Exam 8: Accounting for Joint Arrangements

Exam 1: Text Objectives and Introduction to Consolidation28 Questions

Exam 2: Principles of Consolidation42 Questions

Exam 3: Fair Value Adjustments and Tax Effects34 Questions

Exam 4: Intra-Group Transactions36 Questions

Exam 5: Non-Controlling Interest37 Questions

Exam 6: Partly-Owned Subsidiaries: Indirect Non-Controlling Interest27 Questions

Exam 7: Consolidated Cash Flow Statements25 Questions

Exam 8: Accounting for Joint Arrangements44 Questions

Exam 9: Accounting for Associates and Joint Ventures: the Equity Method37 Questions

Exam 10: Translation and Consolidation of Foreign Currency Financial Statements31 Questions

Exam 11: Segment Reporting by Diversified Entities27 Questions

Select questions type

The holding of 20% or more of the voting power in an investee entity by an investor is a presumptive test that the investee is an associate of the investor.The application of this presumptive test means that:

Free

(Multiple Choice)

4.7/5  (36)

(36)

Correct Answer: Verified

Verified

B

The balance of an investment in associate account cannot be negative

Free

(True/False)

4.9/5 (39)

Correct Answer:Verified

True

There is no formal definition of terms 'investor' and 'investee' under current accounting standards

Free

(True/False)

4.9/5 (31)

Correct Answer:Verified

True

On January 1 20X7,a parent entity Emborough Ltd acquired 20% of the share capital of Bernborough Ltd and the power to participate in the operating and financial policies of that company for $4,500,000 cash.In the period from the date of acquisition to June 30 20X7,Bernborough Ltd earned a profit for the period of $400,000 (after tax of $200,000),recognised a post-acquisition asset revaluation increment of $500,000 (deferred tax liability $100,000)and declared a dividend of $200,000.At June 30 20X7,Emborough Ltd recognised its equity in the dividend. In respect of the increase in the investment recognised in the consolidated balance sheet at June 30 20X7 of the group controlled by Emborough Ltd,a deferred tax liability would be recognised of:

(Multiple Choice)

5.0/5 (37)

When preparing the equity accounting adjustments in the consolidated financial statements,losses on the investment will be accounted for:

(Multiple Choice)

4.8/5 (42)

Ownership of 20% or more of voting shares leads to a presumption of significant influence.

(True/False)

4.9/5 (35)

An investee is considered to be an associate of an investor if:

(Multiple Choice)

4.8/5 (31)

Unrealised profits on both upstream and downstream transactions between an investor and an associate are to be eliminated under accounting standard AASB128 Investments in Associates.

(True/False)

4.8/5 (41)

During the year ended June 30 20X7,a parent entity Rimfire Ltd sold merchandise to its 30% owned associate Neville Ltd at a mark-up of $100,000.At June 30 20X7,Neville Ltd still held one-half of this merchandise in inventory.Because of marketing problems,Neville Ltd had written down the merchandise by $20,000.The income tax rate was 30%.In the consolidated financial statements prepared for the year ended June 30 20X7 of the group controlled by Rimfire Ltd,the effect of the unsold merchandise at June 30 20X7 would be:

(Multiple Choice)

4.9/5 (29)

A owns 40% of B and 30% of C.Both B and C own 15% of D each.There is a presumption of significant influence by A over:

(Multiple Choice)

4.8/5 (37)

What is the rationale for the extensive note disclosure requirements under AASB128?

(Essay)

4.9/5 (43)

Which of the following statements more adequately reflects the current accounting position in regards to accounting for an associate entity?

(Multiple Choice)

4.8/5 (34)

A has significant influence over B but does not have any share ownership in B:

(Multiple Choice)

4.9/5 (40)

On July 1 20X3,Heroic Ltd acquired a 30% interest in Manfred Ltd,and the power to exert significant influence over that company,for a cash consideration of $2,000,000.At the date of acquisition,the net assets of Manfred Ltd approximated fair value.At respective dates,the shareholders' equity of Manfred Ltd was as follows (amounts in thousands):  Other information

I.Heroic Ltd was not a parent entity

II.At June 30 20X7,Heroic Ltd had held inventories which had been supplied by Manfred Ltd at a mark-up of $50,000.The income tax rate was 30%.

III.Due to worsening operating difficulties in Manfred Ltd,at June 30 20X8,the recoverable amount of the investment was estimated to be $1,200,000.

In the balance sheet of Heroic Ltd as at June 30 20X8,the carrying amount of the investment in Manfred Ltd would be:

Other information

I.Heroic Ltd was not a parent entity

II.At June 30 20X7,Heroic Ltd had held inventories which had been supplied by Manfred Ltd at a mark-up of $50,000.The income tax rate was 30%.

III.Due to worsening operating difficulties in Manfred Ltd,at June 30 20X8,the recoverable amount of the investment was estimated to be $1,200,000.

In the balance sheet of Heroic Ltd as at June 30 20X8,the carrying amount of the investment in Manfred Ltd would be:

(Multiple Choice)

4.9/5 (32)

On November 1 20X6,a parent entity Midstream Ltd acquired 25% of the share capital of Delta Ltd and the power to significantly influence the operating and financial policies of that company for $5,000,000 cash.In the period from the date of acquisition to June 30 20X7,Delta Ltd earned a profit for the period of $400,000 (after tax of $200,000)and declared a dividend of $200,000.At June 30 20X7,Midstream Ltd recognised its equity in the dividend.For the year ended June 30 20X7,in the separate income statement of Midstream Ltd and in the consolidated income statement of the group controlled by Midstream Ltd,the equity in the profit before tax of Delta Ltd would be reported as:

(Multiple Choice)

4.7/5 (28)

In equity accounting the investment in Rimfire Ltd in the year ended June 30 20X7,the adjustment to recognise the equity of Delta Ltd in Rimfire Ltd at June 30 20X6 would be:

(Multiple Choice)

4.9/5 (31)

Discuss whether equity accounting profits are 'realised' from the viewpoint of the investor

(Essay)

5.0/5 (28)

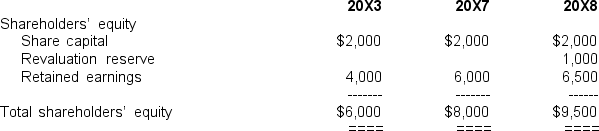

The following statements of shareholders' equity were prepared for Harnham Hill Ltd,a 20% owned associate of the parent entity Delville Wood Ltd,at June 30 (amounts in thousands):  Other information:

I.On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II.During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III.Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

Other information:

I.On July 1 20X3,Delville Wood Ltd acquired its 20% investment for a cash outlay of $2,000,000.

II.During the year ended June 30 20X8,Harnham Hill Ltd earned a profit of $1,400,000 before tax (income tax expense $400,000)and paid a dividend of $500,000.

III.Any goodwill element in the cost of the investment had not been impaired in the investment period.

At June 30 20X8,the carrying amount of the investment in the consolidated balance sheet of the group controlled by Delville Wood Ltd was:

(Multiple Choice)

4.8/5 (34)

Goodwill arising on an equity investment is not required to be separately tested for impairment.

(True/False)

4.9/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)