Deck 13: Foreign Exchange Risk

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

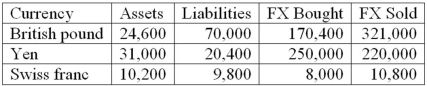

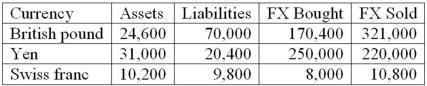

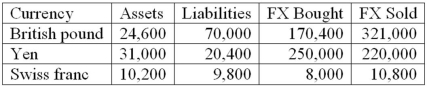

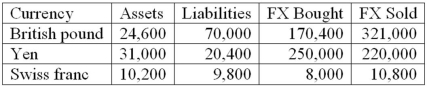

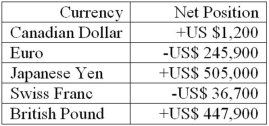

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  What is the FI's net exposure in the Swiss franc?

What is the FI's net exposure in the Swiss franc?

A)+2,400.

B)+400.

C)-2,800.

D)-2,400.

E)+3,200.

What is the FI's net exposure in the Swiss franc?A)+2,400.

B)+400.

C)-2,800.

D)-2,400.

E)+3,200.

Question

Question

Question

Question

Question

Question

Question

Question

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  What is the FI's net exposure in the Japanese yen?

What is the FI's net exposure in the Japanese yen?

A)+30,000.

B)+40,600.

C)-19,400.

D)-40,600.

E)+20,600.

What is the FI's net exposure in the Japanese yen?A)+30,000.

B)+40,600.

C)-19,400.

D)-40,600.

E)+20,600.

Question

Question

Question

Question

Question

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?

A)The FI is net short in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

B)The FI is net short in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

C)The FI is net long in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

D)The FI is net long in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

E)The FI has a balanced position in the British pound.

How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?A)The FI is net short in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

B)The FI is net short in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

C)The FI is net long in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

D)The FI is net long in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

E)The FI has a balanced position in the British pound.

Question

Question

Question

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  What is the FI's net exposure in British pounds?

What is the FI's net exposure in British pounds?

A)-45,400.

B)-150,600.

C)-196,000.

D)+105,200.

E)+196,000.

What is the FI's net exposure in British pounds?A)-45,400.

B)-150,600.

C)-196,000.

D)+105,200.

E)+196,000.

Question

Question

Question

Question

Question

Question

Question

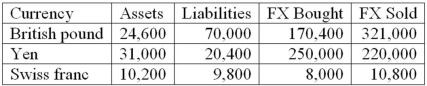

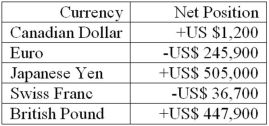

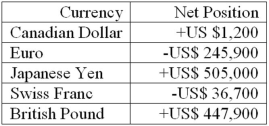

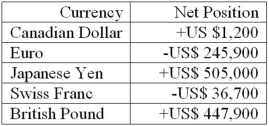

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms.  What is the FI's total FX investment?

What is the FI's total FX investment?

A)US$671,500.

B)US$1,236,700.

C)-US$671,500.

D)-US$1,236,700.

E)0

What is the FI's total FX investment?A)US$671,500.

B)US$1,236,700.

C)-US$671,500.

D)-US$1,236,700.

E)0

Question

Question

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?

A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

Question

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms.  How would you characterize the FI's risk exposure to fluctuations in the Euro to dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the Euro to dollar exchange rate?

A)The FI is net short in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

B)The FI is net short in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

C)The FI is net long in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

D)The FI is net long in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Euro.

How would you characterize the FI's risk exposure to fluctuations in the Euro to dollar exchange rate?A)The FI is net short in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

B)The FI is net short in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

C)The FI is net long in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

D)The FI is net long in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Euro.

Question

Question

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?

A)The FI is net short in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

B)The FI is net short in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

C)The FI is net long in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

D)The FI is net long in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Swiss franc.

How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?A)The FI is net short in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

B)The FI is net short in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

C)The FI is net long in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

D)The FI is net long in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Swiss franc.

Question

Question

Question

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms.  How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?

