Exam 11: Partnerships: Distributions, transfer of Interests, and Terminations

Exam 1: Understanding and Working With the Federal Tax Law72 Questions

Exam 2: Corporations: Introduction and Operating Rules103 Questions

Exam 3: Corporations: Special Situations76 Questions

Exam 4: Corporations: Organization and Capital Structure91 Questions

Exam 5: Corporations: Earnings and Profits and Dividend Distributions82 Questions

Exam 6: Corporations: Redemptions and Liquidations107 Questions

Exam 7: Corporations: Reorganizations138 Questions

Exam 8: Consolidated Tax Returns143 Questions

Exam 9: Taxation of International Transactions142 Questions

Exam 10: Partnerships: Formation, operation, and Basis71 Questions

Exam 11: Partnerships: Distributions, transfer of Interests, and Terminations84 Questions

Exam 12: S Corporations161 Questions

Exam 13: Comparative Forms of Doing Business139 Questions

Exam 14: Exempt Entities159 Questions

Exam 15: Multistate Corporate Taxation169 Questions

Exam 16: Tax Practice and Ethics147 Questions

Exam 17: The Federal Gift and Estate Taxes199 Questions

Exam 18: Family Tax Planning168 Questions

Exam 19: Income Taxation of Trusts and Estates155 Questions

Select questions type

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

-Nonqualified distribution

Free

(Short Answer)

4.9/5  (42)

(42)

Correct Answer: Verified

Verified

K

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below.

a.A payment for the partner's share of partnership income under § 736(a).

b.A payment for the partner's share of partnership property under § 736(b).

c.The payment includes both a § 736(a) and a § 736(b) element.

-Installment receivables for sale of a capital asset.

Free

(Short Answer)

4.9/5 (42)

Correct Answer:Verified

C

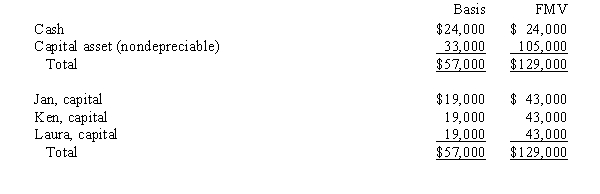

The December 31,2008,balance sheet of the calendar-year JKL Partnership reads as follows.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.On December 31,2008,Jan sells her 1/3 partnership interest to Jennifer for $43,000 cash.Assume the partnership makes a § 754 election for 2008.

a.What is the amount of Jennifer's "step-up" adjustment under § 743(b)?

b.If the nondepreciable capital asset is sold the next year for $120,000, determine the amount of gain that Jennifer will recognize on her tax return because of the sale.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.On December 31,2008,Jan sells her 1/3 partnership interest to Jennifer for $43,000 cash.Assume the partnership makes a § 754 election for 2008.

a.What is the amount of Jennifer's "step-up" adjustment under § 743(b)?

b.If the nondepreciable capital asset is sold the next year for $120,000, determine the amount of gain that Jennifer will recognize on her tax return because of the sale.

Free

(Essay)

4.8/5 (35)

Correct Answer:Verified

a.Jennifer has a § 743(b)step-up adjustment of $24,000 under § 754.The adjustment is determined by subtracting Jennifer's $19,000 share of the inside basis of partnership assets from her $43,000 purchase price for the interest.

b.Jennifer recognizes a $5,000 gain on the sale of the nondepreciable capital asset.When Jennifer acquires the partnership interest,the $24,000 § 743(b)adjustment is allocated to the capital asset under § 755.When the partnership sells the capital asset for $120,000,Jennifer can offset $24,000 of the $29,000 [($120,000 - $33,000)* 1/3] gain she would otherwise recognize with the § 743(b)adjustment.The remaining $5,000 of gain allocated to Jennifer is taxed to her on her return.

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-Mandatory step down

(Short Answer)

4.9/5 (40)

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below.

a.A payment for the partner's share of partnership income under § 736(a).

b.A payment for the partner's share of partnership property under § 736(b).

c.The payment includes both a § 736(a) and a § 736(b) element.

-Payment of an annuity to a retiring general partner in a service oriented partnership of 5% of partnership profits each year for the five years following the partner's retirement.

(Short Answer)

4.8/5 (40)

A partnership has accounts receivable with a basis of $0 and a fair market value of $10,000 and depreciation recapture potential of $15,000.All other assets of the partnership are either cash,capital assets,or § 1231 assets.If a purchaser acquires a 30% interest in the partnership from another partner,the selling partner will be required to recognize ordinary income of $7,500.

(True/False)

4.8/5 (32)

The December 31,2008,balance sheet of the DIP Partnership reads as follows.

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Dana receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.If Dana's outside basis for the partnership interest immediately before the distribution is $90,000,the recognized taxable gain and ordinary income from the distribution is:

Each partner shares in 1/3 of the partnership capital,income,gain,loss,deduction and credit.Capital is not a material income-producing factor to the partnership.On December 31,2008,general partner Dana receives a distribution of $120,000 cash in liquidation of her partnership interest under § 736.If Dana's outside basis for the partnership interest immediately before the distribution is $90,000,the recognized taxable gain and ordinary income from the distribution is:

(Multiple Choice)

4.8/5 (34)

Jason sold his 40% interest in the HIJ Partnership to Kim for $280,000.The inside basis of all partnership assets was $600,000 at the time of the sale.If the partnership makes a § 754 election,it will record a $40,000 step-up in the basis of the partnership assets,and the step-up will be attributed solely to Kim.

