Deck 7: Cost Allocation: Departments, Joint Products, and By-Products

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

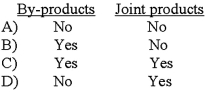

For the purposes of cost accumulation, which of the following are identifiable as different individual products before the split-off point?

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

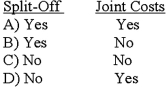

Relative sales value at split-off is used to allocate: Cost Beyond

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Question

Question

Question

Question

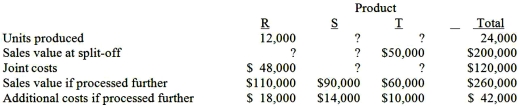

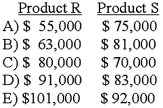

Johns Company manufactures products R, S, and T from a joint process.The following information is available:  Assuming that joint product costs are allocated using the relative-sales-value at split-off approach, what was the sales value at split-off for products R and S?

Assuming that joint product costs are allocated using the relative-sales-value at split-off approach, what was the sales value at split-off for products R and S?

A)Option A

B)Option B

C)Option C

D)Option D

Assuming that joint product costs are allocated using the relative-sales-value at split-off approach, what was the sales value at split-off for products R and S? A)Option A

B)Option B

C)Option C

D)Option D

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/96

Play

Full screen (f)

Deck 7: Cost Allocation: Departments, Joint Products, and By-Products

1

A key ethical issue in cost allocation involves costing in an international context, because the choice of a cost allocation method can affect:

A)Management reward systems.

B)Management fraud.

C)Taxes in domestic and foreign countries.

D)The firm's financial statements.

E)The fair share of cost by a governmental unit.

A)Management reward systems.

B)Management fraud.

C)Taxes in domestic and foreign countries.

D)The firm's financial statements.

E)The fair share of cost by a governmental unit.

C

2

The objectives of cost allocation are to:

A)Motivate, provide incentives, and determine fair rewards.

B)Accurately define, divide and spread direct costs.

C)Value, measure, and interpret cost data.

D)Connect, communicate, and discern information.

E)Define, refine, and re-define indirect costs.

A)Motivate, provide incentives, and determine fair rewards.

B)Accurately define, divide and spread direct costs.

C)Value, measure, and interpret cost data.

D)Connect, communicate, and discern information.

E)Define, refine, and re-define indirect costs.

A

3

The reciprocal method of departmental cost allocation is preferred over the step method because it takes into account all the reciprocal flows between:

A)The service departments.

B)The producing departments.

C)Multiple products.

D)Competing departments.

E)Similar, but separate, products.

A)The service departments.

B)The producing departments.

C)Multiple products.

D)Competing departments.

E)Similar, but separate, products.

A

4

Cost allocation provides a service firm a basis for evaluating the:

A)Cost and profitability of its services.

B)Value of its services.

C)Manufacturing costs for the company.

D)Profitability of its customers.

A)Cost and profitability of its services.

B)Value of its services.

C)Manufacturing costs for the company.

D)Profitability of its customers.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

5

By-product costing that uses the asset recognition method(s) creates:

A)Expense recognition in the current period.

B)A distortion of net income.

C)An adjustment on the income statement.

D)An inventory value in the period in which the by-products are produced.

E)A result that is not compatible with GAAP.

A)Expense recognition in the current period.

B)A distortion of net income.

C)An adjustment on the income statement.

D)An inventory value in the period in which the by-products are produced.

E)A result that is not compatible with GAAP.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

6

Which one of the following methods uses units of output to allocate joint costs to joint products?

A)Net realizable value method.

B)Physical units method.

C)Net sales value method.

D)Sales value at split-off method.

E)Activity-based costing.

A)Net realizable value method.

B)Physical units method.

C)Net sales value method.

D)Sales value at split-off method.

E)Activity-based costing.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

7

The direct method of departmental cost allocation ignores:

A)The managers' bias.

B)Accrual accounting.

C)Tax implications.

D)Long-term implications.

