Deck 18: Employee Expenses and Deferred Compensation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

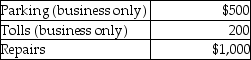

West's adjusted gross income was $90,000.During the current year he incurred and paid the following:  Assuming he can itemize deductions,how much should West claim as miscellaneous itemized deductions (after limitations have been applied)?

Assuming he can itemize deductions,how much should West claim as miscellaneous itemized deductions (after limitations have been applied)?

A)$2,700

B)$4,500

C)$3,500

D)$5,300

Assuming he can itemize deductions,how much should West claim as miscellaneous itemized deductions (after limitations have been applied)?A)$2,700

B)$4,500

C)$3,500

D)$5,300

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Shane,an employee,makes the following gifts,none of which are reimbursed:  What amount of the gifts is deductible before application of the 2% of AGI floor for miscellaneous itemized deductions?

What amount of the gifts is deductible before application of the 2% of AGI floor for miscellaneous itemized deductions?

A)$125

B)$150

C)$75

D)$178

What amount of the gifts is deductible before application of the 2% of AGI floor for miscellaneous itemized deductions?A)$125

B)$150

C)$75

D)$178

Question

Question

Austin incurs $3,600 for business meals while traveling for his employer,Tex,Inc.Austin is reimbursed in full by Tex pursuant to an accountable plan.What amounts can Austin and Tex deduct?

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Jordan,an employee,drove his auto 20,000 miles this year,15,000 to meetings with clients and 5,000 for commuting and personal use. The cost of operating the auto for the year was as follows:  Jordan submitted appropriate reports to his employer,and the employer paid a reimbursement of $ .50 per mile. Jordan has used the actual cost method in the past. Jordan's AGI is $50,000. What is Jordan's deduction for the use of the auto after application of all relevant limitations?

Jordan submitted appropriate reports to his employer,and the employer paid a reimbursement of $ .50 per mile. Jordan has used the actual cost method in the past. Jordan's AGI is $50,000. What is Jordan's deduction for the use of the auto after application of all relevant limitations?

A)$1,500

B)$500

C)$1,000

D)$8,000

Jordan submitted appropriate reports to his employer,and the employer paid a reimbursement of $ .50 per mile. Jordan has used the actual cost method in the past. Jordan's AGI is $50,000. What is Jordan's deduction for the use of the auto after application of all relevant limitations?A)$1,500

B)$500

C)$1,000

D)$8,000

Question

Bill obtained a new job in Boston.He incurred the following moving expenses:  Assuming Bill is entitled to deduct moving expenses,what is the amount of the deduction?

Assuming Bill is entitled to deduct moving expenses,what is the amount of the deduction?

A)$2,600

B)$4,600

C)$6,300

D)$6,800

Assuming Bill is entitled to deduct moving expenses,what is the amount of the deduction?A)$2,600

B)$4,600

C)$6,300

D)$6,800

Question

Question

Steven is a representative for a textbook publishing company.Steven attends a convention which will also be attended by many potential customers.During the week of the convention,Steven incurs the following costs in entertaining potential customers.  Having recently been to a company seminar on the new tax laws,Steven makes sure that business is discussed at the various dinners,and that the entertainment is on the same day as the meetings with customers.Steven is reimbursed $2,000 by his employer under an accountable plan.Steven's AGI for the year is $50,000,and while he itemizes deductions,he has no other miscellaneous itemized deductions.What is the amount and character of Steven's deduction after any limitations?

Having recently been to a company seminar on the new tax laws,Steven makes sure that business is discussed at the various dinners,and that the entertainment is on the same day as the meetings with customers.Steven is reimbursed $2,000 by his employer under an accountable plan.Steven's AGI for the year is $50,000,and while he itemizes deductions,he has no other miscellaneous itemized deductions.What is the amount and character of Steven's deduction after any limitations?

