Deck 5: Interest Rate Risk Measurement: The Repricing Model

Full screen (f)

Question

Question

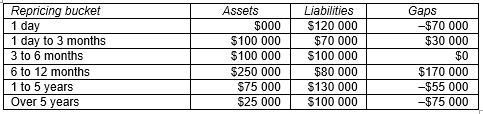

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the overnight interest rate increased by 100 basis points?

What is the annualised change in the bank's future net interest income if the overnight interest rate increased by 100 basis points?

A)-$700

B)$700

C)-$7000

D)$700

What is the annualised change in the bank's future net interest income if the overnight interest rate increased by 100 basis points?A)-$700

B)$700

C)-$7000

D)$700

Question

Question

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?

A)$7500

B)$7500

C)$0

D)Not enough information to answer the question.

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?A)$7500

B)$7500

C)$0

D)Not enough information to answer the question.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

Question

Question

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?

A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

Question

Consider the following repricing buckets and gaps:  What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

A)-$700

B)$700

C)-$7000

D)$700

What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?A)-$700

B)$700

C)-$7000

D)$700

Question

Question

Question

Question

Question

Question

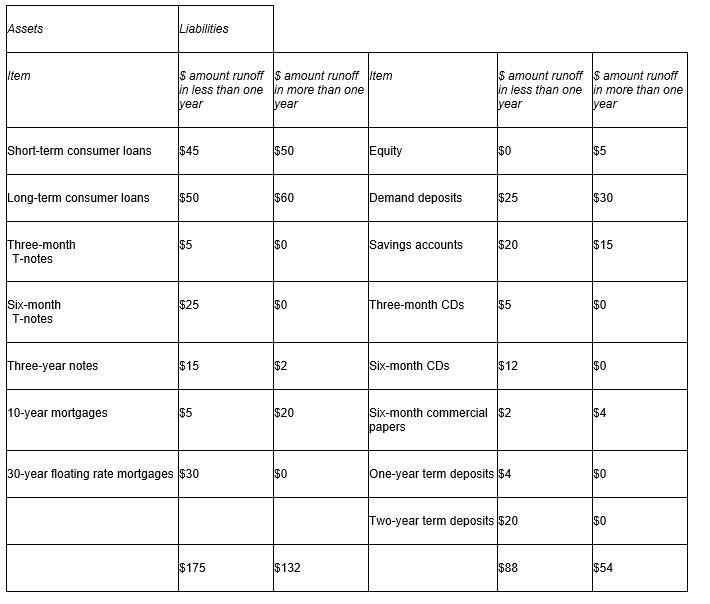

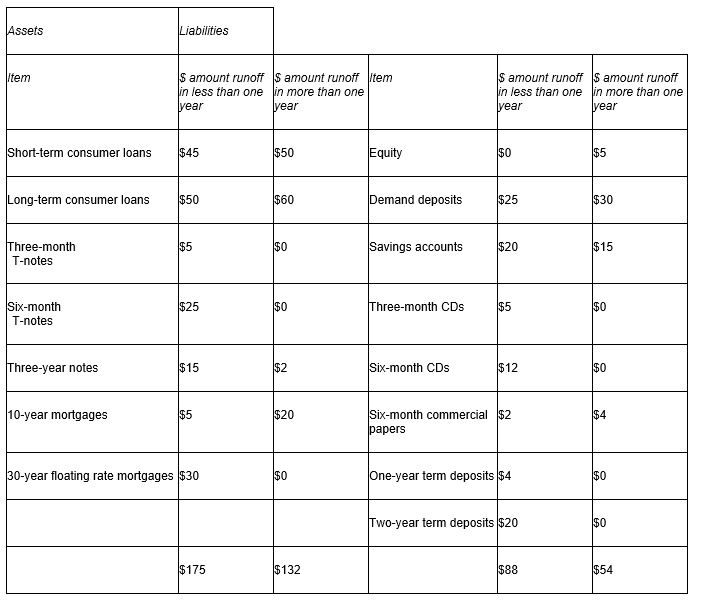

Consider the following table:  What is the one-year gap adjusted for runoffs?

What is the one-year gap adjusted for runoffs?

A)$43

B)$87

C)$121

D)$78

What is the one-year gap adjusted for runoffs?A)$43

B)$87

C)$121

D)$78

Question

Question

Question

Question

Consider the following table:  How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

A)The NII decreases by $0.435.

B)The NII increases by $0.435.

C)The NII remains constant.

D)The NII decreases by $0.39.

How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?A)The NII decreases by $0.435.

B)The NII increases by $0.435.

C)The NII remains constant.

D)The NII decreases by $0.39.

Question

Question

Question

Consider the following table:  How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?

How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?

A)The NII will not change.

B)The NII will increase by $50.

C)The NII will increase by $5.

D)The NII will decrease by $50.

How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?A)The NII will not change.

B)The NII will increase by $50.

C)The NII will increase by $5.

D)The NII will decrease by $50.

