Deck 11: Partnerships: Distributions, transfer of Interests, and Terminations

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Barney,Bob,and Billie are equal partners in the BBB Partnership.The partnership balance sheet reads as follows on December 31 of the current year:

Partner Billie has an adjusted basis of $40,000 for her partnership interest.If Billie sells her entire partnership interest to new partner Janet for $60,000 cash,how much capital gain and ordinary income must Billie recognize from the sale?

A)$20,000 ordinary income.

B)$20,000 capital gain.

C)$10,000 ordinary income; $10,000 capital gain.

D)$30,000 ordinary income; $10,000 capital loss.

E)None of the above.

Partner Billie has an adjusted basis of $40,000 for her partnership interest.If Billie sells her entire partnership interest to new partner Janet for $60,000 cash,how much capital gain and ordinary income must Billie recognize from the sale?

A)$20,000 ordinary income.

B)$20,000 capital gain.

C)$10,000 ordinary income; $10,000 capital gain.

D)$30,000 ordinary income; $10,000 capital loss.

E)None of the above.

Question

The December 31,2008,balance sheet of the RST General Partnership reads as follows.

The partners share equally in partnership capital,income,gain,loss,deduction and credit.Ted's adjusted basis for his partnership interest is $40,000.On December 31,2008,he retires from the partnership,receiving a $60,000 cash payment in liquidation of his interest.The partnership agreement states that $2,500 of the payment is for goodwill.Which of the following statements about this distribution is false?

A)If capital is NOT a material income-producing factor to the partnership, the § 736(a) payment will be $2,500.

B)If capital IS a material income-producing factor, the entire $60,000 payment will be a § 736(b) property payment.

C)The payment for Ted's share of goodwill will create $2,500 of ordinary income to him.

D)The partnership can deduct any amount which is a § 736(a) payment since it will be determined without regard to partnership profits.

E)All statements are false.

The partners share equally in partnership capital,income,gain,loss,deduction and credit.Ted's adjusted basis for his partnership interest is $40,000.On December 31,2008,he retires from the partnership,receiving a $60,000 cash payment in liquidation of his interest.The partnership agreement states that $2,500 of the payment is for goodwill.Which of the following statements about this distribution is false?

A)If capital is NOT a material income-producing factor to the partnership, the § 736(a) payment will be $2,500.

B)If capital IS a material income-producing factor, the entire $60,000 payment will be a § 736(b) property payment.

C)The payment for Ted's share of goodwill will create $2,500 of ordinary income to him.

D)The partnership can deduct any amount which is a § 736(a) payment since it will be determined without regard to partnership profits.

E)All statements are false.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Carla,Marla,and Yancy are equal partners in the CMY Partnership.The partnership balance sheet reads as follows on December 31 of the current year.

Partner Yancy has an adjusted basis of $35,000 for his partnership interest.If Yancy sells his entire partnership interest to new partner Paula for $60,000 cash,how much can the partnership step-up the basis of Paula's share of partnership assets under §§ 754 and 743(b)?

A)$17,000.

B)$25,000.

C)$35,000.

D)$60,000.

E)None of the above.

Partner Yancy has an adjusted basis of $35,000 for his partnership interest.If Yancy sells his entire partnership interest to new partner Paula for $60,000 cash,how much can the partnership step-up the basis of Paula's share of partnership assets under §§ 754 and 743(b)?

A)$17,000.

B)$25,000.

C)$35,000.

D)$60,000.

E)None of the above.

Question

The RBD Partnership balance sheet on August 31 of the current year is as follows:

On that date,Rachel sells her one-third partnership interest to Bill for $300,000,including cash and relief of Rachel's share of the nonrecourse debt.The nonrecourse debt is shared equally among the partners.Rachel's outside basis for her partnership interest is $250,000.How much capital gain and/or ordinary income will Rachel recognize on the sale?

A)$20,000 capital gain; $30,000 ordinary income.

B)$30,000 capital gain; $20,000 ordinary income.

C)$50,000 capital gain; $0 ordinary income.

D)$0 capital gain; $50,000 ordinary income.

E)None of the above.

On that date,Rachel sells her one-third partnership interest to Bill for $300,000,including cash and relief of Rachel's share of the nonrecourse debt.The nonrecourse debt is shared equally among the partners.Rachel's outside basis for her partnership interest is $250,000.How much capital gain and/or ordinary income will Rachel recognize on the sale?

