Exam 13: Foreign Exchange Risk

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. Your position is exposed to

Free

(Multiple Choice)

5.0/5  (34)

(34)

Correct Answer: Verified

Verified

E

An FI has purchased (borrowed) a one-year $10 million Eurodollar deposit at an annual interest rate of 6 percent. It has invested these proceeds in one-year Euro (€) bonds at an annual rate of 6.5 percent after converting them at the current spot rate of €1.75/$. Both interest and principal are paid at the end of the year. What is the spread earned if the bank can sell one-year forward Euros at €1.755/$?

Free

(Multiple Choice)

4.8/5 (24)

Correct Answer:Verified

D

An FI has purchased (borrowed) a one-year $10 million Eurodollar deposit at an annual interest rate of 6 percent. It has invested these proceeds in one-year Euro (€) bonds at an annual rate of 6.5 percent after converting them at the current spot rate of €1.75/$. Both interest and principal are paid at the end of the year. What is the spread earned by the bank if the end-of-year exchange rate is €1.77/$?

Free

(Multiple Choice)

4.8/5 (37)

Correct Answer:Verified

B

Purchasing power parity is based on the difference in productive output (GDP) that exists between two countries.

(True/False)

4.9/5 (32)

During the late 2000's financial crisis, global stock market return correlations decreased relative to the decade before the crisis.

(True/False)

4.9/5 (32)

Canadian pension funds invest approximately one percent (1%) of their portfolios in foreign securities.

(True/False)

4.7/5 (36)

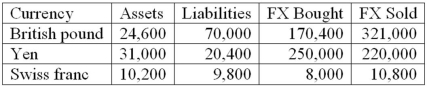

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  What is the FI's net exposure in British pounds?

What is the FI's net exposure in British pounds?

(Multiple Choice)

4.9/5 (38)

The exposure to foreign exchange risk by Canadian FIs has decreased with the growth of the various derivative markets.

(True/False)

4.8/5 (29)

Which of the following factors help explain the decline in FX trading in the early years of this century?

(Multiple Choice)

4.9/5 (36)

The market in which foreign currency is traded for immediate delivery is the

(Multiple Choice)

4.8/5 (34)

An FI can control its FX risk exposure by on-balance-sheet and off-balance-sheet hedging.

(True/False)

4.8/5 (32)

The real interest rate reflects the underlying real sector demand and supply for funds denominated in the domestic currency.

(True/False)

4.8/5 (37)

Which of the following FX trading activities is used for purposes of speculation?

(Multiple Choice)

4.9/5 (29)

As the Canadian dollar appreciates against the Japanese yen, Japanese goods sold in Canada become less expensive to the Canadian consumer.

(True/False)

4.9/5 (28)

Yen Bank wishes to invest in Yen loans at a rate of 10 percent. The bank will fund the loans in the domestic GIC market at a rate of 6.3 percent. This on-balance-sheet FX risk will be hedged in the spot market at a forward rate of $0.62/¥. The spot rate on yen is $0.60/¥. What must be the spot exchange rate to eliminate the preference for the yen loans if the forward rate remains $0.62/¥?

(Multiple Choice)

4.8/5 (28)

Your U.S. bank issues a one-year U.S. CD at 5 percent annual interest to finance a C$1.274 million (Canadian dollar) investment in two-year, fixed rate Canadian bonds selling at par and paying 7 percent annually. You expect to liquidate your position in one year. Currently, spot exchange rates are US$0.78493 per Canadian dollar. What is the end of year profit or loss on the bank's cash position if in one year both Canadian bond rates increase to 7.538 percent and the exchange rate falls to US$0.765 per Canadian dollar? (Assume no change in U.S. interest rates.)

(Multiple Choice)

4.8/5 (34)

In which of the following FX trading activities does the FI not assume FX risk?

(Multiple Choice)

5.0/5 (28)

To a Canadian trader of foreign currencies, a direct quote indicates Canadian dollars received for each one unit of the foreign currency.

(True/False)

5.0/5 (38)

Interest rate parity implies that the discounted spread between interest rates in two currencies should equal the percentage spread between forward and spot exchange rates.

(True/False)

4.8/5 (27)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)