Question

Question

Question

Question

Question

Question

Question

Question

Question

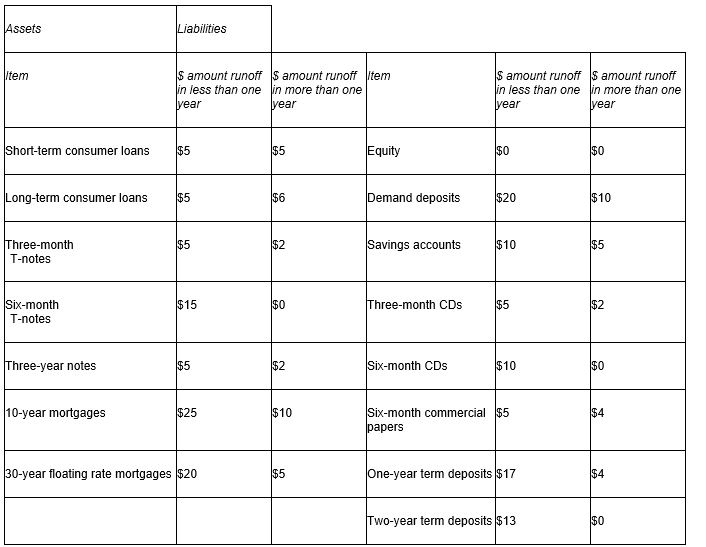

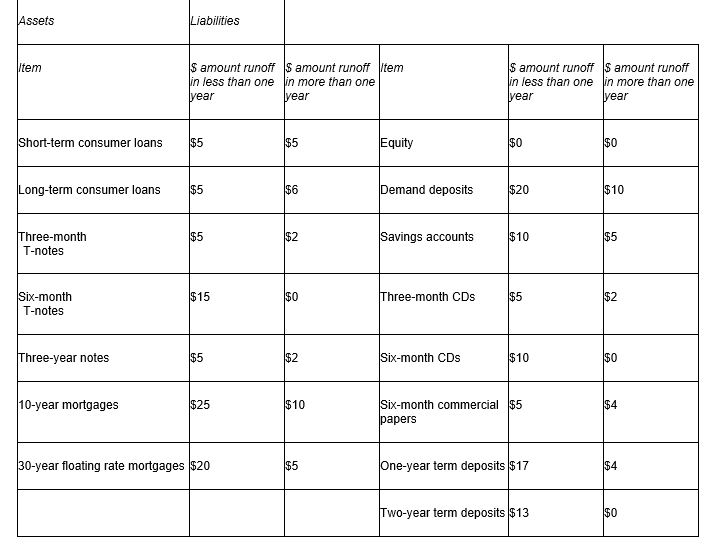

Consider the following table:  What is the one-year gap adjusted for runoffs?

What is the one-year gap adjusted for runoffs?

A)$0

B)$50

C)$55

D)$5.

What is the one-year gap adjusted for runoffs?A)$0

B)$50

C)$55

D)$5.

Question

Question

Question

Question

Question

Question

Question

Consider the following information to answer the question:  What will be the FI's net interest income at year-end if interest rates do not change?

What will be the FI's net interest income at year-end if interest rates do not change?

A)$3.20 million

B)$5.39 million

C)$1.89 million

D)$1.35 million

What will be the FI's net interest income at year-end if interest rates do not change?A)$3.20 million

B)$5.39 million

C)$1.89 million

D)$1.35 million

Question

Question

Question

Question

Question

Question

Question

Question

Consider the following information to answer the question:  What is the repricing gap for the FI?

What is the repricing gap for the FI?

A)$0

B)$5 000 000

C)$9 800 000

D)-$5 000 000

What is the repricing gap for the FI?A)$0

B)$5 000 000

C)$9 800 000

D)-$5 000 000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

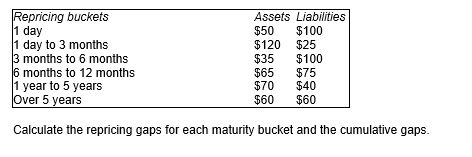

In the last quarter ABC Bank reported the following repricing buckets:

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/69

Play

Full screen (f)

Deck 5: Interest Rate Risk Measurement: The Repricing Model

1

Which of the following statements is true?

A)APRA requires smaller Australian FIs to use the repricing gap method to estimate interest rate exposures in their banking book for capital adequacy.

B)Australian FIs are only required to use the repricing gap method if they are listed on an US stock exchange.

C)APRA does not require Australian FIs to use the repricing gap method to estimate interest rate exposures in their banking book for capital adequacy.

D)Australian FIs are only required to use the repricing gap if they are internationally active.

A)APRA requires smaller Australian FIs to use the repricing gap method to estimate interest rate exposures in their banking book for capital adequacy.

B)Australian FIs are only required to use the repricing gap method if they are listed on an US stock exchange.

C)APRA does not require Australian FIs to use the repricing gap method to estimate interest rate exposures in their banking book for capital adequacy.

D)Australian FIs are only required to use the repricing gap if they are internationally active.

A

2

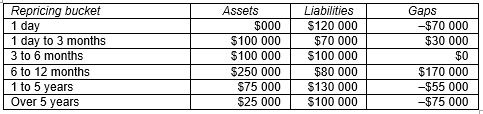

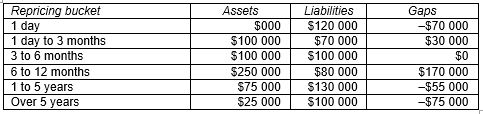

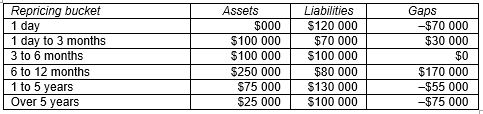

Consider the following repricing buckets and gaps: What is the annualised change in the bank's future net interest income if the overnight interest rate increased by 100 basis points?

