Exam 8: Flexible Budgets, Variances, and Management Control: II

Exam 1: The Accountants Vital Role in Decision Making141 Questions

Exam 2: An Introduction to Cost Terms and Purposes165 Questions

Exam 3: Cost-Volume-Profit Analysis139 Questions

Exam 4: Job Costing138 Questions

Exam 5: Activity-Based Costing and Management133 Questions

Exam 6: Master Budget and Responsibility Accounting150 Questions

Exam 7: Flexible Budgets, Variances, and Management Control: I146 Questions

Exam 8: Flexible Budgets, Variances, and Management Control: II137 Questions

Exam 9: Income Effects of Denominator Level on Inventory Valuation154 Questions

Exam 10: Quantitative Analyses of Cost Functions114 Questions

Exam 11: Decision Making and Relevant Information146 Questions

Exam 12: Pricing Decisions, Product Profitability Decisions, and Cost Management135 Questions

Exam 13: Strategy, Balanced Scorecard, and Profitability Analysis140 Questions

Exam 14: Period Cost Allocation153 Questions

Exam 15: Cost Allocation: Joint Products and Byproducts149 Questions

Exam 16: Revenue and Customer Profitability Analysis137 Questions

Exam 17: Process Costing128 Questions

Exam 18: Spoilage, Rework, and Scrap121 Questions

Exam 19: Cost Management: Quality, Time, and the Theory of Constraints158 Questions

Exam 20: Inventory Cost Management Strategies136 Questions

Exam 21: Capital Budgeting: Methods of Investment Analysis128 Questions

Exam 22: Capital Budgeting: a Closer Look120 Questions

Exam 23: Transfer Pricing and Multinational Management Control Systems141 Questions

Exam 24: Multinational Performance Measurement and Compensation139 Questions

Select questions type

Capacity refers to the quantity of outputs that can be produced from long-term resources available to the company.

Free

(True/False)

4.9/5  (40)

(40)

Correct Answer: Verified

Verified

True

If Miller Company makes the following journal entry:  It may be inferred that

It may be inferred that

Free

(Multiple Choice)

4.8/5 (37)

Correct Answer:Verified

C

Using a standard costing system makes it possible to use a simple recording system.

Free

(True/False)

4.7/5 (37)

Correct Answer:Verified

True

The chapter shows that variance analysis of overhead costs can be presented in 4-, 3-, 2-, and 1-variance analysis. Explain what each of the variances presented under each method shows about overhead costs.

(Essay)

4.7/5 (43)

Budgeted output for DuCane Small Engines Inc. was 20,000 engines during February 2012. Budgeted fixed overhead per output unit was $2.50, and 30,000 engines were actually produced. Actual fixed overhead was allocated at $3.00 per engine. What is the production-volume overhead variance?

(Multiple Choice)

4.8/5 (41)

Which of the following journal entries is correct with respect to recording the fixed overhead cost variances for April?

(Multiple Choice)

4.9/5 (26)

Capacity decisions are considered operating decisions because they involve the long-term acquisition of assets by purchase or lease.

(True/False)

4.8/5 (38)

The (production) denominator level is the quantity of the allocation base used to allocate fixed overhead costs to a cost object in developing a budgeted fixed overhead rate.

(True/False)

4.8/5 (42)

Davis Company produced 20,000 cases of beer. Machinery usage is 1.5 hours per case. Budget outputs are 22,000 cases. What are the required static budget machine hour inputs and flexible budget machine hour inputs, respectively?

(Multiple Choice)

4.7/5 (36)

Everjoice Company makes clocks. The budgeted fixed overhead costs for 2012 total $720,000. The company uses direct labour-hours for fixed overhead allocation and anticipates 240,000 hours during the year for 480,000 units. An equal number of units are budgeted for each month.

During June, 42,000 clocks were produced and $63,000 were spent on fixed overhead.

Required:

a. Determine the fixed overhead rate for 2012 based on units of input.

b. Determine the fixed overhead static-budget variance for June.

c. Determine the production-volume overhead variance for June.

(Essay)

4.8/5 (35)

Use the information below to answer the following question(s).

Michelle Inc. uses a level 4-variance analysis of its manufacturing overhead costs, and has the following results for April.

