Deck 20: Performance Measurement Systems Glossary Photo Credits

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

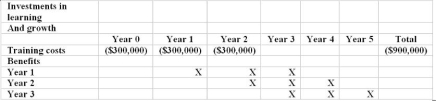

Ignoring the time value of money, what is the break-even benefit level per year?

Joplin Corporation showed the following relationship between training costs and training benefits:

A) $900,000 per year

B) $300,000 per year

C) $ 100,000 per year

D) $ 33,333 per year

Joplin Corporation showed the following relationship between training costs and training benefits:

A) $900,000 per year

B) $300,000 per year

C) $ 100,000 per year

D) $ 33,333 per year

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

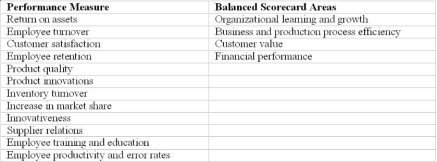

Match each of the following performance measures to one or more of the four areas of a balanced scorecard. Note that a performance measure can relate to more than one area.

Question

Question

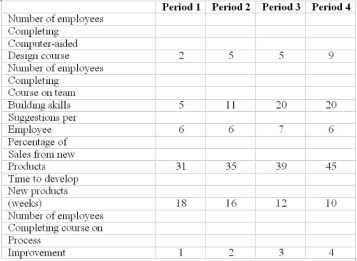

Aries Corporation places great importance on organizational learning to enhance the skills and capabilities of its employees. Ming Tsai, the Human Resources Manager of Aries, encourages all employees to acquire relevant skills and knowledge by attending evening courses in the local community college and special training sessions arranged in-house.

Tsai tracked the following data for the last four periods:

Required:

(a) From the above list of indicators, identify the leading and lagging indicators and indicate the cause-effect relationships.

(b) Comment on the trends present in the above indicators of organizational learning and growth. Do you believe that organizational capabilities are improving?

Tsai tracked the following data for the last four periods:

Required:

(a) From the above list of indicators, identify the leading and lagging indicators and indicate the cause-effect relationships.

(b) Comment on the trends present in the above indicators of organizational learning and growth. Do you believe that organizational capabilities are improving?

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/81

Play

Full screen (f)

Deck 20: Performance Measurement Systems Glossary Photo Credits

1

Leading indicators are measures that identify future financial and non-financial outcomes as guides to management decision making.

True

2

Lagging indicators measure the final outcomes of management plans and their execution.

True

3

Leading indicators of performance are always financial in nature.

False

4

Organizational learning and growth is a major lagging indicator of a company's performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

5

A leading indicator at one stage of the value-chain can be a lagging indicator at another stage.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

6

Most financial performance measures are leading indicators.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

7

A successful balanced scorecard is a random selection of readily available measures of performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

8

The internal business process area of a balanced scorecard indicates how processes work to add value to customers.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

9

Balanced scorecards are primarily used by mid and upper-level management personnel.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

10

A balanced scorecard contains only qualitative measures of performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

11

A balanced scorecard contains both quantitative and qualitative measures of performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

12

When using a balanced scorecard approach, it is not possible to quantify the benefit received from employee training.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

13

Employee productivity can be measured in either physical measures or financial measures.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

14

The number of units inspected would be an example of a financial measure of employee productivity.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

15

Customer satisfaction is the degree to which an organization's products and services meet customers' needs.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

16

Customer value measures the revenues generated per customer.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

17

Logically, a cause-and-effect relationship exists between improvements in organizational learning and growth and improvements in internal business and production processes.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

18

Customer value reflects the degree to which products and services satisfy customers' expectations about the price, function and quality of those products and services.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

19

Customer satisfaction with current products and services is a lagging indicator.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

20

Market share is usually measured by the percentage of a company's customers over the total potential customers.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

21

Market share can be measured in terms of dollar sales, unit volume, or number of customers.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

22

Poor financial performance can often be traced to lapses in leading indicator performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

23

The balanced scorecard is a causal model of leading and lagging indicators of performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

24

The balanced scorecard uses only lagging indicators of performance to communicate to employees the impacts and values of their actions.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

25

Balanced scorecards do not work well in nonprofit environments because of their lack of financial performance measures.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

26

The greatest benefit of using a balanced scorecard is that company profits always improve.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

27

Critical success factors are important key performance indicators in a corporation.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

28

Companies that have achieved the most success using balanced scorecards have utilized a top-down management approach in its design.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

29

The primary purpose of the balanced scorecard should be as a management tool for employee incentives and financial rewards.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

30

The primary purpose of the balanced scorecard should be to communicate and implement corporate strategy.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

31

Most observers believe that a top-down management approach is the most successful way to implement a balanced scorecard.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

32

A participative, bottom-up approach to designing a balanced scorecard improves its acceptance and use by the organization's members.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

33

Measurement of average cycle time would be found in the financial performance section of a balanced scorecard.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

34

Market share would most likely be found in the customer value section of a balanced scorecard.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