E)Reciprocal flows.

A)The managers' bias.

B)Accrual accounting.

C)Tax implications.

D)Long-term implications.

E)Reciprocal flows.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

8

An alternative concept of fairness in cost allocation, absent the cause-and-effect basis, includes:

A)Ability-to-bear.

B)Efficiency.

C)Different costs for different purposes.

D)Consistency.

A)Ability-to-bear.

B)Efficiency.

C)Different costs for different purposes.

D)Consistency.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

9

Cost allocation of shared facilities cost is intended to remind managers of:

A)The cost of using a shared resource.

B)Both the cost and value of using shared resources.

C)How much capacity a firm has.

D)Why the firm invests in these facilities.

E)How dependent the managers are for these facilities.

A)The cost of using a shared resource.

B)Both the cost and value of using shared resources.

C)How much capacity a firm has.

D)Why the firm invests in these facilities.

E)How dependent the managers are for these facilities.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

10

In making decisions about whether to sell or further process joint products, allocation of common or joint costs is:

A)Essential.

B)Useful.

C)Irrelevant.

D)Is useful depending on the method chosen.

E)Is the only way to get the true total product cost.

A)Essential.

B)Useful.

C)Irrelevant.

D)Is useful depending on the method chosen.

E)Is the only way to get the true total product cost.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

11

An overhead cost that can be traced directly to either a service or production department:

A)Is called a "flow through" cost.

B)Requires less allocation effort.

C)Is charged directly to that department.

D)Must be variable.

E)Must be fixed.

A)Is called a "flow through" cost.

B)Requires less allocation effort.

C)Is charged directly to that department.

D)Must be variable.

E)Must be fixed.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

12

Dual allocation is a cost allocation approach that separates direct and indirect costs, tracing the direct costs directly to the cost object that:

A)Can bear the cost.

B)Relates best to the cost.

C)Is first identified with the cost.

D)Caused the cost.

E)Is most impacted by the cost.

A)Can bear the cost.

B)Relates best to the cost.

C)Is first identified with the cost.

D)Caused the cost.

E)Is most impacted by the cost.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

13

Cost allocation is an important strategic issue for U.S.manufacturing firms is with foreign subsidiaries because of:

A)The tax implications.

B)Quality concerns.

C)Import restrictions.

D)Cultural differences.

E)The company's desire to grow.

A)The tax implications.

B)Quality concerns.

C)Import restrictions.

D)Cultural differences.

E)The company's desire to grow.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

14

The concepts of cost allocation that are used in manufacturing can also apply in:

A)Service and not-for-profit industries.

B)Service industries.

C)Not-for-profit industries.

D)Limited instances outside of manufacturing.

E)The concepts apply only in manufacturing.

A)Service and not-for-profit industries.

B)Service industries.

C)Not-for-profit industries.

D)Limited instances outside of manufacturing.

E)The concepts apply only in manufacturing.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

15

The most effective basis for cost allocation exists when which one of the following can be determined?

A)Cost shifting.

B)Benefit received.

C)Equity share.

D)Cause and effect relationship.

E)Ability to bear.

A)Cost shifting.

B)Benefit received.

C)Equity share.

D)Cause and effect relationship.

E)Ability to bear.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following methods considers all reciprocal flows between service departments through simultaneous equations?

A)Dual method.

B)Step method.

C)Reciprocal method.

D)Direct method.

E)The net realizable value method.

A)Dual method.

B)Step method.

C)Reciprocal method.

D)Direct method.

E)The net realizable value method.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

17

Allocation of service department costs to producing departments is the most complex of the allocation phase of departmental cost allocation because of the likely presence of:

A)Manager bias.

B)Formula distracters.

C)Repetitive steps.

D)Reciprocal flows.

E)Non-value adding activities.

A)Manager bias.

B)Formula distracters.

C)Repetitive steps.

D)Reciprocal flows.

