Deck 12: Perfect Competition and the Supply Curve

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

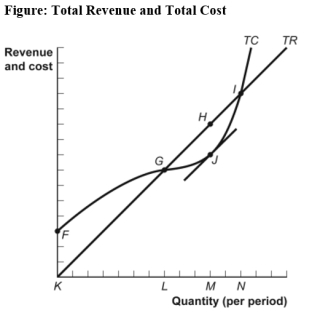

Use the following to answer question 64:

(Figure: Total Revenue and Total Cost)Use Figure: Total Revenue and Total Cost.The MOST profitable level of output occurs at quantity:

A) F.

B) K.

C) L.

D) M.

(Figure: Total Revenue and Total Cost)Use Figure: Total Revenue and Total Cost.The MOST profitable level of output occurs at quantity:

A) F.

B) K.

C) L.

D) M.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/341

Play

Full screen (f)

Deck 12: Perfect Competition and the Supply Curve

1

Perfect competition is characterized by:

A) rivalry in advertising.

B) fierce quality competition.

C) the inability of any one firm to influence price.

D) widely recognized brands.

A) rivalry in advertising.

B) fierce quality competition.

C) the inability of any one firm to influence price.

D) widely recognized brands.

the inability of any one firm to influence price.

2

A perfectly competitive firm is a:

A) price-taker.

B) price searcher.

C) cost maximizer.

D) quantity taker.

A) price-taker.

B) price searcher.

C) cost maximizer.

D) quantity taker.

price-taker.

3

An assumption of the model of perfect competition is:

A) discrimination.

B) difficult entry and exit.

C) many buyers and sellers.

D) limited information.

A) discrimination.

B) difficult entry and exit.

C) many buyers and sellers.

D) limited information.

many buyers and sellers.

4

The assumptions of perfect competition imply that:

A) individuals in the market accept the market price as given.

B) individuals can influence the market price.

C) the price will be fair.

D) the price will be high.

A) individuals in the market accept the market price as given.

B) individuals can influence the market price.

C) the price will be fair.

D) the price will be high.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

5

Price-takers are individuals in a market who:

A) select a price from a wide range of alternatives.

B) select the lowest price available in a competitive market.

C) select the average of prices available in a competitive market.

D) have no ability to affect the price of a good in a market.

A) select a price from a wide range of alternatives.

B) select the lowest price available in a competitive market.

C) select the average of prices available in a competitive market.

D) have no ability to affect the price of a good in a market.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

6

One characteristic of a perfectly competitive market is that there are _____ sellers of the good or service.

A) one or two

B) a few

C) usually fewer than 10

D) many

A) one or two

B) a few

C) usually fewer than 10

D) many

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

7

Which statement is NOT a characteristic of a perfectly competitive industry?

A) Firms seek to maximize profits.

B) Profits may be positive in the short run.

C) There are many firms.

D) Products are differentiated.

A) Firms seek to maximize profits.

B) Profits may be positive in the short run.

C) There are many firms.

D) Products are differentiated.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

8

Individuals in a market who must take the market price as given are:

A) quantity minimizers.

B) quantity takers.

C) price-takers.

D) price searchers.

A) quantity minimizers.

B) quantity takers.

C) price-takers.

D) price searchers.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

9

In a perfectly competitive industry,each firm:

A) is a price maker.

B) produces about half of the total industry output.

C) produces a differentiated product.

D) produces a standardized product.

A) is a price maker.

B) produces about half of the total industry output.

C) produces a differentiated product.

D) produces a standardized product.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

10

In the model of perfect competition:

A) the consumer is at the mercy of powerful firms that can set prices wherever they prefer.

B) individual firms can influence the price,but only slightly.

C) no individual or firm has enough power to affect price.

D) the price is determined by how many years are left in the product's patent.

A) the consumer is at the mercy of powerful firms that can set prices wherever they prefer.

B) individual firms can influence the price,but only slightly.

C) no individual or firm has enough power to affect price.

D) the price is determined by how many years are left in the product's patent.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

11

When a firm cannot affect the market price of the good that it sells,it is said to be a:

A) price-taker.

B) natural monopoly.

C) dominant firm.

D) cartel.

A) price-taker.

B) natural monopoly.

C) dominant firm.