A)$500 from AGI

B)$500 for AGI

C)$2,000 from AGI

D)$2,000 for AGI

Having recently been to a company seminar on the new tax laws,Steven makes sure that business is discussed at the various dinners,and that the entertainment is on the same day as the meetings with customers.Steven is reimbursed $2,000 by his employer under an accountable plan.Steven's AGI for the year is $50,000,and while he itemizes deductions,he has no other miscellaneous itemized deductions.What is the amount and character of Steven's deduction after any limitations?A)$500 from AGI

B)$500 for AGI

C)$2,000 from AGI

D)$2,000 for AGI

Question

Ron obtained a new job and moved from Houston to Washington.He incurred the following moving expenses:  Assuming Ron is eligible to deduct his moving expenses,what is the amount of the deduction?

Assuming Ron is eligible to deduct his moving expenses,what is the amount of the deduction?

A)$3,529

B)$6,600

C)$9,179

D)$3,984

Assuming Ron is eligible to deduct his moving expenses,what is the amount of the deduction?A)$3,529

B)$6,600

C)$9,179

D)$3,984

Question

Chelsea,who is self-employed,drove her automobile a total of 20,000 business miles in 2014.This represents about 75% of the auto's use. She has receipts as follows:  Chelsea has an AGI for the year of $50,000.Chelsea uses the standard mileage rate method. After application of any relevant floors or other limitations,she can deduct

Chelsea has an AGI for the year of $50,000.Chelsea uses the standard mileage rate method. After application of any relevant floors or other limitations,she can deduct

A)$10,900.

B)$11,900.

C)$11,750.

D)$12,900.

Chelsea has an AGI for the year of $50,000.Chelsea uses the standard mileage rate method. After application of any relevant floors or other limitations,she can deductA)$10,900.

B)$11,900.

C)$11,750.

D)$12,900.

Question

Brittany,who is an employee,drove her automobile a total of 20,000 business miles in 2014.This represents about 75% of the auto's use. She has receipts as follows:  Brittany's AGI for the year of $50,000,and her employer does not provide any reimbursement.She uses the standard mileage rate method. After application of any relevant floors or other limitations,Brittany can deduct

Brittany's AGI for the year of $50,000,and her employer does not provide any reimbursement.She uses the standard mileage rate method. After application of any relevant floors or other limitations,Brittany can deduct

A)$10,900.

B)$11,900.

C)$10,750.

D)$12,900.

Brittany's AGI for the year of $50,000,and her employer does not provide any reimbursement.She uses the standard mileage rate method. After application of any relevant floors or other limitations,Brittany can deductA)$10,900.

B)$11,900.

C)$10,750.

D)$12,900.

Question

Question

Question

Joe is a self-employed tax attorney who frequently entertains his clients at his country club.Joe's club expenses include the following:  Assuming the business meals and entertainment qualify as deductible entertainment expenses,Joe may deduct

Assuming the business meals and entertainment qualify as deductible entertainment expenses,Joe may deduct

A)$2,000.

B)$4,700.

C)$5,300.

D)$4,000.

Assuming the business meals and entertainment qualify as deductible entertainment expenses,Joe may deductA)$2,000.

B)$4,700.

C)$5,300.

D)$4,000.

Question

Rajiv,a self-employed consultant,drove his auto 20,000 miles this year,15,000 to meetings with clients and 5,000 for commuting and personal use. The cost of operating the auto for the year was as follows:  Rajiv's AGI is $100,000 before considering the auto costs. Rajiv has used the actual cost method in the past. What is Rajiv's deduction for the use of the auto after application of all relevant limitations?

Rajiv's AGI is $100,000 before considering the auto costs. Rajiv has used the actual cost method in the past. What is Rajiv's deduction for the use of the auto after application of all relevant limitations?

A)$8,325

B)$9,000

C)$6,325

D)$7,000

Rajiv's AGI is $100,000 before considering the auto costs. Rajiv has used the actual cost method in the past. What is Rajiv's deduction for the use of the auto after application of all relevant limitations?A)$8,325

B)$9,000

C)$6,325

D)$7,000

Question

Question

Edward incurs the following moving expenses:  The employer reimburses Edward for the full $10,000.What is the amount to be reported as income by Edward?

