Exam 20: Performance Measurement Systems Glossary Photo Credits

Exam 1: Cost Management and Strategic Decision Making Evaluating Opportunities and Leading Change75 Questions

Exam 2: Product Costing Systems: Concepts and Design Issues117 Questions

Exam 3: Cost Accumulation for Job-Shop and Batch Production Operations90 Questions

Exam 4: Activity-Based Costing Systems102 Questions

Exam 5: Activity-Based Management89 Questions

Exam 6: Managing Customer Profitability73 Questions

Exam 7: Managing Quality and Time to Create Value114 Questions

Exam 8: Process-Costing Systems110 Questions

Exam 9: Joint-Process Costing90 Questions

Exam 10: Managing and Allocating Support-Service Costs80 Questions

Exam 11: Cost Estimation90 Questions

Exam 12: Financial and Cost-Volume-Profit Models69 Questions

Exam 13: Cost Management and Decision Making70 Questions

Exam 14: Strategic Issues in Making Long-Term Capital Investment Decisions97 Questions

Exam 15: Budgeting and Financial Planning81 Questions

Exam 16: Standard Costing, Variance Analysis, and Kaizen Costing80 Questions

Exam 17: Flexible Budgets, Overhead Cost Management, and Activity-Based Budgeting97 Questions

Exam 18: Organizational Design, Responsibility Accounting, and Evaluation of Divisional Performance80 Questions

Exam 19: Transfer Pricing76 Questions

Exam 20: Performance Measurement Systems Glossary Photo Credits81 Questions

Select questions type

Stock appreciation rights (SARs) confer bonuses to employees based on increases in stock prices for a predetermined number of shares.

Free

(True/False)

4.8/5  (38)

(38)

Correct Answer: Verified

Verified

True

The greatest benefit of using a balanced scorecard is that company profits always improve.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

False

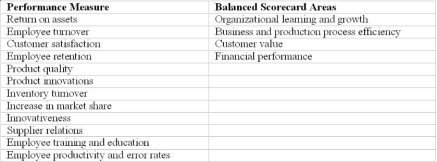

Match each of the following performance measures to one or more of the four areas of a balanced scorecard. Note that a performance measure can relate to more than one area.

Free

(Essay)

4.9/5 (37)

Correct Answer:Verified

Assume the role of a consultant preparing a report for MTI. Discuss the following aspects in your report: The internal value-chain of MTI

The balanced scorecard. Identify the goals of the company under each perspective of the scorecard and cause-effect relationships, and develop potential measures that could be used

How the inter-departmental differences can be eliminated

Sam Mahoney, the CEO of Mahoney Technologies, Inc. (MTI), a biotechnology firm had recently returned from a conference on modern cost management and performance measurement methods where he was exposed to target costing, value-chain analysis, balanced scorecard, activity-based management and other ideas.

MTI is a five-year old company operating in a growing, but competitive market. It develops and produces a number of different enzymes for use by research scientists and pharmaceutical companies. Its main competitors are also small to medium sized firms just like MTI. The key to growth in this industry is the ability to develop new products in a short time. Gail Stevenson, the vice-president (VP) for research & development (R&D) has noticed that some of MTI's new developments did not perform well because of the delays in their introduction into the market. Stevenson is very keen on hiring the best scientists and ensuring that they stay current in their fields because knowledge is the key competitive weapon in the biotechnology industry.

Bob Phillips, the controller of MTI had another concern. He has been noticing that the new products were not only delayed but their actual development costs were usually higher than budgeted. One of his goals was to see that the new products were profitable for the company.

Linda Joseph, the production manager, had a different concern of her own. Based on her observation, the production of the new enzymes was taking longer. Her feeling was that the products spent too much time in the quality control (QC) department. Barry Laker, the manager of the QC department argued that the new enzymes lacked the rigorous specifications that are demanded in the marketplace. Consequently, the QC department has had to perform additional tests to get to the root cause of the problems.

Mahoney had heard complaints from all quarters, and decided to convene a meeting of all the department heads.

Mahoney: Good afternoon, everyone. I am troubled that despite hiring a number of talented scientists, we are unable to compete effectively in the marketplace. Many of the recent entrants in the game seem to be beating us easily.

Stevenson: Sam, the key to our growth is rapid introduction of new products. Although my scientists are developing new enzymes in record times, they seem to be getting held up in manufacturing and especially the QC department.

