Deck 8: Flexible Budgets, Variances, and Management Control: II

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the amount of fixed overhead allocated to production?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $130,000

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the amount of fixed overhead allocated to production?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $130,000

Question

Question

Question

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the flexible-budget amount for fixed-overhead?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $120,983

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the flexible-budget amount for fixed-overhead?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $120,983

Question

Question

Question

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead rate variance?

A) $1,000 unfavourable

B) $2,000 favourable

C) $3,000 unfavourable

D) $5,000 favourable

E) $983 unfavourable

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead rate variance?

A) $1,000 unfavourable

B) $2,000 favourable

C) $3,000 unfavourable

D) $5,000 favourable

E) $983 unfavourable

Question

Question

Question

In order to properly record a fixed manufacturing overhead rate variance of $30,000 unfavourable and a production-volume overhead variance of $20,000 favourable, what would the appropriate journal entry be if actual fixed overhead is $500,000?

A)

B)

C)

D)

E)

A)

B)

C)

D)

E)

Question

Question

Question

Question

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead production-volume variance?

A) $2,000 unfavourable

B) $3,000 favourable

C) $4,000 unfavourable

D) $5,000 favourable

E) $10,000 favourable

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead production-volume variance?

A) $2,000 unfavourable

B) $3,000 favourable

C) $4,000 unfavourable

D) $5,000 favourable

E) $10,000 favourable

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Calculate the fixed manufacturing overhead rate variance based on the following data:

Question

Question

Question

Question

Question

Question

Question

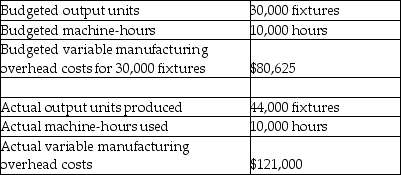

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead sales-volume variance?

A) $2,750 favourable

B) $37,625 favourable

C) $37,625 unfavourable

D) $40,375 favourable

E) $40,375 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead sales-volume variance?

A) $2,750 favourable

B) $37,625 favourable

C) $37,625 unfavourable

D) $40,375 favourable

E) $40,375 unfavourable

Question

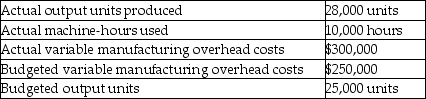

What is the variable manufacturing overhead static-budget variance given the following information?

A) $20,000 favourable

B) $20,000 unfavourable

C) $50,000 unfavourable

D) $50,000 favourable

E) $55,000 favourable

A) $20,000 favourable

B) $20,000 unfavourable

C) $50,000 unfavourable

D) $50,000 favourable

E) $55,000 favourable

Question

During October 2012 Foxmore Inc. used $250,000 in manufacturing overhead costs, of which $66,500 was variable. Budgeted manufacturing overhead was $229,500, of which $75,000 was variable. Which of the following entries for manufacturing overhead could have been recorded?

A)

B)

C)

D)

E)

A)

B)

C)

D)

E)

Question

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Cady Machine Shop used 15,000 machine hours during January. It takes 0.90 machine-hours to produce one unit; 15,000 units were produced during the month. Budgeted production included 12,000 units, using 10,800 machine hours. Budgeted variable manufacturing overhead costs per machine-hour is $22.50. What is the variable overhead efficiency variance for Cady?

A) $67,500 unfavourable

B) $67,500 favourable

C) $37,000 favourable

D) $33,750 favourable

E) $33,750 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Cady Machine Shop used 15,000 machine hours during January. It takes 0.90 machine-hours to produce one unit; 15,000 units were produced during the month. Budgeted production included 12,000 units, using 10,800 machine hours. Budgeted variable manufacturing overhead costs per machine-hour is $22.50. What is the variable overhead efficiency variance for Cady?

A) $67,500 unfavourable

B) $67,500 favourable

C) $37,000 favourable

D) $33,750 favourable

E) $33,750 unfavourable

Question

Question

If Miller Company makes the following journal entry:  It may be inferred that

It may be inferred that

A) Miller over-allocated variable manufacturing overhead.

B) the net variance is a $12,500 favourable rate variance.

C) actual variable manufacturing overhead costs were $62,500.

D) the journal entry accounts are incorrect.

E) the net variance is $12,500 unfavourable.

It may be inferred thatA) Miller over-allocated variable manufacturing overhead.

B) the net variance is a $12,500 favourable rate variance.

C) actual variable manufacturing overhead costs were $62,500.

D) the journal entry accounts are incorrect.

