Deck 9: Profit Maximization in Perfectly Competitive Markets

Full screen (f)

Question

Question

Question

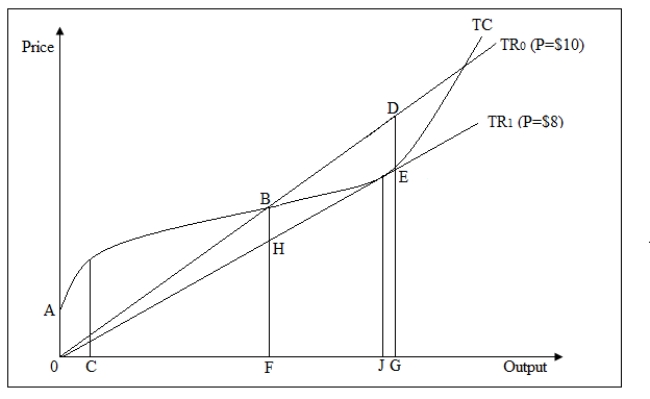

Use the following figure to answer the question : Figure 9-1 : shows the total cost and total revenue for a firm when it prices its products at $8 and $10.

Refer to Figure 9-1.At a price of $10,the profit maximizing level of output for the firm is _____.

A)OA

B)OC

C)OF

D)OG

Refer to Figure 9-1.At a price of $10,the profit maximizing level of output for the firm is _____.

A)OA

B)OC

C)OF

D)OG

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

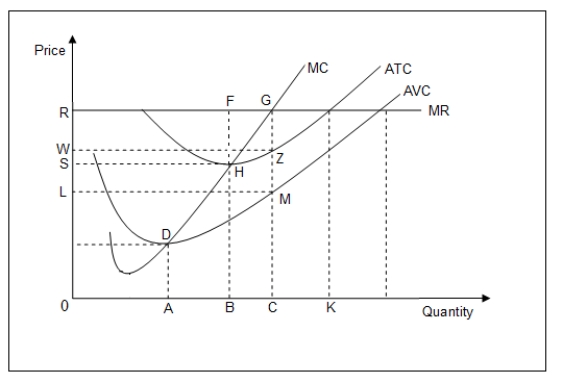

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.At the output level OB,total profits equal the area given by _____.

A)FTDE

B)GMLR

C)FHSR

D)FBOR

Refer to Figure 9-3.At the output level OB,total profits equal the area given by _____.

A)FTDE

B)GMLR

C)FHSR

D)FBOR

Question

Use the following figure to answer the question : Figure 9-1 : shows the total cost and total revenue for a firm when it prices its products at $8 and $10.

In Figure 9-1,if the market price fell to $8 the firm would:

A)decrease production to OJ and would be operating at a loss.

B)decrease production to OJ and would be earning a normal return.

C)decrease production to OF where it would break even.

D)incur losses and shut down.

In Figure 9-1,if the market price fell to $8 the firm would:

A)decrease production to OJ and would be operating at a loss.

B)decrease production to OJ and would be earning a normal return.

C)decrease production to OF where it would break even.

D)incur losses and shut down.

Question

Question

Use the following figure to answer the question : Figure 9-1 : shows the total cost and total revenue for a firm when it prices its products at $8 and $10.

Refer to Figure 9-1.When the firm is producing the profit-maximizing level of output at a price of $10:

A)total fixed costs are OA.

B)economic profits equal BH.

C)average cost equals DG divided by OG.

D)total cost is minimized at B.

Refer to Figure 9-1.When the firm is producing the profit-maximizing level of output at a price of $10:

A)total fixed costs are OA.

B)economic profits equal BH.

C)average cost equals DG divided by OG.

D)total cost is minimized at B.

Question

Question

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.At the output level OC,average fixed cost is equal to _____.

A)ZM

B)GZ

C)GM

D)MC

Refer to Figure 9-3.At the output level OC,average fixed cost is equal to _____.

A)ZM

B)GZ

C)GM

D)MC

Question

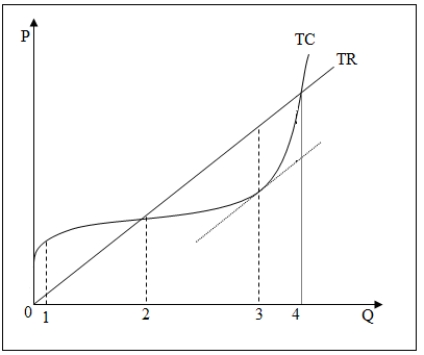

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

Refer to Figure 9-2.At which of the following output levels is the firm incurring its highest loss?

A)1 unit

B)2 units

C)3 units

D)4 units

Refer to Figure 9-2.At which of the following output levels is the firm incurring its highest loss?

A)1 unit

B)2 units

C)3 units

D)4 units

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.Assuming that price at 0R is $10,the profit maximizing level of output for the firm is _____.

A)OA where marginal cost just covers AVC

B)OB where average profit per unit is the greatest

C)OC where marginal cost equals the $10 price

D)OK where average cost equals marginal revenue and the firm earns a normal rate of return

Refer to Figure 9-3.Assuming that price at 0R is $10,the profit maximizing level of output for the firm is _____.

A)OA where marginal cost just covers AVC

B)OB where average profit per unit is the greatest

C)OC where marginal cost equals the $10 price

D)OK where average cost equals marginal revenue and the firm earns a normal rate of return

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.At the profit-maximizing level of output:

A)the firm is earning economic profit.

B)profits per unit are the highest.

C)profit equals ZC.