D) cartel.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

12

If an Ontario grape stand operates in a perfectly competitive market,that stand's owner will be a:

A) price maker.

B) price taker.

C) price discriminator.

D) price maximizer.

A) price maker.

B) price taker.

C) price discriminator.

D) price maximizer.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

13

The assumptions of perfect competition imply that:

A) individuals in the market determine the market price.

B) firms in the market accept the market price as given.

C) there will be no new competition due to natural monopolies.

D) the price will be decreasing yearly.

A) individuals in the market determine the market price.

B) firms in the market accept the market price as given.

C) there will be no new competition due to natural monopolies.

D) the price will be decreasing yearly.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

14

Which statement describes a necessary condition for perfect competition?

A) A small number of firms control a large share of the total market.

B) Movement into and out of the market is limited.

C) Firms produce a standardized product.

D) Extensive advertising is used to promote the firm's product.

A) A small number of firms control a large share of the total market.

B) Movement into and out of the market is limited.

C) Firms produce a standardized product.

D) Extensive advertising is used to promote the firm's product.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

15

The perfectly competitive model does NOT assume:

A) a great number of buyers.

B) easy entry to and exit from the market.

C) a standardized product.

D) that firms attempt to maximize their total revenue.

A) a great number of buyers.

B) easy entry to and exit from the market.

C) a standardized product.

D) that firms attempt to maximize their total revenue.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

16

Which statement is NOT characteristic of perfect competition?

A) All firms produce the same standardized product.

B) There are many producers,and each has only a small market share.

C) There are many producers;one firm has a 25% market share,and all of the remaining firms have a market share of less than 2% each.

D) There are no obstacles to entry into or exit from the industry.

A) All firms produce the same standardized product.

B) There are many producers,and each has only a small market share.

C) There are many producers;one firm has a 25% market share,and all of the remaining firms have a market share of less than 2% each.

D) There are no obstacles to entry into or exit from the industry.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

17

For the Alberta beef industry to be classified as perfectly competitive,ranchers in Alberta must have _____ on prices and beef must be a _____ product.

A) no noticeable effect;standardized

B) a huge effect;standardized

C) a huge effect;differentiated

D) no noticeable effect;differentiated

A) no noticeable effect;standardized

B) a huge effect;standardized

C) a huge effect;differentiated

D) no noticeable effect;differentiated

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

18

If a Quebec strawberry wholesaler operates in a perfectly competitive market,that wholesaler will have a _____ share of the market,and consumers will consider her strawberries and her competitors' strawberries to be _____.Therefore,_____ advertising will take place in this market.

A) large;standardized;no

B) small;standardized;little or no

C) small;differentiated;no

D) large;differentiated;extensive

A) large;standardized;no

B) small;standardized;little or no

C) small;differentiated;no

D) large;differentiated;extensive

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

19

If all firms in an industry are price-takers:

A) each firm can sell at the price it wants to charge,provided it is not too different from the prices other firms are charging.

B) each firm takes the market price as given for its output level,recognizing that the price will change if it alters its output significantly.

C) an individual firm cannot alter the market price even if it doubles its output.

D) the market sets the price,and each firm can take it or leave it by setting a different price.

A) each firm can sell at the price it wants to charge,provided it is not too different from the prices other firms are charging.

B) each firm takes the market price as given for its output level,recognizing that the price will change if it alters its output significantly.

C) an individual firm cannot alter the market price even if it doubles its output.

D) the market sets the price,and each firm can take it or leave it by setting a different price.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

20

The market for breakfast cereal contains hundreds of similar products,such as Froot Loops,cornflakes,and Rice Krispies,that are considered to be different products by different buyers.This situation violates the perfect competition assumption of:

A) many buyers and sellers.

B) a standardized product.

C) ease of entry.

D) ease of exit.

A) many buyers and sellers.

B) a standardized product.

C) ease of entry.

D) ease of exit.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

21

When perfect competition prevails,which characteristic of firms are we likely to observe?

A) They erect and maintain barriers to new firms.

B) There are not many of them.

C) They all try to highlight the substantial product differentiation between producers.

D) They are all price-takers.

A) They erect and maintain barriers to new firms.

B) There are not many of them.

C) They all try to highlight the substantial product differentiation between producers.

