Exam 9: Interest Rate and Currency Swaps

Exam 1: Globalization and the Multinational Enterprise33 Questions

Exam 2: Financial Goals and Corporate Governance36 Questions

Exam 3: The International Monetary System39 Questions

Exam 4: The Balance of Payments49 Questions

Exam 5: Current Multinational Financial Challenges: the Credit Crisis of 2007-200930 Questions

Exam 6: The Foreign Exchange Market50 Questions

Exam 7: International Parity Conditions54 Questions

Exam 8: Foreign Currency Derivatives56 Questions

Exam 9: Interest Rate and Currency Swaps53 Questions

Exam 10: Foreign Exchange Rate Determination and Forecasting34 Questions

Exam 11: Transaction Exposure39 Questions

Exam 12: Operating Exposure47 Questions

Exam 13: Translation Exposure41 Questions

Exam 14: The Global Cost and Availability of Capital46 Questions

Exam 15: Sourcing Equity Globally38 Questions

Exam 16: Sourcing Debt Globally41 Questions

Exam 17: International Portfolio Theory and Diversification36 Questions

Exam 18: Foreign Direct Investment Theory and Political Risk56 Questions

Exam 19: Multinational Capital Budgeting32 Questions

Exam 20: Multinational Tax Management38 Questions

Exam 21: Working Capital Management42 Questions

Exam 22: International Trade Finance39 Questions

Select questions type

The interest rate swap strategy of a firm with fixed rate debt and that expects rates to go up is to

Free

(Multiple Choice)

4.8/5  (38)

(38)

Correct Answer: Verified

Verified

A

The most widely used reference rate for standardized quotations, loan agreements, or financial derivative valuations is the ________.

Free

(Multiple Choice)

4.8/5 (45)

Correct Answer:Verified

C

A firm enters into an agreement to ________ British pounds and ________ U.S. dollars. If the dollar appreciates vs. the pound the firm will realize an accounting profit on the swap transaction.

Free

(Multiple Choice)

4.8/5 (30)

Correct Answer:Verified

A

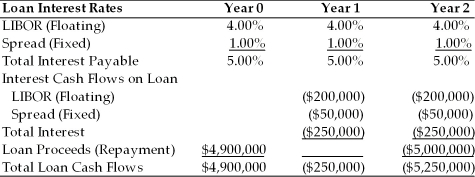

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%  -Refer to Table 9.1. Polaris could have locked in the future interest rate payments by using

-Refer to Table 9.1. Polaris could have locked in the future interest rate payments by using

(Multiple Choice)

4.8/5 (42)

How does counterparty risk influence a firm's decision to trade exchange-traded derivatives rather than over-the-counter derivatives?

(Essay)

4.8/5 (41)

The Federal Funds rate is the most common reference rate for international interest rate calculations.

(True/False)

4.9/5 (48)

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 9.1. If the LIBOR rate jumps to 5.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

(Multiple Choice)

4.8/5 (39)

The financial manager of a firm has a variable rate loan outstanding. If she wishes to protect the firm against an unfavorable increase in interest rates she could

(Multiple Choice)

4.9/5 (45)

Counterparty risk is greater for exchange-traded derivatives than for over-the-counter derivatives.

(True/False)

4.8/5 (43)

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 9.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #3 is (Assume your firm is borrowing money.)

(Multiple Choice)

4.9/5 (32)

Which of the following would be considered an example of a currency swap?

(Multiple Choice)

4.8/5 (42)

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 9.1. The risk of strategy #1 is that interest rates might go down or that your credit rating might improve. The risk of strategy #2 is (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (36)

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 9.1. If your firm felt very confident that interest rates would fall or, at worst, remain at current levels, and were very confident about the firm's credit rating for the next 10 years, which strategy would you likely choose? (Assume your firm is borrowing money.)

(Multiple Choice)

4.8/5 (36)

A swap agreement may involve currencies or interest rates, but never both.

(True/False)

4.9/5 (35)

Which of the following is an unlikely reason for firms to participate in the swap market?

(Multiple Choice)

4.7/5 (42)

Instruction 9.1:

For the following problem(s), consider these debt strategies being considered by a corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year period.

-Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

-Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to be reset annually. The current LIBOR rate is 3.50%

-Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit annually. The current one-year rate is 5%.

-Refer to Instruction 9.1. Choosing strategy #2 will

(Multiple Choice)

4.7/5 (30)

________ is the possibility that the borrower's credit worthiness is reclassified by the lender at the time of renewing credit. ________ is the risk of changes in interest rates charged at the time a financial contract rate is set.

(Multiple Choice)

4.9/5 (42)

TABLE 9.1

Use the information for Polaris Corporation to answer following question(s).

Polaris is taking out a $5,000,000 two-year loan at a variable rate of LIBOR plus 1.00%. The LIBOR rate will be reset each year at an agreed upon date. The current LIBOR rate is 4.00% per year. The loan has an upfront fee of 2.00%

-Refer to Table 9.1. If the LIBOR rate falls to 3.00% after the first year what will be the all-in-cost (i.e. the internal rate of return)for Polaris for the entire loan?

(Multiple Choice)

4.9/5 (39)

A firm with variable-rate debt that expects interest rates to rise may engage in a swap agreement to

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)