E)Non-value adding activities.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

18

The reciprocal method can be solved using the Excel function:

A)Goal Seek

B)Regression

C)Solver

D)Scenarios

E)Pivot Tables

A)Goal Seek

B)Regression

C)Solver

D)Scenarios

E)Pivot Tables

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

19

If a budgeted activity base is used as the base in cost allocation, each department's cost allocation will be predictable, and not influenced by the:

A)Actual total cost.

B)Change in activity.

C)Variations from budget.

D)Errors in calculations.

E)Actual usage in other departments.

A)Actual total cost.

B)Change in activity.

C)Variations from budget.

D)Errors in calculations.

E)Actual usage in other departments.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

20

The mathematical technique that underlies the reciprocal cost allocation method is:

A)Regression analysis.

B)Simultaneous equations.

C)Analysis of variances.

D)Complex algebraic functions.

E)Multiple correlation.

A)Regression analysis.

B)Simultaneous equations.

C)Analysis of variances.

D)Complex algebraic functions.

E)Multiple correlation.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

21

The amount of joint costs allocated to product Z using the physical measure method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$8,000.

B)$32,000.

C)$43,222.

D)$14,000.

E)$6,666.

A)$8,000.

B)$32,000.

C)$43,222.

D)$14,000.

E)$6,666.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

22

The amount of joint costs allocated to product Y using the physical measure method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$22,876.

B)$44,300.

C)$18,500.

D)$16,000.

E)$32,000.

A)$22,876.

B)$44,300.

C)$18,500.

D)$16,000.

E)$32,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

23

The amount of joint costs allocated to product X using the physical measure method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$19,280.

B)$42,450.

C)$23,222.

D)$48,950.

E)$56,000.

A)$19,280.

B)$42,450.

C)$23,222.

D)$48,950.

E)$56,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

24

The amount of joint costs allocated to product M using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$3,614.

B)$4,688.

C)$23,438.

D)$33,434.

E)$46,875.

A)$3,614.

B)$4,688.

C)$23,438.

D)$33,434.

E)$46,875.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

25

Revenue methods of by-product cost allocation are justified on financial accounting concepts of:

A)Revenue realization and materiality.

B)Revenue realization, materiality, and cost-benefit.

C)Materiality and cost-benefit.

D)Materiality and stable dollar.

E)Cost-benefit and stable dollar.

A)Revenue realization and materiality.

B)Revenue realization, materiality, and cost-benefit.

C)Materiality and cost-benefit.

D)Materiality and stable dollar.

E)Cost-benefit and stable dollar.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

26

The amount of joint costs allocated to product L using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$3,614.

B)$4,688.

C)$23,438.

D)$33,434.

E)$46,875.

A)$3,614.

B)$4,688.

C)$23,438.

D)$33,434.

E)$46,875.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

27

The amount of joint costs allocated to product N using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$3,614.

B)$4,688.

C)$23,438.

D)$33,434.

E)$46,875.

A)$3,614.

B)$4,688.

C)$23,438.

D)$33,434.

E)$46,875.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

28

The departmental cost allocation approach is preferred when the firm has:

A)Homogeneous processes.

B)Heterogeneous processes.

C)Diverse products.

D)Many production activities.

A)Homogeneous processes.

B)Heterogeneous processes.

C)Diverse products.

D)Many production activities.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

29

Which one of the following methods of cost allocation is completed by taking the service flows to production departments only and determining each production department's share of that service?

A)Direct method.

B)Indirect method.

C)Step method.

D)Reciprocal method.

E)Cross-functional method.

A)Direct method.

B)Indirect method.

C)Step method.

D)Reciprocal method.

E)Cross-functional method.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

30

The amount of joint costs allocated to product M using the physical measure method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$23,438.

B)$33,434.

C)$40,313.

D)$27,109.

E)$11,250.

A)$23,438.

B)$33,434.

C)$40,313.

D)$27,109.

E)$11,250.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

31

The total cost accumulated in the assembly department using the direct method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$102,750.

B)$114,600.

C)$85,800.