D) They are all price-takers.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

22

A firm's total output times the price at which it sells that output is _____ revenue.

A) net

B) total

C) average

D) marginal

A) net

B) total

C) average

D) marginal

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

23

Perfectly competitive firms will:

A) maximize total revenue by using the marginal decision rule.

B) increase output up to the point that the marginal revenue of an additional unit of output is greater than the marginal cost.

C) increase output up to the point that the marginal revenue of an additional unit of output is equal to the marginal cost.

D) always attempt to minimize average variable cost.

A) maximize total revenue by using the marginal decision rule.

B) increase output up to the point that the marginal revenue of an additional unit of output is greater than the marginal cost.

C) increase output up to the point that the marginal revenue of an additional unit of output is equal to the marginal cost.

D) always attempt to minimize average variable cost.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

24

In perfect competition:

A) a firm's total revenue is found by multiplying the market price by the firm's quantity of output.

B) the firm's total revenue curve is a downward-sloping line.

C) at any price,the more sold,the higher is a firm's marginal revenue.

D) the firm's total revenue curve is non-linear.

A) a firm's total revenue is found by multiplying the market price by the firm's quantity of output.

B) the firm's total revenue curve is a downward-sloping line.

C) at any price,the more sold,the higher is a firm's marginal revenue.

D) the firm's total revenue curve is non-linear.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

25

If a perfectly competitive firm decreases production from 11 units to 10 units and the market price is $20 per unit,total revenue for 10 units is:

A) -$20.

B) $20.

C) $200.

D) $210.

A) -$20.

B) $20.

C) $200.

D) $210.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

26

_____ almost always take the market price as given;that is,they are considered _____.However,this is often not true of _____.

A) Consumers;quantity minimizers;producers

B) Producers;quantity takers;consumers

C) Consumers and producers;price-takers;firms that produce a differentiated product

D) Producers;price searchers;consumers

A) Consumers;quantity minimizers;producers

B) Producers;quantity takers;consumers

C) Consumers and producers;price-takers;firms that produce a differentiated product

D) Producers;price searchers;consumers

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

27

The competitive model of markets does NOT assume:

A) a large number of buyers.

B) easy entry into and exit from the market.

C) a standardized product.

D) patents and copyrights that serve as barriers to entry into the industry.

A) a large number of buyers.

B) easy entry into and exit from the market.

C) a standardized product.

D) patents and copyrights that serve as barriers to entry into the industry.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

28

Marginal revenue is a firm's:

A) ratio of profit to quantity.

B) ratio of average revenue to quantity.

C) price per unit times the number of units sold.

D) increase in total revenue when it sells an additional unit of output.

A) ratio of profit to quantity.

B) ratio of average revenue to quantity.

C) price per unit times the number of units sold.

D) increase in total revenue when it sells an additional unit of output.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

29

A perfectly competitive firm will maximize profits when:

A) marginal revenue equals marginal cost.

B) marginal revenue is lower than average variable cost.

C) price is lower than marginal cost.

D) price is higher than marginal cost.

A) marginal revenue equals marginal cost.

B) marginal revenue is lower than average variable cost.

C) price is lower than marginal cost.

D) price is higher than marginal cost.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

30

Total revenue is a firm's:

A) change in revenue resulting from a unit change in output.

B) ratio of revenue to quantity.

C) difference between revenue and cost.

D) total output times the price of that output.

A) change in revenue resulting from a unit change in output.

B) ratio of revenue to quantity.

C) difference between revenue and cost.

D) total output times the price of that output.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

31

The marginal revenue received by a firm in a perfectly competitive market:

A) is greater than the market price.

B) is less than the market price.

C) is equal to its average revenue.

D) increases with the quantity of output sold.

A) is greater than the market price.

B) is less than the market price.

C) is equal to its average revenue.

D) increases with the quantity of output sold.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

32

Marginal revenue:

A) is the slope of the average revenue curve.

B) equals the market price in perfect competition.

C) is the change in quantity divided by the change in total revenue.

D) is the price divided by the change in quantity.

A) is the slope of the average revenue curve.

B) equals the market price in perfect competition.

C) is the change in quantity divided by the change in total revenue.