D)costs exceed revenue.

Refer to Figure 9-3.At the profit-maximizing level of output:

A)the firm is earning economic profit.

B)profits per unit are the highest.

C)profit equals ZC.

D)costs exceed revenue.

Question

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

At the profit-maximizing level of output in Figure 9-3,the profit of the firm is equal to the area given by _____.

A)RLMG

B)RGZW

C)RGCO

D)RGHS

At the profit-maximizing level of output in Figure 9-3,the profit of the firm is equal to the area given by _____.

A)RLMG

B)RGZW

C)RGCO

D)RGHS

Question

Question

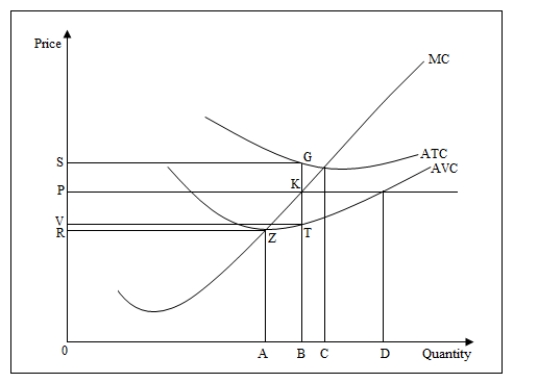

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.At a price of $P,the firm will produce the output level _____.

A)OA where marginal cost just covers AVC

B)OB where marginal cost equals the price

C)OC where marginal cost equals ATC

D)OD where the price just covers AVC

Refer to Figure 9-4.At a price of $P,the firm will produce the output level _____.

A)OA where marginal cost just covers AVC

B)OB where marginal cost equals the price

C)OC where marginal cost equals ATC

D)OD where the price just covers AVC

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

At the output level of OC in Figure 9-3,average profit per unit of output is equal to _____.

A)GZ

B)MG

C)ZM

D)GC

At the output level of OC in Figure 9-3,average profit per unit of output is equal to _____.

A)GZ

B)MG

C)ZM

D)GC

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The firm's average fixed cost at the output level OB is _____.

A)KT

B)GT

C)GB

D)GK

Refer to Figure 9-4.The firm's average fixed cost at the output level OB is _____.

A)KT

B)GT

C)GB

D)GK

Question

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

Refer to Figure 9-2.The firm's profits are positive:

A)from output level 1 to 2.

B)only at output level 2.

C)from output level 2 to 4.

D)only at output level 1.

Refer to Figure 9-2.The firm's profits are positive:

A)from output level 1 to 2.

B)only at output level 2.

C)from output level 2 to 4.

D)only at output level 1.

Question

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

Refer to Figure 9-2.At which of the following levels of output is the firm maximizing profit?

A)1 unit

B)2 units

C)3 units

D)4 units

Refer to Figure 9-2.At which of the following levels of output is the firm maximizing profit?

A)1 unit

B)2 units

C)3 units

D)4 units

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

In Figure 9-3,maximum profit per unit is equal to _____.

A)GZ

B)ZM

C)GM

D)FH

In Figure 9-3,maximum profit per unit is equal to _____.

A)GZ

B)ZM

C)GM

D)FH

Question

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.If the market price is $10,average revenue _____.

A)is greater than $10

B)is less than $10

C)equals $10

D)is equal to $10 - GZ

Refer to Figure 9-3.If the market price is $10,average revenue _____.

A)is greater than $10

B)is less than $10

C)equals $10

D)is equal to $10 - GZ

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.If the firm chooses to shut down when the market price is $P,what is the loss it would incur?

A)KTVP

B)GTVS

C)GKPS

D)TBOV

Refer to Figure 9-4.If the firm chooses to shut down when the market price is $P,what is the loss it would incur?

A)KTVP

B)GTVS

C)GKPS

D)TBOV

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The total revenue for the firm at the output level OB is _____.

A)OVTB

B)OSGB

C)OPKB

D)GTVS

Refer to Figure 9-4.The total revenue for the firm at the output level OB is _____.

A)OVTB

B)OSGB

C)OPKB

D)GTVS

Question

Question

Question

Question

Question

Question

Question

Question

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.Given that the market price is $P,the firm will be operating at a loss of _____.

A)TBOV

B)RZOA

C)KTVP

D)GKPS

Refer to Figure 9-4.Given that the market price is $P,the firm will be operating at a loss of _____.

A)TBOV

B)RZOA

C)KTVP

D)GKPS

Question

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.At the output level OB the total fixed cost is equal to _____.

A)TBOV

B)KTVP

C)GKPS

D)GTVS

Refer to Figure 9-4.At the output level OB the total fixed cost is equal to _____.

A)TBOV

B)KTVP

C)GKPS

D)GTVS

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The firm's average variable cost at the output level OB is _____.

A)BG

B)GT

C)BT

D)BK

Refer to Figure 9-4.The firm's average variable cost at the output level OB is _____.

A)BG

B)GT

C)BT

D)BK

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The total variable cost for the firm at output level OB is _____.

A)BT

B)BKPO

C)BK

D)BTVO

Refer to Figure 9-4.The total variable cost for the firm at output level OB is _____.

A)BT

B)BKPO

C)BK

D)BTVO

Question

Question

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The firm should shut down if the price falls to _____.

A)OP

B)OR

C)OS

D)OV

Refer to Figure 9-4.The firm should shut down if the price falls to _____.