D)$131,250.

E)$135,000.

A)$102,750.

B)$114,600.

C)$85,800.

D)$131,250.

E)$135,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

32

A concept which is commonly employed with allocation bases related to size is:

A)Cost shifting.

B)Benefit received.

C)Equity share.

D)Cause and effect relationship.

E)Ability to bear.

A)Cost shifting.

B)Benefit received.

C)Equity share.

D)Cause and effect relationship.

E)Ability to bear.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

33

The total cost accumulated in the assembly department using the step method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$104,500.

B)$109,950.

C)$124,050.

D)$130,750.

E)$136,500.

A)$104,500.

B)$109,950.

C)$124,050.

D)$130,750.

E)$136,500.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

34

The amount of joint costs allocated to product N using the physical measure method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$23,438.

B)$33,434.

C)$40,313.

D)$27,109.

E)$11,250.

A)$23,438.

B)$33,434.

C)$40,313.

D)$27,109.

E)$11,250.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

35

The total cost accumulated in the fabrication department using the step method is (assume the purchasing department goes first; calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$104,500.

B)$109,950.

C)$124,050.

D)$130,750.

E)$136,500.

A)$104,500.

B)$109,950.

C)$124,050.

D)$130,750.

E)$136,500.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

36

The amount of joint costs allocated to product L using the physical measure method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$23,438.

B)$33,434.

C)$40,313.

D)$27,109.

E)$11,250.

A)$23,438.

B)$33,434.

C)$40,313.

D)$27,109.

E)$11,250.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is not an ethical issue managers encounter with cost allocation?

A)Products that are produced for both a competitive market and a public agency.

B)Governmental agency provides a free service to the public.

C)Governmental agency reimburses the costs of a private institution.

D)Costs of products sold to or from foreign subsidiaries.

A)Products that are produced for both a competitive market and a public agency.

B)Governmental agency provides a free service to the public.

C)Governmental agency reimburses the costs of a private institution.

D)Costs of products sold to or from foreign subsidiaries.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

38

Which one of the following methods of allocating joint costs allocates joint costs to joint products on the basis of estimated sales values at the split-off point?

A)Net realizable value method.

B)Physical measure method.

C)Average cost method.

D)Net sales value method.

E)Sales value at split-off method.

A)Net realizable value method.

B)Physical measure method.

C)Average cost method.

D)Net sales value method.

E)Sales value at split-off method.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

39

Which one of the following methods of allocating joint costs uses a measure of weight, size or number of units to allocate joint costs to joint products?

A)Net realizable value method.

B)Physical unit method.

C)Product measure method.

D)Cost measure method.

E)Sales value at split-off method.

A)Net realizable value method.

B)Physical unit method.

C)Product measure method.

D)Cost measure method.

E)Sales value at split-off method.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

40

The total cost accumulated in the fabrication department using the direct method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$102,750.

B)$114,600.

C)$87,000.

D)$131,250.

E)$135,000.

A)$102,750.

B)$114,600.

C)$87,000.

D)$131,250.

E)$135,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

41

Net Realizable Value (NRV) of a product is:

A)Split-off cost - profit margin - additional processing and selling cost.

B)Profit at split-off + additional processing and selling cost.

C)Ultimate sales value - additional processing and selling cost.

D)Ultimate sales value + additional processing and selling cost.

E)Cost allocation plus separable cost.

A)Split-off cost - profit margin - additional processing and selling cost.

B)Profit at split-off + additional processing and selling cost.

C)Ultimate sales value - additional processing and selling cost.

D)Ultimate sales value + additional processing and selling cost.

E)Cost allocation plus separable cost.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following is not one of the objectives of cost allocation?

A)Motivate managers to exert a high-level of effort.

B)Provide useful departmental and product costs.

C)Identify production constraints.

D)Provide the right incentive for managers to make the right decisions.

E)Provide an appropriate basis for performance evaluation.

A)Motivate managers to exert a high-level of effort.