A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

Question

Question

Question

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms.  What is the portfolio weight of the Euro in this FI's portfolio of foreign currency?

What is the portfolio weight of the Euro in this FI's portfolio of foreign currency?

A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

What is the portfolio weight of the Euro in this FI's portfolio of foreign currency?A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

Question

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms.  What is the portfolio weight of the Japanese yen in this FI's portfolio of foreign currency?

What is the portfolio weight of the Japanese yen in this FI's portfolio of foreign currency?

A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

What is the portfolio weight of the Japanese yen in this FI's portfolio of foreign currency?A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/87

Play

Full screen (f)

Deck 13: Foreign Exchange Risk

1

Forward contracts in FX are typically written for periods exceeding 6 months.

False

2

To a Canadian trader of foreign currencies, a direct quote indicates Canadian dollars received for each one unit of the foreign currency.

True

3

FX trading income is derived only from profit (or loss) on the FI's speculative currency positions.

False

4

A positive net exposure position in FX implies the FI is net short in a currency.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

5

A positive net exposure position in FX implies an FI has purchased more foreign currency than it has sold.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

6

As the Canadian dollar appreciates against the Japanese yen, Japanese goods sold in Canada become less expensive to the Canadian consumer.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

7

The spot foreign exchange market is where forward and futures contracts and swap agreements are transacted.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

8

The underlying cause of foreign exchange volatility reflects fluctuations in the demand and supply of a country's currency.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

9

Average daily turnover in the FX market has recently been over $4 trillion.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

10

The FX markets of the world have become one of the largest of all financial markets.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

11

Most profits or losses on foreign trading come from taking an open position in currencies.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

12

Most nonbank FIs have foreign exchange risk exposure that is smaller than the exposure of the large Canadian banks.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

13

The foreign exchange market in Tokyo is the largest FX trading market.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

14

An FI can eliminate its currency risk exposure by matching its foreign currency assets to its foreign currency liabilities.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

15

As the Canadian dollar appreciates against the Japanese yen, Canadian goods become less expensive to Japanese consumers.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

16

FX trading risk exposure continues into the night until all FI operations are closed.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

17

The greater the volatility of foreign exchange rates given any net exposure position, the greater the fluctuations in value of the foreign exchange portfolio.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

18

The exposure to foreign exchange risk by Canadian FIs has decreased with the growth of the various derivative markets.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

19

The market in which foreign currency is traded for future delivery is the forward foreign exchange market.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

20

Canadian pension funds invest approximately one percent (1%) of their portfolios in foreign securities.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

21

The reason an FI receives a fee when purchasing foreign currencies to allow customers to complete international transactions is because the FI assumes some FX risk.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

22

Directly matching foreign asset and liability books in the same FX currency will allow an FI to hedge or lock in a profit spread regardless of future changes in exchange rates.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

23

A positive net exposure position in FX implies that the FI is

A)net long in a currency and exposed to depreciation of the foreign currency.

B)net short in a currency and exposed to depreciation of the foreign currency.

C)net long in a currency and exposed to appreciation of the foreign currency.

D)net short in a currency and exposed to appreciation of the foreign currency.

E)neither long nor short in a currency.

A)net long in a currency and exposed to depreciation of the foreign currency.

B)net short in a currency and exposed to depreciation of the foreign currency.

C)net long in a currency and exposed to appreciation of the foreign currency.

D)net short in a currency and exposed to appreciation of the foreign currency.

E)neither long nor short in a currency.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

24

Off-balance-sheet hedging involves taking a position in FX forward or other derivative securities even though no FX assets or liabilities are on the balance sheet.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

25

An FI can control its FX risk exposure by on-balance-sheet and off-balance-sheet hedging.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

26

Profits in foreign exchange trading have grown despite the decreased volatility in FX rates in European countries.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

27

On-balance-sheet hedging involves making changes in the on-balance-sheet assets and liabilities to protect FI profits from FX risk without the use of derivative securities.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

28

The market in which foreign currency is traded for immediate delivery is the

A)spot market.

B)forward market.

C)futures market.

D)currency swap market.

E)London capital market.

