Deck 8: Accounting for Joint Arrangements

Full screen (f)

Question

On July 1 20X3,a parent entity,Delta Ltd acquired 20% of the share capital of Rimfire Ltd and the power to exert significant influence over that company's decision making processes for a cash outlay of $1,800,000.At relevant dates,the shareholders' equity of Rimfire Ltd at June 30 was (amounts in thousands):  Additional information:

Additional information:

I)No dividends have been paid by Rimfire Ltd out of pre-acquisition profits.

II)At June 30 20X6,Delta Ltd held inventories,which had been supplied by Rimfire Ltd at a mark-up of $100,000.

III)During the year ended June 30 20X7,Rimfire Ltd earned a profit for the year of $600,000 (after income tax of $200,000)and paid a dividend of $250,000.

IV)The income tax rate was 30%.

V)Any goodwill on acquisition has not been impaired since acquisition.

In the consolidated balance sheet at June 30 20X7 of the group controlled by Delta Ltd,the investment in Rimfire Ltd would be reported at an amount of:

A) $2,150,000

B) $2,164,000

C) $2,200,000

D) None of the above.

Additional information:I)No dividends have been paid by Rimfire Ltd out of pre-acquisition profits.

II)At June 30 20X6,Delta Ltd held inventories,which had been supplied by Rimfire Ltd at a mark-up of $100,000.

III)During the year ended June 30 20X7,Rimfire Ltd earned a profit for the year of $600,000 (after income tax of $200,000)and paid a dividend of $250,000.

IV)The income tax rate was 30%.

V)Any goodwill on acquisition has not been impaired since acquisition.

In the consolidated balance sheet at June 30 20X7 of the group controlled by Delta Ltd,the investment in Rimfire Ltd would be reported at an amount of:

A) $2,150,000

B) $2,164,000

C) $2,200,000

D) None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

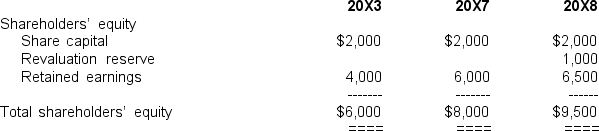

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands):  Other information:

Other information:

I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,493,000

C) $2,693,000

D) None of the above.

Other information:I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,493,000

C) $2,693,000

D) None of the above.

Question

On July 1 20X3,Heroic Ltd acquired a 30% interest in Manfred Ltd,and the power to exert significant influence over that company,for a cash consideration of $2,000,000.At the date of acquisition,the net assets of Manfred Ltd approximated fair value.At respective dates,the shareholders' equity of Manfred Ltd was as follows (amounts in thousands):  Other information

Other information

I)Heroic Ltd was not a parent entity

II)At June 30 20X7,Heroic Ltd had held inventories which had been supplied by Manfred Ltd at a mark-up of $50,000.The income tax rate was 30%.

III)Due to worsening operating difficulties in Manfred Ltd,at June 30 20X8,the recoverable amount of the investment was estimated to be $1,200,000.

In the balance sheet of Heroic Ltd as at June 30 20X8,the carrying amount of the investment in Manfred Ltd would be:

A) $1,700,000

B) $1,200,000

C) $1,215,000

D) None of the above.

Other informationI)Heroic Ltd was not a parent entity

II)At June 30 20X7,Heroic Ltd had held inventories which had been supplied by Manfred Ltd at a mark-up of $50,000.The income tax rate was 30%.

III)Due to worsening operating difficulties in Manfred Ltd,at June 30 20X8,the recoverable amount of the investment was estimated to be $1,200,000.

In the balance sheet of Heroic Ltd as at June 30 20X8,the carrying amount of the investment in Manfred Ltd would be:

A) $1,700,000

B) $1,200,000

C) $1,215,000

D) None of the above.

Question

Question

Question

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands):  Other information:

Other information:

I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,000,000

C) $2,700,000

D) None of the above.

