Deck 8: Foreign Currency Transactions and an Introduction to Hedging

Full screen (f)

Question

Question

Question

Question

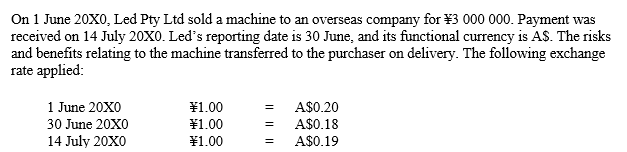

What was the foreign currency exchange difference recognised for Led Ltd on the transaction?

A)$30 000 FC exchange difference revenue

B)$30 000 FC exchange difference expense

C)$60 000 FC exchange difference revenue

D)$60 000 FC exchange difference expense

Question

Question

Question

Question

Question

Question

What was the foreign currency exchange difference on the transaction recognised by Led in the reporting period ending 30 June 20X1?

A)$30 000 FC exchange difference revenue

B)$30 000 FC exchange difference expense

C)$60 000 FC exchange difference revenue

D)$60 000 FC exchange difference expense

Question

Question

Question

Question

What was the foreign currency exchange difference recognised for the reporting period ending 30 June 20X0 by Led Ltd on the transaction?

A)$30 000 FC exchange difference revenue

B)$30 000 FC exchange difference expense

C)$60 000 FC exchange difference revenue

D)$60 000 FC exchange difference expense

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/28

Play

Full screen (f)

Deck 8: Foreign Currency Transactions and an Introduction to Hedging

1

Which of the following factors cannot under AASB 121 be considered in selecting an entity's functional currency:

A)the main currency influencing the selling price of its goods and services

B)the main currency influencing its labour and material costs

C)the currency of the main country whose competitive forces and regulation determine the selling price of its goods and services

D)the preferences of the entity's senior management group

A)the main currency influencing the selling price of its goods and services

B)the main currency influencing its labour and material costs

C)the currency of the main country whose competitive forces and regulation determine the selling price of its goods and services

D)the preferences of the entity's senior management group

D

2

In Australia, the presentation currency adopted must be the Australian currency.

False

3

Under AASB 121 it is possible for an Australian company to have multiple functional currencies, therefore it is possible for the financial report to contain financial statements using different presentation currencies.

False

4

What was the foreign currency exchange difference recognised for Led Ltd on the transaction?

A)$30 000 FC exchange difference revenue

B)$30 000 FC exchange difference expense

C)$60 000 FC exchange difference revenue

D)$60 000 FC exchange difference expense

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

5

A company can have more than one functional currency.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

6

Under AASB 121, foreign currency exchange differences are never recognised for non-monetary items.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

7

The calculation of FC exchange differences is much easier if direct exchange rates are used rather than indirect exchange rates.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

8

Under AASB 121 a company must initially record all transactions in its functional currency

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

9

When a non-monetary asset is remeasured to fair value in a foreign currency, it is translated using the reporting date spot rate.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

10

What was the foreign currency exchange difference on the transaction recognised by Led in the reporting period ending 30 June 20X1?

A)$30 000 FC exchange difference revenue

B)$30 000 FC exchange difference expense

C)$60 000 FC exchange difference revenue

D)$60 000 FC exchange difference expense

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

11

A foreign exchange rate quote can best be thought of as:

A)a bank's estimate of value of the foreign currency

B)the price of one currency in terms of another

C)a measure of the difference between the two countries' risk-free interest rates

D)the market's best guess about the future GDP growth rate for the foreign country

A)a bank's estimate of value of the foreign currency

B)the price of one currency in terms of another

C)a measure of the difference between the two countries' risk-free interest rates

D)the market's best guess about the future GDP growth rate for the foreign country

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

12

The holder of a liability denominated in a foreign currency would experience _____ when its functional currency appreciates against that foreign currency:

A)an economic gain

B)an economic loss

C)no change in value for that asset

D)only an accounting loss

A)an economic gain

B)an economic loss

C)no change in value for that asset

D)only an accounting loss

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

13

Alpha Ltd is an Australian company, the currency of its principal economic environment is UK£ and its financial statements are presented in ¥ the functional currency of its parent entity.