(True/False)

4.8/5 (39)

Toni's basis in her partnership interest was $60,000,including her $50,000 share of partnership liabilities.The partnership decides to liquidate,and after repaying all liabilities,distributes all remaining assets proportionately to the partners.Toni receives $20,000 cash and accounts receivable with a $12,000 basis and a $14,000 fair market value to the partnership.What gain or loss does Toni recognize,and what is her basis in the accounts receivable?

(Multiple Choice)

4.7/5 (35)

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-Step up

(Short Answer)

4.9/5 (41)

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

-Recaptured receivables

(Short Answer)

4.8/5 (34)

Tim receives a proportionate nonliquidating distribution from the RST Partnership when the basis of his interest is $60,000.The distribution consists of cash of $40,000 and inventory with a partnership basis of $30,000 and fair market value of $35,000.As a result of this distribution,Tim recognizes a $10,000 gain and takes a $30,000 basis in the inventory.

(True/False)

4.8/5 (34)

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

-Substantially appreciated inventory

(Short Answer)

4.9/5 (34)

Sarah owns a 30% interest in the capital and profits of the STP Partnership.Immediately before she receives a proportionate nonliquidating distribution from STP,the basis of her partnership interest is $25,000.The distribution consists of $20,000 in cash and land with a fair market value of $40,000.STP's adjusted basis in the land immediately before the distribution is $30,000.As a result of the distribution,Sarah recognizes a gain of $35,000 and her basis in the land is $40,000.

(True/False)

5.0/5 (39)

Greg has a 20% capital and profits interest in the calendar-year GDJ Partnership.His adjusted basis for his partnership interest on September 1 of the current year is $300,000.On that date,the partnership liquidates and makes a proportionate distribution of the following assets to Greg.

a.Calculate Greg's recognized gain or loss on the liquidating distribution, if any.

a. change if the partnership also distributed a chair to Greg? Assume the chair has a $500 adjusted basis (FMV is $800) to the partnership.

b.How would your answer to

a.Calculate Greg's recognized gain or loss on the liquidating distribution, if any.

a. change if the partnership also distributed a chair to Greg? Assume the chair has a $500 adjusted basis (FMV is $800) to the partnership.

b.How would your answer to

(Essay)

4.7/5 (30)

Match the following statements with the best match from the choices below. Note: Choice K may be used more than once.

a.Terminates the partner's interest in the partnership.

b.Ordinary income-producing items.

c.An unrealized receivable.

d.Cash, then inventory and unrealized receivables, then other assets.

e.Cash basis accounts receivable, for example.

f.Fair market value exceeds 120% of basis.

g.Changes the partner's or the partnership's ordinary income potential.

h.Any partnership assets other than cash, capital, or § 1231 assets.

i.Does not eliminate the partner's interest in the partnership.

j.A distribution of all partnership hot assets.

k.No correct match provided.

-Hot assets

(Short Answer)

4.9/5 (31)

Susan is a one-fourth limited partner in the SJ Partnership in which capital is not a material income-producing factor.Partnership assets consist of land (value of $100,000,basis of $80,000),accounts receivable (value of $100,000,basis of $0)and cash of $200,000.SJ distributes $100,000 of the cash to Susan in liquidation of her interest.Susan's basis in the partnership interest was $70,000 immediately before the distribution.Susan recognizes $25,000 of ordinary income,and a $5,000 capital gain on the distribution,and the partnership cannot claim a deduction for the $25,000 Susan recognizes as ordinary income.

(True/False)

5.0/5 (36)

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-Unstated goodwill

(Short Answer)

4.9/5 (31)

Match the following statements with the best match from the choices below. Note: Choice M may be used more than once.

a.Includes the partner's share of partnership liabilities.

b.Could result from sale of a partnership interest for less than the partner's share of the inside basis of assets.

c.Liquidation payments from this type of partnership are always § 736(b) payments.

d.Could arise if a distribution results in gain to the distributee partner.

e.May be a § 736(a) payment.

f.May receive § 736(a) payments.

g.Sale of more than 50% in less than 12 months.

h.Liquidation payments from this type of partnership may include § 736(a) payments.

i.A § 736(b) payment.

j.Adjustment designed to bring inside and outside bases into balance.

k.Partnership asset basis is at least $250,000 > FMV.

l.Would result if the partner contributes appreciated property to the partnership.

m.No correct match is provided.

-General partner

(Short Answer)

4.7/5 (45)

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below.

a.A payment for the partner's share of partnership income under § 736(a).

b.A payment for the partner's share of partnership property under § 736(b).

c.The payment includes both a § 736(a) and a § 736(b) element.

-Inventory with a basis of $10,000 and a fair market value of $15,000.

(Short Answer)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)