A)spot market.

B)forward market.

C)futures market.

D)currency swap market.

E)London capital market.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

29

The FI is acting as a FX market agent for its customers when it

A)buys or sells currency to balance the FI's net exposure.

B)takes a nonzero net position in a particular currency.

C)processes an exporter's transaction in a foreign currency.

D)makes a market in its domestic currency.

E)advises customers on their international business.

A)buys or sells currency to balance the FI's net exposure.

B)takes a nonzero net position in a particular currency.

C)processes an exporter's transaction in a foreign currency.

D)makes a market in its domestic currency.

E)advises customers on their international business.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

30

A negative net exposure position in FX implies that the FI is

A)net long in a currency and exposed to depreciation of the foreign currency.

B)net short in a currency and exposed to depreciation of the foreign currency.

C)net long in a currency and exposed to appreciation of the foreign currency.

D)net short in a currency and exposed to appreciation of the foreign currency.

E)neither long nor short in a currency.

A)net long in a currency and exposed to depreciation of the foreign currency.

B)net short in a currency and exposed to depreciation of the foreign currency.

C)net long in a currency and exposed to appreciation of the foreign currency.

D)net short in a currency and exposed to appreciation of the foreign currency.

E)neither long nor short in a currency.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

31

Violation of the interest rate parity theorem would allow arbitrage profits.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

32

The real interest rate reflects the underlying real sector demand and supply for funds denominated in the domestic currency.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

33

The use of an exchange rate forward contract assures the FI of the opportunity to buy (or sell) the foreign currency at a future time at a known price.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is NOT a source of foreign exchange risk?

A)Trading foreign currencies.

B)Making domestic-currency loans to foreign corporations.

C)Buying foreign-issued securities.

D)Issuing foreign currency-denominated debt.

E)Making foreign currency loans.

A)Trading foreign currencies.

B)Making domestic-currency loans to foreign corporations.

C)Buying foreign-issued securities.

D)Issuing foreign currency-denominated debt.

E)Making foreign currency loans.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

35

During the late 2000's financial crisis, global stock market return correlations decreased relative to the decade before the crisis.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

36

The total FX risk for a domestic bank that is making a one-year loan in a foreign currency is that the interest income expected on the loan is exposed to a depreciation of the foreign currency.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

37

Long-term violations of the interest rate parity relationship may occur if imperfections in the international financial markets are allowed to exist.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

38

Interest rate parity implies that the discounted spread between interest rates in two currencies should equal the percentage spread between forward and spot exchange rates.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

39

The FI is acting as a hedger when it

A)buys or sells currency to balance the FI's net exposure.

B)takes a nonzero net position in a particular currency.

C)processes an exporter's transaction in a foreign currency.

D)makes a market in a currency.

E)advises customers on their international business.

A)buys or sells currency to balance the FI's net exposure.

B)takes a nonzero net position in a particular currency.

C)processes an exporter's transaction in a foreign currency.

D)makes a market in a currency.

E)advises customers on their international business.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

40

Purchasing power parity is based on the difference in productive output (GDP) that exists between two countries.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

41

When purchasing and selling foreign currencies to allow customers to take positions in foreign real and financial investments, the FI

A)acts defensively as a hedger.

B)acts aggressively as a speculator.

C)assumes the FX risk itself.

D)acts as an agent.

E)acts as a market maker.

A)acts defensively as a hedger.

B)acts aggressively as a speculator.

C)assumes the FX risk itself.

D)acts as an agent.

E)acts as a market maker.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

42

The FI is acting as a speculator when it

A)buys or sells currency to balance the FI's net exposure.

B)takes a nonzero net position in a particular currency.

C)processes an exporter's transaction in a foreign currency.

D)makes a market in a currency.

E)advises customers on their international business.

A)buys or sells currency to balance the FI's net exposure.

B)takes a nonzero net position in a particular currency.

C)processes an exporter's transaction in a foreign currency.

D)makes a market in a currency.

E)advises customers on their international business.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

43

The decline in European FX volatility during the last decade has been offset in part by

A)the greater volatilities of Asian currencies.

B)a reduction in inflation rates in European countries.