Other information:I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,000,000

C) $2,700,000

D) None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

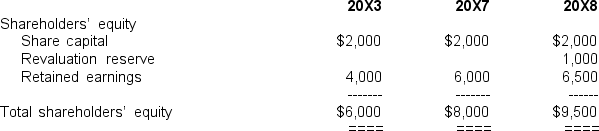

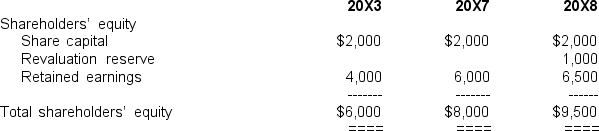

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands):  Other information:

Other information:

I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Other information:I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Question

Question

Question

Question

Question

Question

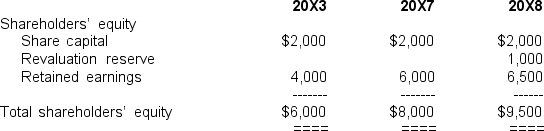

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands):  Other information:

Other information:

I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

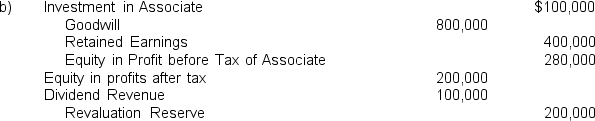

In preparing the consolidated financial statements for the year ended June 30 20X8,the journal adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Other information:I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the journal adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/44

Play

Full screen (f)

Deck 8: Accounting for Joint Arrangements

1

On July 1 20X3,a parent entity,Delta Ltd acquired 20% of the share capital of Rimfire Ltd and the power to exert significant influence over that company's decision making processes for a cash outlay of $1,800,000.At relevant dates,the shareholders' equity of Rimfire Ltd at June 30 was (amounts in thousands): Additional information:

I)No dividends have been paid by Rimfire Ltd out of pre-acquisition profits.

II)At June 30 20X6,Delta Ltd held inventories,which had been supplied by Rimfire Ltd at a mark-up of $100,000.

III)During the year ended June 30 20X7,Rimfire Ltd earned a profit for the year of $600,000 (after income tax of $200,000)and paid a dividend of $250,000.

IV)The income tax rate was 30%.

V)Any goodwill on acquisition has not been impaired since acquisition.

In the consolidated balance sheet at June 30 20X7 of the group controlled by Delta Ltd,the investment in Rimfire Ltd would be reported at an amount of:

A) $2,150,000

B) $2,164,000

C) $2,200,000

D) None of the above.

Additional information:I)No dividends have been paid by Rimfire Ltd out of pre-acquisition profits.

II)At June 30 20X6,Delta Ltd held inventories,which had been supplied by Rimfire Ltd at a mark-up of $100,000.

III)During the year ended June 30 20X7,Rimfire Ltd earned a profit for the year of $600,000 (after income tax of $200,000)and paid a dividend of $250,000.

IV)The income tax rate was 30%.

V)Any goodwill on acquisition has not been impaired since acquisition.

In the consolidated balance sheet at June 30 20X7 of the group controlled by Delta Ltd,the investment in Rimfire Ltd would be reported at an amount of:

A) $2,150,000

B) $2,164,000

C) $2,200,000

D) None of the above.

C

2

On November 1 20X6,a parent entity Helios Ltd acquired 25% (500,000 shares)of the share capital of Havers Ltd and the power to significantly influence the operating and financial policies of that company for $4,000,000 cash.In the period from the date of acquisition to June 30 20X7,Havers Ltd earned a profit for the period of $500,000 (after tax of $200,000)and declared a dividend of $100,000.At June 30 20X7,Helios Ltd recognised its equity in the dividend.At June 30 20X7,the quoted market value of the shares in Havers was $10 per share.At June 30 20X7,in the separate balance sheet of Helios Ltd and in the consolidated balance sheet of the group controlled by Helios Ltd,the investment in Havers Ltd would be reported as:

A) $4,000,000 and $4,100,000 respectively.

B) $5,000,000 and $4,100,000 respectively.

C) $5,000,000 and $5,100,000 respectively.

D) None of the above.

A) $4,000,000 and $4,100,000 respectively.

B) $5,000,000 and $4,100,000 respectively.

C) $5,000,000 and $5,100,000 respectively.

D) None of the above.

A

3

An investee is considered to be an associate of an investor if:

A) The investor has the power to participate in the financial and operating decisions of the investee.

B) The investor has the power to participate in either or both the financial and operating decisions of the investee.

C) The investor has the power to participate in or jointly control the financial and operating decisions of the investee.

D) All of the above.

A) The investor has the power to participate in the financial and operating decisions of the investee.

B) The investor has the power to participate in either or both the financial and operating decisions of the investee.

C) The investor has the power to participate in or jointly control the financial and operating decisions of the investee.

D) All of the above.

