwill as a result of the business combination is:

A) $0

B) $25,000

C) $75,000

D) $90,000

E) Some other amount

On March 1, 2006, the inventories of Supra had a current fair value of $95,000, and the plant assets (net) had a current fair value of $280,000.The amount recognized as goodwill as a result of the business combination is:

A) $0

B) $25,000

C) $75,000

D) $90,000

E) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

24

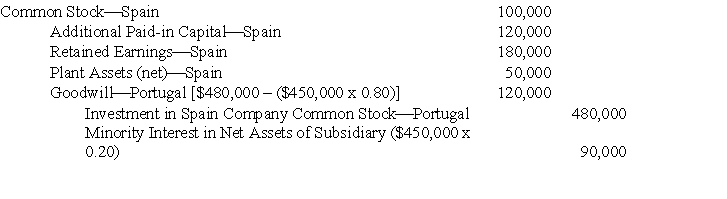

On October 31, 2006, Portugal Corporation acquired 80% of the outstanding common stock of Spain Company in a business combination. Total cost of the investment, including direct out-of-pocket costs, was $480,000. The working paper elimination (in journal entry format, explanation omitted) for Portugal Corporation and Subsidiary on October 31, 2006, was as follows: If minority interest in net assets of subsidiary had been reflected at carrying amount, rather than at current fair value, of the subsidiary's identifiable net assets, the credit to Minority Interest in Net Assets of Subsidiary in the foregoing elimination would have been:

A) $90,000

B) $120,000

C) $60,000

D) Some other amount

If minority interest in net assets of subsidiary had been reflected at carrying amount, rather than at current fair value, of the subsidiary's identifiable net assets, the credit to Minority Interest in Net Assets of Subsidiary in the foregoing elimination would have been:A) $90,000

B) $120,000

C) $60,000

D) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

25

On October 31, 2006, Portugal Corporation acquired 80% of the outstanding common stock of Spain Company in a business combination. Total cost of the investment, including direct out-of-pocket costs, was $480,000. The working paper elimination (in journal entry format, explanation omitted) for Portugal Corporation and Subsidiary on October 31, 2006, was as follows: If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:

A) $120,000

B) $150,000

C) $180,000

D) Some other amount

If goodwill had been computed based on the implied current fair value of the subsidiary's total net assets, the debit to Goodwill-Portugal in the foregoing working paper elimination would have been:A) $120,000

B) $150,000

C) $180,000

D) Some other amount

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

26

In a business combination resulting in a parent company-subsidiary relationship, the parent company's Investment in Subsidiary Common Stock ledger account balance is:

A) Allocated to individual asset and liability ledger accounts in a parent company journal entry

B) Eliminated with a working paper elimination for the working paper for consolidated balance sheet

C) Displayed among noncurrent assets in the consolidated balance sheet

D) Used as a basis for adjusting the subsidiary's asset and liability account balances in the subsidiary's ledger to current fair values

A) Allocated to individual asset and liability ledger accounts in a parent company journal entry

B) Eliminated with a working paper elimination for the working paper for consolidated balance sheet

C) Displayed among noncurrent assets in the consolidated balance sheet

D) Used as a basis for adjusting the subsidiary's asset and liability account balances in the subsidiary's ledger to current fair values

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

27

Working paper eliminations are entered in:

A) Both the parent company's and the subsidiary's accounting records

B) Neither the parent company's nor the subsidiary's accounting records

C) The parent company's accounting records only

D) The subsidiary's accounting records only

A) Both the parent company's and the subsidiary's accounting records

B) Neither the parent company's nor the subsidiary's accounting records

C) The parent company's accounting records only

D) The subsidiary's accounting records only

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

28

On the date of a business combination resulting in a parent-subsidiary relationship, the differences between current fair values and carrying amounts of the subsidiary's identifiable net assets are:

A) Included in a working paper elimination

B) Recognized in the applicable asset and liability ledger accounts of the subsidiary

C) Recognized in the applicable asset and liability ledger accounts of the parent company

D) Accounted for in some other manner

A) Included in a working paper elimination

B) Recognized in the applicable asset and liability ledger accounts of the subsidiary

C) Recognized in the applicable asset and liability ledger accounts of the parent company

D) Accounted for in some other manner

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

29

Consolidated financial statements are intended primarily for the use of:

A) Stockholders of the parent company

B) Taxing authorities

C) Management of the parent company

D) Creditors of the parent company

A) Stockholders of the parent company

B) Taxing authorities

C) Management of the parent company

D) Creditors of the parent company

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

30

How is the minority interest in net assets of subsidiary displayed in a consolidated balance sheet under the economic unit concept of consolidated financial statements?