A)OP

B)OR

C)OS

D)OV

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/99

Play

Full screen (f)

Deck 9: Profit Maximization in Perfectly Competitive Markets

1

The survivor principle in competitive markets implies that:

A)the outcome of a competitive market will not be profit-maximizing.

B)profit maximization need not be the only objective of a firm.

C)all firms follow the objective of profit maximization.

D)firms that do not undertake profit maximization will be driven out of the market.

A)the outcome of a competitive market will not be profit-maximizing.

B)profit maximization need not be the only objective of a firm.

C)all firms follow the objective of profit maximization.

D)firms that do not undertake profit maximization will be driven out of the market.

firms that do not undertake profit maximization will be driven out of the market.

2

Resources are not free to move into and out of an industry when:

A)there are no differential impediments across firms in the mobility of resources.

B)a firm experiences economies of scale.

C)an incumbent firm has an exclusive government patent.

D)firms are price takers.

A)there are no differential impediments across firms in the mobility of resources.

B)a firm experiences economies of scale.

C)an incumbent firm has an exclusive government patent.

D)firms are price takers.

an incumbent firm has an exclusive government patent.

3

Use the following figure to answer the question : Figure 9-1 : shows the total cost and total revenue for a firm when it prices its products at $8 and $10.

Refer to Figure 9-1.At a price of $10,the profit maximizing level of output for the firm is _____.

A)OA

B)OC

C)OF

D)OG

Refer to Figure 9-1.At a price of $10,the profit maximizing level of output for the firm is _____.

A)OA

B)OC

C)OF

D)OG

OG

4

Which of the following is an assumption in the model of perfect competition?

A)The firms in a competitive industry produce a homogeneous product.

B)The firms in a competitive industry actively compete with each other by advertising.

C)There are no natural impediments to entry in a competitive industry,but there may be artificial impediments such as licensing.

D)The firms in a competitive industry have a decreasing short-run marginal cost curve.

A)The firms in a competitive industry produce a homogeneous product.

B)The firms in a competitive industry actively compete with each other by advertising.

C)There are no natural impediments to entry in a competitive industry,but there may be artificial impediments such as licensing.

D)The firms in a competitive industry have a decreasing short-run marginal cost curve.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

5

If firms in a perfectly competitive market produced dissimilar products:

A)the buyers in the market will be price takers.

B)price differentials will exist in equilibrium.

C)they will remain price takers.

D)price differentials between firms will be eliminated.

A)the buyers in the market will be price takers.

B)price differentials will exist in equilibrium.

C)they will remain price takers.

D)price differentials between firms will be eliminated.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

6

The competitive firm's demand curve is:

A)unit elastic over the relevant range of output.

B)perfectly elastic over the relevant range of output.

C)perfectly inelastic over the relevant range of output.

D)elastic above the market price and inelastic below the market price.

A)unit elastic over the relevant range of output.

B)perfectly elastic over the relevant range of output.

C)perfectly inelastic over the relevant range of output.

D)elastic above the market price and inelastic below the market price.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

7

According to the _____ principle,firms that do not approximate profit maximization will not succeed in competitive markets.

A)equity

B)successor

C)survivor

D)winner-takes-all

A)equity

B)successor

C)survivor

D)winner-takes-all

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

8

Assume that coffee shops operate in a perfectly competitive industry.A single coffee shop,Brick & Mortar,decides to charge an entrance fee in addition to charges for its coffee and pastry.Which of the following is most likely to happen?

A)Brick & Mortar can continue to charge the entrance fee in the long-run since there is free entry into the coffee shop industry.

B)As long as the coffee shop industry is perfectly competitive,customers will be willing to pay the extra charges.

C)Brick & Mortar will not be able to sustain the extra charges as customers will move to coffee shops that are cheaper.

D)Brick & Mortar can charge their customers extra because there are a large number of buyers and sellers in the coffee shop industry.

A)Brick & Mortar can continue to charge the entrance fee in the long-run since there is free entry into the coffee shop industry.

B)As long as the coffee shop industry is perfectly competitive,customers will be willing to pay the extra charges.

C)Brick & Mortar will not be able to sustain the extra charges as customers will move to coffee shops that are cheaper.

D)Brick & Mortar can charge their customers extra because there are a large number of buyers and sellers in the coffee shop industry.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

9

A perfectly competitive firm is a price taker.This implies that:

A)price does not change in a perfectly competitive market.

B)price is not determined by supply and demand in a competitive market.

C)price only changes when market conditions change.

D)output of a firm is the only factor that can change prices.

A)price does not change in a perfectly competitive market.

B)price is not determined by supply and demand in a competitive market.

C)price only changes when market conditions change.

D)output of a firm is the only factor that can change prices.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

10

For a perfectly competitive firm,the demand curve:

A)coincides with the marginal revenue curve.

B)is parallel to the vertical axis.

C)is upward sloping.

D)is convex to the origin.

A)coincides with the marginal revenue curve.

B)is parallel to the vertical axis.

C)is upward sloping.

D)is convex to the origin.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

11

Which one of the following is not an assumption of the competitive model?

A)Homogenous products

B)Unrestricted mobility of resources

C)Economies of scale

D)Perfect information

A)Homogenous products

B)Unrestricted mobility of resources

C)Economies of scale

D)Perfect information

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

12

Product homogeneity implies that consumers:

A)buy goods from the lowest-priced source.

B)know which seller produces the highest quality goods.

C)cannot easily decide which seller to buy from.

D)can judge quality easily by price.

A)buy goods from the lowest-priced source.

B)know which seller produces the highest quality goods.

C)cannot easily decide which seller to buy from.