A)$20,000 capital gain; $30,000 ordinary income.

B)$30,000 capital gain; $20,000 ordinary income.

C)$50,000 capital gain; $0 ordinary income.

D)$0 capital gain; $50,000 ordinary income.

E)None of the above.

Question

The December 31,2008,balance sheet of the DIP Partnership reads as follows.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Dana receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.If Dana's outside basis for the partnership interest immediately before the distribution is $90,000,the recognized taxable gain and ordinary income from the distribution is:

A)$30,000 ordinary income.

B)$30,000 capital gain.

C)$10,000 capital gain; $20,000 ordinary income.

D)$20,000 capital gain; $10,000 ordinary income.

E)None of the above.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Dana receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.If Dana's outside basis for the partnership interest immediately before the distribution is $90,000,the recognized taxable gain and ordinary income from the distribution is:

A)$30,000 ordinary income.

B)$30,000 capital gain.

C)$10,000 capital gain; $20,000 ordinary income.

D)$20,000 capital gain; $10,000 ordinary income.

E)None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Greg has a 20% capital and profits interest in the calendar-year GDJ Partnership.His adjusted basis for his partnership interest on September 1 of the current year is $300,000.On that date,the partnership liquidates and makes a proportionate distribution of the following assets to Greg.

a.Calculate Greg's recognized gain or loss on the liquidating distribution, if any.

a. change if the partnership also distributed a chair to Greg? Assume the chair has a $500 adjusted basis (FMV is $800) to the partnership.

b.How would your answer to

a.Calculate Greg's recognized gain or loss on the liquidating distribution, if any.

a. change if the partnership also distributed a chair to Greg? Assume the chair has a $500 adjusted basis (FMV is $800) to the partnership.

b.How would your answer to

Question

Question

Question

Question

Question

Question

Suzy owns a 25% capital and profits interest in the calendar-year SJDV Partnership.Her adjusted basis for her partnership interest on July 1 of the current year is $200,000.On that date,she receives a proportionate nonliquidating current distribution of the following assets:

a.Calculate Suzy's recognized gain or loss on the distribution, if any.

b.Calculate Suzy's basis in the inventory received.

c.Calculate Suzy's basis in land received. The land is a capital asset.

d.Calculate Suzy's basis for her partnership interest after the distribution.

a.Calculate Suzy's recognized gain or loss on the distribution, if any.

b.Calculate Suzy's basis in the inventory received.

c.Calculate Suzy's basis in land received. The land is a capital asset.

d.Calculate Suzy's basis for her partnership interest after the distribution.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The December 31,2008,balance sheet of the BCD General Partnership reads as follows.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Cassie receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.Nothing is stated in the partnership agreement about goodwill.Cassie's outside basis for the partnership interest immediately before the distribution is $74,000.

How much is Cassie's recognized gain from the distribution and what is the character of the gain?

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Cassie receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.Nothing is stated in the partnership agreement about goodwill.Cassie's outside basis for the partnership interest immediately before the distribution is $74,000.

How much is Cassie's recognized gain from the distribution and what is the character of the gain?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/84

Play

Full screen (f)

Deck 11: Partnerships: Distributions, transfer of Interests, and Terminations

1

A § 754 election is made for a tax year in which the partner recognizes gain or loss on a distribution from the partnership or the basis in distributed property is increased or decreased from the inside basis the partnership held in those assets.The election is made by a partner any time it is necessary to adjust his or her share of the inside basis of partnership assets.

False

The partnership,not the partner,makes a basis adjustment election under § 754.Once made,the election remains in effect until it is revoked.

The partnership,not the partner,makes a basis adjustment election under § 754.Once made,the election remains in effect until it is revoked.

2

The JIH Partnership distributed the following assets to partner James in a proportionate liquidating distribution in which the partnership also liquidated: $25,000 cash,land parcel A (basis of $5,000,value of $30,000),and land parcel B (basis of $5,000,value of $15,000).James's basis in his partnership interest was $85,000 immediately before the distribution.James will allocate bases of $40,000 to parcel A and $20,000 to parcel B,and he will have no remaining basis in his partnership interest.

True

James takes a total substituted basis in the land parcels of $60,000 (basis in interest of $85,000 less $25,000 cash distribution).That basis must be allocated between the two properties.First,the properties take a carryover basis of $5,000 each.Next,the remaining basis is allocated to each property,up to its fair market value,resulting in basis allocations of $30,000 and $15,000,respectively.Last,the remaining $15,000 of basis is allocated between the properties according to their respective fair market values (bases after the second allocations): 2/3 of the $15,000 is added to the $30,000 basis of the first parcel and 1/3 is added to the $15,000 basis of the second parcel.Final basis allocations are $40,000 and $20,000,respectively.