A)-$700

B)$700

C)-$7000

D)$700

What is the annualised change in the bank's future net interest income if the overnight interest rate increased by 100 basis points?A)-$700

B)$700

C)-$7000

D)$700

A

3

What is spread effect?

A)Periodic cash flow of interest and principal amortisation payments on long-term assets that can be reinvested at market rates.

B)The effect that a change in the spread between rates on rate sensitive assets and rate sensitive liabilities has on net interest income as interest rates change.

C)The effect of mismatch of asset and liabilities within a maturity bucket.

D)The premium paid to compensate for the future uncertainty in a security's value.

A)Periodic cash flow of interest and principal amortisation payments on long-term assets that can be reinvested at market rates.

B)The effect that a change in the spread between rates on rate sensitive assets and rate sensitive liabilities has on net interest income as interest rates change.

C)The effect of mismatch of asset and liabilities within a maturity bucket.

D)The premium paid to compensate for the future uncertainty in a security's value.

B

4

Consider the following repricing buckets and gaps: What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?

A)$7500

B)$7500

C)$0

D)Not enough information to answer the question.

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced over five years is an increase of 50 basis points?A)$7500

B)$7500

C)$0

D)Not enough information to answer the question.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

5

The term core deposits refers to those deposits that:

A)act as long-term sources of funds for the FI.

B)reflect the true or core nature of the FI's operations.

C)support the core of the FI's operations.

D)None of the listed options are correct.

A)act as long-term sources of funds for the FI.

B)reflect the true or core nature of the FI's operations.

C)support the core of the FI's operations.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

6

Repricing gap refers to the:

A)difference between rate-sensitive assets and rate-sensitive liabilities.

B)sum of rate-sensitive assets and rate-sensitive liabilities.

C)difference between rate-sensitive liabilities and rate-sensitive assets.

D)difference between rate-insensitive assets and rate-insensitive liabilities.

A)difference between rate-sensitive assets and rate-sensitive liabilities.

B)sum of rate-sensitive assets and rate-sensitive liabilities.

C)difference between rate-sensitive liabilities and rate-sensitive assets.

D)difference between rate-insensitive assets and rate-insensitive liabilities.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

7

The cumulative gap over the whole balance sheet by definition:

A)must be greater than zero.

B)must be lower than zero.

C)must equal zero.

D)can take any value.

A)must be greater than zero.

B)must be lower than zero.

C)must equal zero.

D)can take any value.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

8

The term 'runoffs' refers to:

A)one-off cash flow of interest and principal amortisation payments on long-term assets.

B)periodic cash flow of interest and principal amortisation payments on long-term assets.

C)one-off cash flow of interest and principal amortisation payments on short-term assets.

D)periodic cash flow of interest and principal amortisation payments on short-term assets.

A)one-off cash flow of interest and principal amortisation payments on long-term assets.

B)periodic cash flow of interest and principal amortisation payments on long-term assets.

C)one-off cash flow of interest and principal amortisation payments on short-term assets.

D)periodic cash flow of interest and principal amortisation payments on short-term assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

9

The term 'rate-sensitive assets' refers to assets:

A)whose interest rate will be repriced over some future period.

B)with a particularly high interest rate.

C)with a particularly low interest rate.

D)for which demand is highly dependent on the level of interest rates.

A)whose interest rate will be repriced over some future period.

B)with a particularly high interest rate.

C)with a particularly low interest rate.

D)for which demand is highly dependent on the level of interest rates.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements is false?

A)A major reason for cheque accounts to be included in an FI's interest-sensitive liabilities is that the majority of these accounts are core deposits.

B)Cheque accounts should be treated as interest-sensitive liabilities because if interest rates rise, deposits might be withdrawn and thus will need to be replaced by higher-yielding deposits.

C)The final decision whether or not to include cheque accounts as rate sensitive liabilities must be made after an analysis of the actual deposit history.

D)None of the listed options are correct.

A)A major reason for cheque accounts to be included in an FI's interest-sensitive liabilities is that the majority of these accounts are core deposits.

B)Cheque accounts should be treated as interest-sensitive liabilities because if interest rates rise, deposits might be withdrawn and thus will need to be replaced by higher-yielding deposits.

C)The final decision whether or not to include cheque accounts as rate sensitive liabilities must be made after an analysis of the actual deposit history.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is true?

A)A negative gap indicates that a rise in interest rates would increase the bank's net interest income.

B)A positive gap indicates that a rise in interest rates would increase the bank's net interest income.

C)A positive gap indicates that a fall in interest rates would increase the bank's net interest income.

D)None of the listed options are correct.

A)A negative gap indicates that a rise in interest rates would increase the bank's net interest income.

B)A positive gap indicates that a rise in interest rates would increase the bank's net interest income.

C)A positive gap indicates that a fall in interest rates would increase the bank's net interest income.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements is true?

A)The repricing gap model is a market value accounting cash flow analysis of the repricing gap between the interest revenue earned on assets and the interest paid on liabilities over some period.