A

4

The use of the equity method primarily provides information to the investor in relation to:

A) profit performance of the investee

B) valuation of the investment

C) Dividend policy of the investee

D) none of the above

A) profit performance of the investee

B) valuation of the investment

C) Dividend policy of the investee

D) none of the above

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is not an indication that an investor has the power to exert significant influence over an investee company?

A) Representation of the investor on the investee's Board of Directors.

B) Participation by the investor in the investee's policy-making processes.

C) The investee's technological dependency on the investor involving the investor providing the investee with essential technical information.

D) None of the above.

A) Representation of the investor on the investee's Board of Directors.

B) Participation by the investor in the investee's policy-making processes.

C) The investee's technological dependency on the investor involving the investor providing the investee with essential technical information.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

6

Indicia of the position that an investor does not have the power to significantly influence the operating,investment and financial policies of an investee include:

A) Representation on the investee's Board of Directors by the investor or by a party nominated by the investor through which the investor is able to directly or indirectly participate in investee policy decision-making.

B) Operational interrelationships between the investor and the investee.

C) Technological interrelationships between the investor and the investee.

D) None of the above.

A) Representation on the investee's Board of Directors by the investor or by a party nominated by the investor through which the investor is able to directly or indirectly participate in investee policy decision-making.

B) Operational interrelationships between the investor and the investee.

C) Technological interrelationships between the investor and the investee.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

7

On November 1 20X6,a parent entity Midstream Ltd acquired 25% of the share capital of Delta Ltd and the power to significantly influence the operating and financial policies of that company for $5,000,000 cash.In the period from the date of acquisition to June 30 20X7,Delta Ltd earned a profit for the period of $400,000 (after tax of $200,000)and declared a dividend of $200,000.At June 30 20X7,Midstream Ltd recognised its equity in the dividend.For the year ended June 30 20X7,in the separate income statement of Midstream Ltd and in the consolidated income statement of the group controlled by Midstream Ltd,the equity in the profit before tax of Delta Ltd would be reported as:

A) $200,000 and $100,000 respectively

B) $50,000 and $150,000 respectively

C) $50,000 and $120,000 respectively

D) None of the above.

A) $200,000 and $100,000 respectively

B) $50,000 and $150,000 respectively

C) $50,000 and $120,000 respectively

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

8

A has significant influence over B but does not have any share ownership in B:

A) B is an associate of A

B) B is not an associate of A

C) B is a subsidiary of A

D) none of the above

A) B is an associate of A

B) B is not an associate of A

C) B is a subsidiary of A

D) none of the above

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements more adequately reflects the current accounting position in regards to accounting for an associate entity?

A) The reporting by the investor of dividend revenue under the cost method is perceived to be an adequate indicator of investment performance in the case of a significant investment.

B) Even with representation on the associate's Board of Directors, an investor cannot have the power to manipulate its reported earnings (through participation in the dividend policy decisions of the associate) and thus present a misleading picture of its earnings performance.

C) Because of the varying dividend policies of investees it is unlikely that dividend income will provide a reliable indicator of the investment performance of any associate.

D) None of the above.

A) The reporting by the investor of dividend revenue under the cost method is perceived to be an adequate indicator of investment performance in the case of a significant investment.

B) Even with representation on the associate's Board of Directors, an investor cannot have the power to manipulate its reported earnings (through participation in the dividend policy decisions of the associate) and thus present a misleading picture of its earnings performance.

C) Because of the varying dividend policies of investees it is unlikely that dividend income will provide a reliable indicator of the investment performance of any associate.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

10

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands): Other information:

I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,493,000

C) $2,693,000

D) None of the above.

Other information:I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,493,000

C) $2,693,000

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

11

On July 1 20X3,Heroic Ltd acquired a 30% interest in Manfred Ltd,and the power to exert significant influence over that company,for a cash consideration of $2,000,000.At the date of acquisition,the net assets of Manfred Ltd approximated fair value.At respective dates,the shareholders' equity of Manfred Ltd was as follows (amounts in thousands): Other information

I)Heroic Ltd was not a parent entity

II)At June 30 20X7,Heroic Ltd had held inventories which had been supplied by Manfred Ltd at a mark-up of $50,000.The income tax rate was 30%.

III)Due to worsening operating difficulties in Manfred Ltd,at June 30 20X8,the recoverable amount of the investment was estimated to be $1,200,000.

In the balance sheet of Heroic Ltd as at June 30 20X8,the carrying amount of the investment in Manfred Ltd would be:

A) $1,700,000

B) $1,200,000

C) $1,215,000

D) None of the above.