C)the fixing of exchange rates among European countries.

D)the replacement of domestic currencies with the euro.

E)All of these.

A)the greater volatilities of Asian currencies.

B)a reduction in inflation rates in European countries.

C)the fixing of exchange rates among European countries.

D)the replacement of domestic currencies with the euro.

E)All of these.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

44

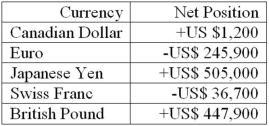

The following are the net currency positions of a Canadian FI (stated in Canadian dollars). What is the FI's net exposure in the Swiss franc?

A)+2,400.

B)+400.

C)-2,800.

D)-2,400.

E)+3,200.

What is the FI's net exposure in the Swiss franc?A)+2,400.

B)+400.

C)-2,800.

D)-2,400.

E)+3,200.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

45

According to purchasing power parity (PPP), foreign currency exchange rates between two countries adjust to reflect changes in each country's

A)unemployment rates.

B)export competitiveness.

C)inflation rates.

D)foreign exchange reserves.

E)reserve requirements.

A)unemployment rates.

B)export competitiveness.

C)inflation rates.

D)foreign exchange reserves.

E)reserve requirements.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

46

If foreign currency exchange rates are highly positively correlated, how can a FI reduce its exchange rate risk exposure?

A)By taking net long positions in all currencies.

B)By taking net short positions in all currencies.

C)By taking opposing net short and net long positions in different currencies.

D)By maximizing net FX exposure in each currency, independently.

E)By minimizing net FX exposure in each currency, independently.

A)By taking net long positions in all currencies.

B)By taking net short positions in all currencies.

C)By taking opposing net short and net long positions in different currencies.

D)By maximizing net FX exposure in each currency, independently.

E)By minimizing net FX exposure in each currency, independently.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

47

Most profits or losses on foreign trading for FIs come from

A)open positions or speculation.

B)market making.

C)acting as agents for retail customers.

D)acting as agents for wholesale customers.

E)hedging activities.

A)open positions or speculation.

B)market making.

C)acting as agents for retail customers.

D)acting as agents for wholesale customers.

E)hedging activities.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is an example of interest rate parity?

A)The Japanese yen trades at the same exchange rate as the Swiss franc.

B)U.S. dollar rates on one year U.S. Treasury securities equal 1 year Japanese government bond rates.

C)U.S. dollar rates on one year U.S. Treasury securities equal 1 year Japanese government bond rates, restated in dollars.

D)British pound 2 year forward rates equal 2 year Swiss franc forward rates.

E)All currency exchange rates and interest rates move in unison.

A)The Japanese yen trades at the same exchange rate as the Swiss franc.

B)U.S. dollar rates on one year U.S. Treasury securities equal 1 year Japanese government bond rates.

C)U.S. dollar rates on one year U.S. Treasury securities equal 1 year Japanese government bond rates, restated in dollars.

D)British pound 2 year forward rates equal 2 year Swiss franc forward rates.

E)All currency exchange rates and interest rates move in unison.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

49

In which of the following FX trading activities does the FI not assume FX risk?

A)The purchase and sale of foreign currencies for the purpose of profiting from forecasting or anticipating future movements in FX rates.

B)The purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions.

C)The purchase and sale of foreign currencies for the purpose of offsetting customer exposure in any given currency.

D)The purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

E)In both the purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions, and the purchase and sale of foreign currencies to allow customers to take positions in foreign and real and financial investments.

A)The purchase and sale of foreign currencies for the purpose of profiting from forecasting or anticipating future movements in FX rates.

B)The purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions.

C)The purchase and sale of foreign currencies for the purpose of offsetting customer exposure in any given currency.

D)The purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

E)In both the purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions, and the purchase and sale of foreign currencies to allow customers to take positions in foreign and real and financial investments.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

50

Deviations from the international currency parity relationships may occur because of

A)free capital movements across national boundaries.

B)barriers to cross-border financial flows.

C)perfect rationality of market participants.

D)differences in each country's productive capacity.

E)Basel capital regulations.

A)free capital movements across national boundaries.