35

The financial performance section of a balanced scorecard would include a company's revenue growth.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

36

Pay for performance incentive systems base at least some portion of a manager's income on measures of organizational performance rather than a guaranteed amount.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

37

Absolute performance evaluation compares an individual's performance to that of others.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

38

Absolute performance evaluation compares individual performance to set objectives or expectations.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

39

A performance evaluation formula computes rewards earned for specific achievements.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

40

Stock appreciation rights (SARs) confer bonuses to employees based on increases in stock prices for a predetermined number of shares.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

41

A manager receiving a deferred reward is less likely to invest in new technology because of the impact on earnings of the company of such an investment.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

42

It is impossible to use the balanced scorecard as a basis for incentive systems because it contains so many non financial measures of performance.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

43

A leading indicator:

A) Measures the final outcomes of management plans and their execution

B) Is a measure of outcomes of early value chain operations that signal future outcomes of later operations

C) Can also be a lagging indicator at another stage in the value chain

D) Both B and C

A) Measures the final outcomes of management plans and their execution

B) Is a measure of outcomes of early value chain operations that signal future outcomes of later operations

C) Can also be a lagging indicator at another stage in the value chain

D) Both B and C

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following statements about customer satisfaction is false?

A) Customer satisfaction is the degree to which an organization's products and services meet customers' needs

B) Alert, well-trained employees may be able to take corrective actions to prevent loss of future sales

C) Customer satisfaction with current products and services is a lead indicator of future sales

D) Improvements of customer satisfaction usually are lead indicators of organization capabilities and process efficiency

A) Customer satisfaction is the degree to which an organization's products and services meet customers' needs

B) Alert, well-trained employees may be able to take corrective actions to prevent loss of future sales

C) Customer satisfaction with current products and services is a lead indicator of future sales

D) Improvements of customer satisfaction usually are lead indicators of organization capabilities and process efficiency

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

45

A balanced scorecard is:

A) A chart showing all of the costs compared to budgeted amounts per unit

B) A listing of all indicators of past performance

C) A causal model of leading and lagging indicators of performance that demonstrates how changes in one . operation cause or are balanced by changes in others

D) A report outlining the company's achievement of target costs

A) A chart showing all of the costs compared to budgeted amounts per unit

B) A listing of all indicators of past performance

C) A causal model of leading and lagging indicators of performance that demonstrates how changes in one . operation cause or are balanced by changes in others

D) A report outlining the company's achievement of target costs

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

46

In a balanced scorecard, which of the following would be a measure of the business and production process performance?

A) Process improvements

B) Retention of existing customers

C) Average employee education level

D) Percentage of on time deliveries

A) Process improvements

B) Retention of existing customers

C) Average employee education level

D) Percentage of on time deliveries

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following best describes the business and production process performance area of the balanced scorecard?

A) Indicates how the infrastructure for innovation and long-term growth should contribute to a company's strategic goals

B) Indicates how a customer oriented strategy adds financial value

C) Indicates how areas of the company should work to add value to customers

D) Measures the company's success in adding value to shareholders

A) Indicates how the infrastructure for innovation and long-term growth should contribute to a company's strategic goals

B) Indicates how a customer oriented strategy adds financial value

C) Indicates how areas of the company should work to add value to customers

D) Measures the company's success in adding value to shareholders

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is true about balanced scorecards?

A) A balanced scorecard compares value added and non-value added activities in a company

B) A balanced scorecard is used more by smaller companies than those with modern manufacturing facilities

C) A balanced scorecard attempts to show causal relationships among major areas of performance in a company

D) A balanced scorecard is a qualitative rather than quantitative measure of a company's performance

A) A balanced scorecard compares value added and non-value added activities in a company

B) A balanced scorecard is used more by smaller companies than those with modern manufacturing facilities

C) A balanced scorecard attempts to show causal relationships among major areas of performance in a company

D) A balanced scorecard is a qualitative rather than quantitative measure of a company's performance

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

49

Ignoring the time value of money, what is the break-even benefit level per year?

Joplin Corporation showed the following relationship between training costs and training benefits:

A) $900,000 per year

B) $300,000 per year

C) $ 100,000 per year

D) $ 33,333 per year

Joplin Corporation showed the following relationship between training costs and training benefits:

A) $900,000 per year

B) $300,000 per year

C) $ 100,000 per year

D) $ 33,333 per year

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

50

Nino Corporation conducted a study of the relationship between employee training costs and benefits. The company determined that it has break-even benefit level of $45,698 per year. This result indicates that Schiller should:

A) Spend at least $45,698 per employee annually on employee training programs

B) Invest in employee training programs if the benefits will be at least $45,698 per employee annually

C) Generate at least $45,698 in additional sales for every $1 spent on employee training programs

D) Expect to save $45,698 per year per employee on waste and efficiency

A) Spend at least $45,698 per employee annually on employee training programs

B) Invest in employee training programs if the benefits will be at least $45,698 per employee annually

C) Generate at least $45,698 in additional sales for every $1 spent on employee training programs

D) Expect to save $45,698 per year per employee on waste and efficiency

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following statements regarding balanced scorecards isFalse?