The employer reimburses Edward for the full $10,000.What is the amount to be reported as income by Edward?

A)$0

B)$4,000

C)$6,000

D)$10,000

The employer reimburses Edward for the full $10,000.What is the amount to be reported as income by Edward?A)$0

B)$4,000

C)$6,000

D)$10,000

Question

Donald takes a new job and moves to a new residence.The distances are as follows:  By how many miles does the move exceed the minimum distance requirement for the moving expense deduction?

By how many miles does the move exceed the minimum distance requirement for the moving expense deduction?

A)12 miles

B)20 miles

C)62 miles

D)none of the above

By how many miles does the move exceed the minimum distance requirement for the moving expense deduction?A)12 miles

B)20 miles

C)62 miles

D)none of the above

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/135

Play

Full screen (f)

Deck 18: Employee Expenses and Deferred Compensation

1

Incremental expenses of an additional night's lodging and additional day's meals that are incurred to obtain "excursion" air fare rates with respect to employees whose business travel extends over Saturday night are not deductible business expenses.

False

2

Jason,who lives in New Jersey,owns several apartment buildings in Baltimore.His travel expenses to Baltimore to inspect his property are tax deductible.

True

3

Gambling losses are miscellaneous itemized deductions subject to the 2% of AGI floor.

False

4

Commuting to and from a job location is a deductible expense.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

5

Unreimbursed employee business expenses are deductions for AGI.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

6

The deduction for unreimbursed transportation expenses for employees is subject to the 2% of AGI floor.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

7

Travel expenses for a taxpayer's spouse are deductible if the spouse is an employee,the travel is for a bona fide purpose,and the expenses are otherwise deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

8

A nondeductible floor of 2% of AGI is imposed on unreimbursed employee business expenses,investment expenses,and many other miscellaneous itemized deductions such as tax preparation fees.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

9

Transportation expenses incurred to travel from one job to another are deductible if a taxpayer has more than one job.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

10

According to the IRS,a person's tax home is the location of the family residence regardless of the location of the taxpayer's principal place of employment.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

11

Personal travel expenses are deductible as miscellaneous itemized deductions subject to the 2% of AGI floor.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

12

Travel expenses related to foreign conventions are disallowed unless the meeting is directly related to the taxpayer's business or is employment related and it is reasonable for the meeting to be held outside of North America.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

13

If the purpose of a trip is primarily personal and only secondarily related to business,the transportation costs to and from the destination are deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

14

An employer-employee relationship exists where the employer has the right to control and direct the individual providing services with regard to the end result and the means by which the result is accomplished.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

15

Deferred compensation refers to methods of compensating employees based upon their current service where the benefits are deferred until future periods.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

16

Taxpayers may use the standard mileage rate method when five vehicles are used simultaneously for business.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

17

If an individual is self-employed,business-related expenses are deductions for AGI.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

18

Travel expenses related to temporary work assignments of one year or less are deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

19

If an individual is not "away from home," expenses related to local transportation are never deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

20

In determining whether travel expenses are deductible,a general rule is that if a person is reassigned for an indefinite period,the individual's tax home shifts to the new location and travel expenses are not deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

21

Dues paid to social or athletic clubs are deductible if they meet a primary-use test,requiring that more than 50% of the use of the facility be for business purposes.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

22

If an employee incurs business-related entertainment expenses that are fully reimbursed,it is the employer who is subject to the 50% limitation.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

23

In-home office expenses for an office used by the taxpayer for administrative or management activities of the taxpayer's trade or business are never deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

24

Generally,50% of the cost of business gifts is deductible up to $25 per donee per year.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

25

If the standard mileage rate is used in the first year,the actual expense method may not be used in future years.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

26

Kim currently lives in Buffalo and works in Rochester,a 60-mile commute each way. Kim accepts a new job in a town outside of Rochester,and the new commute is 75-miles each way. Kim decides the commute for the new job is too long,and she moves to Rochester. Kim is eligible to deduct her moving expenses.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