E) the net variance is $12,500 unfavourable.

Question

Question

Question

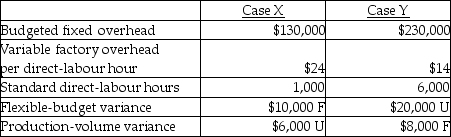

A company had the following information pertaining to two different cases:  The total overhead variance in Case Y was

The total overhead variance in Case Y was

A) $4,000 unfavourable.

B) $4,000 favourable.

C) $10,000 unfavourable.

D) $12,000 favourable.

E) $12,000 unfavourable.

The total overhead variance in Case Y wasA) $4,000 unfavourable.

B) $4,000 favourable.

C) $10,000 unfavourable.

D) $12,000 favourable.

E) $12,000 unfavourable.

Question

Question

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is the variable manufacturing overhead flexible-budget variance?

A) $387 favourable

B) $2,363 unfavourable

C) $2,363 favourable

D) $2,750 favourable

E) $2,750 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is the variable manufacturing overhead flexible-budget variance?

A) $387 favourable

B) $2,363 unfavourable

C) $2,363 favourable

D) $2,750 favourable

E) $2,750 unfavourable

Question

Question

Question

Question

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead static-budget variance?

A) $2,750 favourable

B) $2,750 unfavourable

C) $40,375 favourable

D) $40,375 unfavourable

E) $44,000 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead static-budget variance?

A) $2,750 favourable

B) $2,750 unfavourable

C) $40,375 favourable

D) $40,375 unfavourable

E) $44,000 unfavourable

Question

Question

Question

Question

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Assume that variable manufacturing overhead is allocated according to machine-hours. Aladdin Company expects to produce 400 cases of Product A using 400 machine-hours. Each machine hour is expected to take 10 KWH of electricity, which costs $6 per KWH. What is the maximum amount the company would be willing to pay for the new machine based solely on rate and efficiency variances if a new energy-efficient machine only used 8 KWH per machine-hour?

A) $120

B) $4,680

C) $4,920

D) $4,800

E) $4,120

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Assume that variable manufacturing overhead is allocated according to machine-hours. Aladdin Company expects to produce 400 cases of Product A using 400 machine-hours. Each machine hour is expected to take 10 KWH of electricity, which costs $6 per KWH. What is the maximum amount the company would be willing to pay for the new machine based solely on rate and efficiency variances if a new energy-efficient machine only used 8 KWH per machine-hour?

A) $120

B) $4,680

C) $4,920

D) $4,800

E) $4,120

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/137

Play

Full screen (f)

Deck 8: Flexible Budgets, Variances, and Management Control: II

1

Fixed Manufacturing Overhead Variances that are material should only be written off to Cost of Goods Sold.

False

2

The budgeted fixed overhead rate per output unit is computed by dividing budgeted fixed overhead costs by the level of input units.

False

3

An unfavourable fixed setup overhead rate variance could be due to higher lease costs of new setup equipment or higher salaries paid to engineers and supervisors.

True

4

The difference between budgeted fixed overhead and fixed overhead allocated for actual output units achieved, is the production-volume variance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

5

Capacity decisions are considered operating decisions because they involve the long-term acquisition of assets by purchase or lease.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

6

In the journal entry that records overhead variances, the manufacturing overhead allocated accounts are closed.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

7

The fixed overhead flexible budget variance is the same as the fixed overhead static budget variance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

8

Capacity cost is a variable overhead cost.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

9

Fixed overhead costs are a lump sum that does not change in total despite changes in the cost driver.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

10

The (production) denominator level is the quantity of the allocation base used to allocate fixed overhead costs to a cost object in developing a budgeted fixed overhead rate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

11

Decisions about capacity are considered to be

A) operating decisions.

B) best done by plant supervisors.

C) best done during production.

D) more relevant for variable costs.

E) strategic decisions.

A) operating decisions.

B) best done by plant supervisors.

C) best done during production.

D) more relevant for variable costs.

E) strategic decisions.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

12

Which decisions are most likely to have been made by the start of the accounting period?

A) decisions affecting value-added costs

B) decisions affecting non-value-added costs

C) decisions affecting variable overhead costs

D) decisions affecting both fixed and variable overhead costs

E) decisions affecting fixed overhead costs

A) decisions affecting value-added costs

B) decisions affecting non-value-added costs

C) decisions affecting variable overhead costs

D) decisions affecting both fixed and variable overhead costs

E) decisions affecting fixed overhead costs

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

13

Randy's Production Company uses a single cost pool for fixed manufacturing overhead. The amount for May 2012 was budgeted at $250,000; however, the actual amount was $350,000. Actual production for May was 12,500 units, and actual machine hours were 10,000. Budgeted production included 17,750 units and 12,375 machine hours. What is the budgeted fixed overhead rate per input unit?