A) The greatest value of the balanced scorecard is that it encourages all employees to consider the impact of their actions on profitability

B) Balanced scorecards are only useful in the public sector

C) A balance scorecard continuously evolves as the organization learns and evolves

D) A balanced scorecard measures both financial and non financial results

A) The greatest value of the balanced scorecard is that it encourages all employees to consider the impact of their actions on profitability

B) Balanced scorecards are only useful in the public sector

C) A balance scorecard continuously evolves as the organization learns and evolves

D) A balanced scorecard measures both financial and non financial results

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following would be a balanced scorecard measurement of customer value?

A) Customer retention rate

B) Employee turnover

C) Percentage of lost customers

D) Return on sales

A) Customer retention rate

B) Employee turnover

C) Percentage of lost customers

D) Return on sales

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

53

Which of the following would be a balanced scorecard measure in the financial performance area?

A) Customer retention rate

B) Employee turnover

C) Percentage of lost customers

D) Return on sales

A) Customer retention rate

B) Employee turnover

C) Percentage of lost customers

D) Return on sales

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following would not be a balanced scorecard measure in the business and production efficiency area?

A) Net income growth

B) Supplier error rates

C) Supplier cycle time

D) Defects per 100 units

A) Net income growth

B) Supplier error rates

C) Supplier cycle time

D) Defects per 100 units

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is measured in the organizational learning and growth area of a balanced scorecard?

A) Supplier relations

B) Customer satisfaction

C) Employee turnover

D) Revenue growth

A) Supplier relations

B) Customer satisfaction

C) Employee turnover

D) Revenue growth

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following would be a performance target in the financial performance area of a balanced scorecard?

A) Account and revenue growth of 10% per year

B) Reduction in errors of production from 8 in 1000 pieces to 3 in 1000 pieces

C) Revenue growth above the industry average

D) 25% of sales from new services

A) Account and revenue growth of 10% per year

B) Reduction in errors of production from 8 in 1000 pieces to 3 in 1000 pieces

C) Revenue growth above the industry average

D) 25% of sales from new services

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following is not a commonly used theory of incentive and behavior?

A) Financial rewards theory

B) Goal-setting theory

C) Expectancy theory

D) Agency theory

A) Financial rewards theory

B) Goal-setting theory

C) Expectancy theory

D) Agency theory

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following statements regarding incentive reward systems is False?

A) Employees must believe that their efforts influence performance

B) Performance measures must be observable and verifiable

C) Impossible goals motivate employees more than easy-to-attain goals

D) Performance measures and related rewards must reflect organizational goals

A) Employees must believe that their efforts influence performance

B) Performance measures must be observable and verifiable

C) Impossible goals motivate employees more than easy-to-attain goals

D) Performance measures and related rewards must reflect organizational goals

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

59

Absolute performance evaluation:

A) Compares an individual's performance to that of others

B) Bases rewards on a performance evaluation formula

C) Compares individual performance to set objectives or expectations

D) Uses non-quantified criteria to evaluate individuals

A) Compares an individual's performance to that of others

B) Bases rewards on a performance evaluation formula

C) Compares individual performance to set objectives or expectations

D) Uses non-quantified criteria to evaluate individuals

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

60

Relative performance evaluation:

A) Compares an individual's performance to that of others

B) Bases rewards on a performance evaluation formula

C) Compares individual performance to set objectives or expectations

D) Uses non-quantified criteria to evaluate individuals

A) Compares an individual's performance to that of others

B) Bases rewards on a performance evaluation formula

C) Compares individual performance to set objectives or expectations

D) Uses non-quantified criteria to evaluate individuals

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

61

Subjective performance evaluation:

A) Compares an individual's performance to that of others

B) Bases rewards on a performance evaluation formula

C) Compares individual performance to set objectives or expectations

D) Uses non-quantified criteria to evaluate individuals

A) Compares an individual's performance to that of others

B) Bases rewards on a performance evaluation formula

C) Compares individual performance to set objectives or expectations

D) Uses non-quantified criteria to evaluate individuals

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following is not a financial performance measure?

A) Reducing overall costs by 13%

B) Achieving revenue growth of 10% annually

C) Overall value of the manager to the organization is in the top 15% of all managers

D) Increasing the company stock price 18%

A) Reducing overall costs by 13%

B) Achieving revenue growth of 10% annually

C) Overall value of the manager to the organization is in the top 15% of all managers

D) Increasing the company stock price 18%

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following is not a cost of including nonfinancial measures in incentive plans?