James takes a total substituted basis in the land parcels of $60,000 (basis in interest of $85,000 less $25,000 cash distribution).That basis must be allocated between the two properties.First,the properties take a carryover basis of $5,000 each.Next,the remaining basis is allocated to each property,up to its fair market value,resulting in basis allocations of $30,000 and $15,000,respectively.Last,the remaining $15,000 of basis is allocated between the properties according to their respective fair market values (bases after the second allocations): 2/3 of the $15,000 is added to the $30,000 basis of the first parcel and 1/3 is added to the $15,000 basis of the second parcel.Final basis allocations are $40,000 and $20,000,respectively.

3

A payment to a retiring partner for his or her share of goodwill of a partnership in which capital is a material income-producing factor is classified as a § 736(a)income payment and results in ordinary income to the retiring partner and a current deduction to the partnership.

False

Goodwill is a § 736(a)income payment only if the payment is to a retiring general partner,the partnership is an entity in which capital is not a material income-producing factor,and the goodwill is not provided for in the partnership agreement.

Goodwill is a § 736(a)income payment only if the payment is to a retiring general partner,the partnership is an entity in which capital is not a material income-producing factor,and the goodwill is not provided for in the partnership agreement.

4

Matt,a partner in the MB Partnership,receives a proportionate,nonliquidating distribution of property having a fair market value of $16,000 and a partnership basis of $23,000.Matt's basis in the partnership is $10,000 before the distribution.In this situation,Matt will take a $10,000 basis in the property,and his basis in the partnership interest is reduced to zero.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

5

Jason sold his 40% interest in the HIJ Partnership to Kim for $280,000.The inside basis of all partnership assets was $600,000 at the time of the sale.If the partnership makes a § 754 election,it will record a $40,000 step-up in the basis of the partnership assets,and the step-up will be attributed solely to Kim.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

6

Generally,gain is recognized on a proportionate current or liquidating distribution only if the cash distributed exceeds the partner's basis in the partnership interest.For this purpose,relief of a partner's share of a liability is treated as a distribution of cash,and marketable securities distributed may be treated as cash.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

7

Tim and Janet are equal partners in the TJ Partnership.Partnership income for the year is $20,000.Tim needs cash in order to pay tax on his share of the partnership income,but Janet wants to leave the cash in the partnership for expansion.If the partners agree,it is acceptable to distribute $5,000 to Tim,and no cash or other property to Janet.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

8

Tim receives a proportionate nonliquidating distribution from the RST Partnership when the basis of his interest is $60,000.The distribution consists of cash of $40,000 and inventory with a partnership basis of $30,000 and fair market value of $35,000.As a result of this distribution,Tim recognizes a $10,000 gain and takes a $30,000 basis in the inventory.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

9

Rex and Scott operate a law practice in partnership form.Since Rex and Scott are brothers,the partnership is subject to the family partnership income reallocation rules.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

10

The Crimson Partnership is a service provider.Its assets consist of unrealized receivables (basis $0,value $200,000),cash of $200,000,and land (basis of $280,000,value of $400,000).Assume 25% general partner Jill has a basis in her partnership interest of $130,000.If the ongoing partnership distributes the $200,000 cash to Jill in liquidation of her interest in the partnership,she will recognize ordinary income of $50,000 and a capital gain of $20,000.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

11

A partnership has accounts receivable with a basis of $0 and a fair market value of $10,000 and depreciation recapture potential of $15,000.All other assets of the partnership are either cash,capital assets,or § 1231 assets.If a purchaser acquires a 30% interest in the partnership from another partner,the selling partner will be required to recognize ordinary income of $7,500.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

12

Terry received a proportionate share of partnership inventory in complete liquidation of her partnership interest.If Terry holds the distributed property as a capital asset for six years and sells it for a gain,the gain is taxed as a long-term capital gain.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

13

The MBC Partnership makes a § 736(b)cash payment of $50,000 to partner Betty in liquidation of her interest in the partnership.The partnership owns no hot assets.Betty's basis in her partnership interest before the distribution was $20,000.If the partnership has a § 754 election in effect,it will record a $30,000 decrease in its inside basis in partnership assets,allocable to the remaining partners in the partnership.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