D)can judge quality easily by price.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following will reduce the competitive nature of the agricultural industry?

A)There are restrictions on price volatility in the agricultural market.

B)The output of the agricultural industry is more or less homogeneous.

C)The number of farms across the country is relatively large.

D)There are no import and export restrictions on agricultural products.

A)There are restrictions on price volatility in the agricultural market.

B)The output of the agricultural industry is more or less homogeneous.

C)The number of farms across the country is relatively large.

D)There are no import and export restrictions on agricultural products.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

14

The model of perfect competition assumes that:

A)there is information asymmetry in the market.

B)individual suppliers face a downward sloping demand curve.

C)all goods in that market are homogeneous.

D)there are a small number of sellers in the market.

A)there is information asymmetry in the market.

B)individual suppliers face a downward sloping demand curve.

C)all goods in that market are homogeneous.

D)there are a small number of sellers in the market.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

15

A perfectly competitive firm faces a horizontal demand curve,which implies that:

A)the price in the market never changes.

B)the firm cannot affect price by any action it takes.

C)the quantity of output produced by the firm is indeterminate.

D)the firm makes zero accounting profits.

A)the price in the market never changes.

B)the firm cannot affect price by any action it takes.

C)the quantity of output produced by the firm is indeterminate.

D)the firm makes zero accounting profits.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

16

The demand curve of a perfectly competitive firm is determined by:

A)the quality of the goods the firm produces.

B)the intersection of the market demand and supply curves.

C)the reputation of the firm.

D)the price taking behavior in the market.

A)the quality of the goods the firm produces.

B)the intersection of the market demand and supply curves.

C)the reputation of the firm.

D)the price taking behavior in the market.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

17

The assumptions of perfect competition _____.

A)are satisfied in most real-world markets

B)do not readily apply to most real-world markets

C)are hardly ever satisfied and therefore make the study of perfect competition unwarranted

D)if satisfied,lead to equitable outcomes

A)are satisfied in most real-world markets

B)do not readily apply to most real-world markets

C)are hardly ever satisfied and therefore make the study of perfect competition unwarranted

D)if satisfied,lead to equitable outcomes

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

18

The competitive firm is known as a price taker because:

A)it sets the highest price it can charge.

B)it can vary its price based on variations in its cost.

C)it produces output at a level that minimizes its marginal cost.

D)it accepts the market price as a given.

A)it sets the highest price it can charge.

B)it can vary its price based on variations in its cost.

C)it produces output at a level that minimizes its marginal cost.

D)it accepts the market price as a given.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is true of the economic model of perfect competition?

A)All the assumptions of a competitive model are satisfied in almost all real-world markets.

B)The efficient outcomes of competitive markets hold only in theory and not empirically.

C)Perfect competition is characterized by its impersonal nature.

D)The outcome of perfect competition is equitable.

A)All the assumptions of a competitive model are satisfied in almost all real-world markets.

B)The efficient outcomes of competitive markets hold only in theory and not empirically.

C)Perfect competition is characterized by its impersonal nature.

D)The outcome of perfect competition is equitable.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

20

The perfectly competitive firm's demand curve is horizontal because:

A)the firm faces a constant-cost supply curve.

B)the demand for its goods is infinitely elastic.

C)firms in competitive industries collude and set the same prices.

D)the firm can change prices by varying its output.

A)the firm faces a constant-cost supply curve.

B)the demand for its goods is infinitely elastic.

C)firms in competitive industries collude and set the same prices.

D)the firm can change prices by varying its output.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

21

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.At the output level OB,total profits equal the area given by _____.

A)FTDE

B)GMLR

C)FHSR

D)FBOR

Refer to Figure 9-3.At the output level OB,total profits equal the area given by _____.

A)FTDE

B)GMLR

C)FHSR

D)FBOR

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

22

Use the following figure to answer the question : Figure 9-1 : shows the total cost and total revenue for a firm when it prices its products at $8 and $10.

In Figure 9-1,if the market price fell to $8 the firm would:

A)decrease production to OJ and would be operating at a loss.

B)decrease production to OJ and would be earning a normal return.

C)decrease production to OF where it would break even.

D)incur losses and shut down.

In Figure 9-1,if the market price fell to $8 the firm would:

A)decrease production to OJ and would be operating at a loss.

B)decrease production to OJ and would be earning a normal return.

C)decrease production to OF where it would break even.

D)incur losses and shut down.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

23

A competitive firm maximizes profit at the output level where:

A)the difference between price and average total cost is the largest.

B)the slope of the total revenue curve equals the slope of the total cost curve.

C)the average total cost equals marginal cost.

D)the marginal revenue exceeds marginal cost by the greatest amount.

A)the difference between price and average total cost is the largest.

B)the slope of the total revenue curve equals the slope of the total cost curve.

C)the average total cost equals marginal cost.

D)the marginal revenue exceeds marginal cost by the greatest amount.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

24

Use the following figure to answer the question : Figure 9-1 : shows the total cost and total revenue for a firm when it prices its products at $8 and $10.

Refer to Figure 9-1.When the firm is producing the profit-maximizing level of output at a price of $10:

A)total fixed costs are OA.

B)economic profits equal BH.

C)average cost equals DG divided by OG.

D)total cost is minimized at B.

Refer to Figure 9-1.When the firm is producing the profit-maximizing level of output at a price of $10:

A)total fixed costs are OA.

B)economic profits equal BH.

C)average cost equals DG divided by OG.

D)total cost is minimized at B.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

25

The perfectly competitive firm maximizes profits by producing at the rate of output where:

A)marginal revenue and marginal cost are equal.