B)The repricing gap model is a book value accounting cash flow analysis of the repricing gap between the interest revenue earned on assets and the interest paid on liabilities over some period.

C)The repricing gap model is a market value accounting cash flow analysis of the repricing gap between the interest revenue earned on liabilities and the interest paid on assets over some period.

D)The repricing gap model is a book value accounting cash flow analysis of the repricing gap between the interest revenue earned on liabilities and the interest paid on assets over some period.

A)The repricing gap model is a market value accounting cash flow analysis of the repricing gap between the interest revenue earned on assets and the interest paid on liabilities over some period.

B)The repricing gap model is a book value accounting cash flow analysis of the repricing gap between the interest revenue earned on assets and the interest paid on liabilities over some period.

C)The repricing gap model is a market value accounting cash flow analysis of the repricing gap between the interest revenue earned on liabilities and the interest paid on assets over some period.

D)The repricing gap model is a book value accounting cash flow analysis of the repricing gap between the interest revenue earned on liabilities and the interest paid on assets over some period.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following are rate-sensitive assets?

A)Short-term consumer loans, cheque accounts and three-month Treasury notes.

B)Ten-year fixed rate mortgages, short-term consumer loans and long-term consumer loans.

C)Short-term consumer loans, ten-year fixed rate mortgages and one-year term deposits.

D)Short-term consumer loans, six-month Treasury notes and three-year

A)Short-term consumer loans, cheque accounts and three-month Treasury notes.

B)Ten-year fixed rate mortgages, short-term consumer loans and long-term consumer loans.

C)Short-term consumer loans, ten-year fixed rate mortgages and one-year term deposits.

D)Short-term consumer loans, six-month Treasury notes and three-year

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

14

Consider the following repricing buckets and gaps: What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements is true?

A)Cheque accounts are a type of interest-sensitive asset.

B)Cheque accounts are a type of interest-sensitive liability.

C)There are strong arguments for and against the inclusion of cheque accounts as a type of interest-sensitive asset.

D)There are strong arguments for and against the inclusion of cheque accounts as a type of interest-sensitive liability.

A)Cheque accounts are a type of interest-sensitive asset.

B)Cheque accounts are a type of interest-sensitive liability.

C)There are strong arguments for and against the inclusion of cheque accounts as a type of interest-sensitive asset.

D)There are strong arguments for and against the inclusion of cheque accounts as a type of interest-sensitive liability.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

16

Consider the following repricing buckets and gaps: What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?

A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?A)$17 000

B)-$17 000

C)$13 000

D)-$13 000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

17

Consider the following repricing buckets and gaps: What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

A)-$700

B)$700

C)-$7000

D)$700

What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?A)-$700

B)$700

C)-$7000

D)$700

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following statements is true?

A)A negative gap indicates that a rise in interest rates would lower the bank's net interest income.

B)A positive gap indicates that a rise in interest rates would lower the bank's net interest income.

C)A negative gap indicates that a rise in interest rates would increase the bank's net interest income.

D)None of the listed options are correct.

A)A negative gap indicates that a rise in interest rates would lower the bank's net interest income.

B)A positive gap indicates that a rise in interest rates would lower the bank's net interest income.

C)A negative gap indicates that a rise in interest rates would increase the bank's net interest income.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following statements is true?

A)As opposed to the duration model, the repricing gap model is a market-value based approach.

B)As opposed to the maturity model, the repricing gap model is a market-value based approach.

C)The capital loss effect is captured by the repricing model.

D)None of the listed options are correct.

A)As opposed to the duration model, the repricing gap model is a market-value based approach.

B)As opposed to the maturity model, the repricing gap model is a market-value based approach.

C)The capital loss effect is captured by the repricing model.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following are rate-sensitive liabilities?

A)Short-term consumer loans, cheque accounts and three-month Treasury notes.

B)Three-month term deposits, three month bankers' acceptances, six-month negotiable certificates of deposit and one-year term deposits.

C)Short-term consumer loans, six-month negotiable certificates of deposit and one-year term deposits.

D)Short-term consumer loans, six-month Treasury notes and three-year Treasury bonds.

A)Short-term consumer loans, cheque accounts and three-month Treasury notes.

B)Three-month term deposits, three month bankers' acceptances, six-month negotiable certificates of deposit and one-year term deposits.

C)Short-term consumer loans, six-month negotiable certificates of deposit and one-year term deposits.

D)Short-term consumer loans, six-month Treasury notes and three-year Treasury bonds.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following statements is true?

A)The cumulative repricing gap can also be expressed as a percentage of liabilities.

B)The cumulative repricing gap can also be expressed as a percentage of equity.

C)The cumulative repricing gap can also be expressed as a percentage of assets.

D)None of the listed options are correct.

A)The cumulative repricing gap can also be expressed as a percentage of liabilities.

B)The cumulative repricing gap can also be expressed as a percentage of equity.

C)The cumulative repricing gap can also be expressed as a percentage of assets.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

22

How do you interpret the position of an FI with a negative on-balance-sheet gap and a positive off-balance-sheet gap?

A)The FI uses its on-balance-sheet activities to hedge its off-balance-sheet activities.

B)The FI uses its off-balance-sheet activities to hedge its on-balance-sheet activities.