B)Provide useful departmental and product costs.

C)Identify production constraints.

D)Provide the right incentive for managers to make the right decisions.

E)Provide an appropriate basis for performance evaluation.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

43

For the purposes of cost accumulation, which of the following are identifiable as different individual products before the split-off point?

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following statements best describes a by-product?

A)A product that is produced from material that would otherwise be scrap.

B)A product that has a selling price similar to that of the main product.

C)A product created along with the main product whose sales value does not cover its cost of production.

D)A product that usually produces a small amount of revenue when compared to the main product's revenue.

E)A product that has a lower unit selling price than the main unit.

A)A product that is produced from material that would otherwise be scrap.

B)A product that has a selling price similar to that of the main product.

C)A product created along with the main product whose sales value does not cover its cost of production.

D)A product that usually produces a small amount of revenue when compared to the main product's revenue.

E)A product that has a lower unit selling price than the main unit.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

45

A key disincentive effect of departmental cost allocation can occur when:

A)allocated costs are less than external purchase costs.

B)managers do not understand the incentives in the allocation base.

C)the allocation base is actual usage.

D)the allocation base is budgeted usage.

E)the allocation base is greater than usage.

A)allocated costs are less than external purchase costs.

B)managers do not understand the incentives in the allocation base.

C)the allocation base is actual usage.

D)the allocation base is budgeted usage.

E)the allocation base is greater than usage.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

46

The departmental approach of cost allocation recognizes that the typical manufacturing operation involves which type(s) of departments?

A)Service departments and production departments.

B)Production departments and assembly departments.

C)Joint product departments and separable departments.

D)Cost pools and cost objects.

E)Support departments and other service departments.

A)Service departments and production departments.

B)Production departments and assembly departments.

C)Joint product departments and separable departments.

D)Cost pools and cost objects.

E)Support departments and other service departments.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

47

The amount of joint costs allocated to product Z using the sales value at split-off method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$19,222.

B)$35,000.

C)$18,450.

D)$28,496.

E)$17,778.

A)$19,222.

B)$35,000.

C)$18,450.

D)$28,496.

E)$17,778.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

48

The amount of joint costs allocated to product X using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$24,000.

B)$21,333.

C)$36,444.

D)$40,842.

E)$32,110.

A)$24,000.

B)$21,333.

C)$36,444.

D)$40,842.

E)$32,110.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

49

Place the following phases of the departmental approach in the correct order. 1.Allocate the production department costs to products.

2)Allocate service costs to the overhead costs.

3)Allocate the service department costs to the production department.

4)Trace all direct costs and allocate overhead costs to both the service and production departments.

A)3,4,1,2.

B)4,3,2,1.

C)4,3,1.

D)3,2,1.

E)1,3,2.

2)Allocate service costs to the overhead costs.

3)Allocate the service department costs to the production department.

4)Trace all direct costs and allocate overhead costs to both the service and production departments.

A)3,4,1,2.

B)4,3,2,1.

C)4,3,1.

D)3,2,1.

E)1,3,2.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

50

The total cost accumulated in the marketing department using the direct method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$100,000.

B)$104,000.

C)$126,000.

D)$130,000.

E)$87,000.

A)$100,000.

B)$104,000.

C)$126,000.

D)$130,000.

E)$87,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following is an example of a physical measure used in the physical measure method?

A)Pounds.

B)Minutes.

C)Seconds.

D)Dollars.

E)Volume.

A)Pounds.

B)Minutes.

C)Seconds.

D)Dollars.

E)Volume.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

52

The amount of joint costs allocated to product Y using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$21,222.

B)$24,000.

C)$18,050.

D)$17,155.

E)$33,333.

A)$21,222.

B)$24,000.

C)$18,050.

D)$17,155.

E)$33,333.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

53

Relative sales value at split-off is used to allocate: Cost Beyond

A)Option A

B)Option B

C)Option C

D)Option D

A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

54

By-product costing approaches include:

A)Activity-based approach.