When considering foreign currency transactions and the preparation of financial reports of entities that engaged in transactions denominated in foreign currencies, four currency classifications are adopted:

I the presentation currency

II the domestic currency

III the functional currency

IV foreign currencies

For Alpha Ltd, it presentation currency is:

A)A$

B)¥

C)UK£

D)US$

When considering foreign currency transactions and the preparation of financial reports of entities that engaged in transactions denominated in foreign currencies, four currency classifications are adopted:

I the presentation currency

II the domestic currency

III the functional currency

IV foreign currencies

For Alpha Ltd, it presentation currency is:

A)A$

B)¥

C)UK£

D)US$

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

14

What was the foreign currency exchange difference recognised for the reporting period ending 30 June 20X0 by Led Ltd on the transaction?

A)$30 000 FC exchange difference revenue

B)$30 000 FC exchange difference expense

C)$60 000 FC exchange difference revenue

D)$60 000 FC exchange difference expense

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

15

The holder of an asset denominated in a foreign currency would experience _____ when the functional currency appreciates against that foreign currency:

A)an economic gain

B)an economic loss

C)no change in value for that asset

D)only an accounting loss

A)an economic gain

B)an economic loss

C)no change in value for that asset

D)only an accounting loss

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

16

A direct exchange rate quotation is one expressed in terms of the foreign currency equivalent of one unit of domestic currency.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

17

An entity's functional currency is:

A)always the currency of it place of domicile, for an Australian company the A$

B)a foreign currency used as the benchmark in converting other foreign currencies into the currency of the place of domicile

C)the currency in which most of its activities are denominated

D)always its domestic currency

A)always the currency of it place of domicile, for an Australian company the A$

B)a foreign currency used as the benchmark in converting other foreign currencies into the currency of the place of domicile

C)the currency in which most of its activities are denominated

D)always its domestic currency

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

18

Alpha Ltd is an Australian company, the currency of its principal economic environment is UK£ and its financial statements are presented in ¥ the functional currency of its parent entity.

When considering foreign currency transactions and the preparation of financial reports of entities that engaged in transactions denominated in foreign currencies, four currency classifications are adopted:

I the presentation currency

II the domestic currency

III the functional currency

IV foreign currencies

For Alpha Ltd its functional currency is:

A)A$

B)¥

C)UK£

D)US$

When considering foreign currency transactions and the preparation of financial reports of entities that engaged in transactions denominated in foreign currencies, four currency classifications are adopted:

I the presentation currency

II the domestic currency

III the functional currency

IV foreign currencies

For Alpha Ltd its functional currency is:

A)A$

B)¥

C)UK£

D)US$

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

19

Zeppelin Ltd ordered a batch of computers from the USA on 11 November 20X4 for a total price of US$800 000. Zeppelin Ltd’s reporting date is 31 December and its functional currency is A$. The computers were delivered on 23 December 20X4 and payment was made on 15 January 20X5. The risks and benefits of the ownership transfer to the purchaser on delivery. The computers formed part of Zeppelin’s inventory and was still on hand on 31 December 20X4.

-At what amount would be purchase of the inventory be recognised?

A)$615,385

B)$1,040,000

C)$1,000,000

D)$1,080,000

-At what amount would be purchase of the inventory be recognised?

A)$615,385

B)$1,040,000

C)$1,000,000

D)$1,080,000

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

20

Alpha Ltd is an Australian company, the currency of its principal economic environment is UK£ and its financial statements are presented in ¥ the functional currency of its parent entity.