C)The FI believes that interest rates will decrease and made a mistake in setting its gap for off-balance-sheet activities.

D)The FI believes that interest rates will decrease and made a mistake in setting its gap for on-balance-sheet activities.

A)The FI uses its on-balance-sheet activities to hedge its off-balance-sheet activities.

B)The FI uses its off-balance-sheet activities to hedge its on-balance-sheet activities.

C)The FI believes that interest rates will decrease and made a mistake in setting its gap for off-balance-sheet activities.

D)The FI believes that interest rates will decrease and made a mistake in setting its gap for on-balance-sheet activities.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

23

Consider the following table: What is the one-year gap adjusted for runoffs?

A)$43

B)$87

C)$121

D)$78

What is the one-year gap adjusted for runoffs?A)$43

B)$87

C)$121

D)$78

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following statements is true?

A)An FI with a negative repricing gap expects interest rates to remain stable.

B)An FI with a negative repricing gap expects interest rates to rise.

C)An FI with a negative repricing gap expects interest rates to remain fall.

D)An FI with a negative repricing gap has not particular expectations regarding interest rate movements.

A)An FI with a negative repricing gap expects interest rates to remain stable.

B)An FI with a negative repricing gap expects interest rates to rise.

C)An FI with a negative repricing gap expects interest rates to remain fall.

D)An FI with a negative repricing gap has not particular expectations regarding interest rate movements.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following statements is true?

A)The runoff component is rate-sensitive.

B)The runoff component is rate-insensitive.

C)The runoff component refers to interest payments on long-term liabilities that need to be refinanced at market rates.

D)The run-off component refers to interest payments on short-term liabilities that need to be refinanced at market rates.

A)The runoff component is rate-sensitive.

B)The runoff component is rate-insensitive.

C)The runoff component refers to interest payments on long-term liabilities that need to be refinanced at market rates.

D)The run-off component refers to interest payments on short-term liabilities that need to be refinanced at market rates.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following statements is true?

A)An FI with a positive repricing gap expects interest rates to remain stable.

B)An FI with a positive repricing gap expects interest rates to rise.

C)An FI with a positive repricing gap expects interest rates to remain fall.

D)An FI with a positive repricing gap has not particular expectations regarding interest rate movements.

A)An FI with a positive repricing gap expects interest rates to remain stable.

B)An FI with a positive repricing gap expects interest rates to rise.

C)An FI with a positive repricing gap expects interest rates to remain fall.

D)An FI with a positive repricing gap has not particular expectations regarding interest rate movements.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

27

Consider the following table: How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

A)The NII decreases by $0.435.

B)The NII increases by $0.435.

C)The NII remains constant.

D)The NII decreases by $0.39.

How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?A)The NII decreases by $0.435.

B)The NII increases by $0.435.

C)The NII remains constant.

D)The NII decreases by $0.39.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following statements is true?

A)Expressing the repricing gap as a percentage of assets tells us the direction of the interest rate exposure.

B)Expressing the repricing gap as a percentage of liabilities tells us the scale of the interest rate exposure.

C)Expressing the repricing gap as a percentage of equity tells us the scale of the interest rate exposure.

D)Expressing the repricing gap as a percentage of liabilities tells us the direction of the interest rate exposure.

A)Expressing the repricing gap as a percentage of assets tells us the direction of the interest rate exposure.

B)Expressing the repricing gap as a percentage of liabilities tells us the scale of the interest rate exposure.

C)Expressing the repricing gap as a percentage of equity tells us the scale of the interest rate exposure.

D)Expressing the repricing gap as a percentage of liabilities tells us the direction of the interest rate exposure.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

29

How do you interpret the position of an FI with a positive on-balance-sheet gap and a negative off-balance sheet gap?

A)The FI uses its on-balance-sheet activities to hedge its off-balance-sheet activities.

B)The FI uses its off-balance-sheet activities to hedge its on-balance-sheet activities.

C)The FI believes that interest rates will increase and made a mistake in setting its gap for off-balance-sheet activities.

D)The FI believes that interest rates will increase and made a mistake in setting its gap for on-balance-sheet activities.

A)The FI uses its on-balance-sheet activities to hedge its off-balance-sheet activities.

B)The FI uses its off-balance-sheet activities to hedge its on-balance-sheet activities.

C)The FI believes that interest rates will increase and made a mistake in setting its gap for off-balance-sheet activities.

D)The FI believes that interest rates will increase and made a mistake in setting its gap for on-balance-sheet activities.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

30

Consider the following table: How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?

A)The NII will not change.

B)The NII will increase by $50.

C)The NII will increase by $5.

D)The NII will decrease by $50.

How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income ?A)The NII will not change.

B)The NII will increase by $50.

C)The NII will increase by $5.

D)The NII will decrease by $50.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements is true?

A)A major reason for cheque accounts to be excluded from an FI's interest-sensitive liabilities is that the majority of these accounts are core deposits.

B)Cheque accounts should be treated as interest-sensitive liabilities because if interest rates fall, deposits might be withdrawn and thus will need to be replaced by higher-yielding deposits.

C)The final decision whether or not to include cheque accounts as rate sensitive liabilities must be made by predicting depositors' behaviours.

D)None of the listed options are correct.