14

Sarah owns a 30% interest in the capital and profits of the STP Partnership.Immediately before she receives a proportionate nonliquidating distribution from STP,the basis of her partnership interest is $25,000.The distribution consists of $20,000 in cash and land with a fair market value of $40,000.STP's adjusted basis in the land immediately before the distribution is $30,000.As a result of the distribution,Sarah recognizes a gain of $35,000 and her basis in the land is $40,000.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

15

Susan is a one-fourth limited partner in the SJ Partnership in which capital is not a material income-producing factor.Partnership assets consist of land (value of $100,000,basis of $80,000),accounts receivable (value of $100,000,basis of $0)and cash of $200,000.SJ distributes $100,000 of the cash to Susan in liquidation of her interest.Susan's basis in the partnership interest was $70,000 immediately before the distribution.Susan recognizes $25,000 of ordinary income,and a $5,000 capital gain on the distribution,and the partnership cannot claim a deduction for the $25,000 Susan recognizes as ordinary income.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

16

Milton contributed property to the MDB Partnership in 2006.At the time of the contribution,the basis in the property was $10,000 and its value was $15,000.In 2008,MDB distributed that property to partner Dana.Milton may be required to recognize gain on the distribution to Dana.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

17

Larry's partnership interest basis is $60,000.Larry receives a proportionate,liquidating distribution from a liquidating partnership of $45,000 cash and inventory having a basis of $30,000 to the partnership and a fair market value of $28,000.Larry assigns a basis of $15,000 to the inventory and recognizes no gain or loss.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

18

Maggie,a partner in the Magpie partnership,received a proportionate nonliquidating distribution of $20,000 cash,unrealized receivables with a basis of $0 and a fair market value of $30,000,and land with a basis of $25,000 and a fair market value of $20,000.Her basis in the partnership interest immediately before the distributions was $30,000.She will recognize $0 gain on the distribution,and her basis in the receivables and land will be $0 and $20,000 respectively.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

19

Carlos receives a proportionate liquidating distribution consisting of $8,000 cash and inventory with a basis to the partnership of $5,000 and a fair market value of $6,000.His basis in his partnership interest was $15,000 immediately before the distribution.Carlos assigns a basis of $5,000 to the inventory,and recognizes a $2,000 capital loss.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

20

The LMO Partnership distributed $30,000 cash to Laura in a proportionate,nonliquidating distribution.Laura's basis in her partnership interest was $25,000 immediately before the distribution.As a result of the distribution,Laura's basis is reduced to ($5,000)(negative)and she recognizes no gain or loss.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

21

James received $42,000 cash and a capital asset (basis of $45,000 and fair market value of $54,000)in a proportionate liquidating distribution.His basis in his partnership interest was $90,000 prior to the distribution.How much gain or loss does James recognize and what is his basis in the asset received?

A)$0 gain or loss; $45,000 basis.

B)$0 gain or loss; $48,000 basis.

C)$6,000 gain; $54,000 basis.

D)$3,000 loss; $45,000 basis.

E)$3,000 gain; $45,000 basis.

A)$0 gain or loss; $45,000 basis.

B)$0 gain or loss; $48,000 basis.

C)$6,000 gain; $54,000 basis.

D)$3,000 loss; $45,000 basis.

E)$3,000 gain; $45,000 basis.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

22

Toni's basis in her partnership interest was $60,000,including her $50,000 share of partnership liabilities.The partnership decides to liquidate,and after repaying all liabilities,distributes all remaining assets proportionately to the partners.Toni receives $20,000 cash and accounts receivable with a $12,000 basis and a $14,000 fair market value to the partnership.What gain or loss does Toni recognize,and what is her basis in the accounts receivable?

A)$0 gain; $12,000 basis.

B)$0 gain; $14,000 basis.

C)$10,000 gain; $0 basis.

D)$10,000 loss; $0 basis.

E)$10,000 gain; $12,000 basis.

A)$0 gain; $12,000 basis.

B)$0 gain; $14,000 basis.

C)$10,000 gain; $0 basis.

D)$10,000 loss; $0 basis.

E)$10,000 gain; $12,000 basis.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

23

Barney,Bob,and Billie are equal partners in the BBB Partnership.The partnership balance sheet reads as follows on December 31 of the current year:

Partner Billie has an adjusted basis of $40,000 for her partnership interest.If Billie sells her entire partnership interest to new partner Janet for $60,000 cash,how much capital gain and ordinary income must Billie recognize from the sale?