B)barriers to cross-border financial flows.

C)perfect rationality of market participants.

D)differences in each country's productive capacity.

E)Basel capital regulations.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

51

As of 2012, which of the following FX "markets" is the largest?

A)London.

B)New York.

C)Tokyo.

D)Hong Kong.

E)Zurich.

A)London.

B)New York.

C)Tokyo.

D)Hong Kong.

E)Zurich.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

52

The following are the net currency positions of a Canadian FI (stated in Canadian dollars). What is the FI's net exposure in the Japanese yen?

A)+30,000.

B)+40,600.

C)-19,400.

D)-40,600.

E)+20,600.

What is the FI's net exposure in the Japanese yen?A)+30,000.

B)+40,600.

C)-19,400.

D)-40,600.

E)+20,600.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

53

The nominal interest rate is equal to the

A)real interest rate minus the inflation premium.

B)real interest rate minus the trailing inflation rate.

C)real interest rate plus the expected interest rate increase.

D)real interest rate plus the expected inflation rate.

E)real interest rate plus the interest rate volatility.

A)real interest rate minus the inflation premium.

B)real interest rate minus the trailing inflation rate.

C)real interest rate plus the expected interest rate increase.

D)real interest rate plus the expected inflation rate.

E)real interest rate plus the interest rate volatility.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following factors help explain the decline in FX trading in the early years of this century?

A)Introduction of the euro.

B)Consolidation in the banking industry.

C)Growth of electronic brokering.

D)Mergers in the corporate sector.

E)All of these.

A)Introduction of the euro.

B)Consolidation in the banking industry.

C)Growth of electronic brokering.

D)Mergers in the corporate sector.

E)All of these.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following FX trading activities is used to hedge FX risk?

A)The purchase and sale of foreign currencies for the purpose of profiting from forecasting or anticipating future movements in FX rates.

B)The purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions.

C)The purchase and sale of foreign currencies for the purpose of offsetting customer exposure in any given currency.

D)The purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

E)None of these.

A)The purchase and sale of foreign currencies for the purpose of profiting from forecasting or anticipating future movements in FX rates.

B)The purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions.

C)The purchase and sale of foreign currencies for the purpose of offsetting customer exposure in any given currency.

D)The purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

E)None of these.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

56

The decrease in European FX volatility during the last decade has occurred because of

A)the stabilizing force of the euro.

B)reduction in inflation rates in European countries.

C)the reduced volatility in many emerging-market countries.

D)the greater volatilities of Asian currencies.

E)the stabilizing force of the euro, and reduction in inflation rates in European countries.

A)the stabilizing force of the euro.

B)reduction in inflation rates in European countries.

C)the reduced volatility in many emerging-market countries.

D)the greater volatilities of Asian currencies.

E)the stabilizing force of the euro, and reduction in inflation rates in European countries.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

57

The following are the net currency positions of a Canadian FI (stated in Canadian dollars). How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?

A)The FI is net short in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

B)The FI is net short in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

C)The FI is net long in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

D)The FI is net long in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

E)The FI has a balanced position in the British pound.

How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?A)The FI is net short in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

B)The FI is net short in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

C)The FI is net long in the British pound and therefore faces the risk that the British pound will fall in value against the U.S. dollar.

D)The FI is net long in the British pound and therefore faces the risk that the British pound will rise in value against the U.S. dollar.

E)The FI has a balanced position in the British pound.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following FX trading activities is used for purposes of speculation?

A)The purchase and sale of foreign currencies for the purpose of profiting from forecasting or anticipating future movements in FX rates.

B)The purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions.

C)The purchase and sale of foreign currencies for the purpose of offsetting customer exposure in any given currency.

D)The purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

E)None of these.

A)The purchase and sale of foreign currencies for the purpose of profiting from forecasting or anticipating future movements in FX rates.

B)The purchase and sale of foreign currencies to allow customers to partake in and complete international commercial trade transactions.

C)The purchase and sale of foreign currencies for the purpose of offsetting customer exposure in any given currency.

D)The purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

E)None of these.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

59

FX risk exposure of an FI essentially relates to which of the following activities?