B)marginal revenue exceeds marginal cost by the greatest amount.

C)the profit per unit is the highest.

D)marginal cost is at its minimum.

A)marginal revenue and marginal cost are equal.

B)marginal revenue exceeds marginal cost by the greatest amount.

C)the profit per unit is the highest.

D)marginal cost is at its minimum.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

26

Profits are maximized at the output level where:

A)marginal revenue equals marginal cost.

B)price equals average total cost.

C)price is greater than marginal cost.

D)marginal cost equals average total cost.

A)marginal revenue equals marginal cost.

B)price equals average total cost.

C)price is greater than marginal cost.

D)marginal cost equals average total cost.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

27

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.At the output level OC,average fixed cost is equal to _____.

A)ZM

B)GZ

C)GM

D)MC

Refer to Figure 9-3.At the output level OC,average fixed cost is equal to _____.

A)ZM

B)GZ

C)GM

D)MC

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

28

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

Refer to Figure 9-2.At which of the following output levels is the firm incurring its highest loss?

A)1 unit

B)2 units

C)3 units

D)4 units

Refer to Figure 9-2.At which of the following output levels is the firm incurring its highest loss?

A)1 unit

B)2 units

C)3 units

D)4 units

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

29

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.Assuming that price at 0R is $10,the profit maximizing level of output for the firm is _____.

A)OA where marginal cost just covers AVC

B)OB where average profit per unit is the greatest

C)OC where marginal cost equals the $10 price

D)OK where average cost equals marginal revenue and the firm earns a normal rate of return

Refer to Figure 9-3.Assuming that price at 0R is $10,the profit maximizing level of output for the firm is _____.

A)OA where marginal cost just covers AVC

B)OB where average profit per unit is the greatest

C)OC where marginal cost equals the $10 price

D)OK where average cost equals marginal revenue and the firm earns a normal rate of return

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

30

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.At the profit-maximizing level of output:

A)the firm is earning economic profit.

B)profits per unit are the highest.

C)profit equals ZC.

D)costs exceed revenue.

Refer to Figure 9-3.At the profit-maximizing level of output:

A)the firm is earning economic profit.

B)profits per unit are the highest.

C)profit equals ZC.

D)costs exceed revenue.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

31

The competitive firm maximizes its profit by operating at the point where _____ and price is greater than average variable cost.

A)average cost is at a minimum

B)total revenue is at a maximum

C)profit per unit is at a maximum

D)marginal cost equals price

A)average cost is at a minimum

B)total revenue is at a maximum

C)profit per unit is at a maximum

D)marginal cost equals price

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

32

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

At the profit-maximizing level of output in Figure 9-3,the profit of the firm is equal to the area given by _____.

A)RLMG

B)RGZW

C)RGCO

D)RGHS

At the profit-maximizing level of output in Figure 9-3,the profit of the firm is equal to the area given by _____.

A)RLMG

B)RGZW

C)RGCO

D)RGHS

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

33

A profit-maximizing firm expands output until marginal revenue equals the _____ of producing the last unit.

A)marginal cost

B)average variable cost

C)average total cost

D)average fixed cost

A)marginal cost

B)average variable cost

C)average total cost

D)average fixed cost

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

34

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.At a price of $P,the firm will produce the output level _____.

A)OA where marginal cost just covers AVC

B)OB where marginal cost equals the price

C)OC where marginal cost equals ATC

D)OD where the price just covers AVC

Refer to Figure 9-4.At a price of $P,the firm will produce the output level _____.

A)OA where marginal cost just covers AVC

B)OB where marginal cost equals the price

C)OC where marginal cost equals ATC

D)OD where the price just covers AVC

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

35

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

At the output level of OC in Figure 9-3,average profit per unit of output is equal to _____.

A)GZ

B)MG

C)ZM

D)GC

At the output level of OC in Figure 9-3,average profit per unit of output is equal to _____.

A)GZ

B)MG

C)ZM

D)GC

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

36

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The firm's average fixed cost at the output level OB is _____.

A)KT

B)GT

C)GB

D)GK

Refer to Figure 9-4.The firm's average fixed cost at the output level OB is _____.

A)KT

B)GT

C)GB

D)GK

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

37

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

Refer to Figure 9-2.The firm's profits are positive:

A)from output level 1 to 2.

B)only at output level 2.

C)from output level 2 to 4.

D)only at output level 1.

Refer to Figure 9-2.The firm's profits are positive:

A)from output level 1 to 2.

B)only at output level 2.

C)from output level 2 to 4.

D)only at output level 1.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

38

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

Refer to Figure 9-2.At which of the following levels of output is the firm maximizing profit?

A)1 unit

B)2 units

C)3 units

D)4 units

Refer to Figure 9-2.At which of the following levels of output is the firm maximizing profit?

A)1 unit

B)2 units

C)3 units

D)4 units

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

39

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

In Figure 9-3,maximum profit per unit is equal to _____.

A)GZ

B)ZM

C)GM

D)FH

In Figure 9-3,maximum profit per unit is equal to _____.

A)GZ

B)ZM

C)GM

D)FH

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

40

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.

Refer to Figure 9-3.If the market price is $10,average revenue _____.

A)is greater than $10

B)is less than $10

C)equals $10

D)is equal to $10 - GZ

Refer to Figure 9-3.If the market price is $10,average revenue _____.

A)is greater than $10

B)is less than $10

C)equals $10

D)is equal to $10 - GZ

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

41

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.If the firm chooses to shut down when the market price is $P,what is the loss it would incur?