Laker: Sam, I think I can pinpoint the root cause of the problem. I agree that our scientists are developing new enzymes in record times, but they do not seem to be paying any attention to standards. It looks like my department will have to provide training to them regarding quality control matters.

Stevenson: With due respect, I do not think there is more to know about QC standards. It looks like the department wants more attention and is therefore creating all this unnecessary fuss.

Joseph: I think I will agree with Barry that there are problems at the R&D side. My production scientists are also complaining that adequate specifications have not been developed; they have to constantly phone their R&D counterparts for clarifications.

Stevenson: I do not believe that the production problems can be attributed to R&D) I have personally screened each and every scientist during the hiring process.

Phillips: I don't think we will make much progress as a company if we keep pointing fingers at one another. We all must realize that all problems, regardless of their origin, finally affect the bottom-line of our company. Unless we set aside our differences and work together as a team, we will be unable to compete with our rivals. Some of our competitors follow best practices, which we must try to emulate. Mahoney: I agree with Bob. We must all look for solutions. I recently attended a conference where noted speakers talked about the value-chain of a company, interrelationships between functions, and the balanced scorecard. In fact, some speakers suggested that companies must stop discussing in terms of individual functions or departments; instead they must talk in terms of processes and understand linkages among all the processes that exist in an organization. I believe there are a number of ideas that we could adopt. I will leave the conference proceedings in the library, and suggest that we all read about these different topics. How about getting together after six weeks and discussing a plan of action? Thank you and see you all after six weeks.

Required

(Essay)

4.7/5 (37)

Market share is usually measured by the percentage of a company's customers over the total potential customers.

(True/False)

4.9/5 (35)

The primary purpose of the balanced scorecard should be as a management tool for employee incentives and financial rewards.

(True/False)

5.0/5 (47)

Most observers believe that a top-down management approach is the most successful way to implement a balanced scorecard.

(True/False)

5.0/5 (32)

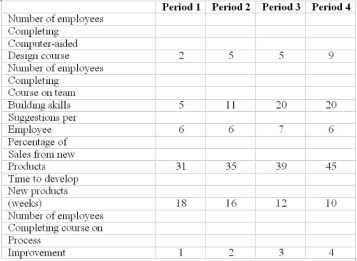

Aries Corporation places great importance on organizational learning to enhance the skills and capabilities of its employees. Ming Tsai, the Human Resources Manager of Aries, encourages all employees to acquire relevant skills and knowledge by attending evening courses in the local community college and special training sessions arranged in-house.

Tsai tracked the following data for the last four periods:

Required:

(a) From the above list of indicators, identify the leading and lagging indicators and indicate the cause-effect relationships.

(b) Comment on the trends present in the above indicators of organizational learning and growth. Do you believe that organizational capabilities are improving?

Required:

(a) From the above list of indicators, identify the leading and lagging indicators and indicate the cause-effect relationships.

(b) Comment on the trends present in the above indicators of organizational learning and growth. Do you believe that organizational capabilities are improving?

(Essay)

4.8/5 (35)

Briefly explain the underlying principle behind each of the theories of motivation and behavior. What specific aspects are built into incentive plans that are based on each of the theories?

In designing incentive systems, companies should be aware of the different aspects of motivation and behavior. Several theories of motivation and incentive stress different aspects of motivation and behavior. Three major theories are expectancy theory, goal-setting theory, and agency theory.

(Essay)

4.7/5 (47)

Absolute performance evaluation compares an individual's performance to that of others.

(True/False)

4.7/5 (33)

Customer value reflects the degree to which products and services satisfy customers' expectations about the price, function and quality of those products and services.

(True/False)

4.7/5 (28)

Which of the following would be a balanced scorecard measurement of customer value?

(Multiple Choice)

4.9/5 (36)

Which of the following statements is True regarding balanced scorecard-based incentive systems?

(Multiple Choice)

4.9/5 (33)

Critical success factors are important key performance indicators in a corporation.

(True/False)

4.8/5 (32)

When using a balanced scorecard approach, it is not possible to quantify the benefit received from employee training.

(True/False)

4.8/5 (37)

Which of the following statements regarding balanced scorecards isFalse?

(Multiple Choice)

4.9/5 (32)

Employee productivity can be measured in either physical measures or financial measures.

(True/False)

4.9/5 (40)

The balanced scorecard is a causal model of leading and lagging indicators of performance.

(True/False)

4.7/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)