Deck 9: Interest Rate and Currency Swaps

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

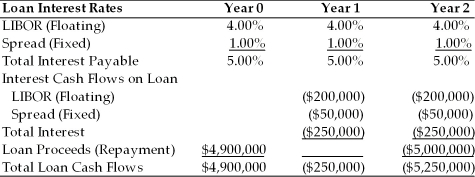

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. Polaris could have locked in the future interest rate payments by using

A)a forward rate agreement.

B)an interest rate future.

C)an interest rate swap.

D)any of the above

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. Polaris could have locked in the future interest rate payments by using

A)a forward rate agreement.

B)an interest rate future.

C)an interest rate swap.

D)any of the above

Question

Question

Question

Question

Question

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)4.00%

B)4.50%

C)5.25%

D)5.60%

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)4.00%

B)4.50%

C)5.25%

D)5.60%

Question

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What is the all-in-cost (i.e., the internal rate of return)of the Polaris loan including the LIBOR rate, fixed spread and upfront fee?

A)4.00%

B)5.00%

C)5.53%

D)6.09%

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What is the all-in-cost (i.e., the internal rate of return)of the Polaris loan including the LIBOR rate, fixed spread and upfront fee?

A)4.00%

B)5.00%

C)5.53%

D)6.09%

Question

Question

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What portion of the cost of the loan is at risk of changing?

A)the LIBOR rate

B)the spread

C)the upfront fee

D)all of the above

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What portion of the cost of the loan is at risk of changing?

A)the LIBOR rate

B)the spread

C)the upfront fee

D)all of the above

Question

Question

Question

Question

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)5.25%

B)5.50%

C)6.09%

D)6.58%

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)5.25%

B)5.50%

C)6.09%

D)6.58%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/53

Play

Full screen (f)

Deck 9: Interest Rate and Currency Swaps

1

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Choosing strategy #2 will

A)guarantee the lowest average annual rate over the next three years.

B)eliminate credit risk but retain repricing risk.

C)maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

D)preclude the possibility of sharing in lower interest rates over the three-year period.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Choosing strategy #2 will

A)guarantee the lowest average annual rate over the next three years.

B)eliminate credit risk but retain repricing risk.

C)maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

D)preclude the possibility of sharing in lower interest rates over the three-year period.

eliminate credit risk but retain repricing risk.

2

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Choosing strategy #3 will

A)guarantee the lowest average annual rate over the next three years.

B)eliminate credit risk but retain repricing risk.

C)maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

D)preclude the possibility of sharing in lower interest rates over the three-year period.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Choosing strategy #3 will

A)guarantee the lowest average annual rate over the next three years.

B)eliminate credit risk but retain repricing risk.

C)maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

D)preclude the possibility of sharing in lower interest rates over the three-year period.

maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

3

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Which strategy (strategies)will eliminate credit risk?

A)Strategy #1

B)Strategy #2

C)Strategy #3

D)Strategy #1 and #2

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Which strategy (strategies)will eliminate credit risk?

A)Strategy #1

B)Strategy #2

C)Strategy #3

D)Strategy #1 and #2

Strategy #1 and #2

4

The Federal Funds rate is the most common reference rate for international interest rate calculations.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

5

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. After the fact, under which set of circumstances would you prefer strategy #1? (Assume your firm is borrowing money.)

A)Your credit rating stayed the same and interest rates went up.

B)Your credit rating stayed the same and interest rates went down.

C)Your credit rating improved and interest rates went down.

D)Not enough information to make a judgment.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. After the fact, under which set of circumstances would you prefer strategy #1? (Assume your firm is borrowing money.)

A)Your credit rating stayed the same and interest rates went up.

B)Your credit rating stayed the same and interest rates went down.

C)Your credit rating improved and interest rates went down.

D)Not enough information to make a judgment.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

6

The most widely used reference rate for standardized quotations, loan agreements, or financial derivative valuations is the ________.

A)Federal Reserve Discount rate

B)federal funds rate

C)LIBOR

D)one-year U.S. Treasury Bill

A)Federal Reserve Discount rate

B)federal funds rate

C)LIBOR

D)one-year U.S. Treasury Bill

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

7

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. After the fact, under which set of circumstances would you prefer strategy #2? (Assume your firm is borrowing money.)

A)Your credit rating stayed the same and interest rates went up.

B)Your credit rating stayed the same and interest rates went down.

C)Your credit rating improved and interest rates went down.

D)Not enough information to make a judgment.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. After the fact, under which set of circumstances would you prefer strategy #2? (Assume your firm is borrowing money.)

A)Your credit rating stayed the same and interest rates went up.

B)Your credit rating stayed the same and interest rates went down.

C)Your credit rating improved and interest rates went down.