Other informationI)Heroic Ltd was not a parent entity

II)At June 30 20X7,Heroic Ltd had held inventories which had been supplied by Manfred Ltd at a mark-up of $50,000.The income tax rate was 30%.

III)Due to worsening operating difficulties in Manfred Ltd,at June 30 20X8,the recoverable amount of the investment was estimated to be $1,200,000.

In the balance sheet of Heroic Ltd as at June 30 20X8,the carrying amount of the investment in Manfred Ltd would be:

A) $1,700,000

B) $1,200,000

C) $1,215,000

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

12

The holding of 20% or more of the voting power in an investee entity by an investor is a presumptive test that the investee is an associate of the investor.The application of this presumptive test means that:

A) Where an investor acquires a 20% equity stakeholding in an investee the investee is an associate of the investor.

B) Where an investor acquires a 20% equity stakeholding in an investee, in the absence of evidence to the contrary, the investee will be treated as an associate of the investor.

C) An investor must have an equity stakeholding in an investee of at least 20% before the investee can be treated as an associate of the investor.

D) None of the above.

A) Where an investor acquires a 20% equity stakeholding in an investee the investee is an associate of the investor.

B) Where an investor acquires a 20% equity stakeholding in an investee, in the absence of evidence to the contrary, the investee will be treated as an associate of the investor.

C) An investor must have an equity stakeholding in an investee of at least 20% before the investee can be treated as an associate of the investor.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

13

In equity accounting the investment in Rimfire Ltd in the year ended June 30 20X7,the adjustment to recognise the equity of Delta Ltd in Rimfire Ltd at June 30 20X6 would be:

A) Debit Investment in Associate $300,000 Credit Retained Earnings 1.7.X7 $300,000.

B) Debit Investment in Associate $316,000 Credit Retained Earnings 1.7.X7 $316,000.

C) Debit Investment in Associate $$394,000 Credit Retained Earnings 1.7.X7 $394,000.

D) None of the above.

A) Debit Investment in Associate $300,000 Credit Retained Earnings 1.7.X7 $300,000.

B) Debit Investment in Associate $316,000 Credit Retained Earnings 1.7.X7 $316,000.

C) Debit Investment in Associate $$394,000 Credit Retained Earnings 1.7.X7 $394,000.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

14

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands): Other information:

I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,000,000

C) $2,700,000

D) None of the above.

Other information:I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

A) $2,500,000

B) $2,000,000

C) $2,700,000

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

15

Even though an investee may be an associate of an investor,if the shares of that associate are traded in an active market,AASB 139 Financial Instruments: requires investments in that investee to be reported at:

A) A market valuation.

B) Value in use.

C) A valuation made by an independent valuer.

D) None of the above.

A) A market valuation.

B) Value in use.

C) A valuation made by an independent valuer.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

16

Investor Ltd holds 25% of the voting shares of Investee Ltd.Another company holds the remaining 75%:

A) Investee Ltd is an associate of Investor Ltd

B) Investee Ltd is not an associate of Investor Ltd

C) It is probable that Investee Ltd is not an associate of Investor Ltd

D) none of the above

A) Investee Ltd is an associate of Investor Ltd

B) Investee Ltd is not an associate of Investor Ltd

C) It is probable that Investee Ltd is not an associate of Investor Ltd

D) none of the above

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

17

If an investment in an associate entity were to be accounted for using the cost method,the investment is initially recognised at its cost of acquisition and:

A) All dividends declared in the post-acquisition period are treated as a recovery of the investment.

B) If the shares in the associate are traded in an active market, market value increments or decrements are recognised as gains or losses at each reporting date.

C) Dividends declared from pre-acquisition profits are deducted from the carrying amount of the investment, even if these dividends are declared subsequent to acquisition.

D) None of the above.

A) All dividends declared in the post-acquisition period are treated as a recovery of the investment.

B) If the shares in the associate are traded in an active market, market value increments or decrements are recognised as gains or losses at each reporting date.

C) Dividends declared from pre-acquisition profits are deducted from the carrying amount of the investment, even if these dividends are declared subsequent to acquisition.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

18

Indicia of an investor's incapacity to exert significant influence over the policy making decisions of an investee include:

A) The existence of a small group of "non-investor" shareholders representing the majority of voting power in the investee.

B) The investor attempting to gain, but not gaining, Board representation.

C) The investor attempting to gain, but not gaining, the financial information necessary to calculate its equity in the fair value of the investee's net assets at the date of acquisition, or its equity in the post-acquisition earnings of the investee.