27

Educational expenses incurred by a bookkeeper for courses necessary to sit for the CPA exam are fully deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

28

An accountant takes her client to a hockey game following a business meeting. Because it is a playoff game,and the tickets were purchased that day,a premium was paid. The deduction for the tickets is limited to 50% of the face value.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

29

Educational expenses incurred by a CPA for courses necessary to meet continuing education requirements are fully deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

30

In addition to the general requirements for in-home office expenses,employees must also prove that the exclusive use of the office is for the convenience of the employer.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

31

A gift from an employee to his or her superior does not qualify as a business gift.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

32

A taxpayer goes out of town to a business convention. The 50% reduction applies to the cost of food,entertainment and transportation expenses.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

33

In-home office expenses which are not deductible in the year in which the costs were incurred due to limitations may be carried forward to subsequent years.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

34

A tax adviser takes a client to a major league hockey game following the conclusion of a meeting involving the signing of a major planning engagement.As it is not "directly related," the entertainment cannot be deductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

35

When a public school system requires advanced education for a teacher to continue employment,the teacher's expenses are a deductible education expense.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

36

Deductible moving expenses include the cost of moving household goods and personal effects as well as temporary living expenses.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

37

Self-employed individuals receive a for AGI deduction for 50% of entertainment expenses paid or incurred in the trade or business.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

38

In-home office expenses are deductible if the office is used exclusively on a regular basis as the principal place of business for any trade or business of the taxpayer.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

39

"Associated with" entertainment expenditures generally must occur on the same day that business is discussed.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

40

If an employee incurs travel expenditures and is fully reimbursed by the employer,neither the reimbursement nor the deduction is reported on the employee's tax return if reporting is pursuant to an accountable plan.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

41

The maximum tax deductible contribution to a Roth IRA in 2014 is $5,500 ($6,500 for a taxpayer age 50 or over).

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following statements regarding independent contractors and employees is true (ignore temporary provisions)?

A)Independent contractors pay Social Security and Medicare tax of 15.3%.

B)Employees must pay unemployment taxes.

C)Independent contractors and employees pay the same Social Security and Medicare tax rates.

D)Independent contractors deduct their business expenses "from AGI."

A)Independent contractors pay Social Security and Medicare tax of 15.3%.

B)Employees must pay unemployment taxes.

C)Independent contractors and employees pay the same Social Security and Medicare tax rates.

D)Independent contractors deduct their business expenses "from AGI."

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

43

All taxpayers are allowed to contribute funds to Health Savings Accounts to supplement their health insurance.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

44

In which of the following situations is the individual is an independent contractor rather than an employee?

A)a nurse who is directly supervised by doctors in an office

B)a computer programmer who is instructed as to what projects to undertake,programming language and format,and hours of work

C)a nurse who travels to several different patients.She sets her own hours and is responsible for the delivery of nursing care and end result

D)a teacher whose hours,classroom responsibilities,content and methods of instruction are established by the school

A)a nurse who is directly supervised by doctors in an office

B)a computer programmer who is instructed as to what projects to undertake,programming language and format,and hours of work

C)a nurse who travels to several different patients.She sets her own hours and is responsible for the delivery of nursing care and end result

D)a teacher whose hours,classroom responsibilities,content and methods of instruction are established by the school

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

45

West's adjusted gross income was $90,000.During the current year he incurred and paid the following: Assuming he can itemize deductions,how much should West claim as miscellaneous itemized deductions (after limitations have been applied)?