A) $25.00 per unit

B) $35.00 per unit

C) $20.00 per unit

D) $14.09 per unit

E) $14.08 per unit

A) $25.00 per unit

B) $35.00 per unit

C) $20.00 per unit

D) $14.09 per unit

E) $14.08 per unit

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

14

The production -volume overhead variance is favourable when actual outputs exceed the denominator level.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

15

The production-volume variance arises because the actual output level differs from the output level used as the denominator to calculate the budgeted fixed overhead rate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

16

Human capital refers to the intangible skills provided by people and is an inventoriable cost under GAAP.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

17

The fixed manufacturing overhead efficiency variance is used to analyze overhead costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

18

Capacity refers to the quantity of outputs that can be produced from long-term resources available to the company.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

19

A favourable production-volume variance arises when manufacturing capacity planned for is not used.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

20

Managers should use unitized fixed manufacturing overhead costs for planning and control.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

21

Regal Company uses a single cost pool for fixed manufacturing overhead. The amount for June 2012 was budgeted at $500,000; however, the actual amount was $700,000. Actual production for June was 12,500 units, and actual machine hours were 10,000. Budgeted production included 17,750 units and 12,375 machine hours. What is the budgeted fixed overhead rate per output unit?

A) $28.17 per unit

B) $39.44 per unit

C) $40.40 per unit

D) $56.56 per unit

E) $65.17 per unit

A) $28.17 per unit

B) $39.44 per unit

C) $40.40 per unit

D) $56.56 per unit

E) $65.17 per unit

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

22

Capacity cost is

A) only an inventoriable cost.

B) only a period cost.

C) never amortized.

D) a variable manufacturing overhead cost.

E) a fixed manufacturing overhead cost.

A) only an inventoriable cost.

B) only a period cost.

C) never amortized.

D) a variable manufacturing overhead cost.

E) a fixed manufacturing overhead cost.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

23

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the amount of fixed overhead allocated to production?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $130,000

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the amount of fixed overhead allocated to production?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $130,000

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

24

The production-volume variance

A) only pertains to variable overhead costs.

B) only pertains to fixed overhead costs.

C) is not applicable in analysis of inventory costs.

D) pertains to both fixed and variable overhead costs.

E) equals the rate variance minus the efficiency variance.

A) only pertains to variable overhead costs.

B) only pertains to fixed overhead costs.

C) is not applicable in analysis of inventory costs.

D) pertains to both fixed and variable overhead costs.

E) equals the rate variance minus the efficiency variance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

25

Actual overhead is $700,000, while budgeted overhead is $598,000. What is the fixed overhead static-budget variance if 250,000 units are produced and 225,000 are budgeted?

A) $80,000 favourable

B) $100,000 unfavourable

C) $100,000 favourable

D) $102,000 unfavourable

E) $102,000 favourable

A) $80,000 favourable

B) $100,000 unfavourable

C) $100,000 favourable

D) $102,000 unfavourable

E) $102,000 favourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

26

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the flexible-budget amount for fixed-overhead?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $120,983

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the flexible-budget amount for fixed-overhead?

A) $120,000

B) $122,000

C) $123,000

D) $125,000

E) $120,983

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

27

Budgeted output for DuCane Small Engines Inc. was 20,000 engines during February 2012. Budgeted fixed overhead per output unit was $2.50, and 30,000 engines were actually produced. Actual fixed overhead was allocated at $3.00 per engine. What is the production-volume overhead variance?

A) $33,500 favourable

B) $25,000 unfavourable

C) $30,000 favourable

D) $30,000 unfavourable

E) $25,000 favourable

A) $33,500 favourable

B) $25,000 unfavourable

C) $30,000 favourable

D) $30,000 unfavourable

E) $25,000 favourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

28

Davis Company produced 20,000 cases of beer. Machinery usage is 1.5 hours per case. Budget outputs are 22,000 cases. What are the required static budget machine hour inputs and flexible budget machine hour inputs, respectively?