A) The danger of information overload from too many measures of performance

B) The increased cost of performance measurement and supporting information systems

C) Increased opportunities for disputes over the validity of performance measures

D) All of the above are costs of including nonfinancial measures in incentive plans

A) The danger of information overload from too many measures of performance

B) The increased cost of performance measurement and supporting information systems

C) Increased opportunities for disputes over the validity of performance measures

D) All of the above are costs of including nonfinancial measures in incentive plans

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

64

Stock appreciation rights (SARs):

A) Give an individual the right to purchase a certain number of shares at a specified price over a specified time period

B) Confer bonuses to employees based on increases in stock prices for a predetermined number of shares

C) Should never be used as employee incentives because they are too narrowly focused on the company's stock price

D) Are considered to be a current reward of employee performance

A) Give an individual the right to purchase a certain number of shares at a specified price over a specified time period

B) Confer bonuses to employees based on increases in stock prices for a predetermined number of shares

C) Should never be used as employee incentives because they are too narrowly focused on the company's stock price

D) Are considered to be a current reward of employee performance

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following statements is True regarding balanced scorecard-based incentive systems?

A) Incentive rewards are based on financial performance only

B) Balanced scorecards should never be used in incentive systems because of their subjective nature

C) Explicit incentives should be tied to performance measures

D) Only the financial aspects of balanced scorecards should be used as incentive measures

A) Incentive rewards are based on financial performance only

B) Balanced scorecards should never be used in incentive systems because of their subjective nature

C) Explicit incentives should be tied to performance measures

D) Only the financial aspects of balanced scorecards should be used as incentive measures

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following is not an element that should be considered when designing an incentive system?

A) Are all employees satisfied with the reward system that is designed?

B) Should the reward system be formula-based or based on subjective performance?

C) Should rewards be current or deferred?

D) Should rewards consist of salary, bonus, or be stock-based?

A) Are all employees satisfied with the reward system that is designed?

B) Should the reward system be formula-based or based on subjective performance?

C) Should rewards be current or deferred?

D) Should rewards consist of salary, bonus, or be stock-based?

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following statements describes expectancy theory?

A) People are motivated by financial rewards only

B) To motivate people, incentive plans should not include undesirable penalties for poor performance

C) People are motivated by monetary or nonmonetary incentives

D) Impossible goals result in extra incentive and motivation

A) People are motivated by financial rewards only

B) To motivate people, incentive plans should not include undesirable penalties for poor performance

C) People are motivated by monetary or nonmonetary incentives

D) Impossible goals result in extra incentive and motivation

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is not an accepted theory of motivation and incentives?

A) Goal-setting theory

B) Pay for performance theory

C) Expectancy theory

D) Agency theory

A) Goal-setting theory

B) Pay for performance theory

C) Expectancy theory

D) Agency theory

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

69

Which of the following statements about agency theory is True?

A) Agency theory focuses on the characteristics of incentive plans that motivate people

B) Agency theory focuses on the contracting behavior between principal and agent

C) Agency theory works with the assumption that easy goals will motivate employees to perform at the highest level

D) Agency theory seeks to understand the types of performance measures and rewards that motivate employees

A) Agency theory focuses on the characteristics of incentive plans that motivate people

B) Agency theory focuses on the contracting behavior between principal and agent

C) Agency theory works with the assumption that easy goals will motivate employees to perform at the highest level

D) Agency theory seeks to understand the types of performance measures and rewards that motivate employees

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following statements about goal-setting theory is False?

A) Impossible goals all but eliminate motivation because people realize that the desired performance and rewards cannot be achieved

B) Easy goals reduce motivation to the minimum necessary to achieve them

C) Both principals and agents want to maximize their rewards at a minimum cost

D) Difficult but attainable goals consistently create the most motivation and effort, and lead to the highest level of performance

A) Impossible goals all but eliminate motivation because people realize that the desired performance and rewards cannot be achieved

B) Easy goals reduce motivation to the minimum necessary to achieve them

C) Both principals and agents want to maximize their rewards at a minimum cost

D) Difficult but attainable goals consistently create the most motivation and effort, and lead to the highest level of performance

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

71

Match each of the following performance measures to one or more of the four areas of a balanced scorecard. Note that a performance measure can relate to more than one area.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

72

Holloway Corporation estimates that a three percentage point increase in retained customers is estimated to cause the organization's gross margin ratio to increase by 2.4 percentage points.

The company's current sales are $20,000,000 and the company is considering a $200,000 advertising campaign, which it estimates will increase the company's retained customers by 4 percentage points. Should the company continue with the advertising campaign?

The company's current sales are $20,000,000 and the company is considering a $200,000 advertising campaign, which it estimates will increase the company's retained customers by 4 percentage points. Should the company continue with the advertising campaign?

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

73

Aries Corporation places great importance on organizational learning to enhance the skills and capabilities of its employees. Ming Tsai, the Human Resources Manager of Aries, encourages all employees to acquire relevant skills and knowledge by attending evening courses in the local community college and special training sessions arranged in-house.

Tsai tracked the following data for the last four periods:

Required:

(a) From the above list of indicators, identify the leading and lagging indicators and indicate the cause-effect relationships.