A)$2,700

B)$4,500

C)$3,500

D)$5,300

Assuming he can itemize deductions,how much should West claim as miscellaneous itemized deductions (after limitations have been applied)?A)$2,700

B)$4,500

C)$3,500

D)$5,300

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

46

An employer receives an immediate tax deduction for pension and profit-sharing contributions made on behalf of employees.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

47

Nonqualified deferred compensation plans can discriminate in favor of highly compensated executives.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

48

SIMPLE retirement plans allow a higher level of employer contributions than do SEP IRAs.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

49

Employees receiving nonqualified stock options recognize ordinary income at the grant date or exercise date if there is a readily ascertainable fair market value.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

50

A sole proprietor establishes a Keogh plan. The highest effective percentage of earned income she can contribute is 25 percent.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

51

The maximum tax deductible contribution to a traditional IRA in 2014 is $5,500 ($6,500 for a taxpayer age 50 or over).

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

52

Corporations issuing incentive stock options receive a tax deduction for compensation expense.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

53

Allison,who is single,incurred $4,000 for unreimbursed employee expenses,$10,000 for mortgage interest and real estate taxes on her home,and $500 for investment counseling fees.Allison's AGI is $80,000.Allison's allowable deductions from AGI are (after limitations have been applied)

A)$10,500.

B)$12,900.

C)$14,000.

D)$14,500.

A)$10,500.

B)$12,900.

C)$14,000.

D)$14,500.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

54

All of the following are allowed a "For AGI" deduction except:

A)Cora owns her own CPA firm and travels from Lafayette,LA.to Washington,D.C.to attend a tax conference.

B)Jennifer,who lives in Houston,is the owner or several apartment buildings in Salt Lake City and travels there to inspect and manage her investments.

C)Alan is self-employed and is away from home overnight on job-related business.

D)Alison is an employee who is required to travel to company facilities throughout the U.S.in the conduct of her management responsibilities.She is not reimbursed by her employer.

A)Cora owns her own CPA firm and travels from Lafayette,LA.to Washington,D.C.to attend a tax conference.

B)Jennifer,who lives in Houston,is the owner or several apartment buildings in Salt Lake City and travels there to inspect and manage her investments.

C)Alan is self-employed and is away from home overnight on job-related business.

D)Alison is an employee who is required to travel to company facilities throughout the U.S.in the conduct of her management responsibilities.She is not reimbursed by her employer.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

55

Ron is a university professor who accepts a visiting position at another university for six months and obtains a leave of absence from his current employer.Ron rents an apartment near the university and purchases his food. These living expenses incurred by Ron while visiting the university will be

A)deductible for AGI.

B)deductible from AGI,without application of a floor.

C)deductible from AGI,subject to the 2% of AGI floor.

D)nondeductible.

A)deductible for AGI.

B)deductible from AGI,without application of a floor.

C)deductible from AGI,subject to the 2% of AGI floor.

D)nondeductible.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

56

Gwen traveled to New York City on a business trip for her employer.Gwen spent 4 days in business meetings and conferences and then spent 2 days sightseeing in the area.Gwen's plane fare for the trip was $250.Meals cost $160 per day.Hotels and other incidental expenses amounted to $250 per day. Gwen was not reimbursed by her employer for any expenses.Her AGI for the year is $50,000 and she itemizes but has no other miscellaneous itemized deductions.Gwen may deduct (after limitations)

A)$570.

B)$890.

C)$1,890.

D)$1,570.

A)$570.

B)$890.

C)$1,890.

D)$1,570.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

57

Under a qualified pension plan,the employer's deduction is usually deferred until the employee recognizes income.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

58

In a defined contribution pension plan,fixed amounts are contributed based upon a specific formula and retirement benefits are based on the value of a participant's account at the time of retirement.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

59

A contributor may make a deductible contribution to a Coverdell Education Savings Account for a qualified designated beneficiary of up to $2,000.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

60

A qualified pension plan requires that employer-provided benefits must be 100 percent vested after five years of service.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

61

Shane,an employee,makes the following gifts,none of which are reimbursed: What amount of the gifts is deductible before application of the 2% of AGI floor for miscellaneous itemized deductions?