A)KTVP

B)GTVS

C)GKPS

D)TBOV

Refer to Figure 9-4.If the firm chooses to shut down when the market price is $P,what is the loss it would incur?

A)KTVP

B)GTVS

C)GKPS

D)TBOV

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

42

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The total revenue for the firm at the output level OB is _____.

A)OVTB

B)OSGB

C)OPKB

D)GTVS

Refer to Figure 9-4.The total revenue for the firm at the output level OB is _____.

A)OVTB

B)OSGB

C)OPKB

D)GTVS

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

43

Following a significant decrease in the price of a variable input,at the initial output level:

A)marginal revenue is higher than average revenue.

B)marginal cost is higher than marginal revenue.

C)marginal cost is lower than average revenue.

D)marginal cost is still equal to marginal revenue.

A)marginal revenue is higher than average revenue.

B)marginal cost is higher than marginal revenue.

C)marginal cost is lower than average revenue.

D)marginal cost is still equal to marginal revenue.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

44

In the short-run,if the price falls,the firm will respond by:

A)liquidating its assets and shutting down.

B)producing at the output level where average variable cost is equal to marginal revenue.

C)reducing output along its marginal cost curve as long as marginal revenue exceeds average variable cost.

D)increasing its output in order to sell higher quantities.

A)liquidating its assets and shutting down.

B)producing at the output level where average variable cost is equal to marginal revenue.

C)reducing output along its marginal cost curve as long as marginal revenue exceeds average variable cost.

D)increasing its output in order to sell higher quantities.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

45

In the short-run,if a competitive firm finds itself operating at a loss,it will:

A)have to shut down and exit the market.

B)continue to operate as long as price is greater than average variable cost.

C)liquidate all its assets to ensure cash flow.

D)reduce the size of its plant to lower fixed costs.

A)have to shut down and exit the market.

B)continue to operate as long as price is greater than average variable cost.

C)liquidate all its assets to ensure cash flow.

D)reduce the size of its plant to lower fixed costs.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

46

Assume that labor is the variable input for a firm.Which of the following will occur if the wage rate increases?

A)Its average variable cost,average fixed cost,average total cost,and marginal costs will increase.

B)Its average variable cost and average total costs will increase and profits will decrease.

C)Its marginal cost,average total costs,and output will increase.

D)Its marginal cost and average variable costs will increase.

A)Its average variable cost,average fixed cost,average total cost,and marginal costs will increase.

B)Its average variable cost and average total costs will increase and profits will decrease.

C)Its marginal cost,average total costs,and output will increase.

D)Its marginal cost and average variable costs will increase.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

47

If market price is below a competitive firm's average total cost,the firm should:

A)shut down only if the price is above its average variable cost.

B)shut down immediately.

C)remain open as long as its average revenue is greater than its average variable cost.

D)expand output in the short-run and expand its production capacity.

A)shut down only if the price is above its average variable cost.

B)shut down immediately.

C)remain open as long as its average revenue is greater than its average variable cost.

D)expand output in the short-run and expand its production capacity.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

48

Abe's Taxi Company operates in a perfectly competitive market.Gasoline is a variable input in the taxi services industry.As the price of gasoline decreases,the short-run marginal cost curve for Abe's Taxi Company:

A)shifts up and to the left.

B)shifts down and to the right.

C)remains unchanged.

D)becomes flatter.

A)shifts up and to the left.

B)shifts down and to the right.

C)remains unchanged.

D)becomes flatter.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

49

A significant decrease in the price of a variable input causes the:

A)marginal,average,and total cost curves to shift downward.

B)average total cost curve to shift downward,causing a fall in output.

C)average variable cost curve to shift downward while leaving the output level unchanged.

D)marginal cost curve to shift downward.

A)marginal,average,and total cost curves to shift downward.

B)average total cost curve to shift downward,causing a fall in output.

C)average variable cost curve to shift downward while leaving the output level unchanged.

D)marginal cost curve to shift downward.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

50

The supply curve of a competitive firm in the short-run is:

A)the marginal cost curve.

B)the marginal cost curve above the minimum of average variable cost.

C)the marginal cost curve above the minimum of average cost.

D)the negatively sloped portion of the marginal cost curve.

A)the marginal cost curve.

B)the marginal cost curve above the minimum of average variable cost.

C)the marginal cost curve above the minimum of average cost.

D)the negatively sloped portion of the marginal cost curve.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

51

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.Given that the market price is $P,the firm will be operating at a loss of _____.

A)TBOV

B)RZOA

C)KTVP

D)GKPS

Refer to Figure 9-4.Given that the market price is $P,the firm will be operating at a loss of _____.

A)TBOV

B)RZOA

C)KTVP

D)GKPS

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

52

The short-run supply curve for a perfectly competitive industry is:

A)downward sloping because of the law of diminishing marginal returns.

B)derived by summing the individual firms' marginal cost curves horizontally.

C)perfectly elastic in the case of homogeneous products.

D)the negatively sloped portion of the marginal cost curve.

A)downward sloping because of the law of diminishing marginal returns.

B)derived by summing the individual firms' marginal cost curves horizontally.

C)perfectly elastic in the case of homogeneous products.

D)the negatively sloped portion of the marginal cost curve.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

53

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.At the output level OB the total fixed cost is equal to _____.

A)TBOV

B)KTVP

C)GKPS

D)GTVS

Refer to Figure 9-4.At the output level OB the total fixed cost is equal to _____.