A)Purchase and sale of foreign currencies to allow customers to participate in and complete international commercial trade transactions.

B)Purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

C)Purchase and sale of foreign currencies for hedging purposes to offset customer exposure in any given currency.

D)Purchase and sale of foreign currencies for speculative purposes through forecasting or anticipating future movements in FX rates.

E)None of these.

A)Purchase and sale of foreign currencies to allow customers to participate in and complete international commercial trade transactions.

B)Purchase and sale of foreign currencies to allow customers to take positions in foreign real and financial investments.

C)Purchase and sale of foreign currencies for hedging purposes to offset customer exposure in any given currency.

D)Purchase and sale of foreign currencies for speculative purposes through forecasting or anticipating future movements in FX rates.

E)None of these.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

60

The following are the net currency positions of a Canadian FI (stated in Canadian dollars). What is the FI's net exposure in British pounds?

A)-45,400.

B)-150,600.

C)-196,000.

D)+105,200.

E)+196,000.

What is the FI's net exposure in British pounds?A)-45,400.

B)-150,600.

C)-196,000.

D)+105,200.

E)+196,000.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

61

The one-year CD rates for financial institutions with AA ratings are 5 percent in Canada and 8 percent in France. An AA-rated Canadian financial institution can borrow by issuing GICs or lend by purchasing GICs at these rates in either market. The current spot rate is $0.20/Euro. If the bank receives a quote of $0.1975/€ for one-year forward rates for the Euro (to buy and to sell), what is the arbitrage profit for the bank if it uses $1,000,000 as the notional amount?

A)$5,000.

B)$16,500.

C)$19,350.

D)$22,000.

E)$25,675.

A)$5,000.

B)$16,500.

C)$19,350.

D)$22,000.

E)$25,675.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

62

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. If in one year there is no change to either interest rates or exchange rates, what is the end-of-year profit or loss for the bank? (Hint: Annual interest is paid on both the Canadian bonds and the CD on the date of liquidation in exactly one year.)

A)Profit of US$20,000.

B)Loss of C$224,000.

C)Profit of US$50,000.

D)Profit of C$63,700.

E)Profit of US$313,000.

A)Profit of US$20,000.

B)Loss of C$224,000.

C)Profit of US$50,000.

D)Profit of C$63,700.

E)Profit of US$313,000.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

63

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. What is the end-of-year profit or loss to the bank if in one year Canadian bond rates increase to 7.538 percent? (Assume no change in either current U.S. interest rates or current exchange rates, US$0.78493/C$1.)

A)Loss of US$5,000.

B)Profit of US$15,000.

C)Loss of C$119,000.

D)Profit of C$50,000.

E)Loss of C$50,000.

A)Loss of US$5,000.

B)Profit of US$15,000.

C)Loss of C$119,000.

D)Profit of C$50,000.

E)Loss of C$50,000.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

64

An FI has purchased (borrowed) a one-year $10 million Eurodollar deposit at an annual interest rate of 6 percent. It has invested these proceeds in one-year Euro (€) bonds at an annual rate of 6.5 percent after converting them at the current spot rate of €1.75/$. Both interest and principal are paid at the end of the year. What is the spread earned by the bank if the end-of-year exchange rate is €1.77/$?

A)-1.00 percent.

B)-0.70 percent.

C)-0.25 percent.

D)0.00 percent.

E)0.20 percent.

A)-1.00 percent.

B)-0.70 percent.

C)-0.25 percent.

D)0.00 percent.

E)0.20 percent.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

65

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. If you wanted to hedge your bank's risk exposure, what hedge position would you take?

A)A short interest rate hedge to protect against interest rate declines and a short currency hedge to protect against increases in the value of the Canadian dollar with respect to the U.S. dollar.

B)A short interest rate hedge to protect against interest rate increases and a short currency hedge to protect against declines in the value of the Canadian dollar with respect to the U.S. dollar.

C)A long interest rate hedge to protect against interest rate increases and a long currency hedge to protect against declines in the value of the Canadian dollar with respect to the U.S. dollar.