A. Budgeted direct labour-hours per unit is used to allocate variable manufacturing overhead.

B. Budgeted amounts for April 2012 are:

B. Budgeted amounts for April 2012 are:

C. Actual amounts for April 2012 are:

C. Actual amounts for April 2012 are:

-What is the fixed manufacturing overhead rate variance?

-What is the fixed manufacturing overhead rate variance?

(Multiple Choice)

4.9/5 (33)

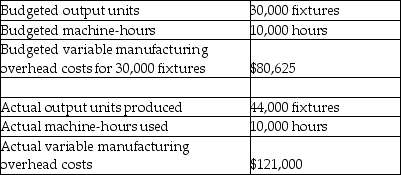

Use the information below to answer the following question(s).

Moeller Electric manufactures light fixtures. The following information pertains to the company's manufacturing overhead data.

-Cady Machine Shop used 15,000 machine hours during January. It takes 0.90 machine-hours to produce one unit; 15,000 units were produced during the month. Budgeted production included 12,000 units, using 10,800 machine hours. Budgeted variable manufacturing overhead costs per machine-hour is $22.50. What is the variable overhead efficiency variance for Cady?

-Cady Machine Shop used 15,000 machine hours during January. It takes 0.90 machine-hours to produce one unit; 15,000 units were produced during the month. Budgeted production included 12,000 units, using 10,800 machine hours. Budgeted variable manufacturing overhead costs per machine-hour is $22.50. What is the variable overhead efficiency variance for Cady?

(Multiple Choice)

4.9/5 (31)

Both financial and nonfinancial performance measures are key inputs when evaluating the performance of managers.

(True/False)

4.9/5 (39)

Answer the following question(s) using the information below.

Jenny's Corporation manufactured 25,000 grooming kits for horses during March. The fixed-overhead cost allocation rate is $20.00 per machine-hour. The following fixed overhead data pertain to March:

-What is the fixed overhead rate variance?

-What is the fixed overhead rate variance?

(Multiple Choice)

4.8/5 (32)

The production -volume overhead variance is favourable when actual outputs exceed the denominator level.

(True/False)

4.8/5 (32)

Use the information below to answer the following question(s).

Michelle Inc. uses a level 4-variance analysis of its manufacturing overhead costs, and has the following results for April.

A. Budgeted direct labour-hours per unit is used to allocate variable manufacturing overhead.

B. Budgeted amounts for April 2012 are:

C. Actual amounts for April 2012 are:

-What is the variable manufacturing overhead rate variance?

(Multiple Choice)

5.0/5 (36)

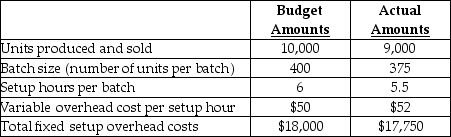

Answer the following question(s) using the information below.

Lukehart Industries Inc. produces air purifiers in batches. To manufacture a batch of the purifiers Lukehart Inc. must setup the machines and assembly line tooling. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and tooling for different models of the air purifiers.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup hours. The following information pertains to June 2012:

-Calculate the rate variance for variable setup overhead costs.

-Calculate the rate variance for variable setup overhead costs.

(Multiple Choice)

4.8/5 (38)

Briefly explain why a favourable variable overhead rate variance may not always be desireable.

(Essay)

4.9/5 (35)

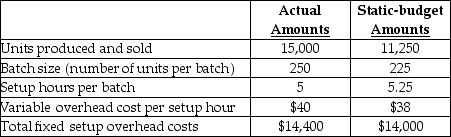

Answer the following question(s) using the information below.

Munoz Inc. produces a special line of plastic toy racing cars in batches. To manufacture a batch of the cars Munoz Inc. must setup the machines and molds. Setup costs are batch-level costs because they are associated with batches rather than individual units of products. A separate Setup Department is responsible for setting up machines and molds for different styles of car.

Setup overhead costs consist of some costs that are variable and some costs that are fixed with respect to the number of setup hours. The following information pertains to June 2012:

-Calculate the rate variance for fixed setup overhead costs.

-Calculate the rate variance for fixed setup overhead costs.

(Multiple Choice)

4.9/5 (34)

Human capital refers to the intangible skills provided by people and is an inventoriable cost under GAAP.

(True/False)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)