D)Not enough information to make a judgment.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

8

The following would be an example of a policy, not a goal.

A)Management shall minimize the firm's overall weighted average cost of capital.

B)Management shall maximize shareholder's wealth.

C)Management will not write uncovered options.

D)Management will hire only happy employees.

A)Management shall minimize the firm's overall weighted average cost of capital.

B)Management shall maximize shareholder's wealth.

C)Management will not write uncovered options.

D)Management will hire only happy employees.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

9

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. If your firm felt very confident that interest rates would fall or, at worst, remain at current levels, and were very confident about the firm's credit rating for the next 10 years, which strategy would you likely choose? (Assume your firm is borrowing money.)

A)Strategy #3

B)Strategy #2

C)Strategy #1

D)Strategy #1, #2, or #3, you are indifferent among the choices.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. If your firm felt very confident that interest rates would fall or, at worst, remain at current levels, and were very confident about the firm's credit rating for the next 10 years, which strategy would you likely choose? (Assume your firm is borrowing money.)

A)Strategy #3

B)Strategy #2

C)Strategy #1

D)Strategy #1, #2, or #3, you are indifferent among the choices.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

10

As a management tool, a ________ is a rule, but a ________ is an objective.

A)policy; goal

B)goal; policy

C)FIBOR; GIBOR

D)none of the above

A)policy; goal

B)goal; policy

C)FIBOR; GIBOR

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following is NOT true regarding a corporate policy?

A)A policy is intended to limit or restrict management actions.

B)Policies make management decision-making more difficult in potentially harmful situations.

C)A policy is intended to restrict some subjective management decision-making.

D)A policy is intended to establish operating guidelines independently of staff.

A)A policy is intended to limit or restrict management actions.

B)Policies make management decision-making more difficult in potentially harmful situations.

C)A policy is intended to restrict some subjective management decision-making.

D)A policy is intended to establish operating guidelines independently of staff.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

12

________ is the possibility that the borrower's credit worthiness is reclassified by the lender at the time of renewing credit. ________ is the risk of changes in interest rates charged at the time a financial contract rate is set.

A)Credit risk; Interest rate risk

B)Repricing risk; Credit risk

C)Interest rate risk; Credit risk

D)Credit risk; Repricing risk

A)Credit risk; Interest rate risk

B)Repricing risk; Credit risk

C)Interest rate risk; Credit risk

D)Credit risk; Repricing risk

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

13

The single largest interest rate risk of a firm is ________.

A)interest sensitive securities

B)debt service

C)dividend payments

D)accounts payable

A)interest sensitive securities

B)debt service

C)dividend payments

D)accounts payable

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

14

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Choosing strategy #1 will

A)guarantee the lowest average annual rate over the next three years.

B)eliminate credit risk but retain repricing risk.

C)maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

D)preclude the possibility of sharing in lower interest rates over the three-year period.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. Choosing strategy #1 will

A)guarantee the lowest average annual rate over the next three years.

B)eliminate credit risk but retain repricing risk.

C)maintain the possibility of lower interest costs, but maximizes the combined credit and repricing risks.

D)preclude the possibility of sharing in lower interest rates over the three-year period.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

15

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. After the fact, under which set of circumstances would you prefer strategy #3? (Assume your firm is borrowing money.)

A)Your credit rating stayed the same and interest rates went up.

B)Your credit rating stayed the same and interest rates went down.

C)Your credit rating improved and interest rates went down.

D)Not enough information to make a judgment.

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. After the fact, under which set of circumstances would you prefer strategy #3? (Assume your firm is borrowing money.)

A)Your credit rating stayed the same and interest rates went up.

B)Your credit rating stayed the same and interest rates went down.

C)Your credit rating improved and interest rates went down.

D)Not enough information to make a judgment.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

16

LIBOR is an acronym for

A)Latest Interest Being Offered Rate.

B)Large International Bank Offered Rate.

C)Least Interest Bearing: Official Rate.

D)London Interbank Offered Rate.

A)Latest Interest Being Offered Rate.

B)Large International Bank Offered Rate.

C)Least Interest Bearing: Official Rate.

D)London Interbank Offered Rate.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

17

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #3 is (Assume your firm is borrowing money.)

A)that interest rates might go down or that your credit rating might improve.

B)that interest rates might go up or that your credit rating might improve.

C)that interest rates might go up or that your credit rating might get worse.

D)none of the above

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #3 is (Assume your firm is borrowing money.)

A)that interest rates might go down or that your credit rating might improve.

B)that interest rates might go up or that your credit rating might improve.

C)that interest rates might go up or that your credit rating might get worse.

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

18

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #2 is (Assume your firm is borrowing money.)

A)that interest rates might go down or that your credit rating might improve.

B)that interest rates might go up or that your credit rating might improve.