(b) Comment on the trends present in the above indicators of organizational learning and growth. Do you believe that organizational capabilities are improving?

Tsai tracked the following data for the last four periods:

Required:

(a) From the above list of indicators, identify the leading and lagging indicators and indicate the cause-effect relationships.

(b) Comment on the trends present in the above indicators of organizational learning and growth. Do you believe that organizational capabilities are improving?

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

74

Fred Doyle, assistant controller, was analyzing alternative ways of increasing gross margin of Somerset Corporation, a manufacturer of fashion clothing. He knew that the following relationship existed between the increase in the sales levels through retention of customers (dX) and the increase in gross margin (dY): dY = (0.60) * (dX)

The marketing and department provided information about four different alternative plans of improving the retention rate of customers.

Alternative 1 Improving quality will retain 20 customers who might have otherwise switched suppliers. Each retained customer will bring in sales revenues of $21,000 on average. The improvements in quality will come through two measures: switching to a substitute material that will cost $8,500 per customer, and purchasing an automatic inspection unit that will cost $80,000.

Alternative 2 An increase in advertising will likely retain 12 customers at an average sales revenue of $25,000 per customer. Increased advertising will cost the company $200,000.

Alternative 3 A price discount will retain 18 customers at an average sales revenue of $30,000 per customer. The discount offer will cost the company $240,000 in lost contribution margin. In addition, the company must spend $70,000 in advertising the sales discount promotion to customers.

Alternative 4 The company has made improvements in the process which will improve its on-time delivery performance by 28% over the previous year. Consequently, it can retain 32 customers at an average sales revenue of $20,000 per customer. Improvements in the process cost the company cost the company as follows: (1) increase in labor costs $170,000, (2) increase in processing costs due to flexible processing technology $180,000, and (3) increase in miscellaneous costs $26,000.

Required

(a) Compute the cost-benefit of the four alternatives.

(b) Which of the above alternatives would you recommend to the operations manager of the company? Why?

The marketing and department provided information about four different alternative plans of improving the retention rate of customers.

Alternative 1 Improving quality will retain 20 customers who might have otherwise switched suppliers. Each retained customer will bring in sales revenues of $21,000 on average. The improvements in quality will come through two measures: switching to a substitute material that will cost $8,500 per customer, and purchasing an automatic inspection unit that will cost $80,000.

Alternative 2 An increase in advertising will likely retain 12 customers at an average sales revenue of $25,000 per customer. Increased advertising will cost the company $200,000.

Alternative 3 A price discount will retain 18 customers at an average sales revenue of $30,000 per customer. The discount offer will cost the company $240,000 in lost contribution margin. In addition, the company must spend $70,000 in advertising the sales discount promotion to customers.

Alternative 4 The company has made improvements in the process which will improve its on-time delivery performance by 28% over the previous year. Consequently, it can retain 32 customers at an average sales revenue of $20,000 per customer. Improvements in the process cost the company cost the company as follows: (1) increase in labor costs $170,000, (2) increase in processing costs due to flexible processing technology $180,000, and (3) increase in miscellaneous costs $26,000.

Required

(a) Compute the cost-benefit of the four alternatives.

(b) Which of the above alternatives would you recommend to the operations manager of the company? Why?

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

75

Consider the following information pertaining to the balanced scorecard of a company:

● A 500-hour increase in job-related training will (a) increase the average employee education level by

1 point on a 100-point scale, (b) reduce cycle time by 0.8 hours, and (c) decrease defective products by 0.3% points.

● A one-point increase in the average education level (on a 100-point scale) will (d) decrease average cycle time by 0.5 hours and (e) decrease defective products by 0.1% points.

● A 1% decrease in defective products will (f) decrease average cycle time by 1 hour and (g) increase on-time deliveries by 0.2%.

● A one-hour decrease in average cycle time will (h) increase on-time deliveries by 0.1% points.

● A 1% point increase in on-time deliveries will (i) increase retained customers by 0.7% points.

● A 1% point increase in retained customers will (j) increase the gross margin ratio by 0.3% points.

Required

(a) Express the cause-effect relationships among the different indicators visually.

(b) Would you expect the benefits of job related training to increase proportionately? For example, would

you expect the benefit of 50,000 hours of job-related training to be 100 times the impact of 500 hours of

training

● A 500-hour increase in job-related training will (a) increase the average employee education level by

1 point on a 100-point scale, (b) reduce cycle time by 0.8 hours, and (c) decrease defective products by 0.3% points.

● A one-point increase in the average education level (on a 100-point scale) will (d) decrease average cycle time by 0.5 hours and (e) decrease defective products by 0.1% points.

● A 1% decrease in defective products will (f) decrease average cycle time by 1 hour and (g) increase on-time deliveries by 0.2%.

● A one-hour decrease in average cycle time will (h) increase on-time deliveries by 0.1% points.

● A 1% point increase in on-time deliveries will (i) increase retained customers by 0.7% points.

● A 1% point increase in retained customers will (j) increase the gross margin ratio by 0.3% points.