D) All of the above.

A) The existence of a small group of "non-investor" shareholders representing the majority of voting power in the investee.

B) The investor attempting to gain, but not gaining, Board representation.

C) The investor attempting to gain, but not gaining, the financial information necessary to calculate its equity in the fair value of the investee's net assets at the date of acquisition, or its equity in the post-acquisition earnings of the investee.

D) All of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

19

On January 1 20X7,a parent entity Emborough Ltd acquired 20% of the share capital of Bernborough Ltd and the power to significantly influence the operating and financial policies of that company for $4,500,000 cash.In the period from the date of acquisition to June 30 20X7,Bernborough Ltd earned a profit for the period of $400,000 (after tax of $200,000),recognised a post-acquisition asset revaluation increment of $500,000 (deferred tax liability $100,000)and declared a dividend of $200,000.At June 30 20X7,Emborough Ltd recognised its equity in the dividend. In the consolidated balance sheet as at June 30 20X7 of the group controlled by Emborough Ltd,the investment in the associate would be reported at an amount of:

A) $4,620,000

B) $4,500,000

C) $4,680,000

D) None of the above.

A) $4,620,000

B) $4,500,000

C) $4,680,000

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

20

A owns 40% of B and 30% of C.Both B and C own 15% of D each.There is a presumption of significant influence by A over:

A) B and C

B) B only

C) B, C and D

D) no significant influence over any of B,C and D

A) B and C

B) B only

C) B, C and D

D) no significant influence over any of B,C and D

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

21

The equity accounting method must be applied by all applicable reporting entities

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

22

Discuss whether equity accounting profits are 'realised' from the viewpoint of the investor

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

23

Accounting for investment in associates by parent entities using the equity method will be done:

A) in the parent entity financial statements

B) in the consolidated financial statements

C) in either the parent entity or consolidated financial statements

D) none of the above

A) in the parent entity financial statements

B) in the consolidated financial statements

C) in either the parent entity or consolidated financial statements

D) none of the above

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

24

The balance of an investment in associate account cannot be negative

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

25

Unrealised profits on both upstream and downstream transactions between an investor and an associate are to be eliminated under accounting standard AASB128 Investments in Associates.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

26

The equity carrying amount of an investment will always be equal to the investor's proportional share of the net assets of the investee.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

27

Goodwill arising on an equity investment is not required to be separately tested for impairment.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

28

Ownership of 20% or more of voting shares leads to a presumption of significant influence.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

29

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands): Other information:

I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Other information:I)On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

30

A gain on bargain purchase of an equity investment will be excluded from the investor's share of profit or loss of the associate.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

31

On January 1 20X7,a parent entity Emborough Ltd acquired 20% of the share capital of Bernborough Ltd and the power to participate in the operating and financial policies of that company for $4,500,000 cash.In the period from the date of acquisition to June 30 20X7,Bernborough Ltd earned a profit for the period of $400,000 (after tax of $200,000),recognised a post-acquisition asset revaluation increment of $500,000 (deferred tax liability $100,000)and declared a dividend of $200,000.At June 30 20X7,Emborough Ltd recognised its equity in the dividend. In respect of the increase in the investment recognised in the consolidated balance sheet at June 30 20X7 of the group controlled by Emborough Ltd,a deferred tax liability would be recognised of:

A) $36,000

B) $60,000

C) No deferred tax liability would be recognised since the increase is not a temporary difference.

D) None of the above.

A) $36,000

B) $60,000

C) No deferred tax liability would be recognised since the increase is not a temporary difference.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

32

Where an associate makes profits subsequent to the investor's acquisition of the equity investment,a deferred tax liability will be required to be recognised.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

33

When preparing the equity accounting adjustments in the consolidated financial statements,losses on the investment will be accounted for:

A) for the current year only

B) for all prior years

C) for current year and all prior years

D) not accounted for

A) for the current year only

B) for all prior years

C) for current year and all prior years

D) not accounted for

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

34

Investors that are not parent entities must record all equity entries in their own records

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

35

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands): Other information:

I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the journal adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Other information:I)Delville Wood Ltd acquired its 20% investment on July 1 20X3 for a cash outlay of $2,000,000.

II)During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III)At June 30 20X7,Delville Wood Ltd held inventories which had been supplied by Harnham Hill Ltd at a mark-up of $100,000.

IV)At June 30 20X8,a subsidiary of Delville Wood Ltd held inventories that had been supplied by Harnham Hill Ltd at a mark-up of $50,000.