A)TBOV

B)KTVP

C)GKPS

D)GTVS

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

54

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The firm's average variable cost at the output level OB is _____.

A)BG

B)GT

C)BT

D)BK

Refer to Figure 9-4.The firm's average variable cost at the output level OB is _____.

A)BG

B)GT

C)BT

D)BK

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

55

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The total variable cost for the firm at output level OB is _____.

A)BT

B)BKPO

C)BK

D)BTVO

Refer to Figure 9-4.The total variable cost for the firm at output level OB is _____.

A)BT

B)BKPO

C)BK

D)BTVO

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

56

In a perfectly competitive market,if the product price remains unchanged,a fall in the price of an input used by a firm will:

A)cause the firm to substitute away from this input.

B)reduce the quantity of output it produces.

C)shift the marginal cost curve downward.

D)reduce the price of the product.

A)cause the firm to substitute away from this input.

B)reduce the quantity of output it produces.

C)shift the marginal cost curve downward.

D)reduce the price of the product.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

57

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.

Refer to Figure 9-4.The firm should shut down if the price falls to _____.

A)OP

B)OR

C)OS

D)OV

Refer to Figure 9-4.The firm should shut down if the price falls to _____.

A)OP

B)OR

C)OS

D)OV

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

58

The short-run supply curve for the firm operating in a perfectly competitive industry is:

A)its marginal cost curve.

B)its marginal cost curve above the minimum of average variable cost.

C)its marginal cost curve above the minimum of average total cost.

D)the average variable cost curve above average revenue curve.

A)its marginal cost curve.

B)its marginal cost curve above the minimum of average variable cost.

C)its marginal cost curve above the minimum of average total cost.

D)the average variable cost curve above average revenue curve.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

59

During the 1970s,oil prices reached historical highs,causing many competitive industries to reduce the supply of goods and services.Which of the following is the most likely explanation for this reduction in supply?

A)The total fixed cost of the firms would have increased due to the higher price of oil.

B)The marginal cost curves of the firms most likely shifted upward.

C)The supply curves of firms may have shifted downward.

D)The average total cost of these firms mostly likely shifted downward due to the high inflation.

A)The total fixed cost of the firms would have increased due to the higher price of oil.

B)The marginal cost curves of the firms most likely shifted upward.

C)The supply curves of firms may have shifted downward.

D)The average total cost of these firms mostly likely shifted downward due to the high inflation.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

60

The perfectly competitive firm minimizes losses by shutting down whenever:

A)price is below average fixed costs.

B)price is below the minimum point of the average cost curve.

C)total variable costs are greater than total fixed costs.

D)price is below the minimum point of the average variable cost curve.

A)price is below average fixed costs.

B)price is below the minimum point of the average cost curve.

C)total variable costs are greater than total fixed costs.

D)price is below the minimum point of the average variable cost curve.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

61

In the long-run,firms in a competitive industry earn only a normal rate of return because:

A)decreasing returns to scale causes per unit costs to rise.

B)input prices will rise in the long-run and eliminate abnormal profits.

C)entry of new firms will eliminate abnormal profits.

D)profit per unit declines in the long-run.

A)decreasing returns to scale causes per unit costs to rise.

B)input prices will rise in the long-run and eliminate abnormal profits.

C)entry of new firms will eliminate abnormal profits.

D)profit per unit declines in the long-run.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

62

The short-run supply curve for a perfectly competitive industry:

A)is less elastic than the long-run industry supply curve.

B)is derived by vertically summing the individual firms' marginal cost curves.

C)reflects zero economic profits at all points on the curve.

D)is typically upward sloping.

A)is less elastic than the long-run industry supply curve.

B)is derived by vertically summing the individual firms' marginal cost curves.

C)reflects zero economic profits at all points on the curve.

D)is typically upward sloping.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

63

The short-run supply curve for a competitive industry:

A)is subject to the law of diminishing returns.

B)is the industry's marginal cost curve.

C)coincides with the marginal revenue curve.

D)is horizontal because there are many buyers and sellers.

A)is subject to the law of diminishing returns.

B)is the industry's marginal cost curve.

C)coincides with the marginal revenue curve.

D)is horizontal because there are many buyers and sellers.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

64

Zero economic profit occurs when:

A)price equals minimum average variable cost.

B)a firm has existed for long enough to make normal profit.

C)price equals long-run average cost.

D)a firm operates at the minimum of its long-run marginal cost curve.

A)price equals minimum average variable cost.

B)a firm has existed for long enough to make normal profit.

C)price equals long-run average cost.

D)a firm operates at the minimum of its long-run marginal cost curve.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

65

As long as there is free entry into a market:

A)firms in that market can sustain prices above average total cost.

B)firms in that market can maintain market power.

C)economic profits are not sustainable.

D)accounting profits will be zero.

A)firms in that market can sustain prices above average total cost.

B)firms in that market can maintain market power.

C)economic profits are not sustainable.

D)accounting profits will be zero.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

66

The short-run supply curve for a competitive industry is upward-sloping because:

A)firms must pay more for inputs as more are hired./firms must incur higher costs the more inputs they hire.

B)the efficiency of the variable inputs decreases as more such inputs are employed in production.

C)new firms enter the industry as product prices increase.

D)of the law of diminishing marginal utility.

A)firms must pay more for inputs as more are hired./firms must incur higher costs the more inputs they hire.

B)the efficiency of the variable inputs decreases as more such inputs are employed in production.

C)new firms enter the industry as product prices increase.

D)of the law of diminishing marginal utility.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is true of a constant cost industry?