When considering foreign currency transactions and the preparation of financial reports of entities that engaged in transactions denominated in foreign currencies, four currency classifications are adopted:

I the presentation currency

II the domestic currency

III the functional currency

IV foreign currencies

For Alpha Ltd the following currencies are foreign currency

A)A$, ¥, and US$ only

B)UK£ only

C)US$ only

D)UK£, ¥, and US$ only

When considering foreign currency transactions and the preparation of financial reports of entities that engaged in transactions denominated in foreign currencies, four currency classifications are adopted:

I the presentation currency

II the domestic currency

III the functional currency

IV foreign currencies

For Alpha Ltd the following currencies are foreign currency

A)A$, ¥, and US$ only

B)UK£ only

C)US$ only

D)UK£, ¥, and US$ only

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

21

Comprehensive Minerals NL borrowed US$35 000 000 from a syndicate of European bankers. The agreement was finalized on 1 June 20X5, the money was received on 1 July 20X5, and interest at 4% per half year is payable on 31 December and 30 June of each year. The company’s functional currency is the A$.

The following exchange rates applied.

-For the reporting period ending 30 June 20X7 the net amount recognised in the profit or loss statement in respect of the loan will be:

A)A$1 820 000 expense

B)A$3 570 000 expense

C)A$5 320 000 expense

D)A$2 730 000 revenue

The following exchange rates applied.

-For the reporting period ending 30 June 20X7 the net amount recognised in the profit or loss statement in respect of the loan will be:

A)A$1 820 000 expense

B)A$3 570 000 expense

C)A$5 320 000 expense

D)A$2 730 000 revenue

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

22

Zeppelin Ltd ordered a batch of computers from the USA on 11 November 20X4 for a total price of US$800 000. Zeppelin Ltd’s reporting date is 31 December and its functional currency is A$. The computers were delivered on 23 December 20X4 and payment was made on 15 January 20X5. The risks and benefits of the ownership transfer to the purchaser on delivery. The computers formed part of Zeppelin’s inventory and was still on hand on 31 December 20X4.

-How many A$ will be paid for the computers and what FC exchange difference will be included in Zeppelin's 20X5 financial report in relation to the purchase?

A)$960 000; $80 000 FC exchange difference expense

B)$960 000; $80 000 FC exchange difference revenue

C)$960 000; $120 000 FC exchange difference expense

D)$960 000; $120 000 FC exchange difference revenue

-How many A$ will be paid for the computers and what FC exchange difference will be included in Zeppelin's 20X5 financial report in relation to the purchase?

A)$960 000; $80 000 FC exchange difference expense

B)$960 000; $80 000 FC exchange difference revenue

C)$960 000; $120 000 FC exchange difference expense

D)$960 000; $120 000 FC exchange difference revenue

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

23

Zeppelin Ltd ordered a batch of computers from the USA on 11 November 20X4 for a total price of US$800 000. Zeppelin Ltd’s reporting date is 31 December and its functional currency is A$. The computers were delivered on 23 December 20X4 and payment was made on 15 January 20X5. The risks and benefits of the ownership transfer to the purchaser on delivery. The computers formed part of Zeppelin’s inventory and was still on hand on 31 December 20X4.

-What FC exchange difference, if any, will be included in Zeppelin's profit or loss statement for the year ended 31 December 20X4 and at what amount will the FC account payable be recognised in the balance sheet?

A)FC account payable = 1,080,000; $40,000 FC exchange difference revenue

B)FC account payable = 1,080,000; $80,000 FC exchange difference revenue

C)FC account payable = 1,080,000; $40,000 FC exchange difference expense

D)FC account payable = 1,080,000; $80,000 FC exchange difference expense

-What FC exchange difference, if any, will be included in Zeppelin's profit or loss statement for the year ended 31 December 20X4 and at what amount will the FC account payable be recognised in the balance sheet?

A)FC account payable = 1,080,000; $40,000 FC exchange difference revenue

B)FC account payable = 1,080,000; $80,000 FC exchange difference revenue

C)FC account payable = 1,080,000; $40,000 FC exchange difference expense

D)FC account payable = 1,080,000; $80,000 FC exchange difference expense

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

24

Sammy Ltd hired a US-based consultant to assist with a major client’s request to improve its internal control system. The consultant’s invoice for US$300,000 was received by Sammy Ltd on 23 June 2000, and paid on 23 July 2000.

Some spot foreign exchanges rates were:

-Which is the journal entry to record the foreign exchange difference at 30 June 20X0?

A)

B)

C)

D)

Some spot foreign exchanges rates were:

-Which is the journal entry to record the foreign exchange difference at 30 June 20X0?