B)Cost approach.

C)Asset recognition approach.

D)Resource consumption approach.

E)Sales value at split off approach.

A)Activity-based approach.

B)Cost approach.

C)Asset recognition approach.

D)Resource consumption approach.

E)Sales value at split off approach.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

55

The amount of joint costs allocated to product Y using the sales value at split-off method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$13,540.

B)$32,000.

C)$22,222.

D)$28,499.

E)$17,667.

A)$13,540.

B)$32,000.

C)$22,222.

D)$28,499.

E)$17,667.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

56

The amount of joint costs allocated to product Z using the net realizable value method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$14,333.

B)$15,158.

C)$18,624.

D)$17,667.

E)$32,454.

A)$14,333.

B)$15,158.

C)$18,624.

D)$17,667.

E)$32,454.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

57

Johns Company manufactures products R, S, and T from a joint process.The following information is available: Assuming that joint product costs are allocated using the relative-sales-value at split-off approach, what was the sales value at split-off for products R and S?

A)Option A

B)Option B

C)Option C

D)Option D

Assuming that joint product costs are allocated using the relative-sales-value at split-off approach, what was the sales value at split-off for products R and S? A)Option A

B)Option B

C)Option C

D)Option D

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

58

The amount of joint costs allocated to product X using the sales value at split-off method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$20.000.

B)$32,444.

C)$40,000.

D)$17,677.

E)$15,000.

A)$20.000.

B)$32,444.

C)$40,000.

D)$17,677.

E)$15,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

59

The cost allocation method most widely used because of its accuracy and ability to provide a detailed level of analysis is:

A)Departmental approach.

B)Activity-based approach.

C)Direct approach.

D)Accounting approach.

E)Joint product costing.

A)Departmental approach.

B)Activity-based approach.

C)Direct approach.

D)Accounting approach.

E)Joint product costing.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

60

Which is not a common method used to allocate costs under the departmental approach?

A)Dual method.

B)Step method.

C)Reciprocal method.

D)Direct method.

A)Dual method.

B)Step method.

C)Reciprocal method.

D)Direct method.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

61

The amount of joint costs allocated to product DBB-3 using the sales value at split-off method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$939,240.

B)$216,870.

C)$447,120.

D)$757,800.

E)$2,213,640.

A)$939,240.

B)$216,870.

C)$447,120.

D)$757,800.

E)$2,213,640.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

62

The amount of joint costs allocated to product DBB-1 using the net realizable value method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$2,009,160.

B)$286,500.

C)$881,640.

D)$667,345.

E)$709,200.

A)$2,009,160.

B)$286,500.

C)$881,640.

D)$667,345.

E)$709,200.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

63

The total cost accumulated in the finishing department using the step method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$1,000,125.

B)$1,890,000.

C)$689,875.

D)$642,000.

E)$923,000.

A)$1,000,125.

B)$1,890,000.

C)$689,875.

D)$642,000.

E)$923,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

64

The total cost accumulated in the finishing department using the direct method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$1,033,333.

B)$1,690,000.

C)$686,667.

D)$646,667.

E)$693,333.

A)$1,033,333.

B)$1,690,000.

C)$686,667.

D)$646,667.

E)$693,333.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

65

The total cost accumulated in the sales department using the direct method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$100,000.

B)$109,000.

C)$126,000.

D)$130,000.

E)$135,000.

A)$100,000.

B)$109,000.

C)$126,000.

D)$130,000.

E)$135,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

66

The total cost accumulated in the finishing department using the reciprocal method is(calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$1,890,000.

B)$627,143.

C)$682,551

D)$1,062,857.

E)$1,007,449.

A)$1,890,000.

B)$627,143.

C)$682,551

D)$1,062,857.

E)$1,007,449.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

67

The total cost accumulated in the assembly department using the reciprocal method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$1,890,000.

B)$627,143.

C)$682,551.

D)$1,062,857.

E)$1,007,449.

A)$1,890,000.

B)$627,143.