A) 30,000 Machine hours, 33,000 Machine hours

B) 33,000 Machine hours, 30,000 Machine hours

C) 39,000 Machine hours, 34,000 Machine hours

D) 34,000 Machine hours, 39,000 Machine hours

E) 39,000 Machine hours, 33,000 Machine hours

A) 30,000 Machine hours, 33,000 Machine hours

B) 33,000 Machine hours, 30,000 Machine hours

C) 39,000 Machine hours, 34,000 Machine hours

D) 34,000 Machine hours, 39,000 Machine hours

E) 39,000 Machine hours, 33,000 Machine hours

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

29

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead rate variance?

A) $1,000 unfavourable

B) $2,000 favourable

C) $3,000 unfavourable

D) $5,000 favourable

E) $983 unfavourable

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead rate variance?

A) $1,000 unfavourable

B) $2,000 favourable

C) $3,000 unfavourable

D) $5,000 favourable

E) $983 unfavourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

30

Leek Company predicted that the fixed overhead would be $200,000 in April 20X1. Production amounted to 60,000 actual and 50,000 budgeted decks of cards. Each deck takes approximately 0.20 machine hours to produce. The actual overhead costs per machine hour are $25. What is the production-volume overhead variance?

A) $40,000 unfavourable

B) $40,000 favourable

C) $150,000 unfavourable

D) $150,000 favourable

E) $0

A) $40,000 unfavourable

B) $40,000 favourable

C) $150,000 unfavourable

D) $150,000 favourable

E) $0

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

31

In flexible budgets, costs that remain the same regardless of the output levels within the relevant range are

A) allocated costs.

B) budgeted costs.

C) fixed costs.

D) variable costs.

E) estimated costs.

A) allocated costs.

B) budgeted costs.

C) fixed costs.

D) variable costs.

E) estimated costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

32

In order to properly record a fixed manufacturing overhead rate variance of $30,000 unfavourable and a production-volume overhead variance of $20,000 favourable, what would the appropriate journal entry be if actual fixed overhead is $500,000?

A)

B)

C)

D)

E)

A)

B)

C)

D)

E)

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

33

A favourable production-volume variance indicates that the company

A) has good management.

B) produced more than it has sold.

C) has a total economic gain from using excess capacity.

D) should increase capacity.

E) has allocated more fixed overhead costs than budgeted.

A) has good management.

B) produced more than it has sold.

C) has a total economic gain from using excess capacity.

D) should increase capacity.

E) has allocated more fixed overhead costs than budgeted.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

34

When machine-hours are used as a cost allocation base, the item MOST likely to contribute to a favourable production-volume variance is

A) an increase in the selling price of the product.

B) the purchase of a new manufacturing machine costing considerably less than expected.

C) a decline in the cost of energy.

D) strengthened demand for the product.

E) a competitor lowering the price of a similar product.

A) an increase in the selling price of the product.

B) the purchase of a new manufacturing machine costing considerably less than expected.

C) a decline in the cost of energy.

D) strengthened demand for the product.

E) a competitor lowering the price of a similar product.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements is true?

A) The fixed manufacturing sales-volume variance is rarely zero.

B) The difference between the allocated and the budgeted overhead is the production-volume variance.

C) The production-volume variance arises for both fixed and variable costs.

D) The fixed manufacturing overhead sales-volume variance can be written-off to cost of goods sold.

E) The production-volume variance arises only for variable costs.

A) The fixed manufacturing sales-volume variance is rarely zero.

B) The difference between the allocated and the budgeted overhead is the production-volume variance.

C) The production-volume variance arises for both fixed and variable costs.

D) The fixed manufacturing overhead sales-volume variance can be written-off to cost of goods sold.

E) The production-volume variance arises only for variable costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

36

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead production-volume variance?

A) $2,000 unfavourable

B) $3,000 favourable

C) $4,000 unfavourable

D) $5,000 favourable

E) $10,000 favourable

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

What is the fixed overhead production-volume variance?

A) $2,000 unfavourable

B) $3,000 favourable

C) $4,000 unfavourable

D) $5,000 favourable

E) $10,000 favourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

37

In variance analysis, fixed manufacturing overhead will have

A) an efficiency variance.

B) a flexible-budget variance.

C) a rate variance.

D) a static-budget variance.

E) no variance, because it is fixed.

A) an efficiency variance.

B) a flexible-budget variance.

C) a rate variance.

D) a static-budget variance.

E) no variance, because it is fixed.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

38

The difference between budgeted fixed manufacturing overhead and the fixed manufacturing overhead allocated to actual output units achieved is called

A) an efficiency variance.

B) a flexible-budget variance.

C) a manufacturing overhead flexible-budget variance.

D) a production-volume overhead variance.

E) an unallocated variable cost.