V)During the year ended June 30 20X8,Delville Wood Ltd charged Harnham Hill Ltd with a management fee of $100,000 for administration services.

VI)In the income statement of Harnham Hill Ltd was interest revenue of $50,000 which had been earned on a loan made to a subsidiary of Delville Wood Ltd.

VII)The income tax rate was 30%.

VIII.Any goodwill element in the cost of the investment had not been impaired in the investment period.

In preparing the consolidated financial statements for the year ended June 30 20X8,the journal adjustment to recognise the equity of Delville Wood Ltd in its associate would be:

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

36

There is no formal definition of terms 'investor' and 'investee' under current accounting standards

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

37

It is possible that different entities can respectively exert control and significant influence over an investee entity

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

38

Assume the same data as in Question 4-27.In July 20X8,Calpurnia Ltd acquired an additional 20% of the share capital of Portia Ltd and the power to control that company.In preparing the consolidated financial statements of the group controlled by Portia Ltd for the year ended June 30 20X8:

A) An adjustment would be made to recognise the equity of Calpurnia Ltd in the retained earnings at June 30 20X7 of Portia Ltd.

B) No adjustments would be required since the consolidation process would automatically recognise the equity of Calpurnia Ltd in the retained earnings at June 30 20X7 of Portia Ltd.

C) Adjustment would be required to reverse the recognition of the deferred tax liability at June 30 20X7 and the minority interest recognised on that adjustment.

D) None of the above.

A) An adjustment would be made to recognise the equity of Calpurnia Ltd in the retained earnings at June 30 20X7 of Portia Ltd.

B) No adjustments would be required since the consolidation process would automatically recognise the equity of Calpurnia Ltd in the retained earnings at June 30 20X7 of Portia Ltd.

C) Adjustment would be required to reverse the recognition of the deferred tax liability at June 30 20X7 and the minority interest recognised on that adjustment.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

39

During the year ended June 30 20X7,a parent entity Rimfire Ltd sold merchandise to its 30% owned associate Neville Ltd at a mark-up of $100,000.At June 30 20X7,Neville Ltd still held one-half of this merchandise in inventory.Because of marketing problems,Neville Ltd had written down the merchandise by $20,000.The income tax rate was 30%.In the consolidated financial statements prepared for the year ended June 30 20X7 of the group controlled by Rimfire Ltd,the effect of the unsold merchandise at June 30 20X7 would be:

A) Rimfire Ltd would recognise an unrealised profit of $21,000 after tax and report merchandise inventory at an amount $30,000 less than that at which the merchandise is carried in the balance sheet of Neville Ltd.

B) Rimfire Ltd would recognise an unrealised profit of $6,300 after tax and report merchandise inventory at an amount $21,000 less than that at which the merchandise is carried in the balance sheet of Neville Ltd.

C) Rimfire Ltd would recognise an unrealised profit of $6,300 after tax and report the inventory of merchandise at an amount $20,000 less than the amount at which the merchandise is carried in the statement of financial position of Neville Ltd.

D) None of the above.

A) Rimfire Ltd would recognise an unrealised profit of $21,000 after tax and report merchandise inventory at an amount $30,000 less than that at which the merchandise is carried in the balance sheet of Neville Ltd.

B) Rimfire Ltd would recognise an unrealised profit of $6,300 after tax and report merchandise inventory at an amount $21,000 less than that at which the merchandise is carried in the balance sheet of Neville Ltd.

C) Rimfire Ltd would recognise an unrealised profit of $6,300 after tax and report the inventory of merchandise at an amount $20,000 less than the amount at which the merchandise is carried in the statement of financial position of Neville Ltd.

D) None of the above.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

40

An investment in an associate company will initially be recorded at fair value

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

41

Explain the following statement:

'When reconciling the investor's interest in an associate's net assets to the equity accounted carrying amount of the investment in the investor's financial statements,the unimpaired balance of goodwill will be a reconciling item'

'When reconciling the investor's interest in an associate's net assets to the equity accounted carrying amount of the investment in the investor's financial statements,the unimpaired balance of goodwill will be a reconciling item'

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

42

Discuss the different identification and disclosure requirements for goodwill purchased as part of an investment in a subsidiary and an associate.

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

43

Discuss the basis of the equity carrying amount of the investment

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

44

What is the rationale for the extensive note disclosure requirements under AASB128?

Unlock Deck

Unlock for access to all 44 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 44 flashcards in this deck.