A)$20,000 ordinary income.

B)$20,000 capital gain.

C)$10,000 ordinary income; $10,000 capital gain.

D)$30,000 ordinary income; $10,000 capital loss.

E)None of the above.

Partner Billie has an adjusted basis of $40,000 for her partnership interest.If Billie sells her entire partnership interest to new partner Janet for $60,000 cash,how much capital gain and ordinary income must Billie recognize from the sale?

A)$20,000 ordinary income.

B)$20,000 capital gain.

C)$10,000 ordinary income; $10,000 capital gain.

D)$30,000 ordinary income; $10,000 capital loss.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

24

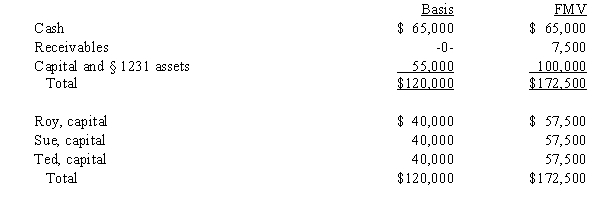

The December 31,2008,balance sheet of the RST General Partnership reads as follows.

The partners share equally in partnership capital,income,gain,loss,deduction and credit.Ted's adjusted basis for his partnership interest is $40,000.On December 31,2008,he retires from the partnership,receiving a $60,000 cash payment in liquidation of his interest.The partnership agreement states that $2,500 of the payment is for goodwill.Which of the following statements about this distribution is false?

A)If capital is NOT a material income-producing factor to the partnership, the § 736(a) payment will be $2,500.

B)If capital IS a material income-producing factor, the entire $60,000 payment will be a § 736(b) property payment.

C)The payment for Ted's share of goodwill will create $2,500 of ordinary income to him.

D)The partnership can deduct any amount which is a § 736(a) payment since it will be determined without regard to partnership profits.

E)All statements are false.

The partners share equally in partnership capital,income,gain,loss,deduction and credit.Ted's adjusted basis for his partnership interest is $40,000.On December 31,2008,he retires from the partnership,receiving a $60,000 cash payment in liquidation of his interest.The partnership agreement states that $2,500 of the payment is for goodwill.Which of the following statements about this distribution is false?

A)If capital is NOT a material income-producing factor to the partnership, the § 736(a) payment will be $2,500.

B)If capital IS a material income-producing factor, the entire $60,000 payment will be a § 736(b) property payment.

C)The payment for Ted's share of goodwill will create $2,500 of ordinary income to him.

D)The partnership can deduct any amount which is a § 736(a) payment since it will be determined without regard to partnership profits.

E)All statements are false.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

25

Marty receives a proportionate nonliquidating distribution when the basis of her partnership interest is $50,000.The distribution consists of $60,000 cash and noninventory property (adjusted basis to the partnership of $20,000; fair market value of $23,000).How much gain or loss does Marty recognize,and what is her basis in the distributed property and in her partnership interest following the distribution?

A)$0 gain or loss; $20,000 basis in property; $0 basis in partnership interest.

B)$0 gain or loss; $23,000 basis in property; $2,000 basis in partnership interest.

C)$10,000 capital gain; $0 basis in property; $0 basis in partnership interest.

D)$10,000 capital gain; $20,000 basis in property; $0 basis in partnership interest.

E)$10,000 ordinary income; $0 basis in property; $10,000 basis in partnership interest.

A)$0 gain or loss; $20,000 basis in property; $0 basis in partnership interest.

B)$0 gain or loss; $23,000 basis in property; $2,000 basis in partnership interest.

C)$10,000 capital gain; $0 basis in property; $0 basis in partnership interest.

D)$10,000 capital gain; $20,000 basis in property; $0 basis in partnership interest.

E)$10,000 ordinary income; $0 basis in property; $10,000 basis in partnership interest.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

26

A partnership may make an optional election to adjust the basis of its property on a distribution to a partner which liquidates the partner's entire interest in the partnership.If such an election is in effect,the partnership:

A)Generally applies the election to transfers that take place at any later date, unless the election is revoked.

B)Only adjusts the basis of its property for differences in basis between that of the partnership and a distributee partner if a transferor-transferee situation arises within two years after the distribution.

C)Increases the basis of similar retained assets when a distributee partner takes a basis which is greater than the partnership's basis in these assets, assuming the partnership does not have any receivables or inventory.