A)A major reason for cheque accounts to be excluded from an FI's interest-sensitive liabilities is that the majority of these accounts are core deposits.

B)Cheque accounts should be treated as interest-sensitive liabilities because if interest rates fall, deposits might be withdrawn and thus will need to be replaced by higher-yielding deposits.

C)The final decision whether or not to include cheque accounts as rate sensitive liabilities must be made by predicting depositors' behaviours.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following statements is true?

A)The major focus of the repricing gap is the capital loss effect.

B)The major focus of the repricing gap is the capital gains effect.

C)The repricing gap focuses on all three, the capital gains, the capital loss and the interest income effect.

D)The major focus of the repricing gap is the interest income effect.

A)The major focus of the repricing gap is the capital loss effect.

B)The major focus of the repricing gap is the capital gains effect.

C)The repricing gap focuses on all three, the capital gains, the capital loss and the interest income effect.

D)The major focus of the repricing gap is the interest income effect.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements is true?

A)An FI with a repricing gap of zero is unsure about interest rate movements.

B)An FI with a repricing gap of zero expects interest rates to rise.

C)An FI with a repricing gap of zero expects interest rates to remain fall.

D)An FI with a repricing gap of zero does not measure and manage its interest rate exposures.

A)An FI with a repricing gap of zero is unsure about interest rate movements.

B)An FI with a repricing gap of zero expects interest rates to rise.

C)An FI with a repricing gap of zero expects interest rates to remain fall.

D)An FI with a repricing gap of zero does not measure and manage its interest rate exposures.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following statements is true?

A)As opposed to the duration gap model, the repricing gap model captures the capital loss and capital gain effect.

B)The repricing gap model is a market-value based approach, while the duration model is a book-value based approach.

C)The repricing gap model does not consider the size and timing of cash flows.

D)The duration gap model focuses on the impact interest rate changes have on an FI's net interest income.

A)As opposed to the duration gap model, the repricing gap model captures the capital loss and capital gain effect.

B)The repricing gap model is a market-value based approach, while the duration model is a book-value based approach.

C)The repricing gap model does not consider the size and timing of cash flows.

D)The duration gap model focuses on the impact interest rate changes have on an FI's net interest income.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is true?

A)One problem with the repricing gap is over-aggregation, which means that while the dollar value of asset-sensitive liabilities and assets within one bucket might be the same, the repricing timing for assets and liabilities within this bucket might differ.

B)One problem with the repricing gap is over-aggregation, which means that managers cannot make informed decisions about interest rate movements.

C)An advantage of the repricing gap is over-aggregation, which means that the information provided in the buckets is precise.

D)None of the listed options are correct.

A)One problem with the repricing gap is over-aggregation, which means that while the dollar value of asset-sensitive liabilities and assets within one bucket might be the same, the repricing timing for assets and liabilities within this bucket might differ.

B)One problem with the repricing gap is over-aggregation, which means that managers cannot make informed decisions about interest rate movements.

C)An advantage of the repricing gap is over-aggregation, which means that the information provided in the buckets is precise.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following statements is true?

A)The size of the range over which bucket gaps are calculated does not matter as the repricing gap will always lead to exact results.

B)The shorter the range over which bucket gaps are calculated, the greater the potential error.

C)The shorter the range over which bucket gaps are calculated, the smaller the potential error.

D)None of the listed options are correct.

A)The size of the range over which bucket gaps are calculated does not matter as the repricing gap will always lead to exact results.

B)The shorter the range over which bucket gaps are calculated, the greater the potential error.

C)The shorter the range over which bucket gaps are calculated, the smaller the potential error.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

37

When repricing all interest sensitive assets and all interest sensitive liabilities in a balance sheet, the cumulative gap will be:

A)zero.

B)one.

C)greater than one.

D)a negative value.

A)zero.

B)one.

C)greater than one.

D)a negative value.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

38

Assume you are the manager of an FI.How would you structure your balance sheet using the repricing gap model if you expected interest rates to increase?

A)I would create a positive gap.

B)I would create a negative gap.

C)I would create a neutral gap.

D)It would depend on my FI's current profitability.

A)I would create a positive gap.

B)I would create a negative gap.

C)I would create a neutral gap.

D)It would depend on my FI's current profitability.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

39

Consider the following table: What is the one-year gap adjusted for runoffs?

A)$0

B)$50

C)$55

D)$5.

What is the one-year gap adjusted for runoffs?A)$0

B)$50

C)$55

D)$5.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following statements is true?

A)An FI that has a positive on-balance-sheet gap and a negative off-balance-sheet gap is not sure about interest movements.

B)An FI that has a positive on-balance-sheet gap and a negative off-balance-sheet gap has made a mistake in hedging its interest rate risk.

C)An FI that has a positive on-balance-sheet gap and a negative off-balance-sheet gap is using its off-balance-sheet position to hedge its on-balance-sheet position.

D)None of the listed options are correct.

A)An FI that has a positive on-balance-sheet gap and a negative off-balance-sheet gap is not sure about interest movements.

B)An FI that has a positive on-balance-sheet gap and a negative off-balance-sheet gap has made a mistake in hedging its interest rate risk.

C)An FI that has a positive on-balance-sheet gap and a negative off-balance-sheet gap is using its off-balance-sheet position to hedge its on-balance-sheet position.