C)that interest rates might go up or that your credit rating might get worse.

D)none of the above

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

Refer to Instruction 9.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #2 is (Assume your firm is borrowing money.)

A)that interest rates might go down or that your credit rating might improve.

B)that interest rates might go up or that your credit rating might improve.

C)that interest rates might go up or that your credit rating might get worse.

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

19

Credit risk is the risk of changes in interest rates charged (earned)at the time a financial rate is reset.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

20

A ________ rate is the rate of interest used in a standardized quotation, loan agreement, or financial derivative valuation.

A)reference rate

B)central rate

C)benchmark rate

D)none of the above

A)reference rate

B)central rate

C)benchmark rate

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

21

Interest rate futures are relatively unpopular among financial managers because of their relative illiquidity and their difficulty of use.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

22

A basis point is one-tenth of one percent.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

23

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. Polaris could have locked in the future interest rate payments by using

A)a forward rate agreement.

B)an interest rate future.

C)an interest rate swap.

D)any of the above

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. Polaris could have locked in the future interest rate payments by using

A)a forward rate agreement.

B)an interest rate future.

C)an interest rate swap.

D)any of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

24

A/an ________ is a contract to lock in today interest rates over a given period of time.

A)forward rate agreement

B)interest rate future

C)interest rate swap

D)none of the above

A)forward rate agreement

B)interest rate future

C)interest rate swap

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

25

An agreement to swap a fixed interest payment for a floating interest payment would be considered a/an ________.

A)currency swap

B)forward swap

C)interest rate swap

D)none of the above

A)currency swap

B)forward swap

C)interest rate swap

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

26

The financial manager of a firm has a variable rate loan outstanding. If she wishes to protect the firm against an unfavorable increase in interest rates she could

A)sell an interest rate futures contract of a similar maturity to the loan.

B)buy an interest rate futures contract of a similar maturity to the loan.

C)swap the adjustable rate loan for another of a different maturity.

D)none of the above

A)sell an interest rate futures contract of a similar maturity to the loan.

B)buy an interest rate futures contract of a similar maturity to the loan.

C)swap the adjustable rate loan for another of a different maturity.

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

27

Unlike the situation with exchange rate risk, there is no uncertainty on the part of management for shareholder preferences regarding interest rate risk. Shareholders prefer that managers hedge interest rate risk rather than having shareholders diversify away such risk through portfolio diversification.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

28

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)4.00%

B)4.50%

C)5.25%

D)5.60%

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)4.00%

B)4.50%

C)5.25%

D)5.60%

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

29

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What is the all-in-cost (i.e., the internal rate of return)of the Polaris loan including the LIBOR rate, fixed spread and upfront fee?

A)4.00%

B)5.00%

C)5.53%

D)6.09%

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What is the all-in-cost (i.e., the internal rate of return)of the Polaris loan including the LIBOR rate, fixed spread and upfront fee?

A)4.00%

B)5.00%

C)5.53%

D)6.09%

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

30

An interbank-traded contract to buy or sell interest rate payments on a notional principal is called a/an ________.

A)forward rate agreement

B)interest rate future

C)interest rate swap

D)none of the above

A)forward rate agreement

B)interest rate future

C)interest rate swap

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

31

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What portion of the cost of the loan is at risk of changing?

A)the LIBOR rate

B)the spread

C)the upfront fee

D)all of the above

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. What portion of the cost of the loan is at risk of changing?

A)the LIBOR rate

B)the spread

C)the upfront fee

D)all of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

32

A firm with variable-rate debt that expects interest rates to rise may engage in a swap agreement to

A)pay fixed-rate interest and receive floating rate interest.

B)pay floating rate and receive fixed rate.

C)pay fixed rate and receive fixed rate.

D)pay floating rate and receive floating rate.

A)pay fixed-rate interest and receive floating rate interest.

B)pay floating rate and receive fixed rate.

C)pay fixed rate and receive fixed rate.

D)pay floating rate and receive floating rate.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

33

Historically, interest rate movements have shown less variability and greater stability than exchange rate movements.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

34

A firm with fixed-rate debt that expects interest rates to fall may engage in a swap agreement to

A)pay fixed-rate interest and receive floating rate interest.

B)pay floating rate and receive fixed rate.

C)pay fixed rate and receive fixed rate.

D)pay floating rate and receive floating rate.

A)pay fixed-rate interest and receive floating rate interest.

B)pay floating rate and receive fixed rate.

C)pay fixed rate and receive fixed rate.

D)pay floating rate and receive floating rate.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

35

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)5.25%

B)5.50%

C)6.09%

D)6.58%

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

Refer to Table 9.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

A)5.25%

B)5.50%

C)6.09%

D)6.58%

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

36

An agreement to exchange interest payments based on a fixed payment for those based on a variable rate (or vice versa)is known as a/an ________.