A) an efficiency variance.

B) a flexible-budget variance.

C) a manufacturing overhead flexible-budget variance.

D) a production-volume overhead variance.

E) an unallocated variable cost.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

39

The production-volume variance may also be referred to as the

A) flexible-budget variance.

B) static-budget variance.

C) rate variance.

D) efficiency variance.

E) denominator-level variance.

A) flexible-budget variance.

B) static-budget variance.

C) rate variance.

D) efficiency variance.

E) denominator-level variance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

40

Regal Company uses a single cost pool for fixed manufacturing overhead. The amount for June 2012 was budgeted at $500,000; however, the actual amount was $700,000. Actual production for June was 12,500 units, and actual machine hours were 10,000. Budgeted production included 17,750 units and 12,375 machine hours. What is the budgeted fixed overhead rate per machine hour?

A) $28.17 per machine hour

B) $39.44 per machine hour

C) $40.40 per machine hour

D) $56.56 per machine hour

E) $65.17 per machine hour

A) $28.17 per machine hour

B) $39.44 per machine hour

C) $40.40 per machine hour

D) $56.56 per machine hour

E) $65.17 per machine hour

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

41

Mostly Miniatures has just implemented a new cost accounting system that provides two variances for fixed manufacturing overhead. While the company's managers are familiar with the concept of static-budget variance, they are unclear as to how to interpret the production-volume overhead variances. Currently the company has a production capacity of 54,000 miniatures a month although it generally produces only 46,000 cases. However, in any given month the actual production is probably something other than 46,000.

Required:

a. Does the production-volume overhead variance measure the difference between the 54,000 and 46,000, or the difference between the 46,000 and the actual monthly production? Explain.

b. What advice can you provide the managers that will help them interpret the production-volume overhead variances?

Required:

a. Does the production-volume overhead variance measure the difference between the 54,000 and 46,000, or the difference between the 46,000 and the actual monthly production? Explain.

b. What advice can you provide the managers that will help them interpret the production-volume overhead variances?

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

42

When machine-hours are used as a cost allocation base, the item MOST likely to contribute to an unfavourable production-volume variance is

A) a new competitor gaining market share.

B) a new manufacturing machine costing considerably more than expected.

C) an increase in the cost of energy.

D) strengthened demand for the product.

E) an increase in the number of direct-labour hours.

A) a new competitor gaining market share.

B) a new manufacturing machine costing considerably more than expected.

C) an increase in the cost of energy.

D) strengthened demand for the product.

E) an increase in the number of direct-labour hours.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

43

All Clean of Alberta manufactures individual shampoos for hotel/motel clientele. The fixed manufacturing overhead costs for 2012 will total $576,000. The company uses good units finished for fixed overhead allocation and anticipates 300,000 units of production. Good units finished average 92 percent of total units produced. During January, 20,000 units were produced. Actual fixed overhead cost per good unit averaged $2.82 in January.

Required:

a. Determine the fixed overhead rate for 2012.

b. Determine the fixed overhead static-budget variance for January.

c. Determine the fixed overhead production-volume variance for January.

d. Determine the fixed overhead rate variance for January.

Required:

a. Determine the fixed overhead rate for 2012.

b. Determine the fixed overhead static-budget variance for January.

c. Determine the fixed overhead production-volume variance for January.

d. Determine the fixed overhead rate variance for January.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

44

An unfavourable variable overhead rate variance can be the result of paying lower prices than budgeted for variable overhead items such as energy.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

45

The variable overhead flexible-budget variance measures the difference between standard variable overhead costs and flexible-budget variable overhead costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

46

The variable overhead efficiency variance measures the efficiency with which the cost-allocation base is used.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

47

Everjoice Company makes clocks. The budgeted fixed overhead costs for 2012 total $720,000. The company uses direct labour-hours for fixed overhead allocation and anticipates 240,000 hours during the year for 480,000 units. An equal number of units are budgeted for each month.

During June, 42,000 clocks were produced and $63,000 were spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on units of input.

b. Determine the fixed overhead static-budget variance for June.

c. Determine the production-volume overhead variance for June.

During June, 42,000 clocks were produced and $63,000 were spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on units of input.

b. Determine the fixed overhead static-budget variance for June.

c. Determine the production-volume overhead variance for June.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

48

Johnston Equipment develops food processing equipment. The budgeted fixed overhead costs for 2012 total $768,000. The company uses direct labour-hours for fixed overhead allocation and anticipates 480,000 hours during the year for 960,000 units. An equal number of units are budgeted for each month.