D)Decreases the basis of similar retained assets when a distributee partner takes a basis for the distributed assets which is less than the partnership's basis in these assets.

E)All of the above.

A)Generally applies the election to transfers that take place at any later date, unless the election is revoked.

B)Only adjusts the basis of its property for differences in basis between that of the partnership and a distributee partner if a transferor-transferee situation arises within two years after the distribution.

C)Increases the basis of similar retained assets when a distributee partner takes a basis which is greater than the partnership's basis in these assets, assuming the partnership does not have any receivables or inventory.

D)Decreases the basis of similar retained assets when a distributee partner takes a basis for the distributed assets which is less than the partnership's basis in these assets.

E)All of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following transactions will not result in termination of a partnership for Federal tax purposes?

A)The partnership is incorporated.

B)A 70% interest in partnership capital and profits is sold to a third party purchaser.

C)Cash is distributed in liquidation of a 60% partner's interest in a five-partner partnership.

D)A 40% interest in partnership capital and profits is sold to the other partner in a two-partner partnership.

E)None of the above.

A)The partnership is incorporated.

B)A 70% interest in partnership capital and profits is sold to a third party purchaser.

C)Cash is distributed in liquidation of a 60% partner's interest in a five-partner partnership.

D)A 40% interest in partnership capital and profits is sold to the other partner in a two-partner partnership.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

28

On December 31 of last year,Pat gave his daughter,Joy,a gift of a 50% interest in a partnership in which capital is a material income-producing factor.For the current calendar year,the partnership's ordinary income was $100,000.Pat and Joy were the only partners,and there were no guaranteed payments.Pat's services performed for the partnership were worth $40,000,and Joy has never performed any services.What is Joy's distributive share of partnership income for the current year?

A)$50,000.

B)$40,000.

C)$30,000.

D)$20,000.

E)None of the above.

A)$50,000.

B)$40,000.

C)$30,000.

D)$20,000.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following statements about the transfer of a partnership interest is not true?

A)The seller's adjusted basis for the partnership interest is increased by the seller's share of undistributed partnership income (or reduced by partnership loss) for the portion of the partnership's taxable year ending on the date of the sale.

B)The partnership taxable year generally closes with respect to a partner who transfers a partnership interest at death.

C)The amount realized on the sale of a partnership interest is the sum of any money and the fair market value of any property received for the interest, plus the selling partner's share of partnership liabilities under § 752.

D)With respect to a transfer of a partnership interest by gift, all partnership gain, loss, credit, etc., items are allocated to the donor.

E)All of the above are true statements.

A)The seller's adjusted basis for the partnership interest is increased by the seller's share of undistributed partnership income (or reduced by partnership loss) for the portion of the partnership's taxable year ending on the date of the sale.

B)The partnership taxable year generally closes with respect to a partner who transfers a partnership interest at death.

C)The amount realized on the sale of a partnership interest is the sum of any money and the fair market value of any property received for the interest, plus the selling partner's share of partnership liabilities under § 752.

D)With respect to a transfer of a partnership interest by gift, all partnership gain, loss, credit, etc., items are allocated to the donor.

E)All of the above are true statements.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

30

Beth has an outside basis of $60,000 in the BBDE Partnership as of December 31 of the current year.On that date the partnership liquidates and distributes to Beth a proportionate distribution of $20,000 cash and inventory with an inside basis to the partnership of $18,000 and a fair market value of $22,000.In addition,Beth receives a desk (not inventory)which has an inside basis and fair market value of $200 and $350,respectively.None of the distribution is for partnership goodwill.How much gain or loss will Beth recognize on the distribution,and what basis will she take in the desk?

A)$21,800 loss; $200 basis.

B)$21,650 loss; $350 basis.

C)$0 loss; $200 basis.

D)$0 loss; $22,000 basis.

E)None of the above.

A)$21,800 loss; $200 basis.

B)$21,650 loss; $350 basis.

C)$0 loss; $200 basis.

D)$0 loss; $22,000 basis.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

31

Last year,Oscar contributed nondepreciable property with a basis of $40,000 and a fair market value of $50,000 to the Starling Partnership in exchange for a 25% interest in the partnership.In the current year,he receives a nonliquidating distribution from the partnership of other property with a basis to the partnership of $26,000 and a fair market value of $32,000.The basis in his partnership interest at the time of the distribution was $30,000.How much gain or loss does Oscar recognize on the distribution? (Assume no other distributions have been made to Oscar,the property he originally contributed is still owned by the partnership,and this is not a disguised sale transaction.)