A)forward rate agreement

B)interest rate future

C)interest rate swap

D)none of the above

A)forward rate agreement

B)interest rate future

C)interest rate swap

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

37

An agreement to swap the currencies of a debt service obligation would be termed a/an ________.

A)currency swap

B)forward swap

C)interest rate swap

D)none of the above

A)currency swap

B)forward swap

C)interest rate swap

D)none of the above

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following would be considered an example of a currency swap?

A)Exchanging a dollar interest obligation for a British pound obligation.

B)Exchanging a eurodollar interest obligation for a dollar obligation.

C)Exchanging a eurodollar interest obligation for a British pound obligation.

D)All of the above are examples of a currency swap.

A)Exchanging a dollar interest obligation for a British pound obligation.

B)Exchanging a eurodollar interest obligation for a dollar obligation.

C)Exchanging a eurodollar interest obligation for a British pound obligation.

D)All of the above are examples of a currency swap.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

39

The interest rate swap strategy of a firm with fixed rate debt and that expects rates to go up is to

A)do nothing.

B)pay floating and receive fixed.

C)receive floating and pay fixed.

D)none of the above.

A)do nothing.

B)pay floating and receive fixed.

C)receive floating and pay fixed.

D)none of the above.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

40

The potential exposure that any individual firm bears that the second party to any financial contract will be unable to fulfill its obligations under the contract is called ________.

A)interest rate risk

B)credit risk

C)counterparty risk

D)clearinghouse risk

A)interest rate risk

B)credit risk

C)counterparty risk

D)clearinghouse risk

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

41

Swap agreements replace existing loan agreements.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

42

A firm enters into an agreement to ________ British pounds and ________ U.S. dollars. If the dollar appreciates vs. the pound the firm will realize an accounting profit on the swap transaction.

A)pay; receive

B)receive; pay

C)pay; pay

D)receive; receive

A)pay; receive

B)receive; pay

C)pay; pay

D)receive; receive

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

43

________ is the potential exposure any individual firm bears that the second party to any financial contract will be unable to fulfill its obligation under the contract's specifications.

A)Inflation risk

B)Counterparty risk

C)Purchasing power risk

D)Swap agreement risk

A)Inflation risk

B)Counterparty risk

C)Purchasing power risk

D)Swap agreement risk

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

44

Your firm is faced with paying a variable rate debt obligation with the expectation that interest rates are likely to go up. Identify two strategies using interest rate futures and interest rate swaps that could reduce the risk to the firm.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

45

How does counterparty risk influence a firm's decision to trade exchange-traded derivatives rather than over-the-counter derivatives?

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

46

Swap rates are derived from the yield curves in each major currency.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

47

A firm entering into a currency or interest rate swap agreement retains ultimate responsibility for the timely servicing of its own debt obligations.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

48

A swap agreement may involve currencies or interest rates, but never both.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

49

Counterparty risk is greater for exchange-traded derivatives than for over-the-counter derivatives.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

50

A firm enters into a swap agreement to pay euros and receive U.S. dollars. If the euro appreciates the firm will record a loss on the swap for accounting purposes.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following is an unlikely reason for firms to participate in the swap market?

A)To replace cash flows scheduled in an undesired currency with cash flows in a desired currency.

B)Firms may raise capital in one currency but desire to repay it in another currency.

C)Firms desire to swap fixed and variable payment or receipt of funds.

D)All of the above are likely reasons for a firm to enter the swap market.

A)To replace cash flows scheduled in an undesired currency with cash flows in a desired currency.

B)Firms may raise capital in one currency but desire to repay it in another currency.

C)Firms desire to swap fixed and variable payment or receipt of funds.

D)All of the above are likely reasons for a firm to enter the swap market.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

52

Johnson Industries is currently paying a variable rate loan and desires greater certainty with regard to their loan payments. Refinancing is currently not available so they decide to pursue an interest rate swap agreement. Which of the following will help Johnson stabilize their anticipated cash outflows? Enter into an agreement to:

A)Receive LIBOR and pay a quoted rate.

B)Receive a quoted rate and pay LIBOR + 1.50%.

C)Receive LIBOR and pay LIBOR + 1.50%.

D)None of the above will help Johnson Industries pay a fixed amount for their obligations.

A)Receive LIBOR and pay a quoted rate.

B)Receive a quoted rate and pay LIBOR + 1.50%.

C)Receive LIBOR and pay LIBOR + 1.50%.

D)None of the above will help Johnson Industries pay a fixed amount for their obligations.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

53

Some of the world's largest and most financially sound firms may borrow at variable rates less than LIBOR.

Unlock Deck

Unlock for access to all 53 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 53 flashcards in this deck.