During April 84,000 packages (units) were produced and $66,000 was spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on direct labour-hours.

b. Determine the fixed overhead static-budget variance for April.

c. Determine the production-volume overhead variance for April.

During April 84,000 packages (units) were produced and $66,000 was spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on direct labour-hours.

b. Determine the fixed overhead static-budget variance for April.

c. Determine the production-volume overhead variance for April.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

49

Variable overhead rate variance is the difference between the actual amount of variable overhead incurred and the budgeted amount allowed for the actual quantity of the variable overhead allocation base used for the actual output units achieved.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

50

Brown Company makes watches. The budgeted fixed overhead costs for 2012 total $324,000. The company uses direct labour-hours for fixed overhead allocation and anticipates 10,800 hours during the year for 540,000 units. An equal number of units are budgeted for each month.

During October, 48,000 watches were produced and $28,000 was spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on the units of input.

b. Determine the fixed overhead static-budget variance for October.

c. Determine the production-volume overhead variance for October.

During October, 48,000 watches were produced and $28,000 was spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on the units of input.

b. Determine the fixed overhead static-budget variance for October.

c. Determine the production-volume overhead variance for October.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

51

How is a budgeted fixed overhead cost rate calculated?

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

52

The variable overhead efficiency variance is computed in a different way than the efficiency variance for direct-cost items.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

53

Explain two concerns when interpreting the production-volume variance as a measure of the economic cost of unused capacity.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

54

Even where separate variable and fixed manufacturing overhead control accounts are used for job costing, it is not necessary to have separate overhead allocated accounts.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

55

Calculate the fixed manufacturing overhead rate variance based on the following data:

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

56

Using a standard costing system makes it possible to use a simple recording system.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

57

What are the arguments for prorating a production-volume variance that has been deemed to be material among work-in-process, finished goods, and cost of goods sold, as opposed to writing it all off to cost of goods sold?

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

58

Explain the meaning of a favourable production-volume variance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

59

If a manager views the proration approach as not being cost-effective, then the adjusted allocation rate approach would be used.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

60

Explain why there is no efficiency variance for fixed manufacturing overhead costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

61

The first step in developing variable overhead rates is

A) consider the potential effect of variances.

B) select homogeneous inputs for variable cost-allocation base(s).

C) analyze and select homogeneous variable cost pools.

D) compute the variable overhead cost-allocation rate(s).

E) choose the budget period.

A) consider the potential effect of variances.

B) select homogeneous inputs for variable cost-allocation base(s).

C) analyze and select homogeneous variable cost pools.

D) compute the variable overhead cost-allocation rate(s).

E) choose the budget period.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

62

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead sales-volume variance?

A) $2,750 favourable

B) $37,625 favourable

C) $37,625 unfavourable

D) $40,375 favourable

E) $40,375 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead sales-volume variance?

A) $2,750 favourable

B) $37,625 favourable

C) $37,625 unfavourable

D) $40,375 favourable

E) $40,375 unfavourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

63

What is the variable manufacturing overhead static-budget variance given the following information?

A) $20,000 favourable

B) $20,000 unfavourable

C) $50,000 unfavourable

D) $50,000 favourable

E) $55,000 favourable

A) $20,000 favourable

B) $20,000 unfavourable

C) $50,000 unfavourable

D) $50,000 favourable

E) $55,000 favourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

64

During October 2012 Foxmore Inc. used $250,000 in manufacturing overhead costs, of which $66,500 was variable. Budgeted manufacturing overhead was $229,500, of which $75,000 was variable. Which of the following entries for manufacturing overhead could have been recorded?

A)

B)

C)

D)

E)

A)

B)

C)

D)

E)

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

65

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Cady Machine Shop used 15,000 machine hours during January. It takes 0.90 machine-hours to produce one unit; 15,000 units were produced during the month. Budgeted production included 12,000 units, using 10,800 machine hours. Budgeted variable manufacturing overhead costs per machine-hour is $22.50. What is the variable overhead efficiency variance for Cady?

A) $67,500 unfavourable

B) $67,500 favourable

C) $37,000 favourable

D) $33,750 favourable

E) $33,750 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Cady Machine Shop used 15,000 machine hours during January. It takes 0.90 machine-hours to produce one unit; 15,000 units were produced during the month. Budgeted production included 12,000 units, using 10,800 machine hours. Budgeted variable manufacturing overhead costs per machine-hour is $22.50. What is the variable overhead efficiency variance for Cady?