D) is the price divided by the change in quantity.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

33

People in the eastern part of Beirut are prevented by border guards from travelling to the western part of Beirut to shop for or sell food.This situation violates the perfect competition assumption of:

A) price-setting behaviour.

B) a small number of buyers and sellers.

C) differentiated goods.

D) ease of entry and exit.

A) price-setting behaviour.

B) a small number of buyers and sellers.

C) differentiated goods.

D) ease of entry and exit.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

34

The demand curve faced by a single perfectly competitive firm is:

A) perfectly inelastic.

B) perfectly elastic.

C) downward sloping.

D) relatively but not perfectly elastic.

A) perfectly inelastic.

B) perfectly elastic.

C) downward sloping.

D) relatively but not perfectly elastic.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

35

If a perfectly competitive firm increases production from 10 units to 11 units and the market price is $20 per unit,total revenue for 11 units is:

A) $10.

B) $20.

C) $200.

D) $220.

A) $10.

B) $20.

C) $200.

D) $220.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

36

An assumption of the model of perfect competition is:

A) identical goods.

B) difficult entry and exit.

C) few buyers and sellers.

D) cooperation and interdependence between sellers.

A) identical goods.

B) difficult entry and exit.

C) few buyers and sellers.

D) cooperation and interdependence between sellers.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

37

For a perfectly competitive firm,marginal revenue:

A) is less than price.

B) is greater than price.

C) decreases as the firm increases output.

D) is equal to price.

A) is less than price.

B) is greater than price.

C) decreases as the firm increases output.

D) is equal to price.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

38

In a perfectly competitive industry,the market demand curve is usually:

A) perfectly inelastic.

B) perfectly elastic.

C) downward sloping.

D) relatively elastic.

A) perfectly inelastic.

B) perfectly elastic.

C) downward sloping.

D) relatively elastic.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

39

The difference between total revenue and total cost is:

A) economic profit or loss.

B) nominal revenue.

C) average revenue.

D) marginal revenue.

A) economic profit or loss.

B) nominal revenue.

C) average revenue.

D) marginal revenue.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

40

If a perfectly competitive gardening shop sells 30 evergreen bushes at $10 per bush,its marginal revenue is:

A) $10.

B) more than $10.

C) less than $10.

D) $300.

A) $10.

B) more than $10.

C) less than $10.

D) $300.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

41

For a firm producing at any level of output GREATER than the most profitable one,a reduction in output decreases total revenue _____ total cost.

A) by less than it decreases

B) by more than it decreases

C) by the same amount as it decreases

D) but not

A) by less than it decreases

B) by more than it decreases

C) by the same amount as it decreases

D) but not

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

42

Zoe's Bakery operates in a perfectly competitive industry and has standard cost curves.The variable costs at Zoe's Bakery increase,so all of the cost curves (except fixed cost)shift upward.The demand for Zoe's pastries does not change,nor does the firm shut down.To maximize profits after the variable cost increase,Zoe's Bakery will _____ its price and _____ its level of production.

A) raise;increase

B) decrease;increase

C) raise;decrease

D) do nothing to;decrease

A) raise;increase

B) decrease;increase

C) raise;decrease

D) do nothing to;decrease

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

43

If a perfectly competitive firm is producing a quantity where MC < MR,then profit:

A) is maximized.

B) can be increased by increasing production.

C) can be increased by decreasing production.

D) can be increased by decreasing the price.

A) is maximized.

B) can be increased by increasing production.

C) can be increased by decreasing production.

D) can be increased by decreasing the price.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

44

In perfect competition:

A) price and average variable cost are the same.

B) price and marginal revenue are the same.

C) price and total revenue are the same.

D) total revenue and total variable cost are the same.

A) price and average variable cost are the same.

B) price and marginal revenue are the same.

C) price and total revenue are the same.

D) total revenue and total variable cost are the same.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

45

If a perfectly competitive firm is producing a quantity where MC > MR,then profit:

A) is maximized.

B) can be increased by increasing production.

C) can be increased by decreasing production.

D) can be increased by decreasing the price.

A) is maximized.

B) can be increased by increasing production.

C) can be increased by decreasing production.