D)A long interest rate hedge to protect against interest rate declines and a long currency hedge to protect against increases in the value of the Canadian dollar with respect to the U.S. dollar.

E)A long interest rate hedge to protect against interest rate declines and a short currency hedge to protect against increases in the value of the Canadian dollar with respect to the U.S. dollar.

A)A short interest rate hedge to protect against interest rate declines and a short currency hedge to protect against increases in the value of the Canadian dollar with respect to the U.S. dollar.

B)A short interest rate hedge to protect against interest rate increases and a short currency hedge to protect against declines in the value of the Canadian dollar with respect to the U.S. dollar.

C)A long interest rate hedge to protect against interest rate increases and a long currency hedge to protect against declines in the value of the Canadian dollar with respect to the U.S. dollar.

D)A long interest rate hedge to protect against interest rate declines and a long currency hedge to protect against increases in the value of the Canadian dollar with respect to the U.S. dollar.

E)A long interest rate hedge to protect against interest rate declines and a short currency hedge to protect against increases in the value of the Canadian dollar with respect to the U.S. dollar.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

66

Suppose that the current spot exchange rate of Canadian dollars for Russian rubles is $0.15/1ruble. The price of Russian-produced goods increases by 8 percent, and the Canadian price index increases by 3 percent. According to PPP, the 8 percent rise in the price of Russian goods relative to the 3 percent rise in the price of Canadian goods results in a(n)

A)depreciation of the Russian ruble by 5 percent.

B)depreciation of the Russian ruble by 6 percent.

C)appreciation of the Russian ruble by 5 percent.

D)appreciation of the Russian ruble by 6 percent.

E)depreciation of the Russian ruble by 7 percent.

A)depreciation of the Russian ruble by 5 percent.

B)depreciation of the Russian ruble by 6 percent.

C)appreciation of the Russian ruble by 5 percent.

D)appreciation of the Russian ruble by 6 percent.

E)depreciation of the Russian ruble by 7 percent.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

67

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms. What is the FI's total FX investment?

A)US$671,500.

B)US$1,236,700.

C)-US$671,500.

D)-US$1,236,700.

E)0

What is the FI's total FX investment?A)US$671,500.

B)US$1,236,700.

C)-US$671,500.

D)-US$1,236,700.

E)0

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

68

Suppose that the current spot exchange rate of Canadian dollars for Russian rubles is $0.15/1ruble. The price of Russian-produced goods increases by 8 percent, and the Canadian price index increases by 3 percent. According to PPP, the new exchange rate of Russian rubles to dollars is

A)0.15.

B)0.1425.

C)0.141.

D)0.1605.

E)0.159.

A)0.15.

B)0.1425.

C)0.141.

D)0.1605.

E)0.159.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

69

The following are the net currency positions of a Canadian FI (stated in Canadian dollars). How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?

A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

70

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms. How would you characterize the FI's risk exposure to fluctuations in the Euro to dollar exchange rate?

A)The FI is net short in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

B)The FI is net short in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

C)The FI is net long in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

D)The FI is net long in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Euro.

How would you characterize the FI's risk exposure to fluctuations in the Euro to dollar exchange rate?A)The FI is net short in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

B)The FI is net short in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

C)The FI is net long in the Euro and therefore faces the risk that the Euro will fall in value against the U.S. dollar.

D)The FI is net long in the Euro and therefore faces the risk that the Euro will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Euro.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

71

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. What is the end-of-year profit or loss to the bank if in one year the exchange rate falls to US$0.765 per Canadian dollar? (Assume that there is no change in interest rates.)

A)Loss of US$75,000.

B)Profit of C$274,000.

C)Loss of US$7,000.

D)Profit of C$9,000.

E)Loss of US$5,000.

A)Loss of US$75,000.

B)Profit of C$274,000.

C)Loss of US$7,000.

D)Profit of C$9,000.

E)Loss of US$5,000.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

72

The following are the net currency positions of a Canadian FI (stated in Canadian dollars). How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?

A)The FI is net short in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

B)The FI is net short in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

C)The FI is net long in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

D)The FI is net long in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Swiss franc.