A)Along the industry's long-run supply curve,firms in the industry earn a positive economic profit.

B)The long-run supply curve for a constant cost industry is horizontal.

C)The industry's long-run supply curve is derived by horizontally summing the long-run supply curves of the individual firms.

D)In the long run,the industry experiences an increase in the price of inputs.

A)Along the industry's long-run supply curve,firms in the industry earn a positive economic profit.

B)The long-run supply curve for a constant cost industry is horizontal.

C)The industry's long-run supply curve is derived by horizontally summing the long-run supply curves of the individual firms.

D)In the long run,the industry experiences an increase in the price of inputs.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

68

Which of the following is true of a long-run competitive equilibrium?

A)The market has a horizontal long-run supply curve.

B)Inputs employed in the industry cannot earn more in other industries.

C)Firms in the market earn high abnormal profits.

D)Firms face constant input costs irrespective of the output level.

A)The market has a horizontal long-run supply curve.

B)Inputs employed in the industry cannot earn more in other industries.

C)Firms in the market earn high abnormal profits.

D)Firms face constant input costs irrespective of the output level.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

69

In an increasing-cost industry,the slope of the long-run supply curve is _____.

A)zero

B)negative

C)positive

D)infinity

A)zero

B)negative

C)positive

D)infinity

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

70

If a competitive industry is characterized by increasing cost,which of the following will occur in response to an unexpected increase in demand?

A)New firms will enter the industry.

B)Economic profit will remain zero.

C)Input prices will remain constant.

D)The price of the product will remain unchanged.

A)New firms will enter the industry.

B)Economic profit will remain zero.

C)Input prices will remain constant.

D)The price of the product will remain unchanged.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

71

If price remains above the average total cost for firms in a competitive industry:

A)existing firms will exit that industry.

B)new firms will enter that industry.

C)the number of firms in the industry will neither increase nor decrease.

D)the existing firms will be making zero economic profit.

A)existing firms will exit that industry.

B)new firms will enter that industry.

C)the number of firms in the industry will neither increase nor decrease.

D)the existing firms will be making zero economic profit.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

72

In a constant-cost industry,the slope of the long-run supply curve is _____.

A)zero

B)negative

C)positive

D)infinity

A)zero

B)negative

C)positive

D)infinity

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

73

In the long run,if the input procurement prices increase as the output supplied by firms in an industry rises:

A)the firms are operating in an increasing-cost industry.

B)the firms' profit margins will increase.

C)the firms are making positive economic profits.

D)the firms' cost curves shift will downward.

A)the firms are operating in an increasing-cost industry.

B)the firms' profit margins will increase.

C)the firms are making positive economic profits.

D)the firms' cost curves shift will downward.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following is a condition for long-run equilibrium in a competitive industry?

A)Each firm in the industry is earning zero economic profit.

B)The inputs employed in the industry earn less than they would had they been used elsewhere.

C)Each firm in the industry will produce that level of output at which marginal cost is the lowest.

D)The number of new entrants into the industry is positive.

A)Each firm in the industry is earning zero economic profit.

B)The inputs employed in the industry earn less than they would had they been used elsewhere.

C)Each firm in the industry will produce that level of output at which marginal cost is the lowest.

D)The number of new entrants into the industry is positive.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

75

Which of the following will occur in response to an unexpected increase in demand in a constant-cost,competitive industry?

A)Resources will move out of the industry.

B)The output of the industry will remain constant.

C)The output will increase with input prices remaining unchanged

D)The existing firms will not be able to expand output sufficiently without incurring huge costs.

A)Resources will move out of the industry.

B)The output of the industry will remain constant.

C)The output will increase with input prices remaining unchanged

D)The existing firms will not be able to expand output sufficiently without incurring huge costs.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

76

At the profit maximizing level of output in a competitive industry,the firm is:

A)making economic profit.

B)losing money on each unit sold.

C)making zero accounting profit.

D)making abnormal profits

A)making economic profit.

B)losing money on each unit sold.

C)making zero accounting profit.

D)making abnormal profits

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

77

In an increasing cost industry,as output increases:

A)firms' cost curves shift downward.

B)input prices increase.

C)profit per unit increases.

D)the price of the product in the market increases.

A)firms' cost curves shift downward.

B)input prices increase.

C)profit per unit increases.

D)the price of the product in the market increases.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

78

Suppose a constant-cost competitive industry produces widgets using labor and capital in fixed proportions.A firm in the industry faces:

A)a vertical supply curve for labor and capital.

B)a downward sloping supply curve for labor and capital.

C)a horizontal supply curve for labor and capital.

D)an upward sloping supply curve for labor and capital.

A)a vertical supply curve for labor and capital.

B)a downward sloping supply curve for labor and capital.

C)a horizontal supply curve for labor and capital.

D)an upward sloping supply curve for labor and capital.

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

79

The slope of the long-run supply curve in a decreasing-cost industry is _____.

A)zero

B)negative

C)positive

D)infinite

A)zero

B)negative

C)positive

D)infinite

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

80

The short-run supply curve for a competitive industry is derived by summing the _____ for each firm in the industry.

A)portion of the marginal cost curves above average variable cost

B)upward sloping portion of the average variable cost curve

C)downward sloping portions of the marginal cost curve

D)upward sloping portion of the average total cost curve

A)portion of the marginal cost curves above average variable cost

B)upward sloping portion of the average variable cost curve

C)downward sloping portions of the marginal cost curve

D)upward sloping portion of the average total cost curve

Unlock Deck

Unlock for access to all 99 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 99 flashcards in this deck.