D)None of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

41

The unbiased expectations theory of the term structure of interest rates:

A)assumes that long-term interest rates are an arithmetic average of short-term rates.

B)assumes that the yield curve reflects the market's current expectations of future short-term interest rates.

C)recognises that forward rates are perfect predictors of future interest rates.

D)assumes that risk premiums increase uniformly with maturity.

A)assumes that long-term interest rates are an arithmetic average of short-term rates.

B)assumes that the yield curve reflects the market's current expectations of future short-term interest rates.

C)recognises that forward rates are perfect predictors of future interest rates.

D)assumes that risk premiums increase uniformly with maturity.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

42

The bank has a positive repricing gap.Is it exposed to interest rate increases or decreases and why?

A)Interest rate increases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

B)Interest rate increases because the interest income on its assets will fall more than the interest expenses on its liabilities and net interest income will fall.

C)Interest rate decreases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

D)Interest rate decreases because the interest income on its assets will fall more than the interest expenses on its liabilities and net interest income will fall.

A)Interest rate increases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

B)Interest rate increases because the interest income on its assets will fall more than the interest expenses on its liabilities and net interest income will fall.

C)Interest rate decreases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

D)Interest rate decreases because the interest income on its assets will fall more than the interest expenses on its liabilities and net interest income will fall.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

43

An FI with a neutral repricing gap in its three to six month bucket is hedged against any interest rate changes at all points in time.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

44

The bank has a negative repricing gap.Is it exposed to interest rate increases or decreases and why?

A)Interest rate increases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

B)Interest rate increases because the interest income on its assets will rise by less than the interest expenses on its liabilities and net interest income will fall.

C)Interest rate decreases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

D)Interest rate decreases because the interest income on its assets will rise by less than the interest expenses on its liabilities and net interest income will fall.

A)Interest rate increases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

B)Interest rate increases because the interest income on its assets will rise by less than the interest expenses on its liabilities and net interest income will fall.

C)Interest rate decreases because the interest income on its assets will rise more than the interest expenses on its liabilities and net interest income will rise.

D)Interest rate decreases because the interest income on its assets will rise by less than the interest expenses on its liabilities and net interest income will fall.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

45

An FI with a positive repricing gap expects interest rates to decrease.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

46

Consider the following information to answer the question: What will be the FI's net interest income at year-end if interest rates do not change?

A)$3.20 million

B)$5.39 million

C)$1.89 million

D)$1.35 million

What will be the FI's net interest income at year-end if interest rates do not change?A)$3.20 million

B)$5.39 million

C)$1.89 million

D)$1.35 million

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

47

The market segmentation theory of the term structure of interest rates:

A)assumes that investors will hold long-term maturity assets if there is a sufficient premium to compensate for the uncertainty of the long term.

B)assumes that the yield curve reflects the market's current expectations of future short-term interest rates.

C)assumes that market rates are determined by supply and demand conditions within fairly distinct time or maturity buckets.

D)assumes that both investors and borrowers are willing to shift from one maturity sector to another to take advantage of opportunities arising from changing yields.

A)assumes that investors will hold long-term maturity assets if there is a sufficient premium to compensate for the uncertainty of the long term.

B)assumes that the yield curve reflects the market's current expectations of future short-term interest rates.

C)assumes that market rates are determined by supply and demand conditions within fairly distinct time or maturity buckets.

D)assumes that both investors and borrowers are willing to shift from one maturity sector to another to take advantage of opportunities arising from changing yields.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

48

The repricing model ignores information regarding the distribution of assets and liabilities within maturity buckets.This limitation of the model refers to:

A)market value effect.

B)over-aggregation.

C)runoffs and pre-payments.

D)off-balance sheet activities.

A)market value effect.

B)over-aggregation.

C)runoffs and pre-payments.

D)off-balance sheet activities.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

49

Over-aggregation and runoffs are the major problems associated with the repricing gap.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following is a weakness of the repricing model to measure interest rate risk?

A)Potential for over-aggregation of assets and liabilities within each maturity bucket.

B)It ignores how changes in interest rates affect the market value of assets and liabilities.

C)It ignores the reinvestment of loan interest and principal payments that are reinvested at current market rates and it fails to recognise off-balance-sheet activities that may be rate sensitive.

D)All of the listed options are correct.

A)Potential for over-aggregation of assets and liabilities within each maturity bucket.

B)It ignores how changes in interest rates affect the market value of assets and liabilities.

C)It ignores the reinvestment of loan interest and principal payments that are reinvested at current market rates and it fails to recognise off-balance-sheet activities that may be rate sensitive.

D)All of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

51

The repricing gap considers the timing and size of cash flows.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

52

The repricing gap is a book-value based approach.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

53

If an FI's repricing gap is less than zero, then:

A)it is deficient in its required reserves.

B)it is deficient in its capital ratio requirement.

C)its liability costs are more sensitive to changing market interest rates than are its asset yields.

D)its liability costs are less sensitive to changing market interest rates than are its asset yields.

A)it is deficient in its required reserves.

B)it is deficient in its capital ratio requirement.

C)its liability costs are more sensitive to changing market interest rates than are its asset yields.