A)$0 gain or loss.

B)$2,000 gain.

C)$10,000 gain.

D)$18,000 gain.

E)$4,000 loss.

A)$0 gain or loss.

B)$2,000 gain.

C)$10,000 gain.

D)$18,000 gain.

E)$4,000 loss.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

32

Carl receives a proportionate nonliquidating distribution when the basis of his partnership interest is $60,000.The distribution consists of $20,000 in cash and property with an adjusted basis to the partnership of $35,000 and a fair market value of $45,000.Carl's basis in the noncash property and his remaining basis in the partnership interest are:

A)$60,000; $0.

B)$35,000; $0.

C)$35,000; $5,000.

D)$40,000; $0.

E)None of the above.

A)$60,000; $0.

B)$35,000; $0.

C)$35,000; $5,000.

D)$40,000; $0.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

33

A limited liability company generally provides limited liability for those owners that are not active in the management of the LLC but requires owner-managers of the LLC to have unlimited personal liability for LLC debts.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

34

Carla,Marla,and Yancy are equal partners in the CMY Partnership.The partnership balance sheet reads as follows on December 31 of the current year.

Partner Yancy has an adjusted basis of $35,000 for his partnership interest.If Yancy sells his entire partnership interest to new partner Paula for $60,000 cash,how much can the partnership step-up the basis of Paula's share of partnership assets under §§ 754 and 743(b)?

A)$17,000.

B)$25,000.

C)$35,000.

D)$60,000.

E)None of the above.

Partner Yancy has an adjusted basis of $35,000 for his partnership interest.If Yancy sells his entire partnership interest to new partner Paula for $60,000 cash,how much can the partnership step-up the basis of Paula's share of partnership assets under §§ 754 and 743(b)?

A)$17,000.

B)$25,000.

C)$35,000.

D)$60,000.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

35

The RBD Partnership balance sheet on August 31 of the current year is as follows:

On that date,Rachel sells her one-third partnership interest to Bill for $300,000,including cash and relief of Rachel's share of the nonrecourse debt.The nonrecourse debt is shared equally among the partners.Rachel's outside basis for her partnership interest is $250,000.How much capital gain and/or ordinary income will Rachel recognize on the sale?

A)$20,000 capital gain; $30,000 ordinary income.

B)$30,000 capital gain; $20,000 ordinary income.

C)$50,000 capital gain; $0 ordinary income.

D)$0 capital gain; $50,000 ordinary income.

E)None of the above.

On that date,Rachel sells her one-third partnership interest to Bill for $300,000,including cash and relief of Rachel's share of the nonrecourse debt.The nonrecourse debt is shared equally among the partners.Rachel's outside basis for her partnership interest is $250,000.How much capital gain and/or ordinary income will Rachel recognize on the sale?

A)$20,000 capital gain; $30,000 ordinary income.

B)$30,000 capital gain; $20,000 ordinary income.

C)$50,000 capital gain; $0 ordinary income.

D)$0 capital gain; $50,000 ordinary income.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

36

The December 31,2008,balance sheet of the DIP Partnership reads as follows.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Dana receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.If Dana's outside basis for the partnership interest immediately before the distribution is $90,000,the recognized taxable gain and ordinary income from the distribution is:

A)$30,000 ordinary income.

B)$30,000 capital gain.

C)$10,000 capital gain; $20,000 ordinary income.

D)$20,000 capital gain; $10,000 ordinary income.

E)None of the above.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Dana receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.If Dana's outside basis for the partnership interest immediately before the distribution is $90,000,the recognized taxable gain and ordinary income from the distribution is:

A)$30,000 ordinary income.

B)$30,000 capital gain.

C)$10,000 capital gain; $20,000 ordinary income.

D)$20,000 capital gain; $10,000 ordinary income.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

37

Marilyn is a partner in a continuing partnership.At the end of the current year,the partnership distributed to Marilyn in a proportionate,nonliquidating distribution cash of $40,000,inventory with a basis to the partnership of $12,000 and a fair market value of $10,000,and a parcel of land with a basis to the partnership of $30,000 and a fair market value of $40,000.Marilyn's basis in the partnership interest was $80,000 before the distribution.What basis does Marilyn take in the inventory and land,and what is her basis in the partnership interest following the distribution?