A) $67,500 unfavourable

B) $67,500 favourable

C) $37,000 favourable

D) $33,750 favourable

E) $33,750 unfavourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following would possibly be adjusted as an end-of-period adjustment, using the adjusted allocation rate approach?

A) individual job records

B) ending work-in-process and finished goods inventories

C) cost of goods sold

D) only individual job records and ending finished goods inventory

E) ending work-in-process and finished goods inventories, individual job records, and cost of goods sold

A) individual job records

B) ending work-in-process and finished goods inventories

C) cost of goods sold

D) only individual job records and ending finished goods inventory

E) ending work-in-process and finished goods inventories, individual job records, and cost of goods sold

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

67

If Miller Company makes the following journal entry: It may be inferred that

A) Miller over-allocated variable manufacturing overhead.

B) the net variance is a $12,500 favourable rate variance.

C) actual variable manufacturing overhead costs were $62,500.

D) the journal entry accounts are incorrect.

E) the net variance is $12,500 unfavourable.

It may be inferred thatA) Miller over-allocated variable manufacturing overhead.

B) the net variance is a $12,500 favourable rate variance.

C) actual variable manufacturing overhead costs were $62,500.

D) the journal entry accounts are incorrect.

E) the net variance is $12,500 unfavourable.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

68

If Pope Inc. uses standard costing, the overhead allocated to work in process is recorded as a

A) debit to Manufacturing Overhead Allocated and a credit to Work-in-Process.

B) debit to Work-in-Process and credit to Manufacturing Overhead Control.

C) debit to Manufacturing Overhead Allocated and a credit to Manufacturing Overhead Control.

D) debit to Manufacturing Overhead Control and a credit to Manufacturing Overhead Allocated.

E) debit to Work-in-Process and a credits to Manufacturing Overhead Allocated.

A) debit to Manufacturing Overhead Allocated and a credit to Work-in-Process.

B) debit to Work-in-Process and credit to Manufacturing Overhead Control.

C) debit to Manufacturing Overhead Allocated and a credit to Manufacturing Overhead Control.

D) debit to Manufacturing Overhead Control and a credit to Manufacturing Overhead Allocated.

E) debit to Work-in-Process and a credits to Manufacturing Overhead Allocated.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

69

Two of the primary ways to manage variable-overhead costs include

A) eliminating non-value-added costs and reducing the consumption of cost drivers.

B) eliminating non-value-added costs and increasing fixed overhead expenses.

C) reducing the consumption of cost drivers and increasing variable costs.

D) using more energy-efficient equipment and planning for appropriate capacity levels.

E) increasing variable costs and eliminating non-value added costs.

A) eliminating non-value-added costs and reducing the consumption of cost drivers.

B) eliminating non-value-added costs and increasing fixed overhead expenses.

C) reducing the consumption of cost drivers and increasing variable costs.

D) using more energy-efficient equipment and planning for appropriate capacity levels.

E) increasing variable costs and eliminating non-value added costs.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

70

A company had the following information pertaining to two different cases: The total overhead variance in Case Y was

A) $4,000 unfavourable.

B) $4,000 favourable.

C) $10,000 unfavourable.

D) $12,000 favourable.

E) $12,000 unfavourable.

The total overhead variance in Case Y wasA) $4,000 unfavourable.

B) $4,000 favourable.

C) $10,000 unfavourable.

D) $12,000 favourable.

E) $12,000 unfavourable.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

71

The variable overhead efficiency variance can be interpreted the same way as the efficiency variance for direct-cost items.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

72

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is the variable manufacturing overhead flexible-budget variance?

A) $387 favourable

B) $2,363 unfavourable

C) $2,363 favourable

D) $2,750 favourable

E) $2,750 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is the variable manufacturing overhead flexible-budget variance?

A) $387 favourable

B) $2,363 unfavourable

C) $2,363 favourable

D) $2,750 favourable

E) $2,750 unfavourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

73

Which option(s) would be consistent with the proration approach for end-of-period adjustments when the underallocated or overallocated variable overhead costs are significant?

A) prorate based on the allocated overhead amount in the ending balance of work-in-process inventory and cost of goods sold

B) immediate write-off to cost of goods sold

C) prorate based on the total ending balance of variable overhead allocated and variable overhead control

D) prorate based on the allocated overhead amount in the ending balance of work-in-process inventory, finished goods inventory, and cost of goods sold

E) prorate based on the total ending balance of cost of goods sold and variable overhead control

A) prorate based on the allocated overhead amount in the ending balance of work-in-process inventory and cost of goods sold

B) immediate write-off to cost of goods sold

C) prorate based on the total ending balance of variable overhead allocated and variable overhead control

D) prorate based on the allocated overhead amount in the ending balance of work-in-process inventory, finished goods inventory, and cost of goods sold

E) prorate based on the total ending balance of cost of goods sold and variable overhead control

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

74

A favourable variable manufacturing overhead efficiency variance may be interpreted as meaning which of the following?