Required

(a) Express the cause-effect relationships among the different indicators visually.

(b) Would you expect the benefits of job related training to increase proportionately? For example, would

you expect the benefit of 50,000 hours of job-related training to be 100 times the impact of 500 hours of

training

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

76

Syed Ali, an accountant, was recently hired by LOGAN INDUSTRIES, Inc. As part of his first task,

Feingold was asked to develop a balanced scorecard for the company. He developed the following

measures:

On-time deliveries

Customer retention

Customer profitability

Product innovation

Market share

Return on assets

Number of defectives

Employee satisfaction

Employee training

Ali knows that some of these indicators are what are called leading indicators and others are lagging indicators. However, he does not know enough and has approached you to help him.

Required

(a) Re-arrange the above indicators to reflect whether they are lead or lag indicators. Also identify the cause-effect relationships that may exist.

(b) Why is it important for managers to differentiate between leading and lagging indicators?

(c) Classify the above indicators under the different perspectives of the balanced scorecard.

(d) How many measures under each perspective of the balanced scorecard should a company use? Why?

(e) Briefly discuss the major benefits of the balanced scorecard.

(f) Identify and briefly discuss three types of costs associated with the balanced scorecard.

Feingold was asked to develop a balanced scorecard for the company. He developed the following

measures:

On-time deliveries

Customer retention

Customer profitability

Product innovation

Market share

Return on assets

Number of defectives

Employee satisfaction

Employee training

Ali knows that some of these indicators are what are called leading indicators and others are lagging indicators. However, he does not know enough and has approached you to help him.

Required

(a) Re-arrange the above indicators to reflect whether they are lead or lag indicators. Also identify the cause-effect relationships that may exist.

(b) Why is it important for managers to differentiate between leading and lagging indicators?

(c) Classify the above indicators under the different perspectives of the balanced scorecard.

(d) How many measures under each perspective of the balanced scorecard should a company use? Why?

(e) Briefly discuss the major benefits of the balanced scorecard.

(f) Identify and briefly discuss three types of costs associated with the balanced scorecard.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

77

Assume the role of a consultant preparing a report for MTI. Discuss the following aspects in your report: The internal value-chain of MTI

The balanced scorecard. Identify the goals of the company under each perspective of the scorecard and cause-effect relationships, and develop potential measures that could be used

How the inter-departmental differences can be eliminated

Sam Mahoney, the CEO of Mahoney Technologies, Inc. (MTI), a biotechnology firm had recently returned from a conference on modern cost management and performance measurement methods where he was exposed to target costing, value-chain analysis, balanced scorecard, activity-based management and other ideas.

MTI is a five-year old company operating in a growing, but competitive market. It develops and produces a number of different enzymes for use by research scientists and pharmaceutical companies. Its main competitors are also small to medium sized firms just like MTI. The key to growth in this industry is the ability to develop new products in a short time. Gail Stevenson, the vice-president (VP) for research & development (R&D) has noticed that some of MTI's new developments did not perform well because of the delays in their introduction into the market. Stevenson is very keen on hiring the best scientists and ensuring that they stay current in their fields because knowledge is the key competitive weapon in the biotechnology industry.

Bob Phillips, the controller of MTI had another concern. He has been noticing that the new products were not only delayed but their actual development costs were usually higher than budgeted. One of his goals was to see that the new products were profitable for the company.

Linda Joseph, the production manager, had a different concern of her own. Based on her observation, the production of the new enzymes was taking longer. Her feeling was that the products spent too much time in the quality control (QC) department. Barry Laker, the manager of the QC department argued that the new enzymes lacked the rigorous specifications that are demanded in the marketplace. Consequently, the QC department has had to perform additional tests to get to the root cause of the problems.

Mahoney had heard complaints from all quarters, and decided to convene a meeting of all the department heads.

Mahoney: Good afternoon, everyone. I am troubled that despite hiring a number of talented scientists, we are unable to compete effectively in the marketplace. Many of the recent entrants in the game seem to be beating us easily.

Stevenson: Sam, the key to our growth is rapid introduction of new products. Although my scientists are developing new enzymes in record times, they seem to be getting held up in manufacturing and especially the QC department.

Laker: Sam, I think I can pinpoint the root cause of the problem. I agree that our scientists are developing new enzymes in record times, but they do not seem to be paying any attention to standards. It looks like my department will have to provide training to them regarding quality control matters.

Stevenson: With due respect, I do not think there is more to know about QC standards. It looks like the department wants more attention and is therefore creating all this unnecessary fuss.

Joseph: I think I will agree with Barry that there are problems at the R&D side. My production scientists are also complaining that adequate specifications have not been developed; they have to constantly phone their R&D counterparts for clarifications.

Stevenson: I do not believe that the production problems can be attributed to R&D) I have personally screened each and every scientist during the hiring process.