How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?A)The FI is net short in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

B)The FI is net short in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

C)The FI is net long in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

D)The FI is net long in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Swiss franc.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

73

The one-year CD rates for financial institutions with AA ratings are 5 percent in Canada and 8 percent in France. An AA-rated Canadian financial institution can borrow by issuing GICs or lend by purchasing GICs at these rates in either market. The current spot rate is $0.20/Euro. What should be the spot rate in order for no arbitrage to take place, assuming the one-year forward rate is $0.1975/€?

A)$0.1944/€.

B)$0.1975/€.

C)$0.2000/€.

D)$0.2025/€.

E)$0.2031/€.

A)$0.1944/€.

B)$0.1975/€.

C)$0.2000/€.

D)$0.2025/€.

E)$0.2031/€.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

74

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. What is the end of year profit or loss on the bank's cash position if in one year both Canadian bond rates increase to 7.538 percent and the exchange rate falls to US$0.765 per Canadian dollar? (Assume no change in U.S. interest rates.)

A)Loss of US$12,000.

B)Loss of US$75,000.

C)Profit of C$9,000.

D)Profit of US$50,000.

E)Loss of C$119,800.

A)Loss of US$12,000.

B)Loss of US$75,000.

C)Profit of C$9,000.

D)Profit of US$50,000.

E)Loss of C$119,800.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

75

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms. How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?

A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

How would you characterize the FI's risk exposure to fluctuations in the yen/dollar exchange rate?A)The FI is net short in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

B)The FI is net short in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

C)The FI is net long in the yen and therefore faces the risk that the yen will fall in value against the U.S. dollar.

D)The FI is net long in the yen and therefore faces the risk that the yen will rise in value against the U.S. dollar.

E)The FI has a balanced position in the Japanese yen.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

76

An FI has purchased (borrowed) a one-year $10 million Eurodollar deposit at an annual interest rate of 6 percent. It has invested these proceeds in one-year Euro (€) bonds at an annual rate of 6.5 percent after converting them at the current spot rate of €1.75/$. Both interest and principal are paid at the end of the year. What is the spread earned by the bank at the end of the year if the exchange rate remains at €1.75/$?

A)0.50 percent.

B)1.00 percent.

C)1.5 percent.

D)2.0 percent.

E)2.5 percent.

A)0.50 percent.

B)1.00 percent.

C)1.5 percent.

D)2.0 percent.

E)2.5 percent.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

77

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. Your position is exposed to

A)interest rate risk only.

B)credit risk only.

C)exchange rate risk only.

D)interest rate and exchange rate risk only.

E)interest rate risk, exchange rate risk, and credit risk.

A)interest rate risk only.

B)credit risk only.

C)exchange rate risk only.

D)interest rate and exchange rate risk only.

E)interest rate risk, exchange rate risk, and credit risk.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

78

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms. What is the portfolio weight of the Euro in this FI's portfolio of foreign currency?

A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

What is the portfolio weight of the Euro in this FI's portfolio of foreign currency?A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

79

The following are the net currency positions of a U.S. FI (stated in U.S. dollars). Note: Net currency positions are foreign exchange bought minus foreign exchange sold restated in U.S. dollar terms. What is the portfolio weight of the Japanese yen in this FI's portfolio of foreign currency?

A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

What is the portfolio weight of the Japanese yen in this FI's portfolio of foreign currency?A)+0.18 percent.

B)-36.62 percent.

C)+75.20 percent.

D)-5.47 percent.

E)+66.70 percent.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

80

The one-year CD rates for financial institutions with AA ratings are 5 percent in Canada and 8 percent in France. An AA-rated Canadian financial institution can borrow by issuing GICs or lend by purchasing GICs at these rates in either market. The current spot rate is $0.20/Euro. What should be the one-year forward rate in order to prevent any arbitrage?

A)$0.1944/€.

B)$0.1975/€.

C)$0.2000/€.

D)$0.2025/€.

E)$0.2031/€.

A)$0.1944/€.

B)$0.1975/€.

C)$0.2000/€.

D)$0.2025/€.

E)$0.2031/€.

Unlock Deck

Unlock for access to all 87 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 87 flashcards in this deck.