A) Employees used too much electricity during production.

B) Less maintenance was required than expected.

C) Excess supplies were used.

D) Too much of the cost driver was used.

E) The cost driver is inappropriate.

A) Employees used too much electricity during production.

B) Less maintenance was required than expected.

C) Excess supplies were used.

D) Too much of the cost driver was used.

E) The cost driver is inappropriate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

75

If Ferg Company has a $12,000 unfavourable variable-overhead efficiency variance, which of the following statements would be true?

A) Ferg would credit the Cost of Goods Sold account to write-off the variance.

B) Ferg used the variable overhead components more effectively than expected.

C) Ferg made efficient use of the cost driver.

D) Ferg used the variable overhead components and cost driver as expected.

E) Ferg did not use the cost driver efficiently.

A) Ferg would credit the Cost of Goods Sold account to write-off the variance.

B) Ferg used the variable overhead components more effectively than expected.

C) Ferg made efficient use of the cost driver.

D) Ferg used the variable overhead components and cost driver as expected.

E) Ferg did not use the cost driver efficiently.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

76

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead static-budget variance?

A) $2,750 favourable

B) $2,750 unfavourable

C) $40,375 favourable

D) $40,375 unfavourable

E) $44,000 unfavourable

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

What is Moeller Electric's variable manufacturing overhead static-budget variance?

A) $2,750 favourable

B) $2,750 unfavourable

C) $40,375 favourable

D) $40,375 unfavourable

E) $44,000 unfavourable

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

77

If budgeted machine-hours allowed per actual output unit equals 1.0 hour, and budgeted variable manufacturing overhead per machine-hour is $200, what is the budgeted variable manufacturing overhead rate per output unit?

A) $100

B) $200

C) $300

D) $400

E) $500

A) $100

B) $200

C) $300

D) $400

E) $500

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

78

Effective planning of variable overhead costs means that a company performs those variable overhead costs that primarily add value

A) for the current shareholders.

B) for the customer using the products or services.

C) for plant employees.

D) for major suppliers of component parts.

E) for management.

A) for the current shareholders.

B) for the customer using the products or services.

C) for plant employees.

D) for major suppliers of component parts.

E) for management.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

79

A leased factory building has a fixed monthly rental payment, and a variable overhead cost of energy and indirect labour. Which of the following is TRUE, assuming that all activity levels are within the relevant range?

A) Variable OVH costs will increase as production increases, but Fixed OVH costs will decrease.

B) Variable OVH costs will decrease as production increases, but Fixed OVH costs will increase.

C) Variable OVH costs will increase as production increases, and Fixed OVH costs will increase.

D) Variable OVH costs will increase as production increases, but Fixed OVH costs will remain constant.

E) Both will increase with production, but at different rates.

A) Variable OVH costs will increase as production increases, but Fixed OVH costs will decrease.

B) Variable OVH costs will decrease as production increases, but Fixed OVH costs will increase.

C) Variable OVH costs will increase as production increases, and Fixed OVH costs will increase.

D) Variable OVH costs will increase as production increases, but Fixed OVH costs will remain constant.

E) Both will increase with production, but at different rates.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

80

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Assume that variable manufacturing overhead is allocated according to machine-hours. Aladdin Company expects to produce 400 cases of Product A using 400 machine-hours. Each machine hour is expected to take 10 KWH of electricity, which costs $6 per KWH. What is the maximum amount the company would be willing to pay for the new machine based solely on rate and efficiency variances if a new energy-efficient machine only used 8 KWH per machine-hour?

A) $120

B) $4,680

C) $4,920

D) $4,800

E) $4,120

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

Assume that variable manufacturing overhead is allocated according to machine-hours. Aladdin Company expects to produce 400 cases of Product A using 400 machine-hours. Each machine hour is expected to take 10 KWH of electricity, which costs $6 per KWH. What is the maximum amount the company would be willing to pay for the new machine based solely on rate and efficiency variances if a new energy-efficient machine only used 8 KWH per machine-hour?

A) $120

B) $4,680

C) $4,920

D) $4,800

E) $4,120

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 137 flashcards in this deck.