Phillips: I don't think we will make much progress as a company if we keep pointing fingers at one another. We all must realize that all problems, regardless of their origin, finally affect the bottom-line of our company. Unless we set aside our differences and work together as a team, we will be unable to compete with our rivals. Some of our competitors follow best practices, which we must try to emulate. Mahoney: I agree with Bob. We must all look for solutions. I recently attended a conference where noted speakers talked about the value-chain of a company, interrelationships between functions, and the balanced scorecard. In fact, some speakers suggested that companies must stop discussing in terms of individual functions or departments; instead they must talk in terms of processes and understand linkages among all the processes that exist in an organization. I believe there are a number of ideas that we could adopt. I will leave the conference proceedings in the library, and suggest that we all read about these different topics. How about getting together after six weeks and discussing a plan of action? Thank you and see you all after six weeks.

Required

The balanced scorecard. Identify the goals of the company under each perspective of the scorecard and cause-effect relationships, and develop potential measures that could be used

How the inter-departmental differences can be eliminated

Sam Mahoney, the CEO of Mahoney Technologies, Inc. (MTI), a biotechnology firm had recently returned from a conference on modern cost management and performance measurement methods where he was exposed to target costing, value-chain analysis, balanced scorecard, activity-based management and other ideas.

MTI is a five-year old company operating in a growing, but competitive market. It develops and produces a number of different enzymes for use by research scientists and pharmaceutical companies. Its main competitors are also small to medium sized firms just like MTI. The key to growth in this industry is the ability to develop new products in a short time. Gail Stevenson, the vice-president (VP) for research & development (R&D) has noticed that some of MTI's new developments did not perform well because of the delays in their introduction into the market. Stevenson is very keen on hiring the best scientists and ensuring that they stay current in their fields because knowledge is the key competitive weapon in the biotechnology industry.

Bob Phillips, the controller of MTI had another concern. He has been noticing that the new products were not only delayed but their actual development costs were usually higher than budgeted. One of his goals was to see that the new products were profitable for the company.

Linda Joseph, the production manager, had a different concern of her own. Based on her observation, the production of the new enzymes was taking longer. Her feeling was that the products spent too much time in the quality control (QC) department. Barry Laker, the manager of the QC department argued that the new enzymes lacked the rigorous specifications that are demanded in the marketplace. Consequently, the QC department has had to perform additional tests to get to the root cause of the problems.

Mahoney had heard complaints from all quarters, and decided to convene a meeting of all the department heads.

Mahoney: Good afternoon, everyone. I am troubled that despite hiring a number of talented scientists, we are unable to compete effectively in the marketplace. Many of the recent entrants in the game seem to be beating us easily.

Stevenson: Sam, the key to our growth is rapid introduction of new products. Although my scientists are developing new enzymes in record times, they seem to be getting held up in manufacturing and especially the QC department.

Laker: Sam, I think I can pinpoint the root cause of the problem. I agree that our scientists are developing new enzymes in record times, but they do not seem to be paying any attention to standards. It looks like my department will have to provide training to them regarding quality control matters.

Stevenson: With due respect, I do not think there is more to know about QC standards. It looks like the department wants more attention and is therefore creating all this unnecessary fuss.

Joseph: I think I will agree with Barry that there are problems at the R&D side. My production scientists are also complaining that adequate specifications have not been developed; they have to constantly phone their R&D counterparts for clarifications.

Stevenson: I do not believe that the production problems can be attributed to R&D) I have personally screened each and every scientist during the hiring process.

Phillips: I don't think we will make much progress as a company if we keep pointing fingers at one another. We all must realize that all problems, regardless of their origin, finally affect the bottom-line of our company. Unless we set aside our differences and work together as a team, we will be unable to compete with our rivals. Some of our competitors follow best practices, which we must try to emulate. Mahoney: I agree with Bob. We must all look for solutions. I recently attended a conference where noted speakers talked about the value-chain of a company, interrelationships between functions, and the balanced scorecard. In fact, some speakers suggested that companies must stop discussing in terms of individual functions or departments; instead they must talk in terms of processes and understand linkages among all the processes that exist in an organization. I believe there are a number of ideas that we could adopt. I will leave the conference proceedings in the library, and suggest that we all read about these different topics. How about getting together after six weeks and discussing a plan of action? Thank you and see you all after six weeks.

Required

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

78

The New York Times recently reported that a number of publicly-held corporations have been accused of illegally doctoring hourly employees' time records. Examples included:

? Workers sued Family Dollar and Pep Boys, accusing managers of deleting hours from their time records.

? More than a dozen former Wal-Mart employees said in interviews and depositions that managers had altered time records to shortchange employees.

? The Department of Labor reached two back-pay settlements with Kinko's photocopy centers after finding that managers had erased time for 13 employees.

When interviewed, many of the managers cited pressure from upper-management and the impact of their actions on their own compensation as underlying causes for their actions. All of the companies strongly denied encouraging such illegal and unethical behavior by managers. Compensation experts interviewed agreed that the companies' incentive performance systems may have contributed to the managers' behavior. (New York Times, April 4, 2004)

Required:

(a) Explain how the incentive performance systems of the above named companies could have contributed to this illegal behavior by managers.

