Exam 9: Profit Maximization in Perfectly Competitive Markets

Exam 1: An Introduction to Microeconomics72 Questions

Exam 2: Supply and Demand97 Questions

Exam 3: The Theory of Consumer Choice97 Questions

Exam 4: Individual and Market Demand99 Questions

Exam 5: Using Consumer Choice Theory75 Questions

Exam 6: Exchange, Efficiency, and Prices82 Questions

Exam 7: Production112 Questions

Exam 8: The Cost of Production121 Questions

Exam 9: Profit Maximization in Perfectly Competitive Markets99 Questions

Exam 10: Using the Competitive Model82 Questions

Exam 11: Monopoly115 Questions

Exam 12: Product Pricing With Monopoly Power88 Questions

Exam 13: Monopolistic Competition and Oligopoly98 Questions

Exam 14: Game Theory and the Economics of Information88 Questions

Exam 15: Using Noncompetitive Market Models77 Questions

Exam 16: Employment and Pricing of Inputs100 Questions

Exam 17: Wages, Rent, Interest, and Profit92 Questions

Exam 18: Using Input Market Analysis83 Questions

Exam 19: General Equilibrium Analysis and Economic Efficiency93 Questions

Exam 20: Public Goods and Externalities101 Questions

Select questions type

Which of the following is a condition for long-run equilibrium in a competitive industry?

Free

(Multiple Choice)

4.9/5  (34)

(34)

Correct Answer: Verified

Verified

A

Explain the difference between diminishing marginal returns to factor and a decreasing-cost industry.

Free

(Essay)

4.8/5 (39)

Correct Answer:Verified

The upward slope of the short-run industry supply curve (the portion of the marginal cost curve above the average variable cost curve)is due to diminishing marginal returns.Diminishing marginal returns operates in the short-run when one input is fixed.It implies that as the employment of an input is increased,the additional output that is produced with the help of the additional input decreases.

A decreasing-cost industry is one where the long-run supply curve is downward sloping.This means that output expands at a lower cost.Lower cost is due to the fall in input prices as more is demanded.

The short-run supply curve for a competitive industry:

Free

(Multiple Choice)

4.8/5 (28)

Correct Answer:Verified

A

According to the _____ principle,firms that do not approximate profit maximization will not succeed in competitive markets.

(Multiple Choice)

4.8/5 (36)

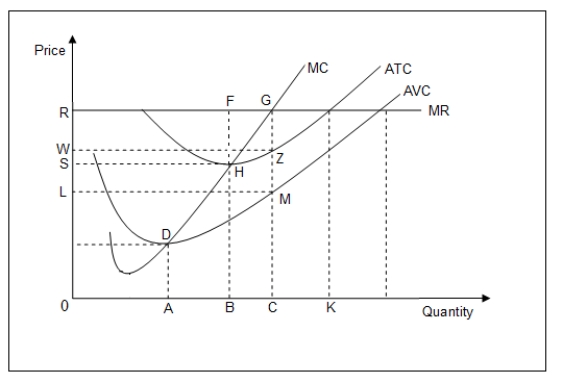

Use the following figure to answer the question : Figure 9-3 : shows the marginal cost curve,average total cost curve,average variable cost curve,and marginal revenue curve for a firm for different levels of output.  -At the profit-maximizing level of output in Figure 9-3,the profit of the firm is equal to the area given by _____.

-At the profit-maximizing level of output in Figure 9-3,the profit of the firm is equal to the area given by _____.

(Multiple Choice)

4.8/5 (34)

Which of the following is true of a long-run competitive equilibrium?

(Multiple Choice)

4.9/5 (44)

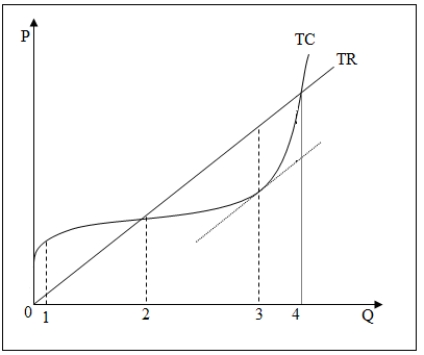

Use the following figure to answer the question : Figure 9-2 : shows the total cost and total revenue curves for a firm.

-Refer to Figure 9-2.The firm's profits are positive:

-Refer to Figure 9-2.The firm's profits are positive:

(Multiple Choice)

4.8/5 (29)

On the graphs below,demonstrate the circumstances that would prevail in a perfectly competitive market where the representative firm is experiencing economic losses.Draw the relevant cost curves (marginal,average total,and average variable costs;use U-shaped curves),the marginal revenue curve,and the market supply and demand curves.Shade in the area of total revenue and the area of economic loss.As you've drawn it,will the firm shut down in the short-run or choose to continue production? Explain your answer.

(Essay)

4.9/5 (25)

The slope of the long-run supply curve in a decreasing-cost industry is _____.

(Multiple Choice)

4.8/5 (33)

In an increasing-cost industry,the slope of the long-run supply curve is _____.

(Multiple Choice)

5.0/5 (22)

In a constant-cost industry,the slope of the long-run supply curve is _____.

(Multiple Choice)

5.0/5 (37)

Assume a competitive industry produces widgets using labor and capital in fixed proportions.Both input supply curves slope upward.The government considers the equilibrium price of widgets to be too high and imposes a price ceiling that is below the equilibrium price.Which of the following is most likely to occur?

(Multiple Choice)

4.8/5 (32)

Which of the following is constant along the industry long-run supply curve?

(Multiple Choice)

5.0/5 (33)

The short-run supply curve for the firm operating in a perfectly competitive industry is:

(Multiple Choice)

4.9/5 (36)

If a competitive industry is characterized by increasing cost,which of the following will occur in response to an unexpected increase in demand?

(Multiple Choice)

4.8/5 (38)

Following a significant decrease in the price of a variable input,at the initial output level:

(Multiple Choice)

4.8/5 (28)

Eggs,which are standardized products,are sold within a city at higher prices than in the suburbs.Given that firms in the city are able to sustain the higher prices but do not make higher profits than firms in the suburbs,this means that:

(Multiple Choice)

4.8/5 (32)

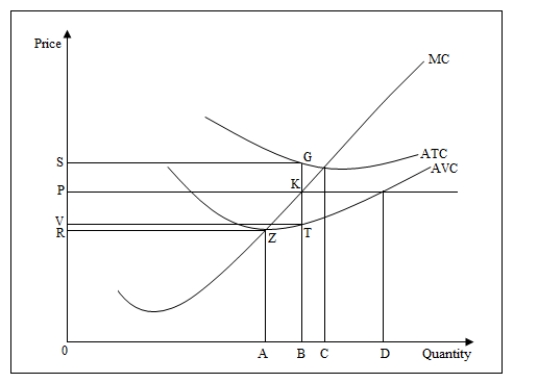

Use the following figure to answer the question : Figure 9-4 : shows the marginal cost curve,the average cost curve,the average variable cost curve,and the demand curve for a firm over different levels of output.The market price is $P.  -Refer to Figure 9-4.At the output level OB the total fixed cost is equal to _____.

-Refer to Figure 9-4.At the output level OB the total fixed cost is equal to _____.

(Multiple Choice)

4.9/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)