D)its liability costs are less sensitive to changing market interest rates than are its asset yields.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

54

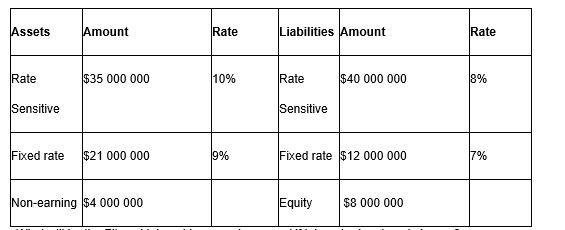

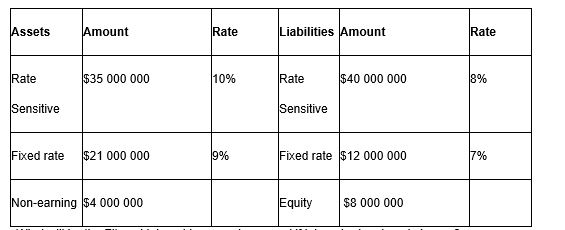

Consider the following information to answer the question: What is the repricing gap for the FI?

A)$0

B)$5 000 000

C)$9 800 000

D)-$5 000 000

What is the repricing gap for the FI?A)$0

B)$5 000 000

C)$9 800 000

D)-$5 000 000

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

55

The Reserve Bank of Australia's (RBA) undertook actions in regards to their open market operation in the post global financial crisis environment to move financial markets towards greater stability.This was achieved by:

A)increasing the maturity of repos to reduce money pressure in the money market over the longer term.

B)increasing RBA holdings of non-government securities for use with repos due to the shortage of government securities

C)increasing the supply of deposits held by banks and other authorised deposit-taking institutions in their exchange settlement accounts held with the RBA.

D)All of the listed options are correct.

A)increasing the maturity of repos to reduce money pressure in the money market over the longer term.

B)increasing RBA holdings of non-government securities for use with repos due to the shortage of government securities

C)increasing the supply of deposits held by banks and other authorised deposit-taking institutions in their exchange settlement accounts held with the RBA.

D)All of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

56

Convexity is the major problem associated with the repricing gap.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

57

The repricing gap focuses on the interest income effect.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

58

The repricing gap approach calculates the gaps in each maturity bucket by subtracting the:

A)current assets from the current liabilities.

B)long-term liabilities from the fixed assets.

C)rate sensitive assets from the total assets.

D)rate sensitive liabilities from the rate sensitive assets.

A)current assets from the current liabilities.

B)long-term liabilities from the fixed assets.

C)rate sensitive assets from the total assets.

D)rate sensitive liabilities from the rate sensitive assets.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

59

The liquidity premium theory of the term structure of interest rates:

A)assumes that investors will hold long-term maturity assets if there is a sufficient premium to compensate for the uncertainty of the long term.

B)assumes that long-term interest rates are an arithmetic average of short-term rates plus a liquidity premium.

C)recognises that forward rates are perfect predictors of future interest rates.

D)assumes that risk premiums increase uniformly with maturity.

A)assumes that investors will hold long-term maturity assets if there is a sufficient premium to compensate for the uncertainty of the long term.

B)assumes that long-term interest rates are an arithmetic average of short-term rates plus a liquidity premium.

C)recognises that forward rates are perfect predictors of future interest rates.

D)assumes that risk premiums increase uniformly with maturity.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

60

The Reserve Bank of Australia's (RBA) monetary policy can reduce an FI's interest rate risk:

A)by smoothing or targeting the level of interest rates it increases unexpected interest rate shocks and interest volatility.

B)by smoothing or targeting the level of interest rates it decreases unexpected interest rate shocks and interest volatility.

C)by letting interest rates find their own level it increases interest volatility.

D)All of the listed options are correct.

A)by smoothing or targeting the level of interest rates it increases unexpected interest rate shocks and interest volatility.

B)by smoothing or targeting the level of interest rates it decreases unexpected interest rate shocks and interest volatility.

C)by letting interest rates find their own level it increases interest volatility.

D)All of the listed options are correct.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

61

Outline what is meant by the CGAP effect and explain the relationship between interest rate changes and changes in net interest income.Specifically indicate whether a FI would wish to hold a negative or positive CGAP and under which interest rate conditions.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

62

An FI with a positive gap of $30 million suffers a $0.15 million decrease in its net interest income if interest rates increase by 0.5 per cent.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

63

The cumulative repricing gap position of an FI for a given extended time period is the sum of the repricing gap values for the individual time periods that make up the extended time period.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

64

What is meant by the 'run-off' problem and how can bank managers deal with this problem?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

65

Because the repricing model ignores the market value effect of changing interest rates, the repricing gap is an incomplete measure of the true interest rate risk exposure of an FI.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

66

If the spread between rate sensitive assets and rate sensitive liabilities increases for a bank, future changes in interest rates will lead to an increase in net interest income.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

67

Would you consider the repricing model to be a good and well-founded interest rate risk measurement and management tool? Why or why not?

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

68

In the last quarter ABC Bank reported the following repricing buckets:

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

69

An FI with a negative gap of $20 million suffers a $0.2 million decrease in its net interest income if interest rates decrease by 1 per cent.

Unlock Deck

Unlock for access to all 69 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 69 flashcards in this deck.