D) can be increased by decreasing the price.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

46

The equilibrium price of a guidebook is $35 in the perfectly competitive guidebook industry.Our firm produces 10 000 guidebooks for an average total cost of $38,a marginal cost of $30,and an average variable cost of $30.Our firm,in the short run,should:

A) raise the price of guidebooks because the firm is losing money.

B) keep output the same because the firm is producing at a minimum average variable cost.

C) produce more guidebooks because the next guidebook produced will increase profit by $5.

D) shut down because the firm is losing money.

A) raise the price of guidebooks because the firm is losing money.

B) keep output the same because the firm is producing at a minimum average variable cost.

C) produce more guidebooks because the next guidebook produced will increase profit by $5.

D) shut down because the firm is losing money.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

47

If a firm in perfect competition sells 10 units of output at $5 per unit,its marginal revenue is:

A) $5.

B) more than $5 but less than $50.

C) $50.

D) $250.

A) $5.

B) more than $5 but less than $50.

C) $50.

D) $250.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

48

A perfectly competitive firm maximizes profit in the short run by producing the quantity at which:

A) TR = TC.

B) MR = MC.

C) Q × (P - ATC)= 0.

D) P < AVC.

A) TR = TC.

B) MR = MC.

C) Q × (P - ATC)= 0.

D) P < AVC.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

49

If a perfectly competitive firm sells 300 units of output at $1 per unit,its marginal revenue is:

A) less than $1.

B) $1.

C) more than $1 but less than $300.

D) $300.

A) less than $1.

B) $1.

C) more than $1 but less than $300.

D) $300.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

50

The marginal revenue received by a firm in a perfectly competitive market:

A) is unrelated to the market price.

B) is less than the market price.

C) is greater than the market price.

D) is the change in total revenue divided by the change in output.

A) is unrelated to the market price.

B) is less than the market price.

C) is greater than the market price.

D) is the change in total revenue divided by the change in output.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

51

Marginal revenue is a firm's:

A) ratio of the change in total revenue to the change in output.

B) ratio of average revenue to total revenue.

C) profit per unit times the number of units sold.

D) increase in profit when it sells an additional unit of output.

A) ratio of the change in total revenue to the change in output.

B) ratio of average revenue to total revenue.

C) profit per unit times the number of units sold.

D) increase in profit when it sells an additional unit of output.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

52

The slope of the total cost curve is:

A) marginal cost.

B) marginal revenue.

C) constant under perfect competition.

D) always negative.

A) marginal cost.

B) marginal revenue.

C) constant under perfect competition.

D) always negative.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

53

The slope of the total revenue curve is:

A) marginal cost.

B) net revenue.

C) equal to marginal revenue and is constant under perfect competition.

D) equal to marginal revenue and varies under perfect competition.

A) marginal cost.

B) net revenue.

C) equal to marginal revenue and is constant under perfect competition.

D) equal to marginal revenue and varies under perfect competition.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

54

If a perfectly competitive firm is producing a quantity where MC = MR,then profit:

A) is maximized.

B) can be increased by increasing production.

C) can be increased by decreasing production.

D) can be increased by decreasing the price.

A) is maximized.

B) can be increased by increasing production.

C) can be increased by decreasing production.

D) can be increased by decreasing the price.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

55

If a perfectly competitive firm sells 10 units of output at $30 per unit,its marginal revenue is:

A) $10.

B) $30.

C) more than $30.

D) $300.

A) $10.

B) $30.

C) more than $30.

D) $300.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

56

For a firm producing at any level of output LOWER than the most profitable one,an increase in output adds:

A) more to total cost than to total revenue.

B) more to total revenue than to total cost.

C) the same amount to total revenue as to total cost.

D) to total revenue but not to total cost.

A) more to total cost than to total revenue.

B) more to total revenue than to total cost.

C) the same amount to total revenue as to total cost.

D) to total revenue but not to total cost.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

57

The price received by a firm in a perfectly competitive market:

A) is equal to the market price.

B) is less than the market price.

C) is greater than the market price.

D) decreases with the quantity of output sold by the firm.

A) is equal to the market price.

B) is less than the market price.

C) is greater than the market price.

D) decreases with the quantity of output sold by the firm.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

58

The profit-maximizing level of output for a perfectly competitive firm in the short run occurs where _____ equals _____.