(b) Discuss the ethical issues involved in the design of incentive performance systems. In designing a performance-based incentive system, what measures should companies take to avoid illegal and unethical behavior by supervisors?

? Workers sued Family Dollar and Pep Boys, accusing managers of deleting hours from their time records.

? More than a dozen former Wal-Mart employees said in interviews and depositions that managers had altered time records to shortchange employees.

? The Department of Labor reached two back-pay settlements with Kinko's photocopy centers after finding that managers had erased time for 13 employees.

When interviewed, many of the managers cited pressure from upper-management and the impact of their actions on their own compensation as underlying causes for their actions. All of the companies strongly denied encouraging such illegal and unethical behavior by managers. Compensation experts interviewed agreed that the companies' incentive performance systems may have contributed to the managers' behavior. (New York Times, April 4, 2004)

Required:

(a) Explain how the incentive performance systems of the above named companies could have contributed to this illegal behavior by managers.

(b) Discuss the ethical issues involved in the design of incentive performance systems. In designing a performance-based incentive system, what measures should companies take to avoid illegal and unethical behavior by supervisors?

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

79

Briefly explain the underlying principle behind each of the theories of motivation and behavior. What specific aspects are built into incentive plans that are based on each of the theories?

In designing incentive systems, companies should be aware of the different aspects of motivation and behavior. Several theories of motivation and incentive stress different aspects of motivation and behavior. Three major theories are expectancy theory, goal-setting theory, and agency theory.

In designing incentive systems, companies should be aware of the different aspects of motivation and behavior. Several theories of motivation and incentive stress different aspects of motivation and behavior. Three major theories are expectancy theory, goal-setting theory, and agency theory.

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

80

Prepare a brief report on the Balanced Scorecard with particular emphasis on the following aspects:

● What are leading and lagging indicators?

● Why are leading indicators important?

● What is the relationship between leading and lagging indicators (cause-effect relationships)?

● What are the different dimensions of the Balanced Scorecard?

● What are some examples of indicators pertaining to the different dimensions of the Scorecard? David Palmer, manager of the Paper Products Division of a Graham Corporation, is a strong believer of outcome measures. During one of his management meetings, he impressed upon his management team that financial measures are the most important, and that his managers should only focus on improving those measures.

Nina Meyers, a recent CMA who was at the meeting filling in for her superior, was not too impressed with Palmer's exclusive focus on financial measures. As the meeting was about to end, she nervously pointed out to Palmer that his focus on outcome measures could be detrimental to the performance of the company.

Meyers: Excuse me, Mr. Palmer, but I think it is wrong to place exclusive emphasis on financial outcome measures. Instead, the emphasis must be on what are known as lead indicators, which provide information about the likely outcome of managerial decisions.

Palmer: I commend you for your knowledge on recent developments. However, I have more than 20 years' experience in this field and I think I know what I am doing. After all, ultimately financial results are what we want.

Meyers: I do not dispute that the ultimate result may largely be the financial returns to our shareholders. However, unless we pay attention to the drivers of the results, we will not understand the problems that exist in our processes. I can bring you up to date on a new performance measurement system known as the Balanced Scorecard if you like.

Although Palmer was not too impressed at being challenged, he instructed Meyers to write him a report on the Balanced Scorecard.

Required:

● What are leading and lagging indicators?

● Why are leading indicators important?

● What is the relationship between leading and lagging indicators (cause-effect relationships)?

● What are the different dimensions of the Balanced Scorecard?

● What are some examples of indicators pertaining to the different dimensions of the Scorecard? David Palmer, manager of the Paper Products Division of a Graham Corporation, is a strong believer of outcome measures. During one of his management meetings, he impressed upon his management team that financial measures are the most important, and that his managers should only focus on improving those measures.

Nina Meyers, a recent CMA who was at the meeting filling in for her superior, was not too impressed with Palmer's exclusive focus on financial measures. As the meeting was about to end, she nervously pointed out to Palmer that his focus on outcome measures could be detrimental to the performance of the company.

Meyers: Excuse me, Mr. Palmer, but I think it is wrong to place exclusive emphasis on financial outcome measures. Instead, the emphasis must be on what are known as lead indicators, which provide information about the likely outcome of managerial decisions.

Palmer: I commend you for your knowledge on recent developments. However, I have more than 20 years' experience in this field and I think I know what I am doing. After all, ultimately financial results are what we want.

Meyers: I do not dispute that the ultimate result may largely be the financial returns to our shareholders. However, unless we pay attention to the drivers of the results, we will not understand the problems that exist in our processes. I can bring you up to date on a new performance measurement system known as the Balanced Scorecard if you like.

Although Palmer was not too impressed at being challenged, he instructed Meyers to write him a report on the Balanced Scorecard.

Required:

Unlock Deck

Unlock for access to all 81 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 81 flashcards in this deck.