A) As a separate item in the liabilities section

B) As a deduction from consolidated goodwill, if any

C) By means of a note to the consolidated financial statements

D) As a separate item in the stockholders' equity section

A) As a separate item in the liabilities section

B) As a deduction from consolidated goodwill, if any

C) By means of a note to the consolidated financial statements

D) As a separate item in the stockholders' equity section

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

31

On November 30, 2006, Pegler Corporation paid $500,000 cash and issued 100,000 shares of $1 par common stock with a current fair value of $10 a share for all 50,000 outstanding shares of $5 par common stock (carrying amount $20 a share) of Stadler Company, which became a subsidiary of Pegler. Also on November 30, 2006, Pegler paid $50,000 for finder's, accounting, and legal fees related to the business combination and $80,000 for costs associated with the SEC registration statement for the common stock issued in the combination. The net result of Pegler's journal entries to record the combination is to:

A) Debit Investment in Stadler Company Common stock for $1,000,000

B) Credit Paid-In Capital in Excess of Par for $900,000

C) Debit Expenses of Business Combination for $130,000

D) Credit Cash for $630,000

A) Debit Investment in Stadler Company Common stock for $1,000,000

B) Credit Paid-In Capital in Excess of Par for $900,000

C) Debit Expenses of Business Combination for $130,000

D) Credit Cash for $630,000

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

32

Minority interest in net assets of subsidiary is displayed in the consolidated balance sheet as:

A) A part of consolidated stockholders' equity under the parent company concept of consolidated financial statements

B) A liability under the parent company concept of consolidated financial statements

C) An offset to investment in subsidiary common stock under the parent company concept of consolidated financial statements

D) An item between liabilities and stockholders' equity under the economic unit concept of consolidated financial statements

A) A part of consolidated stockholders' equity under the parent company concept of consolidated financial statements

B) A liability under the parent company concept of consolidated financial statements

C) An offset to investment in subsidiary common stock under the parent company concept of consolidated financial statements

D) An item between liabilities and stockholders' equity under the economic unit concept of consolidated financial statements

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

33

Before the computation of goodwill, the debits in the date-of-business-combination working paper elimination for the consolidated balance sheet of Promo Corporation and its 80%-owned subsidiary subtotaled $640,000, compared with a $540,000 credit to Investment in Sindow Company Common Stock-Promo. The working paper elimination should be completed with:

A) An allocation of the $100,000 bargain-purchase excess to reduce the amounts initially assigned to specified assets of Sindow.

B) A $100,000 credit to Minority Interest in Net Assets of Subsidiary

C) A $28,000 debit to Goodwill-Promo and a $128,000 credit to Minority Interest in Net Assets of Subsidiary

D) A $35,000 debit to Goodwill-Promo and a $135,000 credit to Minority Interest in Net Assets of Subsidiary

A) An allocation of the $100,000 bargain-purchase excess to reduce the amounts initially assigned to specified assets of Sindow.

B) A $100,000 credit to Minority Interest in Net Assets of Subsidiary

C) A $28,000 debit to Goodwill-Promo and a $128,000 credit to Minority Interest in Net Assets of Subsidiary

D) A $35,000 debit to Goodwill-Promo and a $135,000 credit to Minority Interest in Net Assets of Subsidiary

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

34

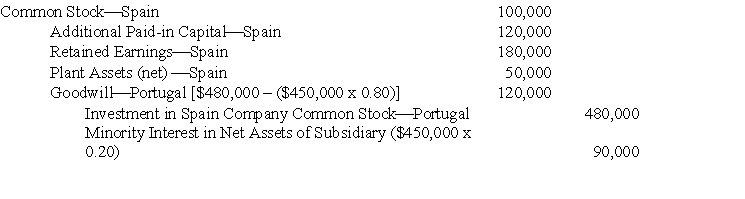

On June 30, 2006, Purdom Corporation acquired 80% of the outstanding common stock of Sudan Company. On the date of the business combination, identifiable net assets of Sudan with current fair values differing from carrying amounts were as follows:

Complete the following working paper for consolidated balance sheet of Purdom Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes.

Complete the following working paper for consolidated balance sheet of Purdom Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes. Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

35

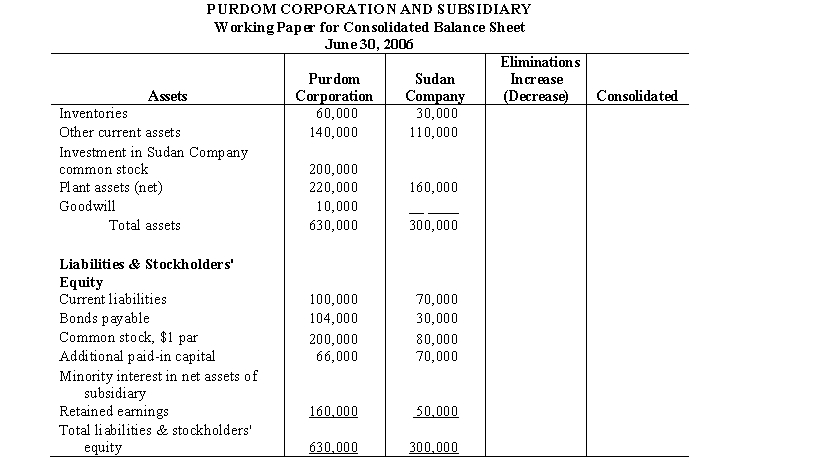

On May 31, 2006, Ping Corporation paid $300,000, including direct out-of-pocket costs of the business combination, for 82% of the outstanding common stock of Spring Company, which became a subsidiary. Differences between current fair values and carrying amounts of identifiable net assets of Spring Company on May 31, 2006, were limited to the following:

Complete the following working paper for consolidated balance sheet of Ping Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes.

Explanation of elimination: (a)

Complete the following working paper for consolidated balance sheet of Ping Corporation and subsidiary. Do not prepare a working paper elimination in journal entry format; however, explain the elimination on the working paper. Disregard income taxes. Explanation of elimination: (a) Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

36

Punt Corporation acquired a controlling interest in Saye Company for cash. The separate balance sheet of Punt and the consolidated balance sheet immediately after the business combination were as follows:

Plant assets of Saye Company were undervalued by $15,000 on the date of the business combination; the remainder of Punt's cost was assigned to goodwill. The retained earnings of Saye on the date of the business combination amounted to $37,000.

a. Prepare the separate balance sheet of Saye Company on the date of the business combination.

b. What percentage of the common stock of Saye was acquired by Punt?

c. Prepare the working paper elimination (in journal entry format) for Punt Corporation and subsidiary on the date of the business combination.

Plant assets of Saye Company were undervalued by $15,000 on the date of the business combination; the remainder of Punt's cost was assigned to goodwill. The retained earnings of Saye on the date of the business combination amounted to $37,000.a. Prepare the separate balance sheet of Saye Company on the date of the business combination.

b. What percentage of the common stock of Saye was acquired by Punt?

c. Prepare the working paper elimination (in journal entry format) for Punt Corporation and subsidiary on the date of the business combination.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

37

On December 31, 2006, the balance sheet of Sint Company included stockholders' equity of $2,000,000. On that date, Plane Corporation acquired for cash a controlling interest in the common stock of Sint. The December 31, 2006, current fair values of Sint's identifiable net assets totaled $2,400,000, and goodwill computed as the difference between Plane's cost and its share of the current fair value of Sint's identifiable net assets was $180,000.

Prepare a working paper to compute the total cost of Plane's investment in Sint if Plane owns:

a. 100% of Sint's common stock

b. 90% of Sint's common stock

c. 80% of Sint's common stock

Prepare a working paper to compute the total cost of Plane's investment in Sint if Plane owns:

a. 100% of Sint's common stock

b. 90% of Sint's common stock

c. 80% of Sint's common stock

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

38

On April 30, 2006, Press Corporation paid $168,000 cash for 80% of the outstanding common stock of Sow Company. Legal, accounting, and finder's fees paid by Press relative to the business combination totaled $24,000. The current fair value of Sow's identifiable net assets was $220,000 on April 30, 2006; the carrying amount was $200,000.

Prepare a working paper to compute the minority interest and goodwill in the April 30, 2006 consolidated balance sheet of Press Corporation and subsidiary under each of the following independent assumptions:

a. Sow's identifiable net assets are recognized at current fair value; minority interest is based on current fair value of identifiable net assets.

b. Sow's identifiable net assets are recognized at current fair value only to the extent of Press Corporation's interest; balance of net assets and minority interest are reflected at carrying amounts in Sow's accounting records.

c. Current fair value, through inference, is assigned to total net assets of Sow, including goodwill.

Prepare a working paper to compute the minority interest and goodwill in the April 30, 2006 consolidated balance sheet of Press Corporation and subsidiary under each of the following independent assumptions:

a. Sow's identifiable net assets are recognized at current fair value; minority interest is based on current fair value of identifiable net assets.

b. Sow's identifiable net assets are recognized at current fair value only to the extent of Press Corporation's interest; balance of net assets and minority interest are reflected at carrying amounts in Sow's accounting records.

c. Current fair value, through inference, is assigned to total net assets of Sow, including goodwill.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

39

In a proposed Statement, "Consolidated Financial Statements: Purpose and Policy," the FASB would replace objectively determined legal form by subjectively determined economic substance as a basis for consolidated financial statements. Majority ownership of an investee's outstanding common stock would no longer be a prerequisite for consolidation.

a. Present arguments in support of the FASB's proposal.

b. Present arguments in opposition to the FASB's proposal.

a. Present arguments in support of the FASB's proposal.

b. Present arguments in opposition to the FASB's proposal.

Unlock Deck

Unlock for access to all 39 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 39 flashcards in this deck.