A)$125

B)$150

C)$75

D)$178

What amount of the gifts is deductible before application of the 2% of AGI floor for miscellaneous itemized deductions?A)$125

B)$150

C)$75

D)$178

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

62

Matt is a sales representative for a local company. He entertains customers as part of his job. During the current year he spends $3,000 on business entertainment. The company provides him an expense allowance of $2,000 under a nonaccountable plan. How will Matt treat the $2,000 partial reimbursement and the $3,000 entertainment expense?

A)He will deduct the $1,000 net expense as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

B)He will deduct $500 of the net expense as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

C)He will recognize $2,000 of income and deduct $3,000 as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

D)He will recognize $2,000 of income and deduct $1,500 as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

A)He will deduct the $1,000 net expense as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

B)He will deduct $500 of the net expense as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

C)He will recognize $2,000 of income and deduct $3,000 as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

D)He will recognize $2,000 of income and deduct $1,500 as a miscellaneous itemized deduction,subject to the 2% of AGI floor.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

63

Austin incurs $3,600 for business meals while traveling for his employer,Tex,Inc.Austin is reimbursed in full by Tex pursuant to an accountable plan.What amounts can Austin and Tex deduct?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

64

Sarah incurred employee business expenses of $5,000 consisting of $3,000 business meals and $2,000 customer entertainment.She provided an adequate accounting to her employer's accountable plan and received reimbursement for one-half of the total expenses.How much of the meals and entertainment will be deductible by Sarah without consideration of the 2% of AGI limit?

A)$0

B)$1,250

C)$2,500

D)$5,000

A)$0

B)$1,250

C)$2,500

D)$5,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

65

Alex is a self-employed dentist who operates a qualifying office in his home.Alex has $180,000 gross income from his practice and $160,000 of expenses directly related to the business,i.e.,non-home office expenses.Alex's allocable home office expenses for mortgage interest expenses and property taxes are $14,000 and other home office expenses are $9,000.What is Alex's total allowable home office deduction?

A)$9,000

B)$14,000

C)$20,000

D)$23,000

A)$9,000

B)$14,000

C)$20,000

D)$23,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

66

Jordan,an employee,drove his auto 20,000 miles this year,15,000 to meetings with clients and 5,000 for commuting and personal use. The cost of operating the auto for the year was as follows: Jordan submitted appropriate reports to his employer,and the employer paid a reimbursement of $ .50 per mile. Jordan has used the actual cost method in the past. Jordan's AGI is $50,000. What is Jordan's deduction for the use of the auto after application of all relevant limitations?

A)$1,500

B)$500

C)$1,000

D)$8,000

Jordan submitted appropriate reports to his employer,and the employer paid a reimbursement of $ .50 per mile. Jordan has used the actual cost method in the past. Jordan's AGI is $50,000. What is Jordan's deduction for the use of the auto after application of all relevant limitations?A)$1,500

B)$500

C)$1,000

D)$8,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

67

Bill obtained a new job in Boston.He incurred the following moving expenses: Assuming Bill is entitled to deduct moving expenses,what is the amount of the deduction?

A)$2,600

B)$4,600

C)$6,300

D)$6,800

Assuming Bill is entitled to deduct moving expenses,what is the amount of the deduction?A)$2,600

B)$4,600

C)$6,300

D)$6,800

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

68

All of the following may deduct education expenses except:

A)Richard is a self-employed dentist who incurs expenses to attend a convention on new techniques in oral surgery.

B)Paige is an accountant who incurs expenses to take a CPA exam review course.

C)Hope is a business executive who incurs expenses to pursue an MBA degree.

D)Marvin is a high school teacher who incurs expenses for education courses to meet new course requirements to maintain his job.

A)Richard is a self-employed dentist who incurs expenses to attend a convention on new techniques in oral surgery.

B)Paige is an accountant who incurs expenses to take a CPA exam review course.

C)Hope is a business executive who incurs expenses to pursue an MBA degree.