A)$12,000 basis in inventory; $30,000 basis in land; $38,000 basis in partnership.

B)$12,000 basis in inventory; $40,000 basis in land; $28,000 basis in partnership.

C)$10,000 basis in inventory; $30,000 basis in land; $0 basis in partnership.

D)$10,000 basis in inventory; $40,000 basis in land; $30,000 basis in partnership.

E)$12,000 basis in inventory; $28,000 basis in land; $0 basis in partnership.

A)$12,000 basis in inventory; $30,000 basis in land; $38,000 basis in partnership.

B)$12,000 basis in inventory; $40,000 basis in land; $28,000 basis in partnership.

C)$10,000 basis in inventory; $30,000 basis in land; $0 basis in partnership.

D)$10,000 basis in inventory; $40,000 basis in land; $30,000 basis in partnership.

E)$12,000 basis in inventory; $28,000 basis in land; $0 basis in partnership.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following statements,if any,about an LLC is false?

A)An LLC is usually taxed like a partnership.

B)"Members" of an LLC generally have limited personal liability for debts of the LLC.

C)"Members" of an LLC can participate in management of the LLC unless the member agrees not to participate.

D)An LLC can specially allocate income items, as long as the substantial economic effect rules of § 704(b) are followed.

E)None of the above statements is false.

A)An LLC is usually taxed like a partnership.

B)"Members" of an LLC generally have limited personal liability for debts of the LLC.

C)"Members" of an LLC can participate in management of the LLC unless the member agrees not to participate.

D)An LLC can specially allocate income items, as long as the substantial economic effect rules of § 704(b) are followed.

E)None of the above statements is false.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

39

Wendy receives a proportionate nonliquidating distribution from the WXY Partnership.The distribution consists of $75,000 cash and property with an adjusted basis to the partnership of $20,000 and a fair market value of $25,000.Immediately before the distribution,Wendy's adjusted basis for her partnership interest is $90,000.Wendy's basis in the noncash property received is:

A)$0.

B)$15,000.

C)$20,000.

D)$25,000.

E)None of the above.

A)$0.

B)$15,000.

C)$20,000.

D)$25,000.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

40

The ABC Partnership makes a proportionate distribution of its assets to Charles,in complete liquidation of his partnership interest.The distribution consists of $30,000 in cash and capital assets with a basis to the partnership of $20,000 and a fair market value of $28,000.None of the payment is for partnership goodwill.At the time of the distribution,Charles's partnership basis is $42,000 and the partnership has no liabilities and no "hot assets." If the partnership makes an optional basis adjustment election on a timely filed return,it recognizes:

A)Capital gain of $16,000 and increases the basis of its remaining assets by $8,000.

B)Capital loss of $8,000 and decreases the basis of its remaining assets by $16,000.

C)No gain or loss and increases the basis of its remaining assets by $8,000.

D)No gain or loss and decreases the basis of its remaining assets by $16,000.

E)None of the above.

A)Capital gain of $16,000 and increases the basis of its remaining assets by $8,000.

B)Capital loss of $8,000 and decreases the basis of its remaining assets by $16,000.

C)No gain or loss and increases the basis of its remaining assets by $8,000.

D)No gain or loss and decreases the basis of its remaining assets by $16,000.

E)None of the above.

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

41

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Sales price of partnership interest

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Sales price of partnership interest

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

42

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Nonliquidating distribution

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Nonliquidating distribution

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

43

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Inventory

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Inventory

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

44

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Hot assets

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Hot assets

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

45

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Ordering rules

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Ordering rules

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

46

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Nonqualified distribution

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Nonqualified distribution

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

47

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Capital intensive partnership

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Capital intensive partnership

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

48

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Substantially appreciated inventory

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Substantially appreciated inventory

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

49

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Stated goodwill

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Stated goodwill

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

50

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Service providing partnership

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Service providing partnership

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

51

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Disproportionate distribution

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Disproportionate distribution

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

52

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Liquidating distribution

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Liquidating distribution

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

53

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Unstated goodwill

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Unstated goodwill

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

54

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Section 754

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Section 754

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

55

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Mandatory step down

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Mandatory step down

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

56

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Depreciation recapture

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Depreciation recapture

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

57

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Limited partner

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

Limited partner

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

58

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

General partner

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

General partner

Unlock Deck

Unlock for access to all 84 flashcards in this deck.

Unlock Deck

k this deck

59

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

Unrealized receivable