A) marginal cost;price

B) marginal revenue;price

C) total revenue;total cost

D) average revenue;average total cost

A) marginal cost;price

B) marginal revenue;price

C) total revenue;total cost

D) average revenue;average total cost

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

59

For a firm in a perfectly competitive market,_____ revenue equals _____.

A) marginal;total revenue

B) marginal;market price

C) net;price

D) net;marginal revenue

A) marginal;total revenue

B) marginal;market price

C) net;price

D) net;marginal revenue

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

60

Price in a perfectly competitive industry:

A) is determined by each firm,depending on its costs of production.

B) is always equal to marginal revenue for the firm.

C) must be greater than average total cost or the firm will shut down in the short run.

D) is indeterminate in the short run.

A) is determined by each firm,depending on its costs of production.

B) is always equal to marginal revenue for the firm.

C) must be greater than average total cost or the firm will shut down in the short run.

D) is indeterminate in the short run.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

61

Suppose a perfectly competitive firm can increase its profits by increasing its output.Then it must be true that the firm's _____ exceeds its _____.

A) marginal revenue;marginal cost

B) price;average total cost but is less than marginal cost

C) marginal cost;marginal revenue

D) price;marginal revenue

A) marginal revenue;marginal cost

B) price;average total cost but is less than marginal cost

C) marginal cost;marginal revenue

D) price;marginal revenue

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

62

In the short run,if P = ATC,a perfectly competitive firm:

A) produces output and earns zero economic profit.

B) produces output and earns an economic profit.

C) produces output and incurs an economic loss.

D) does not produce output and incurs an economic loss.

A) produces output and earns zero economic profit.

B) produces output and earns an economic profit.

C) produces output and incurs an economic loss.

D) does not produce output and incurs an economic loss.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

63

Zoe's Bakery operates in a perfectly competitive industry.When the market price of iced cupcakes is $5,the profit-maximizing output level is 150 cupcakes.Her average total cost is $4,and her average variable cost is $3.Zoe's marginal cost is _____,and her short-run profit is _____.

A) $5;$150

B) $5;$300

C) $1;$150

D) $1;$300

A) $5;$150

B) $5;$300

C) $1;$150

D) $1;$300

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

64

In the short run,if P > ATC,a perfectly competitive firm:

A) produces output and earns zero economic profit.

B) produces output and earns an economic profit.

C) produces output and incurs an economic loss.

D) does not produce output and earns economic profit.

A) produces output and earns zero economic profit.

B) produces output and earns an economic profit.

C) produces output and incurs an economic loss.

D) does not produce output and earns economic profit.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

65

In perfectly competitive markets,if the price is _____,the firm will _____.

A) greater than ATC;make an economic profit

B) greater than the minimum ATC;break even

C) less than ATC;make an economic profit

D) less than ATC;break even

A) greater than ATC;make an economic profit

B) greater than the minimum ATC;break even

C) less than ATC;make an economic profit

D) less than ATC;break even

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

66

In the short run,a perfectly competitive firm produces output and breaks even if the firm produces the quantity at which:

A) P < ATC.

B) P = ATC.

C) P > ATC.

D) P = (TR/Q + TC/Q)× Q.

A) P < ATC.

B) P = ATC.

C) P > ATC.

D) P = (TR/Q + TC/Q)× Q.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

67

If a perfectly competitive firm is producing a quantity where P < MC,then profit:

A) is maximized.

B) can be increased by decreasing the price.

C) can be increased by increasing production.

D) can be increased by decreasing production.

A) is maximized.

B) can be increased by decreasing the price.

C) can be increased by increasing production.

D) can be increased by decreasing production.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

68

In the short run,a perfectly competitive firm produces output and earns ZERO economic profit if:

A) P < ATC.

B) P = ATC.

C) P < MC.

D) P > ATC.

A) P < ATC.

B) P = ATC.

C) P < MC.

D) P > ATC.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

69

Consider a perfectly competitive firm in the short run.Assume that the firm produces the profit-maximizing output and earns economic profits.Which statement is definitely FALSE?

A) Price is equal to marginal cost.

B) Price is equal to marginal revenue.

C) Price is equal to average total cost.

D) Marginal cost is greater than average total cost.

A) Price is equal to marginal cost.

B) Price is equal to marginal revenue.