D)Marvin is a high school teacher who incurs expenses for education courses to meet new course requirements to maintain his job.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

69

Steven is a representative for a textbook publishing company.Steven attends a convention which will also be attended by many potential customers.During the week of the convention,Steven incurs the following costs in entertaining potential customers. Having recently been to a company seminar on the new tax laws,Steven makes sure that business is discussed at the various dinners,and that the entertainment is on the same day as the meetings with customers.Steven is reimbursed $2,000 by his employer under an accountable plan.Steven's AGI for the year is $50,000,and while he itemizes deductions,he has no other miscellaneous itemized deductions.What is the amount and character of Steven's deduction after any limitations?

A)$500 from AGI

B)$500 for AGI

C)$2,000 from AGI

D)$2,000 for AGI

Having recently been to a company seminar on the new tax laws,Steven makes sure that business is discussed at the various dinners,and that the entertainment is on the same day as the meetings with customers.Steven is reimbursed $2,000 by his employer under an accountable plan.Steven's AGI for the year is $50,000,and while he itemizes deductions,he has no other miscellaneous itemized deductions.What is the amount and character of Steven's deduction after any limitations?A)$500 from AGI

B)$500 for AGI

C)$2,000 from AGI

D)$2,000 for AGI

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

70

Ron obtained a new job and moved from Houston to Washington.He incurred the following moving expenses: Assuming Ron is eligible to deduct his moving expenses,what is the amount of the deduction?

A)$3,529

B)$6,600

C)$9,179

D)$3,984

Assuming Ron is eligible to deduct his moving expenses,what is the amount of the deduction?A)$3,529

B)$6,600

C)$9,179

D)$3,984

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

71

Chelsea,who is self-employed,drove her automobile a total of 20,000 business miles in 2014.This represents about 75% of the auto's use. She has receipts as follows: Chelsea has an AGI for the year of $50,000.Chelsea uses the standard mileage rate method. After application of any relevant floors or other limitations,she can deduct

A)$10,900.

B)$11,900.

C)$11,750.

D)$12,900.

Chelsea has an AGI for the year of $50,000.Chelsea uses the standard mileage rate method. After application of any relevant floors or other limitations,she can deductA)$10,900.

B)$11,900.

C)$11,750.

D)$12,900.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

72

Brittany,who is an employee,drove her automobile a total of 20,000 business miles in 2014.This represents about 75% of the auto's use. She has receipts as follows: Brittany's AGI for the year of $50,000,and her employer does not provide any reimbursement.She uses the standard mileage rate method. After application of any relevant floors or other limitations,Brittany can deduct

A)$10,900.

B)$11,900.

C)$10,750.

D)$12,900.

Brittany's AGI for the year of $50,000,and her employer does not provide any reimbursement.She uses the standard mileage rate method. After application of any relevant floors or other limitations,Brittany can deductA)$10,900.

B)$11,900.

C)$10,750.

D)$12,900.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

73

Norman traveled to San Francisco for four days on vacation,and while there spent another two days conducting business for his employer.Norman's plane fare for the trip was $500; meals cost $150 per day; hotels cost $300 per day; and a rental car cost $150 per day that was used for all six days.Norman was not reimbursed by his employer for any expenses.Norman's AGI for the year is $40,000 and he did not have any other miscellaneous itemized deductions.Norman may deduct (after limitations)

A)$250.

B)$800.

C)$1,050.

D)$1,200.

A)$250.

B)$800.

C)$1,050.

D)$1,200.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

74

Gayle,a doctor with significant investments in the stock market,traveled on a cruise ship to Bermuda. Investment specialists provided daily seminars which Gayle attended. The cost of the cruise for four days is $2,500.Gayle can deduct (before application of any floors)

A)$0.

B)$1,250.

C)$2,000.

D)$2,500.

A)$0.

B)$1,250.

C)$2,000.

D)$2,500.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

75

Joe is a self-employed tax attorney who frequently entertains his clients at his country club.Joe's club expenses include the following: Assuming the business meals and entertainment qualify as deductible entertainment expenses,Joe may deduct

A)$2,000.

B)$4,700.

C)$5,300.

D)$4,000.