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

25

On 10 June 20X0, Jackson Ltd an Australian company, purchased inventory for £100 000 from Pollock Ltd, a Welsh company. Under the contract of sale, property passes when the inventory was delivered to OzWale Air Cargo Ltd, this occurred on 20 June 20X0. The inventory was delivered to Jackson Ltd on 25 June 20X0. Jackson Ltd’s reporting period ends on 30 June and its functional currency is A$. Jackson paid the UK£ amount on 15 July 20X0. Some foreign exchange rates were:

-What FC exchange difference amounts will be included in Jackson's profit or loss statement if property passed on delivery in Australia?

20X0 20X1

$ $

A)10,000 revenue 20,000 revenue

B)10,000 expense 30,000 revenue

C)15,000 revenue 25,000 revenue

D)15,000 revenue 25,000 expense

-What FC exchange difference amounts will be included in Jackson's profit or loss statement if property passed on delivery in Australia?

20X0 20X1

$ $

A)10,000 revenue 20,000 revenue

B)10,000 expense 30,000 revenue

C)15,000 revenue 25,000 revenue

D)15,000 revenue 25,000 expense

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

26

Comprehensive Minerals NL borrowed US$35 000 000 from a syndicate of European bankers. The agreement was finalized on 1 June 20X5, the money was received on 1 July 20X5, and interest at 4% per half year is payable on 31 December and 30 June of each year. The company’s functional currency is the A$.

The following exchange rates applied.

-In the company's financial statements for the reporting period ending 30 June 20X6 the following items will appear:

A)interest expense A$3 500 000; foreign currency denominated loan A$43 750 000

B)interest expense A$3 360 000; foreign currency denominated loan A$43 750 000

C)interest revenue A$3 500 000; foreign currency denominated loan A$43 750 000

D)interest expense A$3 864 000; foreign currency denominated loan A$43 750 000

The following exchange rates applied.

-In the company's financial statements for the reporting period ending 30 June 20X6 the following items will appear:

A)interest expense A$3 500 000; foreign currency denominated loan A$43 750 000

B)interest expense A$3 360 000; foreign currency denominated loan A$43 750 000

C)interest revenue A$3 500 000; foreign currency denominated loan A$43 750 000

D)interest expense A$3 864 000; foreign currency denominated loan A$43 750 000

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

27

On 10 June 20X0, Jackson Ltd an Australian company, purchased inventory for £100 000 from Pollock Ltd, a Welsh company. Under the contract of sale, property passes when the inventory was delivered to OzWale Air Cargo Ltd, this occurred on 20 June 20X0. The inventory was delivered to Jackson Ltd on 25 June 20X0. Jackson Ltd’s reporting period ends on 30 June and its functional currency is A$. Jackson paid the UK£ amount on 15 July 20X0. Some foreign exchange rates were:

-What FC exchange difference amounts will be included in Jackson's profit or loss statement?

20X0 20X1

$ $

A)10,000 expense 10,000 revenue

B)10,000 expense 20,000 expense

C)10,000 revenue 20,000 revenue

D)5,000 revenue 20,000 revenue

-What FC exchange difference amounts will be included in Jackson's profit or loss statement?

20X0 20X1

$ $

A)10,000 expense 10,000 revenue

B)10,000 expense 20,000 expense

C)10,000 revenue 20,000 revenue

D)5,000 revenue 20,000 revenue

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

28

Sammy Ltd hired a US-based consultant to assist with a major client’s request to improve its internal control system. The consultant’s invoice for US$300,000 was received by Sammy Ltd on 23 June 2000, and paid on 23 July 2000.

Some spot foreign exchanges rates were:

-What is the difference between the expense for consultant's fees in the profit or loss statement and the amount of A$ cash paid for this consultant?

A)10,517

B)22,290

C)38,460

D)16,170

Some spot foreign exchanges rates were:

-What is the difference between the expense for consultant's fees in the profit or loss statement and the amount of A$ cash paid for this consultant?

A)10,517

B)22,290

C)38,460

D)16,170

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 28 flashcards in this deck.