C) Price is equal to average total cost.

D) Marginal cost is greater than average total cost.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

70

A perfectly competitive firm will earn a profit in the short run when it produces the profit-maximizing quantity of output and the price is:

A) greater than marginal cost.

B) less than marginal cost.

C) less than average variable cost.

D) greater than average total cost.

A) greater than marginal cost.

B) less than marginal cost.

C) less than average variable cost.

D) greater than average total cost.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

71

If the price is greater than average total cost at the profit-maximizing quantity of output in the short run,a perfectly competitive firm will:

A) produce at a loss.

B) produce at a profit.

C) shut down production.

D) produce more than the profit-maximizing quantity.

A) produce at a loss.

B) produce at a profit.

C) shut down production.

D) produce more than the profit-maximizing quantity.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

72

If a perfectly competitive firm is producing a quantity where P > MC,then the firm can increase profit by:

A) making no change in output or price because it is already maximizing profit.

B) increasing the price.

C) decreasing the price.

D) increasing production.

A) making no change in output or price because it is already maximizing profit.

B) increasing the price.

C) decreasing the price.

D) increasing production.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

73

Which statement is TRUE?

A) Profit per unit is price minus MC.

B) Total economic profit is per-unit profit times quantity.

C) If price is less than ATC,the firm will break even in the short run.

D) If price is less than marginal cost,the perfectly competitive firm should raise the price and increase output.

A) Profit per unit is price minus MC.

B) Total economic profit is per-unit profit times quantity.

C) If price is less than ATC,the firm will break even in the short run.

D) If price is less than marginal cost,the perfectly competitive firm should raise the price and increase output.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

74

A perfectly competitive firm will earn a profit and will continue producing the profit-maximizing quantity of output in the short run if the price is:

A) less than average fixed cost.

B) less than marginal cost.

C) greater than average variable cost but less than average total cost.

D) greater than average total cost.

A) less than average fixed cost.

B) less than marginal cost.

C) greater than average variable cost but less than average total cost.

D) greater than average total cost.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

75

A competitive firm operating in the short run is producing the output level at which ATC is at a minimum.If ATC = $8 and MR = $9,to maximize profits (or minimize losses),this firm should:

A) increase output.

B) reduce output.

C) increase price.

D) do nothing,because it is already maximizing profits.

A) increase output.

B) reduce output.

C) increase price.

D) do nothing,because it is already maximizing profits.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

76

If the price is greater than average total cost at the profit-maximizing quantity of output in the short run,a perfectly competitive firm will:

A) continue to produce at a loss.

B) produce at a profit.

C) shut down production.

D) reduce its fixed costs.

A) continue to produce at a loss.

B) produce at a profit.

C) shut down production.

D) reduce its fixed costs.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

77

Use the following to answer question 64:

(Figure: Total Revenue and Total Cost)Use Figure: Total Revenue and Total Cost.The MOST profitable level of output occurs at quantity:

A) F.

B) K.

C) L.

D) M.

(Figure: Total Revenue and Total Cost)Use Figure: Total Revenue and Total Cost.The MOST profitable level of output occurs at quantity:

A) F.

B) K.

C) L.

D) M.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

78

In the short run,a perfectly competitive firm produces output and earns an economic profit if:

A) P > ATC.

B) P = ATC.

C) P < MC.

D) P < ATC.

A) P > ATC.

B) P = ATC.

C) P < MC.

D) P < ATC.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

79

For a perfectly competitive firm in the short run,if the firm produces the quantity at which _____,the firm _____.

A) P > ATC;is profitable

B) P < ATC;breaks even

C) P = ATC;incurs a loss

D) P < ATC;is profitable

A) P > ATC;is profitable

B) P < ATC;breaks even

C) P = ATC;incurs a loss

D) P < ATC;is profitable

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

80

If a perfectly competitive firm is producing a quantity where P = MC,then profit:

A) is maximized.

B) can be increased by decreasing the quantity.

C) can be increased by decreasing the price.

D) can be increased by increasing production.

A) is maximized.

B) can be increased by decreasing the quantity.

C) can be increased by decreasing the price.

D) can be increased by increasing production.

Unlock Deck

Unlock for access to all 341 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 341 flashcards in this deck.