Assuming the business meals and entertainment qualify as deductible entertainment expenses,Joe may deductA)$2,000.

B)$4,700.

C)$5,300.

D)$4,000.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

76

Rajiv,a self-employed consultant,drove his auto 20,000 miles this year,15,000 to meetings with clients and 5,000 for commuting and personal use. The cost of operating the auto for the year was as follows: Rajiv's AGI is $100,000 before considering the auto costs. Rajiv has used the actual cost method in the past. What is Rajiv's deduction for the use of the auto after application of all relevant limitations?

A)$8,325

B)$9,000

C)$6,325

D)$7,000

Rajiv's AGI is $100,000 before considering the auto costs. Rajiv has used the actual cost method in the past. What is Rajiv's deduction for the use of the auto after application of all relevant limitations?A)$8,325

B)$9,000

C)$6,325

D)$7,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

77

The following individuals maintained offices in their home: (1)Dr.Austin is a self-employed surgeon who performs surgery at four hospitals.He uses his home for administrative duties as he does not have an office in any of the hospitals.

(2)June,who is a self-employed plumber,earns her living in her customer's homes.She maintains an office at home where she bills clients and does other paperwork related to her plumbing business.

(3)Cassie,who is an employee of Montgomery Electrical,is provided an office at the work but does significant administrative work at home.Her employer does not require her to do extra work but she feels it is necessary.

Who is entitled to a home office deduction?

A)Dr Austin

B)Dr.Austin and June

C)Cassie and June

D)All of the taxpayers are entitled to a deduction.

(2)June,who is a self-employed plumber,earns her living in her customer's homes.She maintains an office at home where she bills clients and does other paperwork related to her plumbing business.

(3)Cassie,who is an employee of Montgomery Electrical,is provided an office at the work but does significant administrative work at home.Her employer does not require her to do extra work but she feels it is necessary.

Who is entitled to a home office deduction?

A)Dr Austin

B)Dr.Austin and June

C)Cassie and June

D)All of the taxpayers are entitled to a deduction.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

78

Edward incurs the following moving expenses: The employer reimburses Edward for the full $10,000.What is the amount to be reported as income by Edward?

A)$0

B)$4,000

C)$6,000

D)$10,000

The employer reimburses Edward for the full $10,000.What is the amount to be reported as income by Edward?A)$0

B)$4,000

C)$6,000

D)$10,000

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

79

Donald takes a new job and moves to a new residence.The distances are as follows: By how many miles does the move exceed the minimum distance requirement for the moving expense deduction?

A)12 miles

B)20 miles

C)62 miles

D)none of the above

By how many miles does the move exceed the minimum distance requirement for the moving expense deduction?A)12 miles

B)20 miles

C)62 miles

D)none of the above

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

80

In which of the following situations is the taxpayer not allowed a deduction for moving expenses?

A)Pam moves from Phoenix to Los Angeles to take a new job.She works at the Los Angeles job for 45 weeks before starting a new job in Las Vegas.

B)Paul moves from Boston to Miami to start a new business selling t-shirts.The business is not successful and Paul returns to Boston after 52 weeks.

C)Phyllis opens a coffee bar after moving from Seattle to San Francisco.She still owns the coffee bar and lives in San Francisco 90 weeks after her move.

D)Marva moves from Dallas to Washington D.C.in her job as an IRS agent.She is still working at the IRS Washington office after one year.

A)Pam moves from Phoenix to Los Angeles to take a new job.She works at the Los Angeles job for 45 weeks before starting a new job in Las Vegas.

B)Paul moves from Boston to Miami to start a new business selling t-shirts.The business is not successful and Paul returns to Boston after 52 weeks.

C)Phyllis opens a coffee bar after moving from Seattle to San Francisco.She still owns the coffee bar and lives in San Francisco 90 weeks after her move.

D)Marva moves from Dallas to Washington D.C.in her job as an IRS agent.She is still working at the IRS Washington office after one year.

Unlock Deck

Unlock for access to all 135 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 135 flashcards in this deck.