C)$682,551.

D)$1,062,857.

E)$1,007,449.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

68

The amount of joint costs allocated to product DBB-3 using the net realizable value method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$2,009,160.

B)$286,500.

C)$881,640.

D)$667,345.

E)$709,200.

A)$2,009,160.

B)$286,500.

C)$881,640.

D)$667,345.

E)$709,200.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

69

The total cost accumulated in the sales department using the reciprocal method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$102,222.

B)$122,402.

C)$127,778.

D)$142,471.

E)$150,050.

A)$102,222.

B)$122,402.

C)$127,778.

D)$142,471.

E)$150,050.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

70

The amount of joint costs allocated to product DBB-3 using the physical measure method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$54,250.

B)$757,800.

C)$1,705,320.

D)$49,200.

E)$1,136,880.

A)$54,250.

B)$757,800.

C)$1,705,320.

D)$49,200.

E)$1,136,880.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

71

The total cost accumulated in the sales department using the step method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$100,000.

B)$104,000.

C)$126,000.

D)$130,000.

E)$135,000.

A)$100,000.

B)$104,000.

C)$126,000.

D)$130,000.

E)$135,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

72

The amount of joint costs allocated to product DBB-2 using the net realizable value method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$2,009,160.

B)$286,500.

C)$881,640.

D)$667,345.

E)$709,200.

A)$2,009,160.

B)$286,500.

C)$881,640.

D)$667,345.

E)$709,200.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

73

The total cost accumulated in the assembly department using the direct method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$1,033,333.

B)$1,690,000.

C)$686,667.

D)$646,667.

E)$693,333.

A)$1,033,333.

B)$1,690,000.

C)$686,667.

D)$646,667.

E)$693,333.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

74

The amount of joint costs allocated to product DBB-1 using the physical measure method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$54,250.

B)$757,800.

C)$1,705,320.

D)$49,200.

E)$1,136,880.

A)$54,250.

B)$757,800.

C)$1,705,320.

D)$49,200.

E)$1,136,880.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

75

The total cost accumulated in the marketing department using the step method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$100,000.

B)$104,000.

C)$126,000.

D)$130,000.

E)$135,000.

A)$100,000.

B)$104,000.

C)$126,000.

D)$130,000.

E)$135,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

76

The amount of joint costs allocated to product DBB-1 using the sales value at split-off method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$939,240.

B)$216,870.

C)$447,120.

D)$757,800.

E)$2,213,640.

A)$939,240.

B)$216,870.

C)$447,120.

D)$757,800.

E)$2,213,640.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

77

The amount of joint costs allocated to product DBB-2 using the physical measure method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$54,250.

B)$757,800.

C)$1,705,320.

D)$49,200.

E)$1,136,880.

A)$54,250.

B)$757,800.

C)$1,705,320.

D)$49,200.

E)$1,136,880.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

78

The amount of joint costs allocated to product DBB-2 using the sales value at split-off method is (calculate all ratios and percentages to 2 decimal places, for example 33.33%, and round all dollar amounts to the nearest whole dollar):

A)$939,240.

B)$216,870.

C)$447,120.

D)$757,800.

E)$2,213,640.

A)$939,240.

B)$216,870.

C)$447,120.

D)$757,800.

E)$2,213,640.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

79

The total cost accumulated in the assembly department using the step method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$1,000,125.

B)$1,890,000.

C)$689,875.

D)$642,000.

E)$923,000.

A)$1,000,125.

B)$1,890,000.

C)$689,875.

D)$642,000.

E)$923,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

80

The total cost accumulated in the marketing department using the reciprocal method is (calculate all ratios and percentages to 4 decimal places, for example 33.3333%, and round all dollar amounts to the nearest whole dollar):

A)$102,222.

B)$122,402.

C)$127,778.

D)$142,471.

E)$150,050.

A)$102,222.

B)$122,402.

C)$127,778.

D)$142,471.

E)$150,050.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 96 flashcards in this deck.